VLRS - Volaris Stock: 2022 Fear Has Created A Huge Buying Opportunity

Summary

- Following a remarkable recovery in 2021, Volaris' profitability has evaporated in 2022 due to a huge jump in fuel prices.

- Volaris made a strategic decision to sacrifice short-term profits in 2022 by growing capacity rapidly to solidify its dominant position in a fast-growing market.

- Over the past decade, Volaris has always made a full recovery following periods of profit pressure.

- Volaris stock could triple or more within a few years.

Mexican budget airline Volaris ( VLRS ) recovered from the COVID-19 pandemic faster than any other airline in the world . The company recorded a superb 18.1% operating margin last year: well ahead of its pre-pandemic performance.

As a result, Volaris stock surged from a pandemic low around $3 to an all-time high closing price of $22.84 by July 2021. Despite some volatility in the following months, Volaris stock continued to trade above the $20 mark as recently as February. More recently, though, the shares have plunged back into single-digit territory, as soaring fuel prices have eroded the company's profitability.

However, this temporary margin pressure does not diminish Volaris' long-term earnings prospects. That makes Volaris stock extremely attractive following its sharp pullback.

Fuel prices drive an earnings crunch

Through the first nine months of 2022, Volaris was unprofitable , posting an operating margin of -0.8%. That compared to 16.5% for the first nine months of 2021 and 9.5% for the same period in 2019.

This sharp reversal in Volaris' fortunes was driven entirely by a huge rise in fuel prices. Unit revenue ticked up by 2.6% while non-fuel unit costs decreased 2.3%. Fuel efficiency also improved slightly. But Volaris' average fuel cost per gallon jumped 79%, rising from $2.14 per gallon in the first nine months of 2021 to $3.83 in the comparable period of 2022.

Even when jet fuel prices were low in 2021, Volaris spent more than a quarter of its revenue on jet fuel: by far its largest expense item. Year to date, that has jumped to 46%. This explains why the company has suffered such a massive earnings hit.

Tradeoffs between growth and profitability

Skeptics might note that most U.S. airlines have posted significant year-over-year earnings growth in 2022 despite facing similar profit headwinds from rising jet fuel prices. Some of that relates to the Mexican market's faster post-pandemic recovery. (Volaris is facing tougher comparisons than U.S. carriers.) But even relative to 2019, Volaris has experienced greater margin erosion.

However, Volaris faces a different calculus than U.S. carriers. First, the U.S. air travel market is quite mature. That incentivizes U.S. airlines to prioritize profitability over growth by pulling back on capacity to support higher fares when fuel prices jump or economic conditions sour.

Second, U.S. airlines have struggled with broad staffing shortages this year, particularly with respect to pilots. That forced a further moderation in growth plans across the sector in the first nine months of 2022. During this period, even formerly fast-growing ultra-low cost carriers (ULCCs) Spirit Airlines ( SAVE ) and Frontier Group ( ULCC ) increased capacity just 14% and 12%, respectively, compared to 2019. The combination of tight capacity and strong demand has enabled U.S. airlines to offset much of their fuel cost increases with big unit revenue gains.

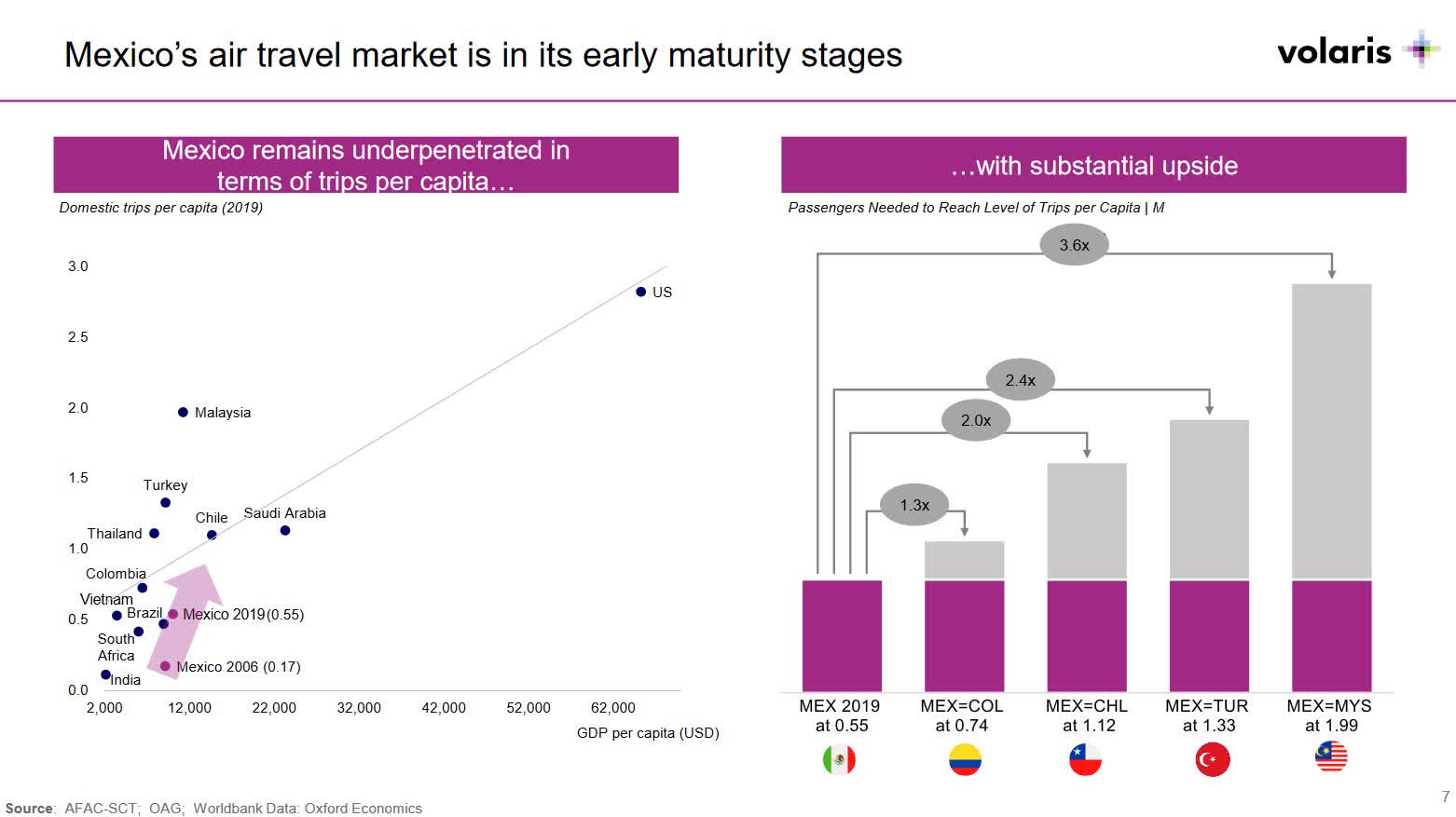

By contrast, the Mexican air travel market is growing rapidly. Domestic air trips per capita have more than tripled since 2006, driven primarily by ULCCs Volaris and VivaAerobus disrupting the market with lower fares. Moreover, there's plenty of room for further growth in trips per capita to reach the levels seen in other developing countries such as Turkey and Malaysia . (See slide 7.)

Source: Volaris October 2022 presentation, slide 7.

{kind=link}

While reducing capacity and raising fares would likely maximize Volaris' near-term profitability, it would slow air travel adoption in Mexico. That would hurt the company's future growth. Additionally, Mexico's air travel market is still adjusting to the late-2020 collapse of Interjet, which was the country's third-largest airline as recently as 2019. Cutting capacity now would give rivals Aeromexico and VivaAerobus a jump on winning the loyalty of former Interjet customers.

Accordingly, Volaris operated 42% more capacity in the first nine months of 2022 than it did in the same period of 2019. This included 28% growth just over the past year. It's not surprising that Volaris could not raise fares significantly to offset higher fuel prices while growing at this pace.

The long-term case for Volaris remains intact

Some readers might ask, "What's the point of growing quickly if you're not making money?" It's a reasonable question, given that profitless growth has been a hallmark of the airline industry for most of its history.

That said, consolidation drove a dramatic structural improvement in the U.S. airline industry's profitability during the 2010s. In recent years, the four largest U.S. airlines have controlled more than 80% of the market, paving the way for more rational competition.

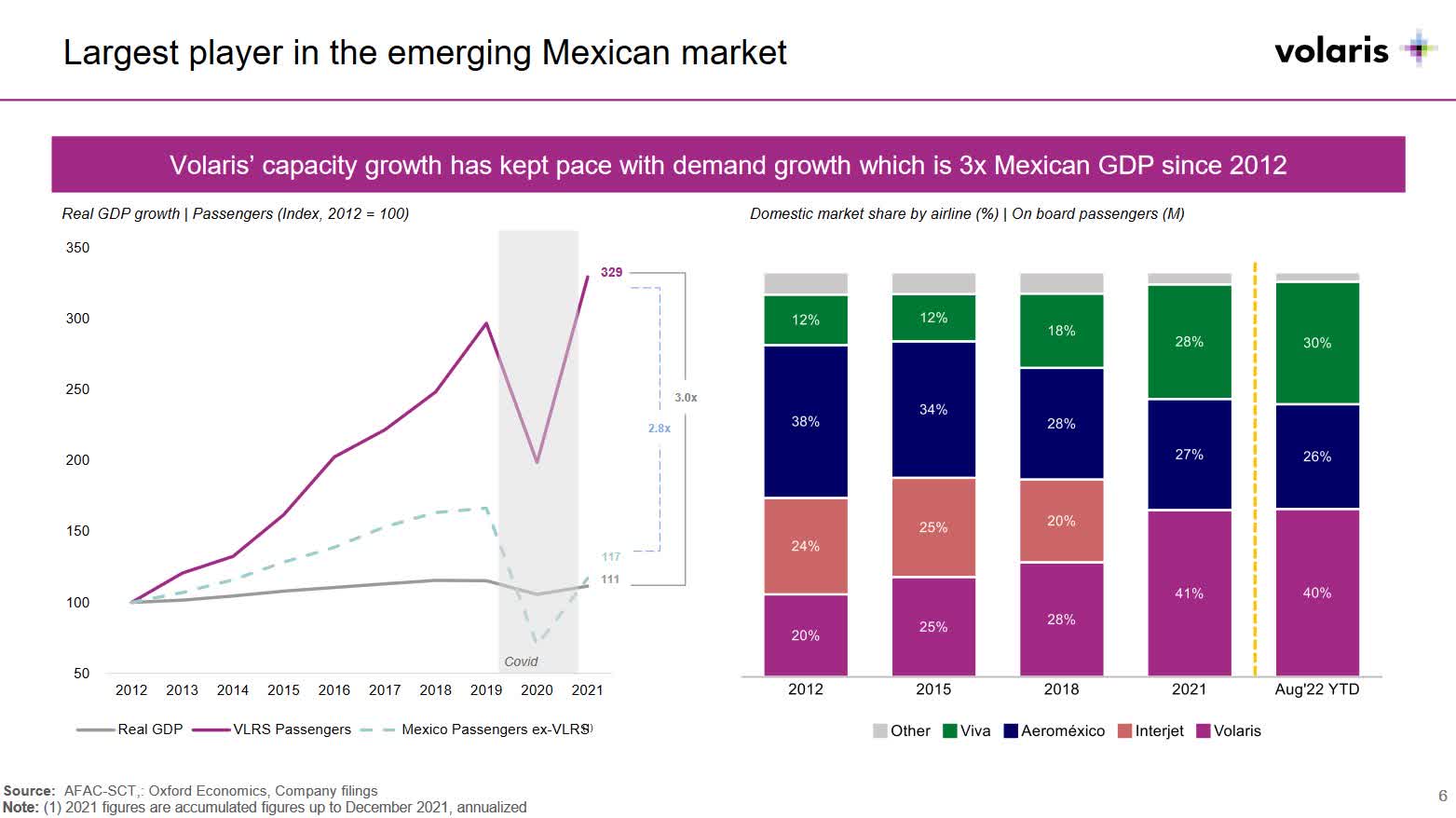

For comparison, following Interjet's collapse, Mexico's three major airlines have a combined 96% share of the domestic market. Volaris leads the way with 40% market share. This market structure should enable solid industry-level profitability over the long term. Volaris is especially well positioned, thanks to its leading market share and rock-bottom costs.

Source: Volaris October 2022 presentation, slide 6.

{kind=link}

Investors have already seen glimpses of Volaris' earnings potential. The company recorded a net margin of 7.6% in 2019, and after posting a big loss in 2020 due to the pandemic, adjusted net margin improved to 8.7% in 2021. Volaris also had a run of strong profitability in 2015 and 2016 .

Of course, there have also been periodic setbacks during Volaris' nine years as a public company. But each time, Volaris has come back stronger, with significantly higher revenue and earnings. Considering its best-in-class cost structure and leading market share in the highly-consolidated Mexican air travel market, Volaris is likely to make another robust recovery in the next couple of years.

A dramatically undervalued stock

Volaris estimates that it will end 2022 with revenue between $2.8 billion and $3 billion and an EBITDAR (earnings before interest, taxes, depreciation, amortization, and rent) margin "in the low twenties." Assuming revenue of $2.85 billion and a 21% EBITDAR margin, EBITDAR would come in right around $600 million.

Based on its recent lease-adjusted enterprise value of approximately $3.19 billion, Volaris stock trades for around 5.3 times estimated 2022 EBITDAR.

Source: Seeking Alpha VLRS quote page.

A valuation in the 5-6 times EBITDAR range would be reasonable given the risk inherent in the airline business and the greater volatility of the Mexican airline industry compared to the U.S., but only as a mid-cycle average. For Volaris, 2022 will likely prove to be a cyclical trough for profitability due to this year's spike in fuel prices.

By contrast, EBITDAR came in around $800 million last year. Moreover, management estimates that Volaris' margins should average in the " low to mid-30s " over the long term. While that's a bit lower than the 36.7% EBITDAR margin Volaris posted in 2021, revenue is on track to grow about 30% this year. That puts Volaris' normalized EBITDAR potential (based on 2022 revenue and a low to mid-30s EBITDAR margin) at around $900 million-$1 billion.

Even at 5 times the low end of that EBITDAR range (i.e., $4.5 billion), Volaris stock would have a fair value of just over $20: up more than 150% from its Wednesday closing price of $8.00. A 6X multiple on $1 billion of EBITDAR would imply a $33 stock price.

Looking ahead, Volaris plans to slow its capacity growth to around 10% in 2023. That will lead to lower revenue growth, but it will create a foundation for firmer pricing to support a margin recovery.

Additionally, fuel prices are likely to moderate over the next year. Crude oil prices have already come down significantly from the peaks seen this spring and summer, with the forward curve pricing in further declines. Crack spreads have also been dramatically higher than usual in 2022 and will likely moderate in 2023.

Thus, Volaris' margin recovery is likely to begin by Q2 2023, if not earlier. That should in turn help Volaris stock regain its momentum.

The key risks

As noted above, Volaris has historically reported extremely volatile earnings results. To some extent, this stems from the Mexican air travel market being prone to bouts of irrational competition. Interjet's market exit likely reduced this tendency, but it's too soon to be confident that Mexican airlines will be more careful about protecting the bottom line in the future.

Furthermore, if fuel prices remain high and the company finds that it can't increase fares without torpedoing ticket sales, Volaris could continue losing money.

Relatedly, high aircraft-related costs would make it difficult for Volaris to reduce capacity in the near term. That removes what otherwise could be an important tool for protecting profitability in the face of further fuel price increases or a downturn in demand.

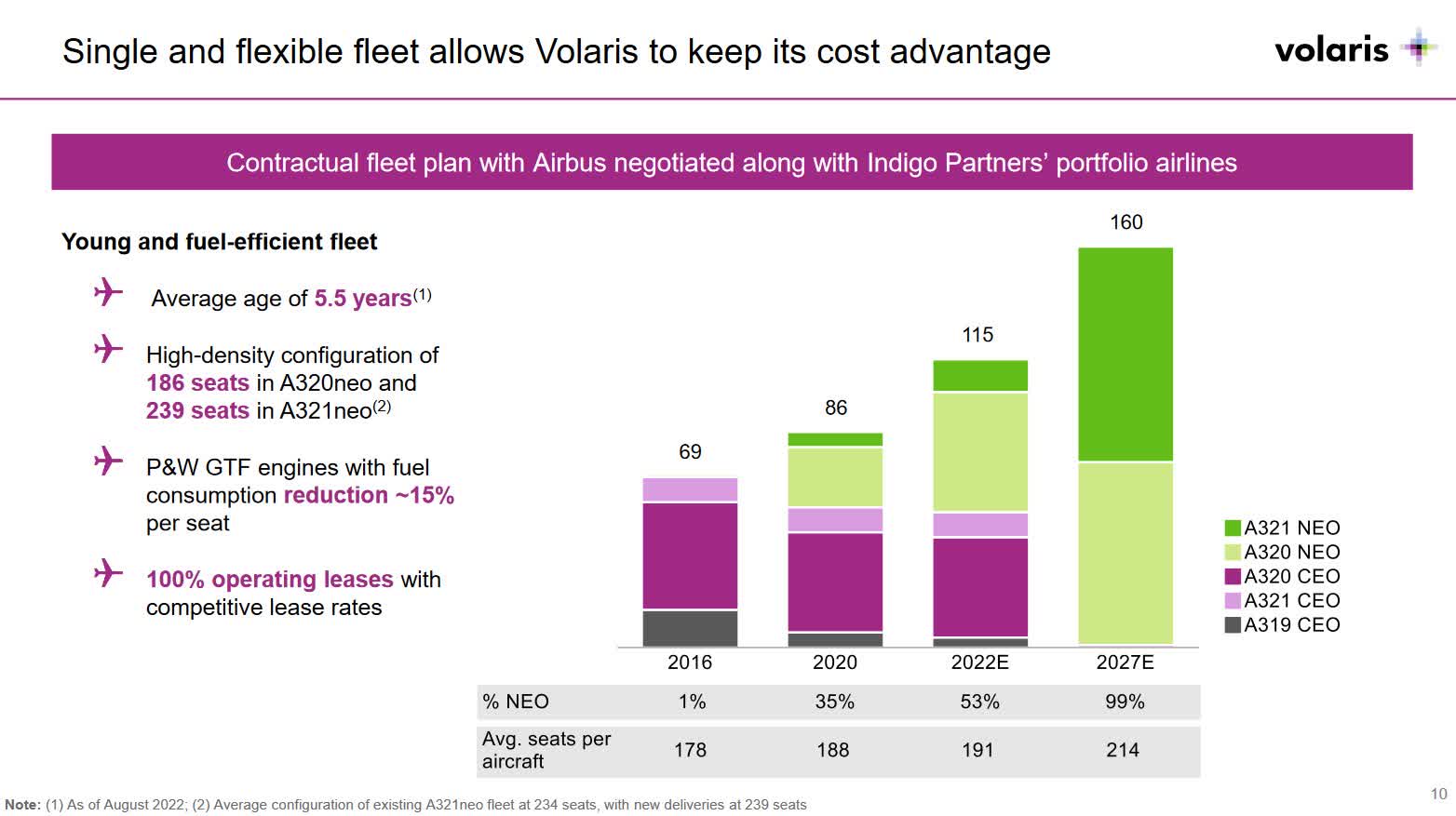

Fortunately, Volaris' position as the largest and strongest airline in Mexico means that rivals feel the pain of irrational competition before it does serious damage to Volaris' finances. Additionally, the company is poised to continue its aggressive migration towards next-generation Airbus ( OTCPK:EADSY ) planes: particularly the A321neo. This will improve fuel efficiency by more than 10% over the next five years, mitigating the impact of fuel prices on Volaris' bottom line. And the company's new subsidiaries in El Salvador and Costa Rica give Volaris the option to shift its growth outside of Mexico if warranted.

Source: Volaris October 2022 presentation, slide 10.

{kind=link}

Like any airline stock, Volaris is a risky investment. The company's participation in the still-immature Mexican air travel market makes Volaris stock even riskier.

However, Volaris offers more than enough upside potential to justify taking that risk. Analysts expect revenue to reach $3.4 billion by 2024 . Even at the low end of the company's long-term margin guidance range, that would imply over $1 billion of EBITDAR.

To be fair, lease liabilities will continue to grow as Volaris expands and refreshes its fleet. Nevertheless, this level of underlying earnings power gives Volaris stock a good chance of tripling or more within 2-3 years to surpass the all-time high reached in 2021.

Editor's Note: This article was submitted as part of Seeking Alpha's Top Ex-US Stock Pick competition, which runs through November 7. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

Volaris Stock: 2022 Fear Has Created A Huge Buying Opportunity