VLRS - Volaris: A Growth Story Hitting A Limit

Summary

- Volaris, like any other airline, is feeling the pain of high oil prices.

- Despite high fuel costs and softer than expected unit costs, Volaris put on display strong cost control necessary to navigate the current climate.

- Underpentration of air travel in Mexico provides significant opportunity for Volaris and shareholders.

Airline stocks are hot at the moment, most often to buy sometimes to sell as economic pressures cast a doubt on continued robustness of demand for air travel. In recent earnings releases, we have observed a bullish tone among airline executives believing in countercyclical behavior of air travel demand patterns for at least the coming quarter. In this report, I will be analyzing the results for Volaris (VLRS) showing that while growth is strong, the airline seems to be meeting some limits.

Unlocking Growth Potential

{kind=link}

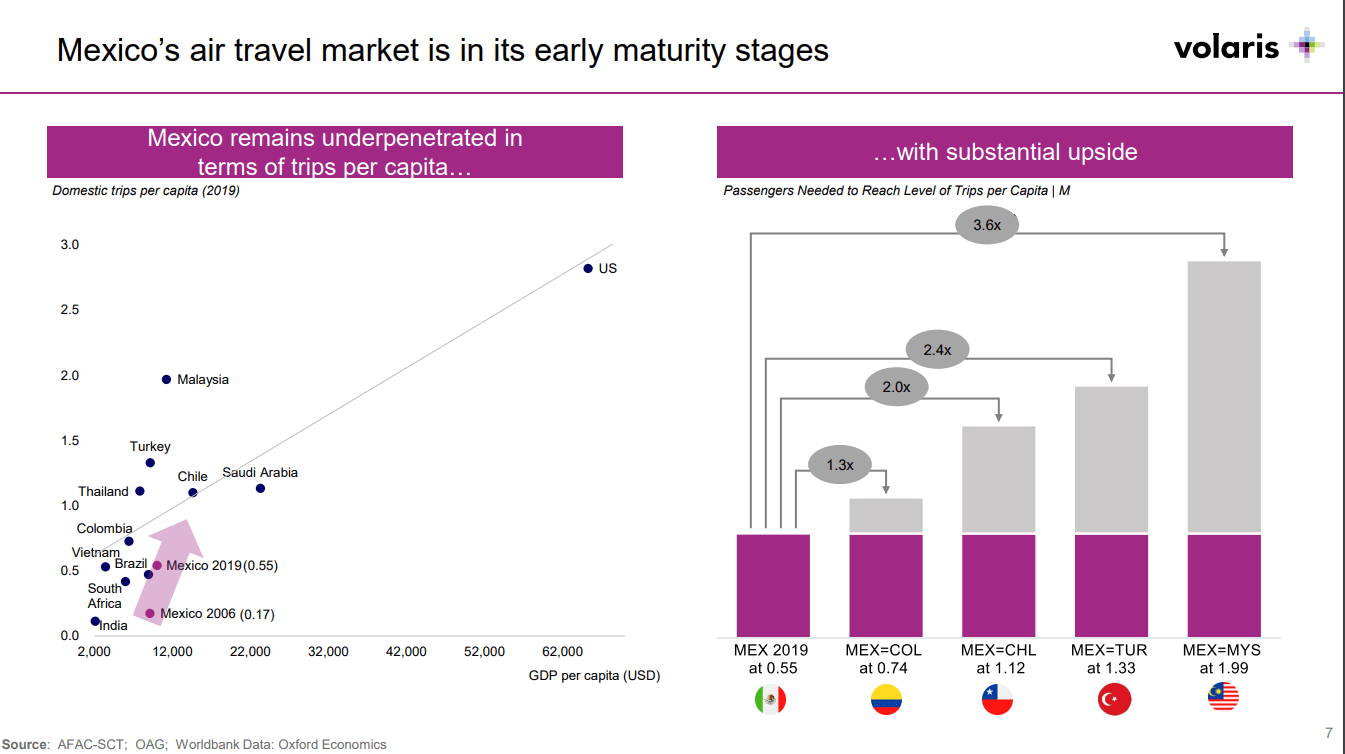

Just from a quick glance at the relation between trips per capita and GDP per capita, there seems to be a lot of growth if we compare countries with similar GDP per capita to Mexico, where Volaris is active. Obviously, a distribution of the GDP plays a big role as well but overall Volaris seems to be active in a market that has a lot of space to grow. Furthermore, nearly 50% of the routes Volaris operates has no competition from other airlines competing only against luxury bus travel which saw its market share shrinking for several years in a row.

From other airlines, the main competition and biggest threat going forward would be Viva which has reached an agreement to merge with Avianca. Aiding to Volaris' strength is the low cost structure that allows it to keep ticket prices low. The company has cost per available seat mile that are comparable to that of Wizz Air allowing it to be offering ticket prices at which many other airlines would no longer be profitable.

Weak Spot In Recent Earnings Result

{kind=link}

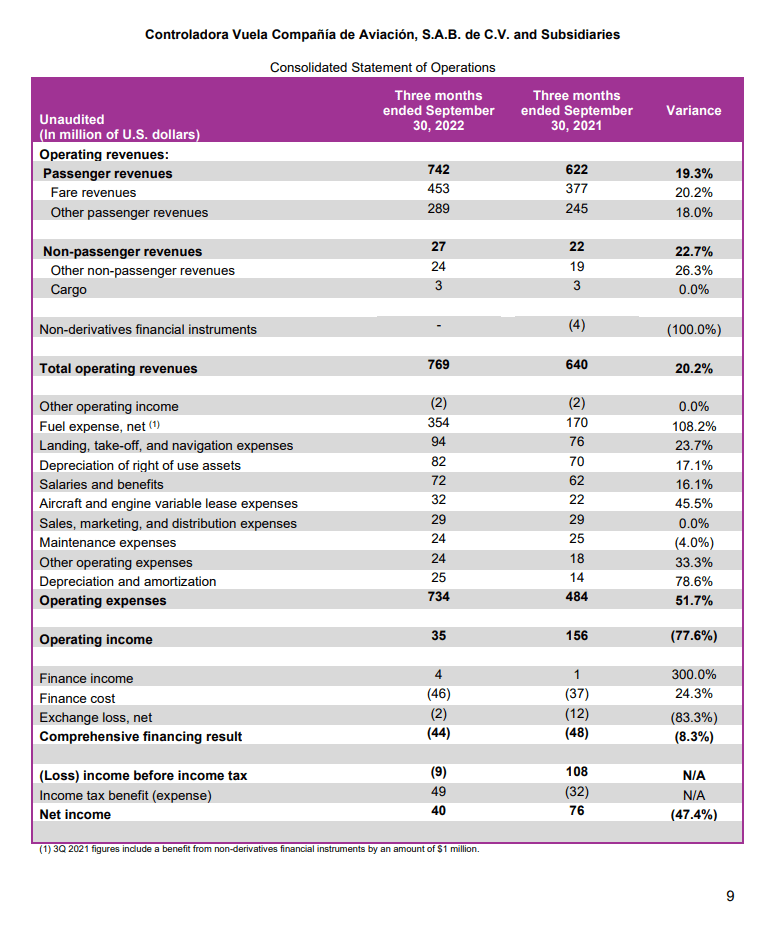

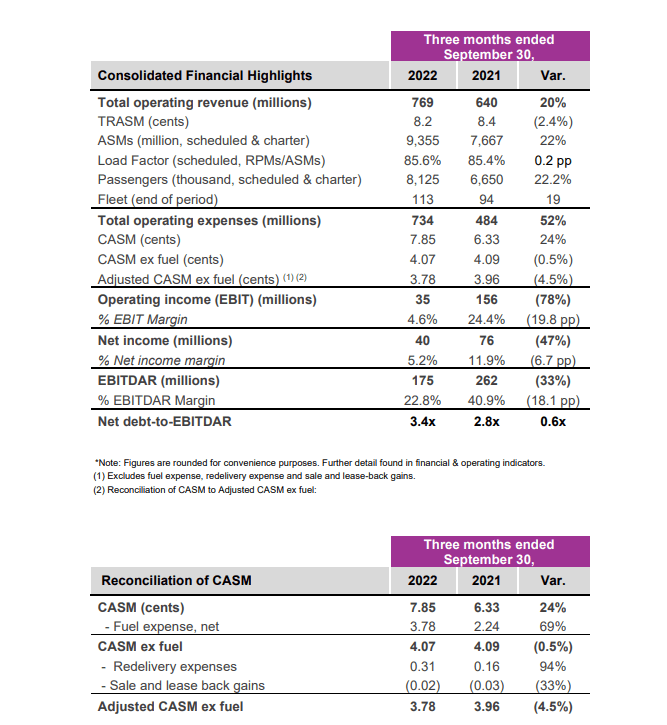

Operating revenues increased by over 20%, but none of it translated to the bottom line as costs increased 51.7%. By now it does not come as a surprise that the reason of high airline operating costs are elevated fuel prices. Fuel costs were 108.2% higher year-over-year driven by higher unit fuel costs and higher gallons consumed. The operating margin dropped from 24.4% to 4.6%. Operating income decline in the current fuel price environment is not something that worries me. Ideally with strong demand levels, we would like to see operating income growing but with elevated fuel prices that is not realistic for most airlines.

{kind=link}

What I found somewhat unfortunate is that while most airlines are seeing continued strong TRASM growth, Volaris is actually seeing TRASM decline. The year-over-year capacity addition was 22% and on stable load factors should normally amount to similar passenger revenue growth. However, during the quarter this was offset by lower unit revenues. Average base fares dropped to $56, marking a 1.8% decrease while ancillary revenues dropped 2.5% to $39, marking a 2.1% decrease in revenue per passenger to $95. That is what I found most disappointing as this could be an indication that for Volaris the times of unit revenue growth driven by strong demand are over and it has to bring down prices to fill the aircraft. Analysts were expecting revenues that were $27.6 million higher. Over half of the shortfall can be explained by the softening in average fares.

Was it that bad? The answer is no. While Volaris missed on top line, its earnings per share of $0.30 was strong and CASM-Ex and adjusted CASM-Ex were down as well showing that the costs that Volaris can control and reduce have been lowered.

2022 Outlook More Or Less The Same

{kind=link}

For 2022, Volaris now expects capacity growth of 25% up from 23 to 25 percent earlier. While maintaining its revenue guide for $2.8 billion to $3.0 billion with EBITDAR margins in the low 20s and CapEx at the higher end of the $140 million to $145 million previously guided for. So, overall Volaris is still on track on delivering on its targets and its CASM-ex growth is actually expected to be 1% instead of the 1 to 3 percent previously guided.

Conclusion: Volaris Stock A Speculative Penetration Buy

Reality is that right now fuel prices are significantly impacting the P&L statements of airlines and there is nothing really that airlines can do about that elevated fuel price environment other than seeing where it can pass through costs and operate the most efficient aircraft. Volaris, with a low unit cost basis, is positioned relatively well but even the airline is feeling the pain of these higher costs. Somewhat disappointing was that unit revenues declined which raises some questions regarding robustness of average fares going forward.

In that regard, I do consider Volaris somewhat of a risky investment but over the longer term with strong cost control and under-penetration of air travel in general in Mexico, I do believe that Volaris is one of the airlines that could be very well positioned to benefit from a catch up in air travel adoption in Mexico.

For further details see:

Volaris: A Growth Story Hitting A Limit