EADSF - Volaris Stock Beaten Down As It Navigates Through GTF Challenges

2023-10-30 14:59:10 ET

Summary

- Volaris reported Q3 results with missed EPS but beat revenue estimates.

- The company adjusted its full-year guidance due to issues with the Pratt & Whitney geared turbofan.

- Volaris plans to redistribute capacity to international routes and negotiate compensation for grounded aircraft.

Volaris (VLRS) reported its third quarter results last week and the stock has not reacted much, even though EPS of -$0.34 missed expectations by $0.54 while revenues beat estimates by $18.49 million. In this report, I will be discussing the results but I will also discuss some forward-looking items as the focus is shifting to the impact of the issues with the Pratt & Whitney geared turbofan or GTF issues and capacity expansion on routes to the US.

Volaris Manages Margins

{kind=link}

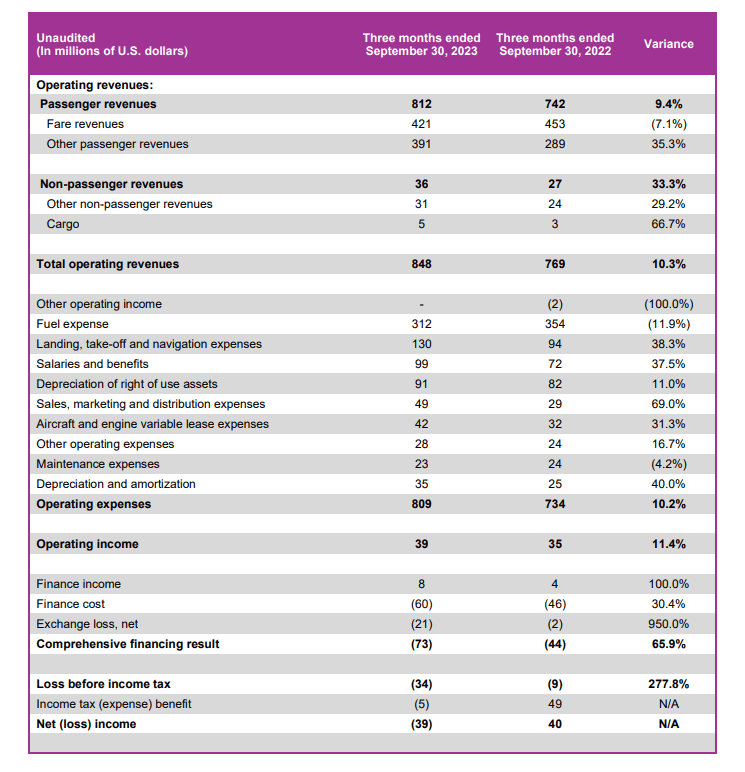

Total revenues increased 10.3% consisting of 9.4% growth in passenger revenues and 33.3% increase in non-passenger revenues. The 9.4% growth in passenger revenues was achieved on an 8.2% increase in capacity and 1.8% increase in unit revenues where a reduction in base fares was offset higher ancillary revenues.

Cost increased in line with revenues indicating that operating margins remained stable. Fuel expenses decreased by 11.9% on a 20% lower economic fuel price per gallon. However, we saw significant cost growth in almost all other segments. Total unit costs increased 1.7% as a result showing that the reduction in oil prices was offset by cost growth on other line items. Excluding fuel, the unit costs increased by 20.6% which seems like a bad thing for a company that prides itself in having a very low cost basis. However, the strengthening of the Mexican peso drove 8% out of the 20.6% increase in unit cost. I looked at the earnings call transcript and what I was missing is any discussions on what drove the costs higher and the expectations going forward. My best guess is that the company is still going through a round of cost inflation that we have been seeing this year.

Overall, the Q3 results were not extremely exciting with stable operating margins despite lower fuel costs. At the same time that puts some pressure on expectations as oil prices have been heading higher providing a high non-fuel cost base and a high fuel cost base.

Volaris Adjusts Guidance

{kind=link}

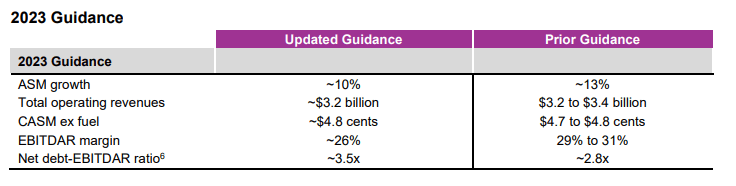

On the back of the GTF issues, Volaris has adjusted its full-year guidance. The company now expects capacity expansion to be in the range of 10% compared to the prior guidance of 13% with revenues coming in at the lower end of the previous guidance and ex-fuel costs being marginally higher than previously expected.

Volaris Eyes International Capacity Expansion

On the Mexican market there will be some changes as the Mexican Aviation Authority has announced a reduction at the Mexico City Airport from 52 to 43 aircraft slots per hour effective Jan. 8, 2024. In the previous quarter we already saw Volaris discussing slot reductions in Mexico City Airport which drove some capacity to underserved markets and Volaris is now eying to redistribute some capacity to international routes. The company will have four airplanes less in Mexico City Airport and will use those to bolster capacity on the Mexico-US routes as Mexico has regained its Category 1 FAA aviation safety rating allowing it to establish new routes to the US. For the fourth quarter, around 20% of capacity expansion is expected in the international market.

Volaris Capacity Plans Are Uncertain Going Into 2024

On the back of the GTF issues, the Volaris capacity plans for the coming years are highly uncertain, which provides a burden as capacity expansion is key to its ability to reduce unit costs. So, while we previously saw significant growth opportunity with the reinstatement of the Category 1 rating, the big question has now become how much capacity will be left to serve the US markets as aircraft are being grounded. Volaris stock has lost more than half of its value due to oil prices heading higher and the geared turbofan issues, but we also have to consider that there will be positive offsets to the capacity issues.

Volaris and RTX Corporation ( RTX ) are discussing compensation for the grounding of parts of its Airbus A320neo family fleet and perhaps amidst a more challenging cost environment that is not necessarily a bad thing. Just a quick calculation assuming that all 52 neo airplanes will require prolonged grounding, and given that 80% of the $6 billion to $7 billion cost of the GTF debacle is earmarked for customer compensations, we would get to a compensation of $160 million to $194 million. The actual compensation is subject to many factors, but we already know that if negotiated well there's a significant compensation package for the issues.

Currently, the company has 16 airplanes grounded and in July and August, the capacity pressure was 3% while it was 8% in September. The company will be extending the lease on 18 airplanes that were initially scheduled to be redelivered in 2024 and 2025. So, the issues with the geared turbofans are not helping Volaris at all but the company will be able to negotiate compensation which also could include unrealized unit cost reduction progress and perhaps even negotiate additional considerations for the future while it will adjust redelivery schedules for which RTX could also carry the compensation. Beyond that the big question will be how much embedded cost the company can cut out of its cost structure.

Is Volaris Stock Still A Buy With GTF Issues?

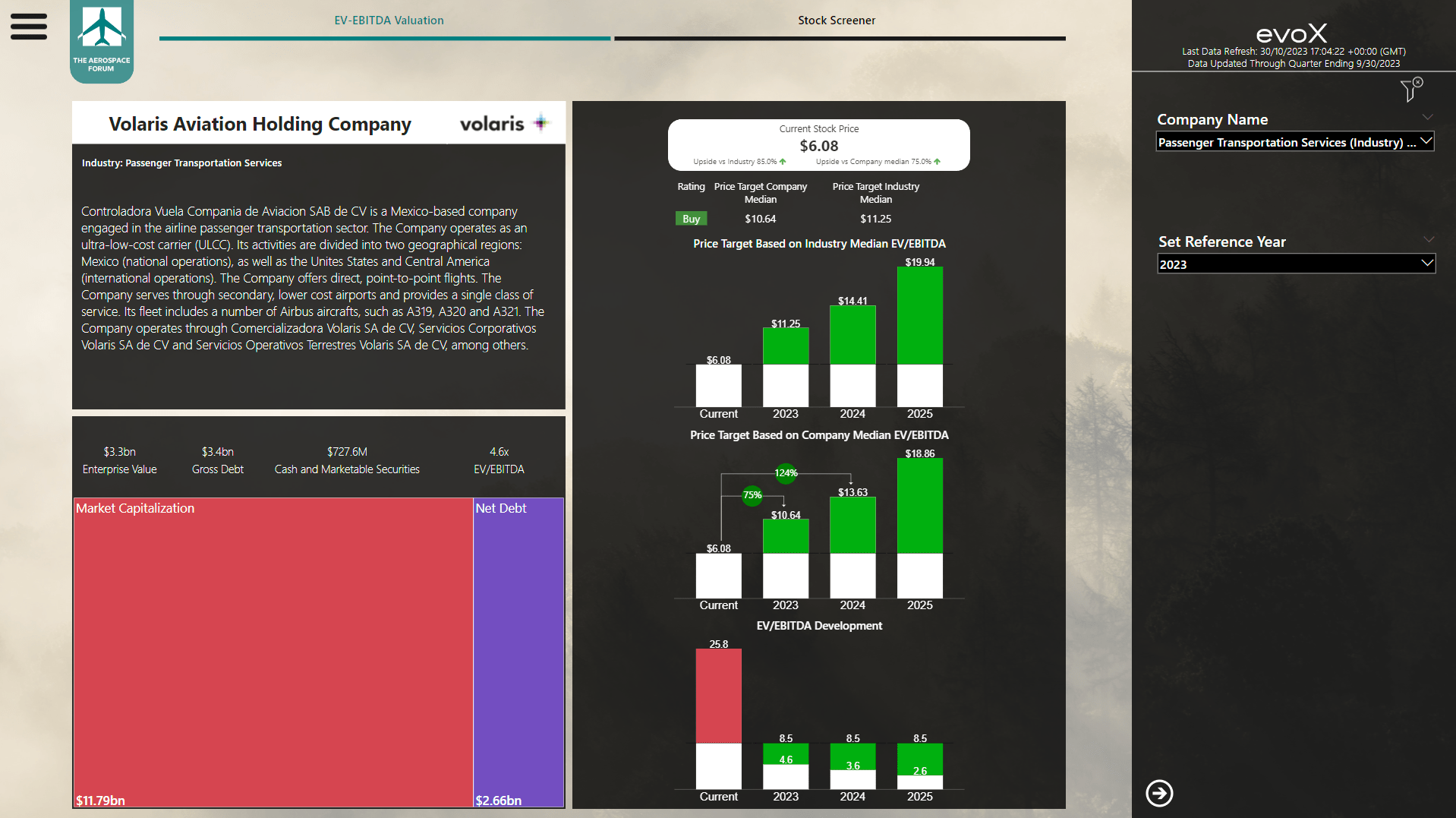

I previously had a buy rating on Volaris stock, but given the lower capacity expansion profile going forward as well as higher oil prices that rating could as well change. So, I have entered the balance sheet data for Volaris as well as forward projections into my model to assess whether the stock is still a buy.

| Changes to EBITDA in $ millions |

| Year |

| Previous |

| New |

| Change |

| Change [%] |

| 2023 |

| $ 774.42 |

| $ 726.22 |

| $ -48 |

| -6.2% |

| 2024 |

| $ 917.03 |

| $ 845.28 |

| $ -72 |

| -7.8% |

| 2025 |

| $ 1,030.59 |

| $ 974.06 |

| $ -57 |

| -5.5% |

| Total |

| $ 2,722 |

| $ 2,546 |

| $ -176 |

| -6.5% |

EBITDA projections have come down quite significantly with 6.5% lower EBITDA in the 2023-2025 timeframe with the biggest reduction in 2024, but overall we see quite notable reductions in estimates in the upcoming years.

| Changes to FCF in $ millions |

| Year |

| Previous |

| New |

| Change |

| Change [%] |

| 2023 |

| $ 346.1 |

| $ 269.5 |

| $ -77 |

| -22.1% |

| 2024 |

| $ 498.5 |

| $ 305.3 |

| $ -193 |

| -38.8% |

| 2025 |

| $ 565.8 |

| $ 507.2 |

| $ -59 |

| -10.4% |

| Total |

| $ 1,410.5 |

| $ 1,081.9 |

| $ -329 |

| -23.3% |

The pressure on free cash flow seems to be more severe with a 23.3% overall reduction and similar to EBITDA reductions, expectations for 2024 have been lowered the most.

{kind=link}

Given the current balance sheet data and reductions to EBITDA and free cash flow, I have significantly reduced my price target by $6.95 for 2023, $11.30 for 2024 and $19.20 for 2025. So, the cut is significant but that does not mean there's no upside. Indeed, investors that stepped in before fuel prices went higher and the capacity pressure became clear will see little to no fundamental upside vs. their cost basis for 2023 and 2024, but the current situation also provides an opportunity to average down on costs as the upside from current levels provides significant upside. So, I'm maintaining my buy rating as I see this as an opportunity to average down and from a fundamental perspective it is not to be equated to catching a falling knife.

Conclusion: Volaris Faces Big Pressures But Stock Has Significant Upside

For investors with a high cost basis, Volaris stock offers little to no upside. Q3 2023 earnings were nothing exciting but the significant reduction in stock price is primarily driven by an inability to execute the planned capacity expansions in the years to come. That, however, does not mean that Volaris stock does not offer any upside for investors taking a position now granted that the market rationalizes a bit rather than having airline names priced as if another global disruptive event is about to happen.

The risk that exists is that the airline industry will see further pressure on unit revenues and oil prices remain elevated, putting further pressure on forward earnings expectations, which is something that could be kept in mind.

For further details see:

Volaris Stock Beaten Down As It Navigates Through GTF Challenges