VOE - VOE: Mid-Cap Value Exposure Flat Compounding Effect Without Momentum

2023-11-10 07:04:26 ET

Summary

- Markets flipped after the Fed's decision to pause rate hikes, leading to a snap-back rally in high beta and tech names.

- The Vanguard Mid-Cap Value Index Fund ETF has not performed as well as other value funds and has seen weak fund flows in H2 '23.

- Starting valuations and technical factors suggest a neutral outlook for VOE, with more selective opportunities available elsewhere.

Investment briefing

Markets flipped in almost vertical fashion after the Fed's decision to pause its rates hiking cycle in the November FOMC meeting. This was the 2nd time the committee decided to pause tightening financial conditions since July. Investors were quick to change their risk appetite following the announcement, shifting the character of U.S. markets, and some global indices.

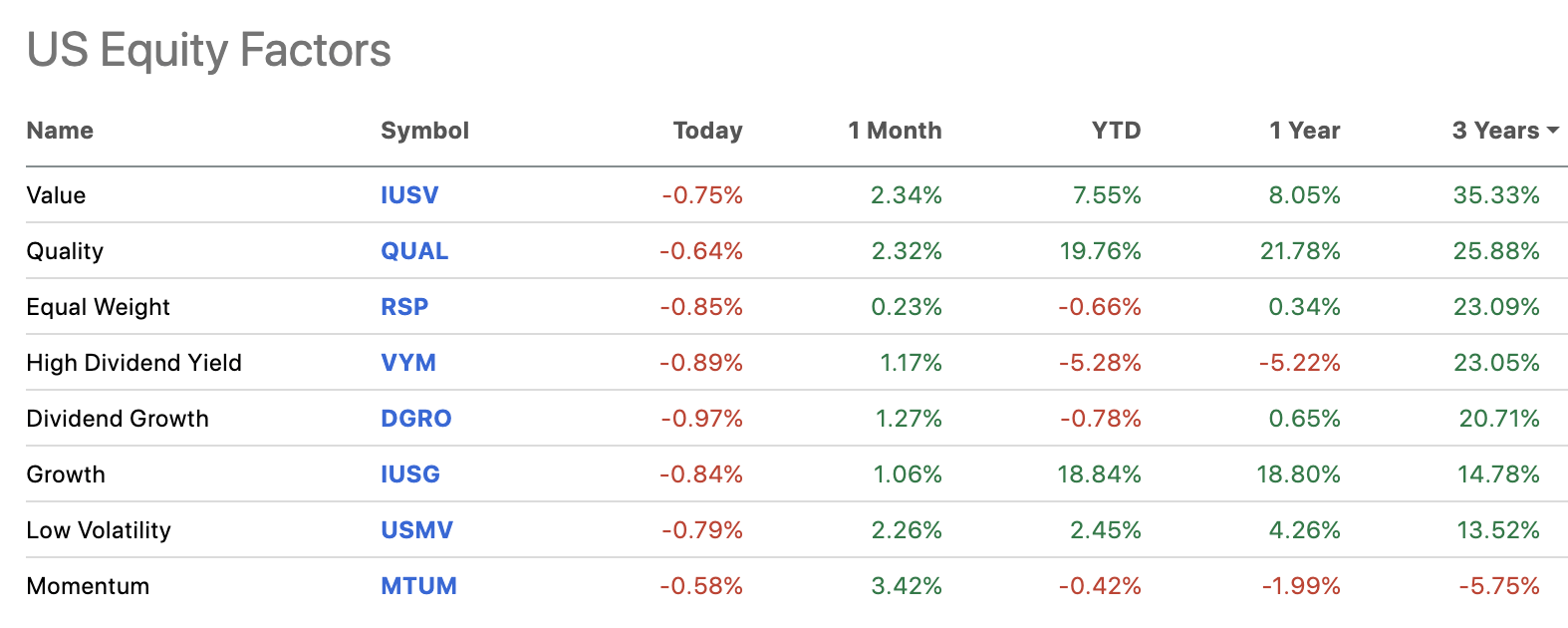

The snap-back rally was led by high beta and tech names (there is overlap between the two) but most equity factors + sectors have caught the bid in November, with markets pricing in a period of potential better business in the coming 12-24 months. Critically, the reversal was short-lived in many instances. This again opened the debate of "value vs. growth", with the former demonstrating superior performance on a 3 year basis, but lagging this YTD (Figure 1). However, one must acknowledge much of this dislocation is driven by the performance of the "magnificent 7" companies leading the benchmark indices.

So the prevailing questions are 1) where to from here, and 2) how likely are investors to lift the bid on value factors moving forward?

Figure 1. U.S. equity factors, ranked by 3-year performance

{kind=link}

The other factor in contention is size. Large caps and mid caps have often outperformed small cap peers in times of turbulence. But the mid cap space is still full of plenty of bargains. It's just whether these reflect statistical discounts, or, whether the market has got it right in these instances.

For investors seeking diversified exposure to both value factors and mid-cap equities, The Vanguard Mid-Cap Value Index Fund ETF Shares (VOE) is a holding to consider in the equity risk budget.

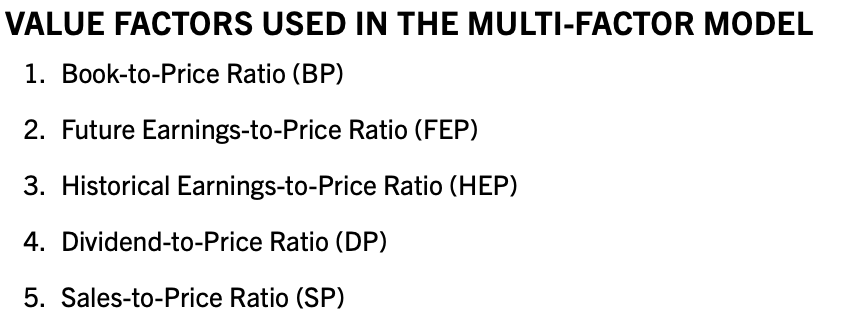

The fund tracks the CRSP US Mid Cap Value Index using a replication methodology to match this benchmark as closely as possible. According to CRSP, the index is constructed using a composite of multiples/ratios using a " composite score a rank value " to approximate selections and weightings. These are seen in Figure 2.

Figure 2.

{kind=link}

The replication methodology and tight exposure to a composite of value factors has several benefits, not in the least capturing risk premia against the current market cycle.

Despite these facts, VOE hasn't performed as well as other value funds (both mid cap and mixed blend of size) in recent times, given certain risks . Namely:

- 1-year and 3-year tracking error of 9.8% and 8.6% respectively, placing it in the 20th and c.50th percentiles vs. all ETFs respectively,

- Annualized volatility of 15.7% at the time of writing,

- Turnover of around 18%, indicating capital is rotated out of performing names into under-performing names with more 'attractive' ratios in the composite.

As a result, the fund has lagged comparable names, such as IUSV ( IUSV ) which invests in market capitalizations' of all sizes.

Figure 3.

{kind=link}

Figure 3a. VOE long-term price evolution, 2021-date

{kind=link}

Still, VOE is highly diversified and has exposure to low-beta sectors which may reduce drawdowns and help risk-adjusted returns for equity portfolios. It has 197 holdings split across a number of sectors, with financials (18%) and industrials (14.5%) taking the most weight, and technology and consumer cyclicals holding 8-8.5% of the portfolio respectively. The top 10 holdings make up around 12.4% of the portfolio's total weight.

Dividends , paid quarterly, amount to $3.38/share in the TTM, yielding 2.5% as I write. The fund has nearly $25Bn in AUM, charging an expense fee of just 7bps on this, placing it in the 85th percentile vs. all ETFs.

The yield on cost and diversification principles employed by VOE don't overcome the fact it is lagging comparable peers, especially on the growth side of the book. With investors igniting a new flame of risk appetite in U.S. markets, my judgement is that VOE will continue to lag its counterparts, and that investors may be better served in searching for more selective opportunities elsewhere.

In that vein, my recommendations across all 3 investment horizons are as follows:

- Short term (coming, 12 months) - Neutral; starting valuations aren't expensive but aren't necessarily cheap either at 15x earnings and the 2.5% dividend yield. The fund's momentum factors are absent. Momentum will be a critical factor for equity prices over the coming 12 months in my view.

- Medium term (1-3 years) - Neutral; Whilst I am constructive on the mid-term outlook for U.S. equities on aggregate, those names with exceptional growth economics are better positioned to catch the bid in my opinion. This places a dampener on mid-cap value propositions such as VOE.

- Long-term (3 years+) - Neutral; Similar to the above. Here it becomes more an argument of opportunity cost vs. more selective names with more attractive economics that make up the fund's constituents.

Net-net, given the culmination of factors discussed in this report, I rate VOE a hold.

Talking points

- Investors still bidding U.S. equities higher based on fundamentals

As seen in Figure 4, U.S. equities are at all-time highs vs. global peers in terms of stock returns. Since 2013, this gap has widened at an increasing rate. One might question the validity of this moving forward but the facts are clear based on economics.

For one, U.S. GDP pulled in at 4.9% annualized last quarter, and according to a UBS report , U.S. consumers are in good shape, showing "consumer resilience". In a separate note , the investment bank reported that Q3 earnings clearly illustrate that listed companies are in equally as top shape moving forward.

"It's clear to us that the earnings recession is over as earnings are set to grow for the first time in four quarters" , it said.

In aggregate, earnings are beating by 5.5% and corporate profits are on pace to grow by 4%-in line with our initial expectation of 3-4% growth.

Although the 4Q23 S&P 500 EPS estimate has been revised lower, it hasn't deviated substantially from the historical pattern after accounting for some non-recurring items".

Secondly, FactSet reports that Q4 this year, the median of Wall Street analyst estimates YoY earnings growth of ~4% and revenues to grow by 3.5%. For FY'24, consensus estimates forecast ~12% earnings growth and 5.5% in sales upside.

Consequently, even though U.S. equities are still priced at a premium to global peers, in my judgement this reflects the market's view on the continued outperformance of the U.S. vs rest of the world. This is a constructive point for VOE. It supports the fact that it may continue to remain attractive for value-orientated players moving forward.

Figure 4.

Source: Bank of America

- Starting valuations remain a talking point between value vs. growth

For what it's worth, VOE is priced at a relative discount to large-cap peers in the benchmark indices. The fund trades at ~15x earnings, behind the S&P 500 index's 17.8x forward earnings multiple as I write. However, it is still above the category avg. of 11.4x, and above FactSet's segment average of 11.4x as well. Coming 12-month returns are heavily impacted by starting multiples, and beyond that, sales and earnings growth is the major lever. So the sentiment is mixed here in my analysis. On the one hand, you've got VOE reasonably priced, but not at a major discount. On the other, you have exceptional fundamentals looking out 12 months or so in the large cap space, with multiples a few points ahead of the curve. Without a wide valuation disconnect, my investment cortex is not firing for VOE given (i) its recent performance in trending markets, and (ii) prospects for growth in higher-growth areas of the market. In that vein, the fund's low weighting to tech and other cyclicals may serve to be a relative hinderance.

Figure 5.

Source: Goldman Sachs Investment Research

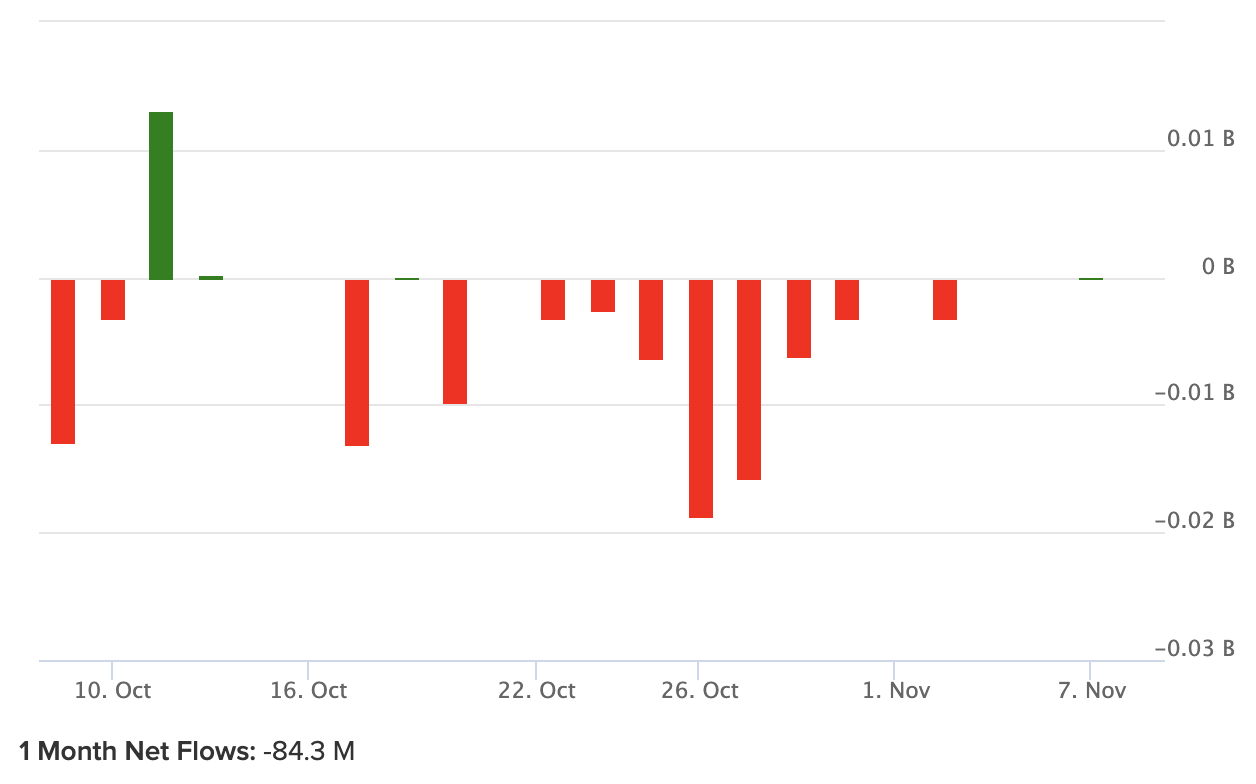

- Fund flows a weakening factor

Related to the point above, capital flows into/out of VOE has been weak in the last 12 months. If investors were in fact buying mid-cap stocks at small discounts, then I'd expect to see more positive flows into VOE to represent this.

Instead 1-month net flows are negative $84mm as I write, and investors haven't lifted the bid on VOE amid the latest snap-back rally in equities. To me this implies two things:

(1). Investors don't value the fund's ability to compound wealth, and

(2). Investors are allocating to more selective opportunities elsewhere.

We can't overlook these principles. Instead, we must embrace the money flows, and respect the fact things have changed in the investment debate for large caps and growth names. This supports a neutral view on the fund.

Figure 6. VOE 12-month fund flows

{kind=link}

Technical factors for consideration

1. Regarding momentum

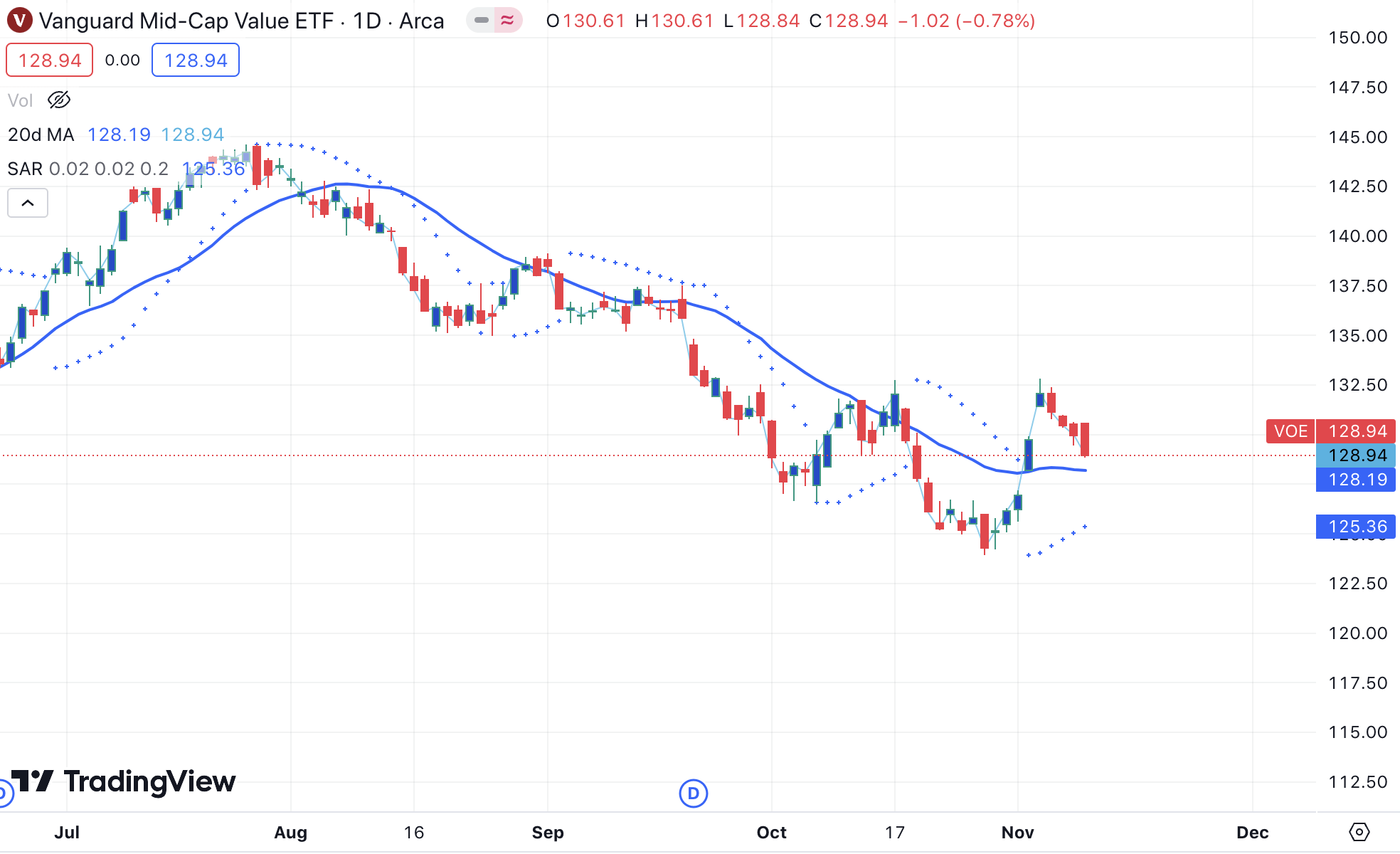

The latest price action in VOE has left plenty of upsides on the table in my opinion. It gapped above its 20DMA this month but has retraced towards this level in subsequent days. The Parabolic SAR has shown a short-reversal, but nothing remarkable to indicate the fund will continue its range extension higher. We are now in line with October range again.

Figure 7.

{kind=link}

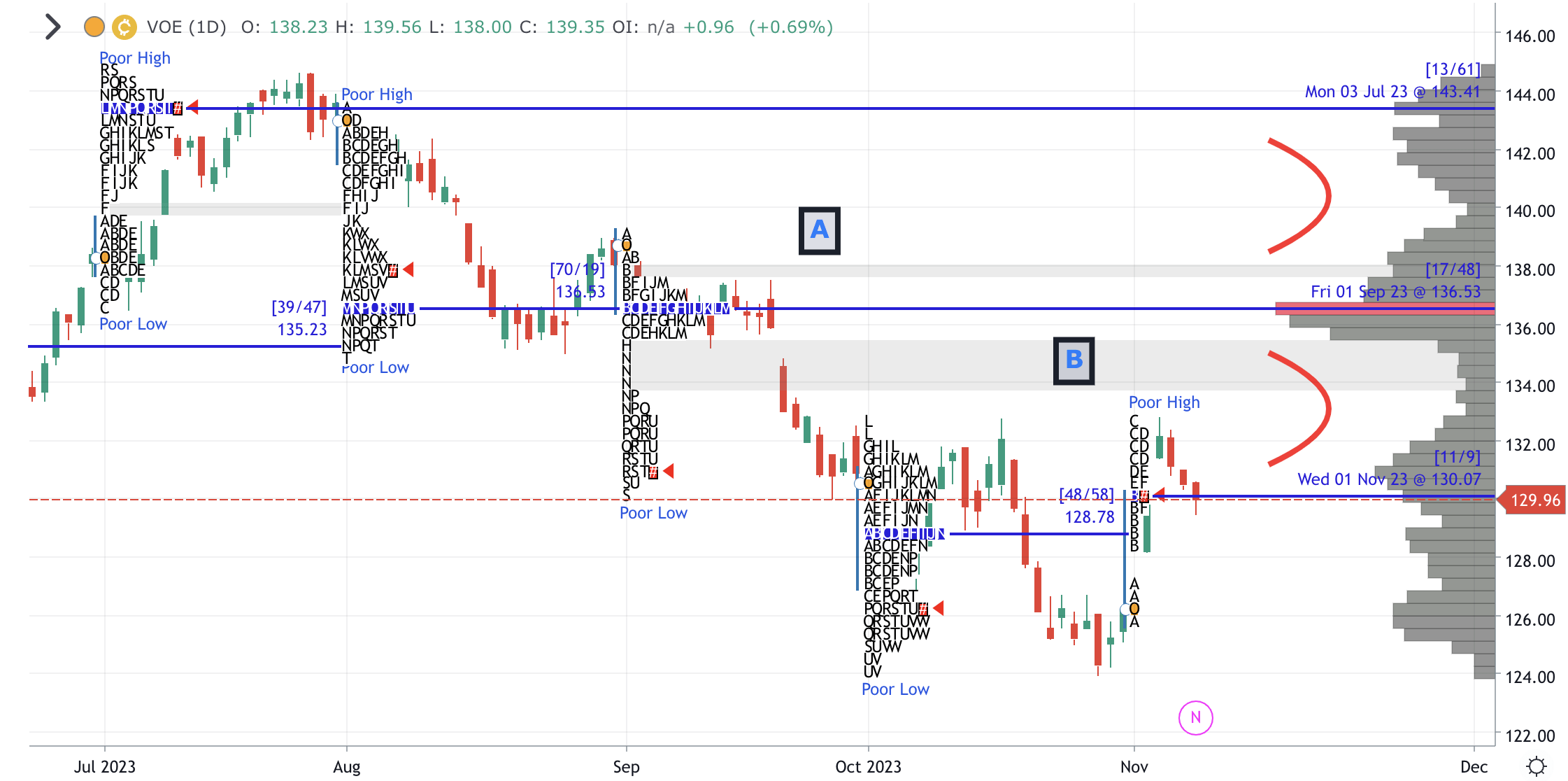

2. Skew, Price distribution

Observations: There are 2 pockets of low usage in the $134s and the $140s. Both contain single print vacuums at A and B, which may attract price even with the recent pullback. But we can't ignore the underdeveloped ledge forming at the $128-$129s either. Investors look to be filling this ledge to match the superior ledge as I write. This area may be have price control until the ledge is matched, before investors decide to fill the low usage pocket from $132-$136. This is a multi-modal distribution with multiple peaks, sporting the notion of further sideways trade.

Key levels: Investors should watch the $128-$129 region closely as we could rotate around this area to complete the ledge to match it to the one above. On the upside, $135 is significant, whereas anything below the $128s on the downside is a soft outcome for the name.

Actionable strategy: The bell curve is not yet formed to reflect price acceptance, so there may be further competition around the $129s. Range trade is therefore supported vs. a directional view.

Figure 8.

{kind=link}

3. Directional bias of trends

Trend action is clearly mixed for VOE, evidenced in the following 3 charts.

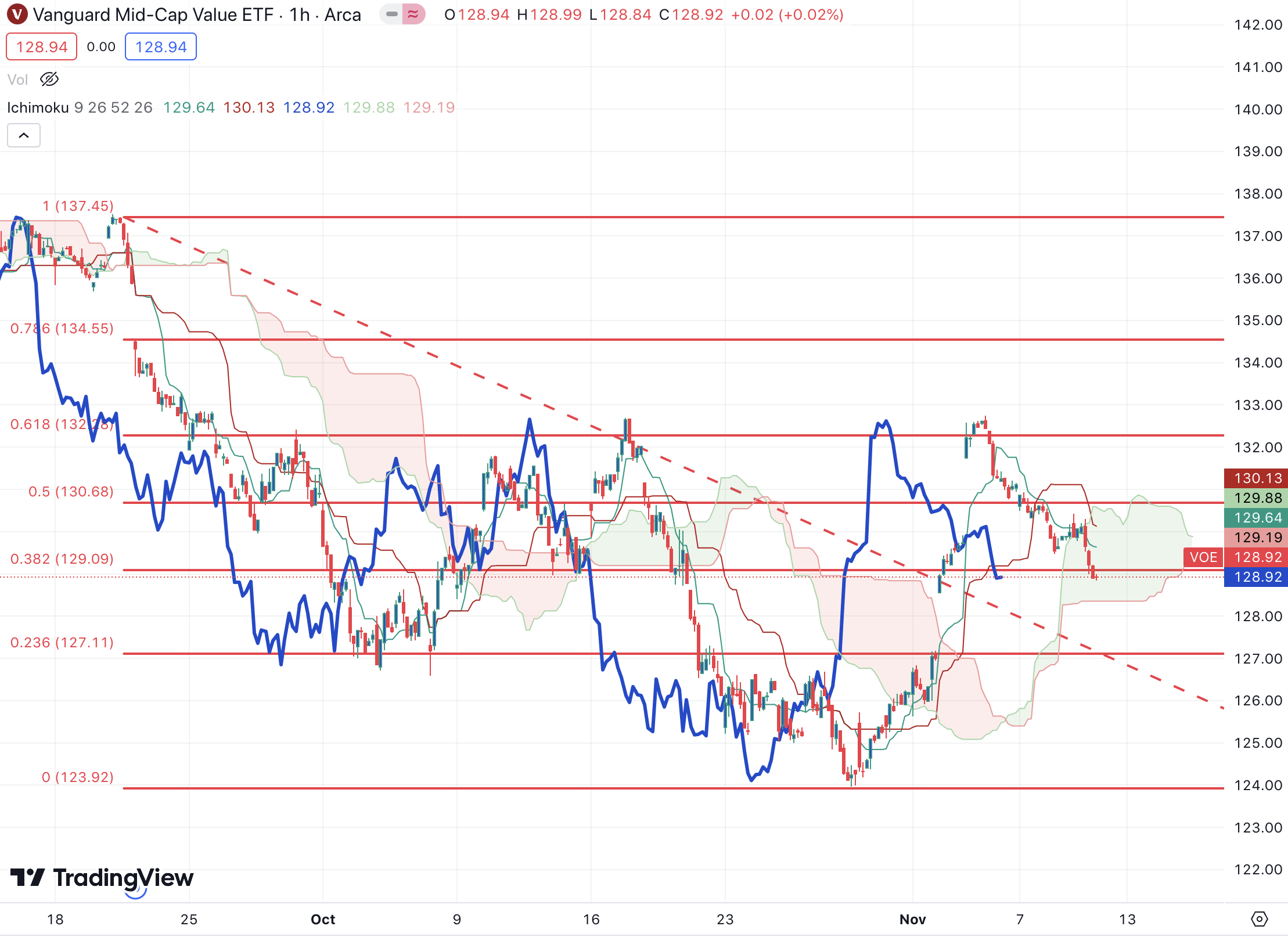

Figure 9 . Short-term (60-minute chart, looking to coming days)-

- Pushing back into the cloud, with both price and lagging line in countertrend to the bullish cloud. Turning line and conversion line are now downward facing, indicating the momentum reversal.

- We took the October high and then sold off sharply, likely an institutional seller. This is not surprising, seeing that ( a ) VOE was heavily sold in October, and ( b ) investors likely took capital off the table once this level was reached once again.

- Tracing the fibs from the September high, we took the 61.8% mark at $132s before progressing south again.

Key levels: $127 is the next level on the downside to watch out for. Taking this, we'd be far less constructive. On the upside, $129-$132 are the key levels to recapture.

{kind=link}

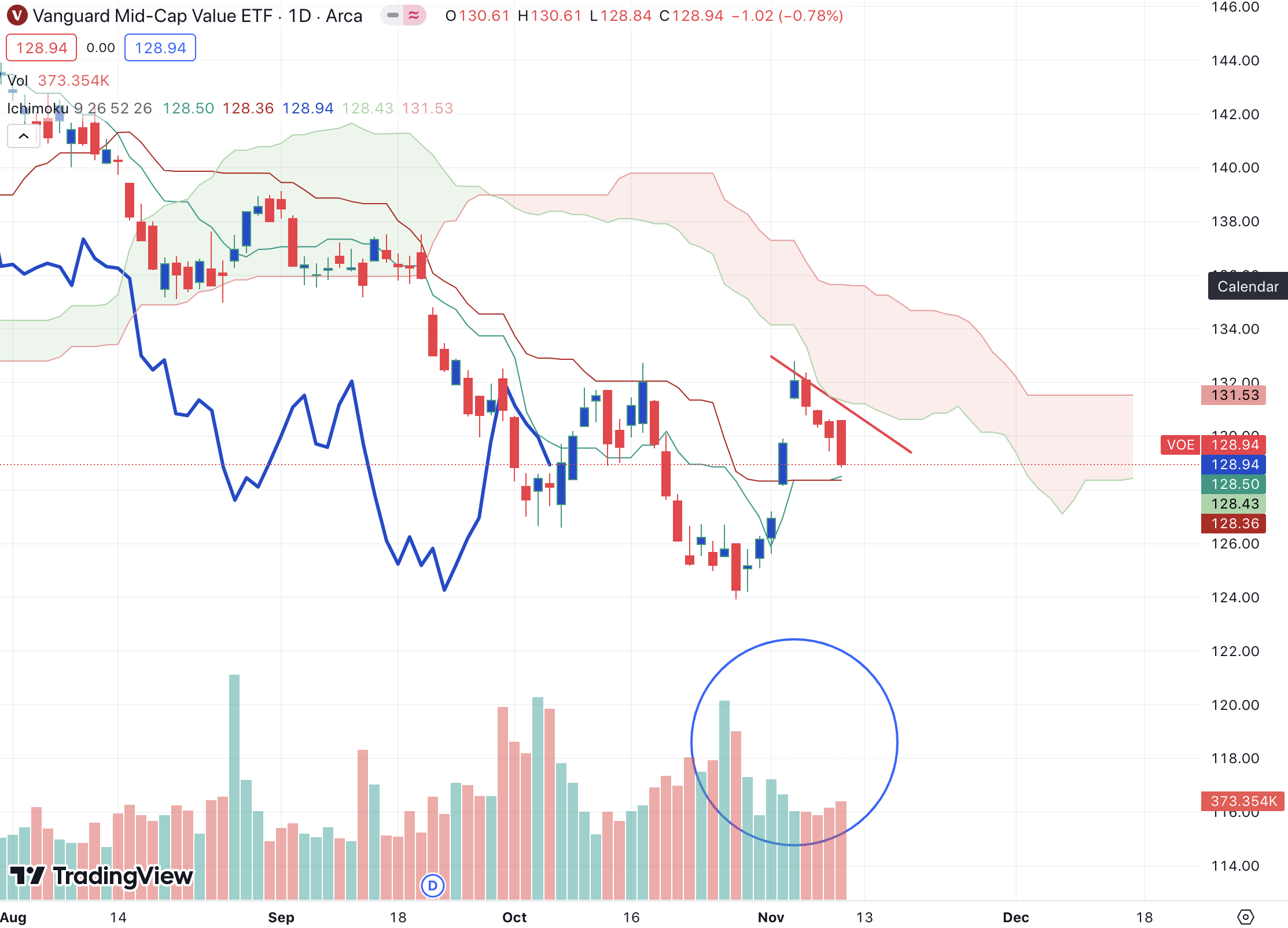

Figure 10. Medium-term (daily chart, looking to the coming weeks)-

- Clearly testing + rejecting the cloud base with the last 4 days of trade. Evening star formation indicated the reversal as buying volume dried up as the move began to take off.

- We closed the 2nd cap higher with this bearish reversal and are now testing the marabuzo line at $128.

- Looking to cross the turning + conversion lines with another decline.

Key levels: The cloud is descending from $128-$126 across the course of November-December, so this is the key level to break. If it doesn't, we could test the $124 lows. On the upside, a break to the $130-$132s by December would have us above the cloud, but the lagging line has more to do.

{kind=link}

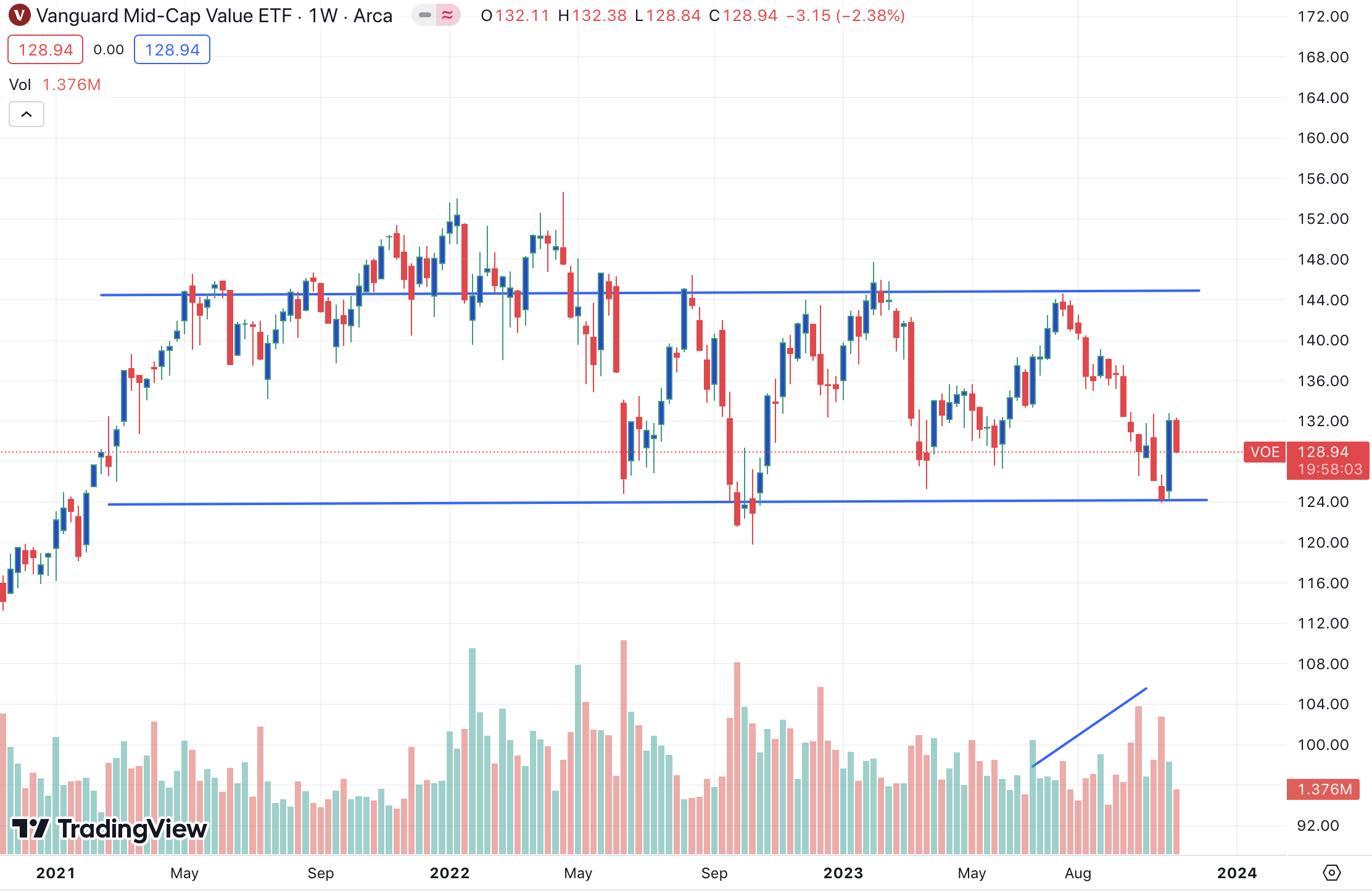

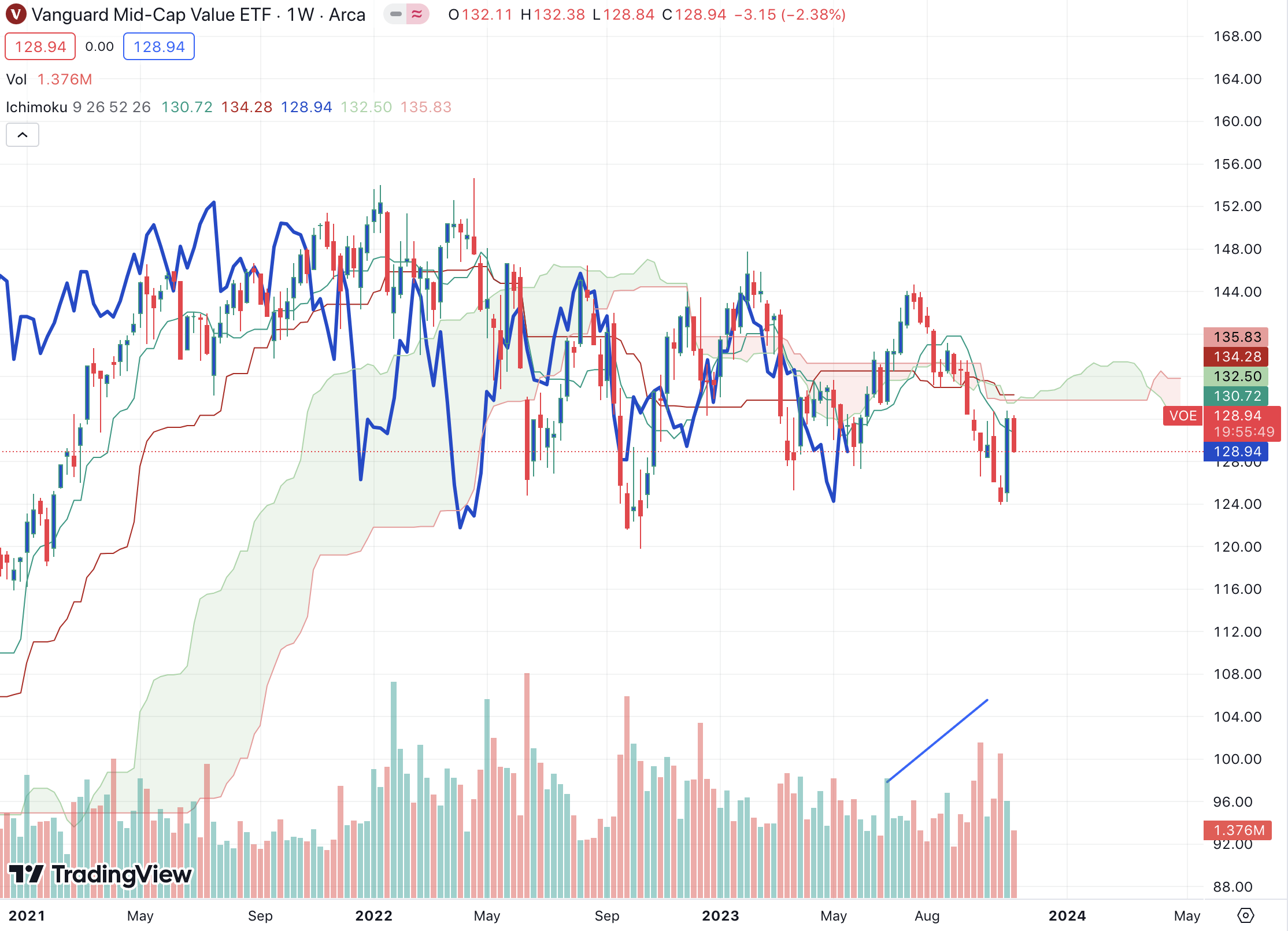

Figure 11. Long-term (weekly chart, looking to coming months)-

- Rangebound trade from bulk of '23 looks set to continue with congestion around $128-$135. Cloud pinch this month reduces amount of work needed, but momentum just isn't there.

- The bullish engulfing candle of last week hasn't added to demand, despite taking out the last 5 weeks range.

- Selling volume still very high, buyers aren't present this week.

Key levels: $135 on the upside, $124 at the prior lows on the downside.

{kind=link}

Discussion summary

In short, VOE hasn't garnered the same attention as its large cap and growth peers. This is a sign of the current risk sentiment that's accompanies the market's change in character since November 1st. Critically, the case for VOE to compound shareholder wealth is dampened by the following factors:

- Low weighting to momentum and growth factors,

- Constituent sectors lagging in earnings/sales growth + projections,

- Starting multiples not at a wide discount to other issues,

- Soft technicals.

Together, these factors imply a neutral outlook on VOE, and my judgement shares this view. Net-net, rate hold.

For further details see:

VOE: Mid-Cap Value Exposure, Flat Compounding Effect Without Momentum