VODPF - Vodafone: Should You Buy The Dip?

2023-06-15 11:15:00 ET

Summary

- Vodafone has reported weak results in recent years and its growth prospects aren't impressive.

- It has announced a merger of its U.K. operations with its competitor Three, creating the largest mobile operator in the country.

- This could be an important catalyst for a re-rating of its shares.

Vodafone ( OTCPK:VODPF ) has relatively weak growth prospects and its track record isn’t impressive, but this seems to be already reflected in its discounted valuation and the recent agreement to merge its U.K. operations may be the required catalyst for a higher share price going forward.

Background

As I’ve analyzed in a previous article , Vodafone’s investment case is highly geared to its high-dividend yield given that its business growth prospects are somewhat muted and its recent track record is not impressive.

The company has made some efforts to improve its business profile and monetize assets, such as the listing and subsequent sale of Vantage Towers ( OTCPK:VTAGY ), but its share price performance in recent months has been quite weak and has reached new all-time lows. Indeed, since my last article, Vodafone’s share price has declined by close to 15% including dividends, a much worse performance than the S&P 500 index during the same period.

Article performance (Seeking Alpha)

This weak performance is justified by Vodafone’s relatively weak earnings recently and a new business plan that was not well received by investors. However, Vodafone has announced yesterday an agreement with CK Hutchison Holdings Limited ( OTCPK:CKHUY ) to combine the company’s operations in the U.K., which may be the necessary catalyst for improved investor sentiment towards Vodafone.

Recent Developments

Since my last article, Vodafone has reported annual earnings related to fiscal year (FY) 2023 , and its new CEO presented a turnaround plan for the next few years.

In the last FY, Vodafone’s revenues amounted to €45.7 billion, an increase of only 0.3% YoY. This relatively weak performance was justified by commercial underperformance in Germany and other European countries (such as Spain and Italy), while Africa had a better performance but was not enough to offset weaker performance elsewhere.

Vodafone’s weak performance in Germany is quite worrisome because is the company’s largest market, representing some 36% of total EBITDAaL, and customer losses had a negative impact on service revenues (-1.6% YoY) and profitability (EBITDAaL -6.1% YoY). Furthermore, Vodafone had to cut prices to retain customers, which led to steeper revenue declines in Q3 and Q4, not boding well for revenue growth over the coming quarters.

Vodafone’s overall EBITDAaL was €14.7 billion in FY 2023, a decline of 1.3% YoY and below the company’s guidance, justified by higher energy costs, the inflationary environment, and currency headwinds. This led to a margin of 32.1% in the year, the lowest over the past four fiscal years.

EBITDA (Vodafone)

Recognizing the Vodafone’s performance over the past few years has not been good enough, the company’s new CEO (which was appointed last January) presented some initiatives to improve Vodafone’s performance over the next three years, focusing the business on customers and reducing business complexity.

Vodafone’s service revenues have been quite flat to negative over the past few years, a trend that is justified to some extent by low customer satisfaction and also fierce competition. To improve its operational performance, Vodafone aims to increase customer focus and commercial agility, reduce business complexity, and sell underperforming units. This will lead to some 11,000 job cuts over the next three years and to the disposal of some units, of which the Spanish unit seems to be the first on sale.

However, this seems to be to a large extent a vague plan and don’t have clear targets to measure execution, thus investors reacted badly to this announcement pushing its shares to new all-time lows.

This also reflects, in my opinion, the fact that Vodafone operates in a mature industry in countries with relatively weak growth prospects (with the exception of Africa), thus a turnaround is not easy to achieve and may take some time.

On the other hand, its recent announcement of an agreement with CK Hutchison to merger Vodafone’s U.K with CK’s Three U.K. unit was better received, as its strengthens the company’s position in an important market (weight of about 9% on EBITDA in the last FY).

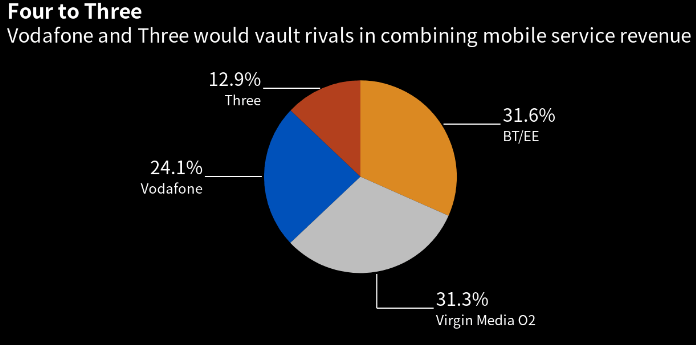

This deal will create the largest mobile operator in the country, and if approved by regulators, reduce the market operators from four to three. Currently, Vodafone is the third largest mobile operator in the U.K., while Three is the fourth operator, which combined would have a market share of about 37% as shown in the next graph.

{kind=link}

This business combination will integrate both networks into a single entity, plus they plan to invest some £11 billion over the next ten years to have the best 5G network in the country. This is expected to improve Vodafone’s competitiveness in the market, achieve cost synergies of about £700 million by year five following the merger, and potentially improve its profitability that has been among the weakest in the U.K.

From a financial standpoint, instead of contributing with cash, both companies will transfer debt to the MergeCo, to achieve a 51% stake for Vodafone and 49% for CK Hutchison. Three years after completion of the transaction, Vodafone has a call option to acquire CK’s stake in the MergeCo, if it reaches a valuation of at least £16.5 billion including debt.

Even though the U.K. is not the largest market within Vodafone’s group, this is a step in the right direction to improve the group’s fundamentals, which together with the disposal of some of its weakest units from a profitability perspective, is important to have better investor sentiment and achieve higher shareholder returns in the future.

Reflecting weak market perspective towards its business in the next few years, Vodafone is currently trading at only 9.7x forward earnings, at a significant discount to its own historical average over the past five years of 14.9x. While Vodafone’s growth prospects aren’t impressive and its recent track record has been weak, this valuation seems to be too low and the recent agreement to combine its U.K. operations with its competitor Three may be a catalyst for a potential re-rating over the coming months.

Conclusion

While Vodafone is a mature company and has relatively weak growth prospects, its depressed valuation and high-dividend yield are strong supports for positive shareholder returns over the next three to five years. This means that a turnaround may take some time to bear fruit, but for investors willing to invest for some years the returns may be quite good, both from dividends and share price appreciation.

For further details see:

Vodafone: Should You Buy The Dip?