VODPF - Vodafone: Waiting For Disposal To Re-Rating

2023-12-19 05:09:00 ET

Summary

- Following the Spanish deal, we believe Vodafone will consider options for consolidating the Italian market.

- Net debt is slightly higher on lower Vantage proceeds.

- Vodafone is evolving with guidance confirmed. Disposals are vital catalysts in the equity story. Our buy rating is then confirmed.

This morning, there was breaking news on the European Telco industry - Iliad's founder, Xavier Niel, is doing it again. Two years from its first approach, Iliad is stepping forward for Vodafone Italia. The French telecommunications group has presented to the British giant a proposal to merge their Italian activities with a NewCo aim to develop " an attractive market offering, based on innovation, growth, and an unparalleled customer experience ." As a reminder, Vodafone ( VOD , VODPF ) had already rejected a €11.25 billion offer for its Italian division, arguing that the offer was not in the interests of its shareholders. However, Vodafone CEO Margherita Della Valle, who took over the role in April 2023, is facing challenging times, with a declining market share penetration and pressure to sell or merge underperforming group divisions. Our buy rating was backed by 1) higher interest from strategic buyers such as Iliad owner coupled with portfolio optimization , 2) a generous dividend per share payment backed by an FCF generation, and 3) higher cost-saving initiatives. To support our buy rating, we also reported how Xavier Niel (Iliad owner) acquired a 2.5% equity stake in Vodafone, and we also commented on M&A optionality in the UK.

Vodafone - Iliad: A potential deal is coming

Before commenting on the numbers here at the Lab, this news is positive for Vodafone and the telecommunications sector, considering the European market implications for consolidation. This implies that Iliad still believes in market restructuring through consolidation at a time when the EU Antitrust has lit up the Spain telco consolidation. Before the EU decision, Iliad's announcements suggested that the French group was confident that the Antitrust requests would be limited. However, will Vodafone want to leave Italy? If it does so, we believe it will benefit from a decrease in the holding discount at which the shares trade, a discount which currently affects its sum-of-the-part valuation.

In more detail, the enterprise value proposed is equal to €10.45 billion. Vodafone will receive €6.5 billion in cash and €2 billion in shareholder financing. The equity value of Vodafone's 50% stake in the new company is valued at €1.95 billion. Based on the estimated EBITDA after the lease for Vodafone, 2024 EBITDA is set at €1.34 billion with an EV/EBITDA after lease multiple of 7.8x, higher than the multiple of 7.1x offered by Iliad last February 2022. The combined entity will generate a turnover of approximately €5.8 billion and an EBITDA of €1.6 billion after the lease. Furthermore, according to the Iliad press release, the combined entity will benefit from annual synergies expected to exceed €600 million in OPEX plus CAPEX.

Among other things, Iliad will also have a call option on Vodafone's stake in the new company with the right to acquire 10% of the share capital each year at a price per share equal to the equity value at closing . Suppose it fully exercises the call options, paving the way for complete company control. In that case, this will generate a further €1.95 billion in liquidity for Vodafone, which, however, has the final say.

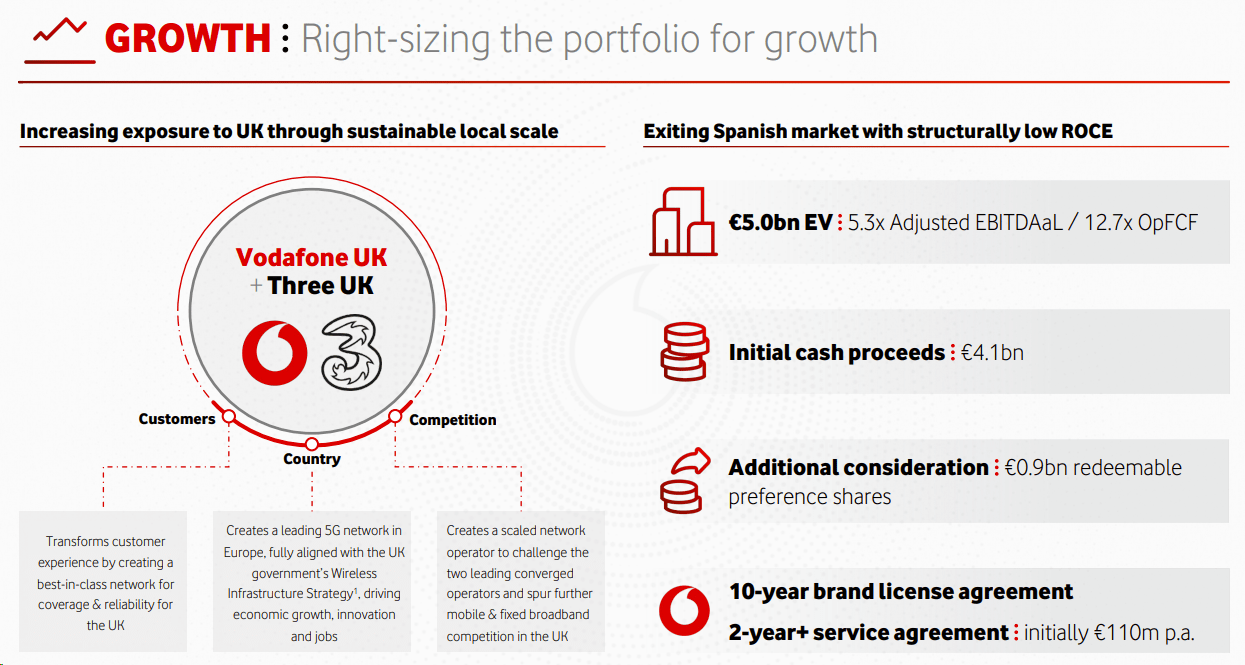

Based on the announced terms, we estimate the proposed deal would help Vodafone lighten its net debt to EBITDA ratio by 0.2-0.3x from the current 2.8x. Vodafone recently agreed to sell its Spanish operations to Zegona Communications for €5 billion. These latest transactions and Iliad rumors supported our investment thesis on Vodafone's unappreciated asset portfolio.

Vodafone's new CEO already made significant progress in the company's restructuring process. She secured a scale deal in the UK with the Hutch merger. The Germany transaction is moving on, and there are Italian options with Swisscom.

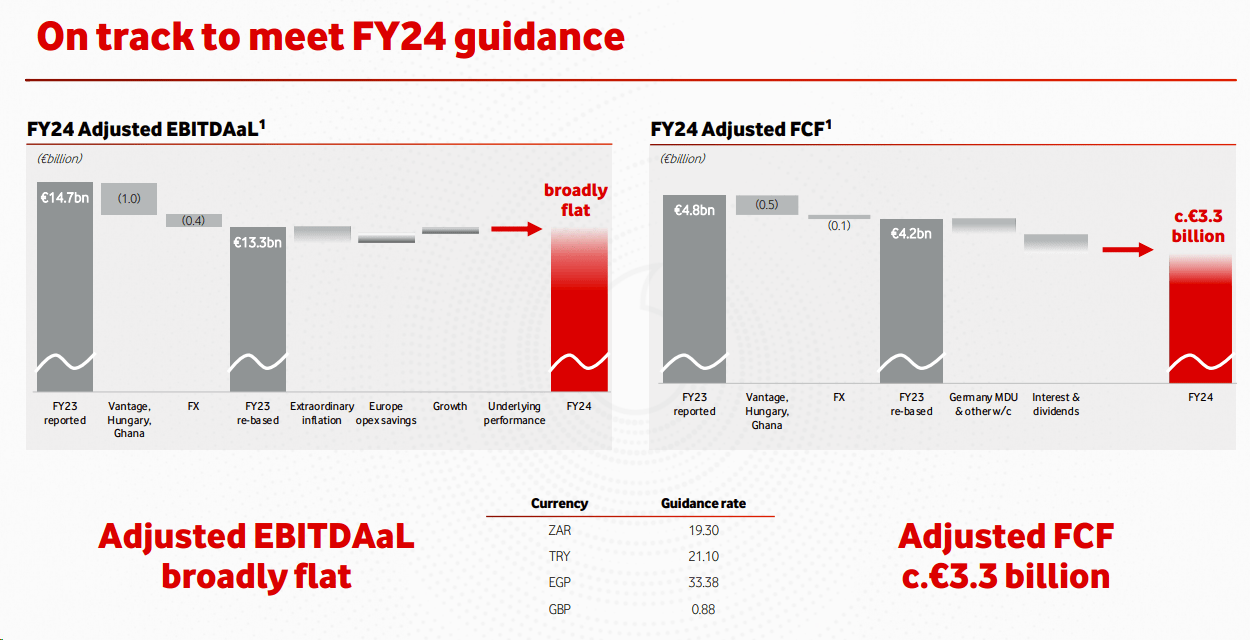

Where the scale is not a viable proposition, the company is maximizing its asset portfolio, as happened in Spain. Vodafone ROCE is the CEO's priority and should support a company re-rating in the medium-term horizon. Looking back, the company delivered revenues and EBITDA slightly below our estimates. In H1, European EBITDA after the lease was weaker due to cost phasing and energy comps; however, these negative detractors should unwind in H2. In number, there was a €300 million energy drag impact in H1, but we forecast a relief of approximately €200 million compared to H1. Beyond energy, according to the management team, UK MVNO will return to EBITDA growth, and German commercial volume trends will pick up. Germany will face initial multi-dwelling unit headwinds, and we estimate €100 million more marketing investment.

{kind=link}

The company's FCF was weak, and EBITDA was below numbers in Spain, the UK, and Italy, with Vodafone's central function offsetting slightly. In the analyst call, the CEO stressed EBITDA growth ambition for 2025. Still, in our guidance, excluding disposals, we model a +1% organic growth at constant FX with operational uncertainties in Italy and Germany. Despite that, Vodafone reiterated its yearly guidance.

{kind=link}

Valuation

Our team now projects sales of €45.7 and €43.9 billion in 2023 and 2024, respectively. Our adjusted EBITDA reached €14.6 and €13.1 billion in the same year. The lower numbers are mainly due to disposal already accounted for. We are forecasting an unchanged dividend per share based on cash disposal and FCF generation, and even if returns are not optimal, a 9% FCF yield cannot go unnoticed. In addition, the Vodafone balance sheet is solid, with an 11.7-year maturity and a fixed interest rate of approximately 2.5%. Moreover, the company has limited refinance in the next 1.5 years. Our net debt evolution moves slightly higher on lower Vantage proceeds.

Vodafone Net Debt progression

Looking at the Spanish disposal and Iliad offers, on average, the past EV/EBITDA transactions were between 5-11x. Valuing the red giant with a 5x multiple with an EBITDA projection of €13.1 billion in 2024 (at the bottom line of the implied M&A guidance), we arrived at €65.5 billion enterprise value, and with a €33.4 billion debt, our equity value is set at €32.1 billion vs. a current market cap of €21 billion. Therefore, we confirm our Vodafone buy rating target, lowering our overweight from £130 to £100 per share. Downside risks are included in our initiation of coverage . In addition, we include 1) pressure on hard-currency earnings with potential further FCF dilution, 2) Germany's lower net adds, 3) lower than expected TV retention rate (35% vs. 65%), 4) execution risks in the restructuring process, and 5) a lower dividend per share given the current disposals.

For further details see:

Vodafone: Waiting For Disposal To Re-Rating