VLPNF - Voestalpine Trades At 4.5x EBITDA Despite Anticipated 25% EBITDA Drop

2023-07-18 11:30:00 ET

Summary

- Voestalpine is an Austrian producer of steel and steel products.

- The majority of its sales are generated within the EU. The automotive sector is the largest customer.

- The company anticipates a 25% EBITDA decrease, but this should still result in an EPS of 3 EUR per share.

- The past few years, Voestalpine made good progress in reducing net debt and pension deficit.

Introduction

Voestalpine ( OTCPK:VLPNF ) ( OTCPK:VLPNY ) is an Austria-based steel producer with four main divisions with the steel production division being the most important contributor to revenue and EBITDA in fiscal year 2023 (which ended in March).

{kind=link}

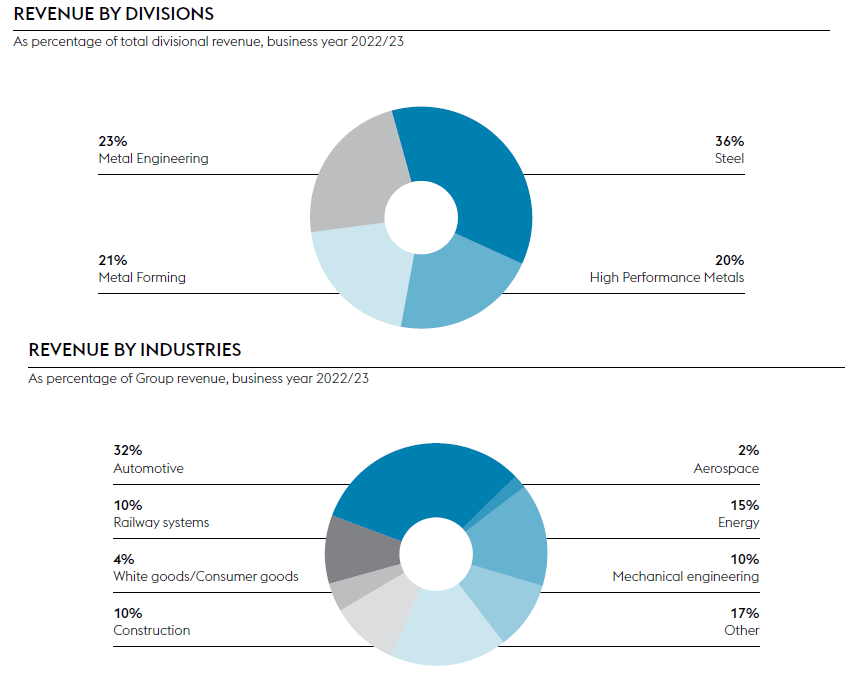

As you can see below, the vast majority of Voestalpine’s revenue is generated within the European Union which accounts for almost two thirds of total revenue. The automotive industry is the most important sector for Voestalpine as almost a third of its revenue is generated from selling steel and steel products to car manufacturers . Energy (15%) and railway systems (10%) also are important contributors to the consolidated revenue of Voestalpine.

{kind=link}

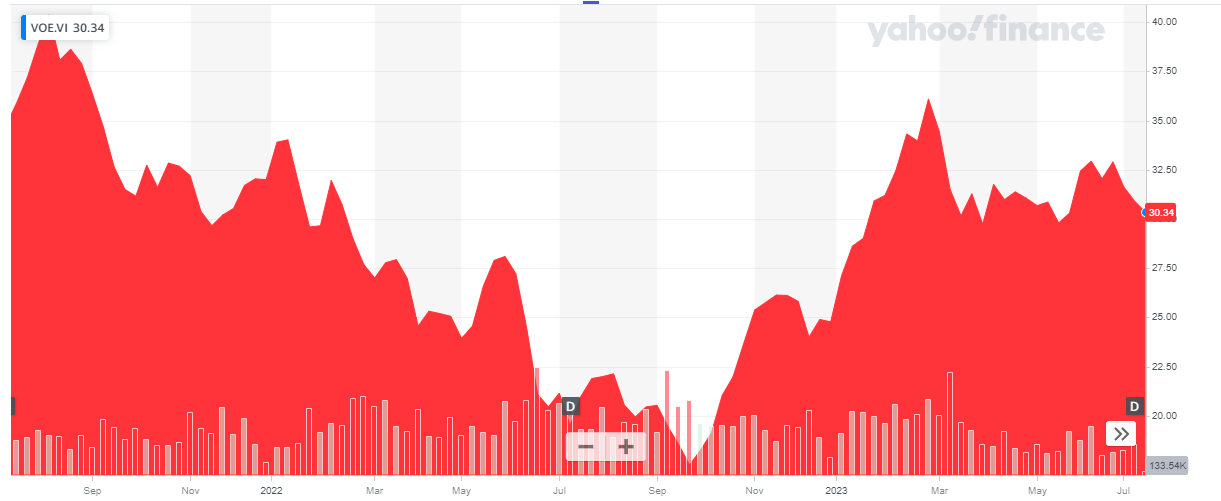

The company’s Austrian listing is much more liquid, and I think it’s recommended to use the Vienna Stock Exchange to trade in Voestalpine’s shares. The ticker symbol in Austria is VOE , and the average daily volume is roughly a quarter of a million shares. The current market capitalization is approximately 5.23B EUR as there are approximately 172.7M shares outstanding (after taking the treasury shares into account).

{kind=link}

FY 2023 was great but that performance won’t be replicated this year

As mentioned in the introduction, Voestalpine’s financial year does not fall within a calendar year as the company’s financial year ends in March. This means the most recent financial results we have access to are the full-year results for FY 2023, and the company published its annual report just a few weeks ago.

Despite being hit with a substantial increase in the energy prices (which more than tripled to 1.5B EUR in FY 2023 compared to less than 425M EUR in FY 2021 before the war in Ukraine started), Voestalpine put in an excellent financial performance as the company was able to capitalize on the strong steel prices.

During FY 2023, Voestalpine reported a total revenue of 18.23B EUR, an increase of more than 20% compared to FY 2022 but as the COGS increased at a faster pace, the gross profit increase remained limited to less than 10%.

{kind=link}

Some of the other expenses also increased: the distribution expenses jumped by in excess of 10% while the administrative expenses also increased by almost 10% and the main reason why Voestalpine was able to report a 12% increase in its EBIT (to 1.62B EUR) was the net income related to the sale of the majority stake in a US subsidiary. With a pre-tax income of 1.49B EUR and a net income of 1.085B EUR, the net EPS from continuing operations was 5.48 EUR. Including the impact of discontinued operations , the EPS was a very handsome 6.01 EUR.

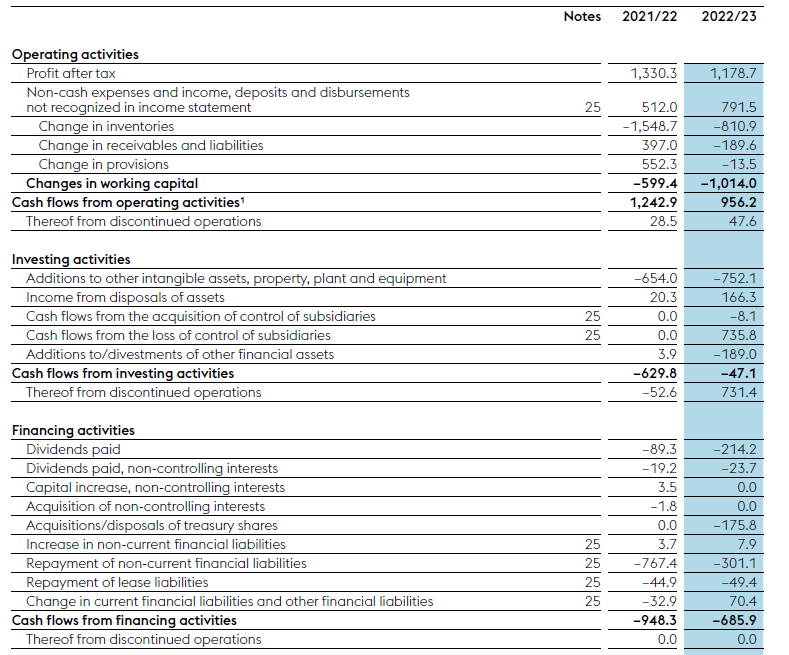

The cash flow result also is very interesting (and important, as Voestalpine will invest in Electric Arc Furnaces in the next few years). Voestalpine reported an operating cash flow of 956M EUR. However, this includes a 1.01B EUR investment in the working capital position but also includes 48M EUR generated by the discontinued operations. In order to get a better idea of the free cash flow performance moving forward, I think it’s only fair to ignore the contribution from the discontinued activities. We should also deduct the 24M EUR in dividend paid to non-controlling interests as well as the 49M EUR in lease payments.

{kind=link}

This means that on an adjusted basis, the operating cash flow generated by Voestalpine in FY 2023 was approximately 1.85B EUR. The total capex was approximately 752M EUR resulting in a net underlying free cash flow of approximately 1.12B EUR or almost 7.2 EUR per share. That’s higher than the reported net income as the total capex + lease payments of approximately 800M EUR was lower than the 938M EUR in depreciation expenses.

That’s great but this will change soon as the company’s capex will likely exceed 1B EUR in the next few years as part of Voestalpine’s "Greentec" push: "Producing "green" steel by installing electric arc furnaces.

While this indeed indicates Voestalpine is trading at a pretty cheap valuation, it would be dangerous to just use last year’s financial results to determine how well the company will do this year. After all, FY 2023 was a good year thanks to the steel price, the decent volumes and the non-recurring income from an asset sale.

Voestalpine has released official guidance for this year wherein it expects to generate 1.7-1.9B EUR in EBITDA . We know the total depreciation and amortization expenses will come in around 900M EUR while the interest expenses will increase further to 200M EUR (up from 182M EUR). The company has about 1.25B EUR in bonds at a fixed interest rate of just under 1.8% (see below) but the bank debt is pushing the total interest expenses higher. I think it was a smart move by Voestalpine to issue a convertible bond with a 2.75% coupon but unfortunately it only raised 250M EUR at these terms (convertible at in excess of 40 EUR per share).

{kind=link}

The assumptions above, offset by an assumed 40M EUR in finance income, would result in a pre-tax income of 740M EUR (using the midpoint of the EBITDA guidance). Applying an average tax rate of 25%, the net income would be 555M EUR and approximately 525M EUR would be attributable to Voestalpine. This should work out to around 3 EUR per share. So based on the full-year guidance, Voestalpine should still perform well this year and also generate enough cash flow to invest in the electric arc furnaces while there also is no reason for Voestalpine to cut its dividend from the current level of 1.50 EUR per share (that being said, we should understand the recent dividend payments were based on extraordinary years and I’d prefer to see a lower dividend and a faster debt reduction).

{kind=link}

In my previous article I was starting to get a bit worried about the total net debt and pension deficit on Voestalpine’s balance sheet. The initial phase of the COVID pandemic in 2020 didn’t do much to ease those fears but the subsequent boom in the demand for steel and steel prices has improved the debt position while the increasing interest rates on the financial markets obviously had a positive impact on the pension deficit as using a higher discount rate reduces the current value of the deficit).

As of the end of March, Voestalpine had 1.06B EUR in cash on the balance sheet while its total amount of financial liabilities came in at 3.1B EUR, for a net debt of just over 2B EUR (down from the in excess of 3.1B EUR in the year before the COVID pandemic). Considering the group expects to generate 1.8-1.9B EUR in EBITDA this year, the net debt level isn’t really a concern at this point.

As of the end of FY 2023, Voestalpine’s pension deficit decreased further to 939M EUR (if included in the net debt level, this would add about 0.5 to the net debt to EBITDA ratio, which would increase to 1.6. Still manageable). And a further 1% increase in the average interest rate would further reduce the pension (and severance) deficit. While Voestalpine will have to continue to keep an eye on the pension deficit, it appears to be pretty manageable.

{kind=link}

Investment thesis

I like how Voestalpine doesn’t even try to sugarcoat an expected decrease in its EBITDA and I can certainly appreciate this transparent and straightforward approach. Based on the midpoint of Voestalpine’s guidance, I expect the company to report an EPS of 3 EUR per share this year while the EV/EBITDA (including the pension deficit) comes in at approximately 4.5 (and around 4 if you would exclude the pension deficit.

Voestalpine appears cheap but keep in mind we're likely in a slow downcycle and I don’t expect the EBITDA nor the net income to increase anytime soon. In any case, I do expect Voestalpine to remain profitable and I think the increasing cost of debt remains manageable. The financial markets also don’t appear to be overly concerned as the 2026 bond is currently trading with a yield to maturity of around 4%. I currently have no position in Voestalpine but I will be keeping an eye on the stock as it offers exposure to the European steel industry. As energy costs have been trending down, Voestalpine’s performance may actually exceed expectations.

For further details see:

Voestalpine Trades At 4.5x EBITDA Despite Anticipated 25% EBITDA Drop