VLRS - Volaris Stock: Strong Buy On Huge Undervaluation

2023-04-25 13:26:01 ET

Summary

- Volaris Q1 2023 results missed analyst expectations.

- Management has reconfirmed its 2023 guidance with opportunities for international expansion.

- I upgrade Volaris stock to strong buy.

Volaris ( VLRS ) reported first quarter earnings on the 24 th of April. The results missed analyst consensus, but as I discuss in this report, earnings were not extraordinarily weak and in fact, fit in the nature of the first quarter, as I discuss in this report, analyzing the first quarter results and provide a valuation for the airline’s stock price.

Volaris Stock Had Strong Returns

Seeking Alpha

Since I covered Volaris in October 2022, the stock has easily outperformed the broader markets with a 42% return compared to 7.2% for the broader markets. More recently, the stock has underperformed with a 1.1% return compared to the 3.9% for the broader markets, but with opportunities for air travel penetration in the Mexican market, I continue to like the stock.

{kind=link}

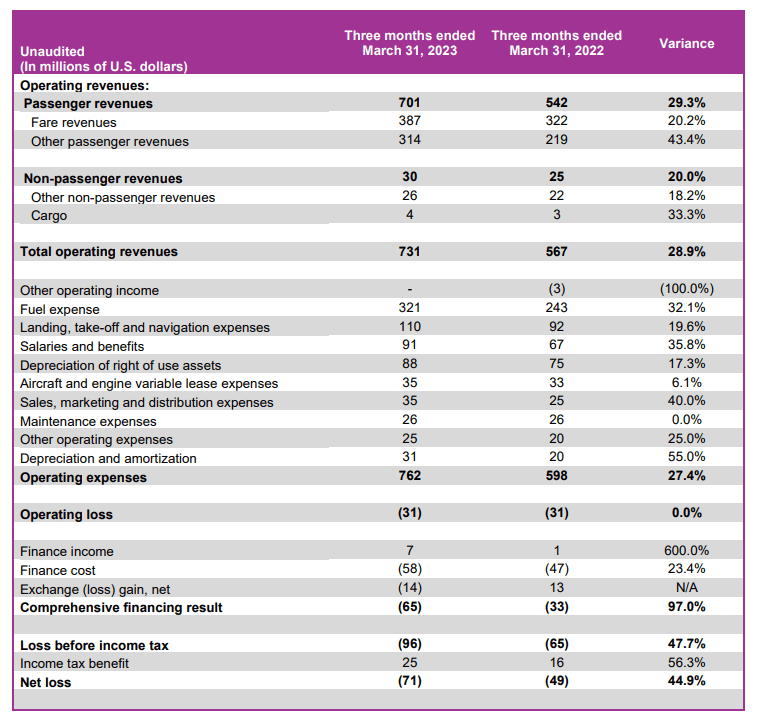

For the first quarter, analysts were expecting revenues of roughly $765 million and earnings per ADS or EPADS of negative $0.40. Total revenues increased by 29% on capacity expansion of 18%. So, we did see revenue growth in excess of capacity growth but the passenger numbers fell short by 0.6 percent points. However, I do think that the biggest part of the miss can be attributed to average base fares only rising 2.4% and the majority of the increase in average fares was actually achieved by higher ancillary revenues. So, it seems that analysts had been expecting higher base fares coupled with the capacity expansion, but Volaris only grew the basis fares modestly.

Looking at costs, we saw that some costs were significantly higher than the 18% capacity expansion or the 11.7% higher departure count. The obvious higher cost component was fuel. With 15.1% more block hours, we could have expected $37.7 million higher fuel costs but the remaining $40.3 million increase in fuel costs was driven by higher fuel prices partially offset by having more fuel efficient airplanes in the fleet. Landing, take off and navigation fees increased by 19.6% but that was mostly driven by inflation escalation on the fees. Taking 11.7% more departures and applying the inflation rate would give 20% higher landing fees and that is also what was reported. So, no major surprise there.

Salaries and sales, market and distribution expenses also grew faster likely as a function of inflation and capacity expansion but I noted that even when incorporating higher capacity and inflation salary growth outpaced the estimate by 7%. This is likely driven by overall shortages of staff in the industry.

The loss per ADS was $0.20 higher than expected or around $23 million higher than expected. I would estimate this was for 25% driven by lower than expected revenues, for 35% by higher than anticipated salaries, around 15% higher distribution costs and the remainder is likely caused by higher fuel prices. The alternative way to view the loss is by keeping in mind that the strong dollar and higher interest rates increased costs. In Q1 2023, there was an exchange loss of $14 million which provides a $27 million swing in negative direction year-over-year while finance costs increased $11 million.

Volaris

The overall pressure for the company has been that it increased its capacity, but it did not translate into lower unit costs. Excluding fuel, the adjusted CASM was around 6.3% higher despite an 18% increase in capacity. Normally, the capacity expansion should roughly have driven down the unit costs by 15% or 9% after the incorporation of inflationary pressures. So, the cost control seemingly was not all that great and that hurts to a company that managed costs quite well in 2022.

For the full year, the company had previously guided for a CASM in the range of 4.6 to 4.8 cents just like what we saw in Q1 on a 10% increase in capacity. Does it bode well for the company? Perhaps not, but it should be pointed out that a strengthening US dollar could help with stronger demand for travel to Mexico driving up the international revenues which would also allow Volaris to move some capacity away from the domestic market where base fares are under pressure.

While it remains unclear where fuel prices will head, fuel prices have dropped from $3.30 to $2.61 from the start of Q1 to the end of Q1 and continued to drop by another 4% in the first two weeks of April. So, lower fuel prices along with the full effect of two fuel efficient Airbus A321neos that were delivered in Q1 and two more on the near-term delivery schedule could help with getting costs down somewhat.

Furthermore, it is likely that the current cost profile already incorporates costs to execute the summer schedule meaning that there will be further capacity additions with little incremental costs added. Furthermore, the 2023 guidance aiming for around 10% growth and a 29 to 31 percent EBITDAR margin has remained in place as well as its $3.2 billion to $3.4 billion in revenues. The capacity guide assumes that by Q4 2023, the safety rating of Mexico will be increased to Category 1 by the FAA, which would allow new services to the US. May that rating change come in earlier, the airline will also be able to deploy capacity earlier.

While the market is not liking the results as the stock is trading nearly 10% lower at the time of writing, I do think it is important to point out that Q1 is naturally a weak quarter that generally is not reflective of the remainder of the year and with Volaris maintaining its guidance that should send a signal that while the results were not in line of market expectations, they were in line with expectations from management.

What Is Volaris Stock Worth?

| Valuation Volaris |

| Market Capitalization [$ bn] |

| $ 1.2 |

| Total debt [$ bn] |

| $ 3.1 |

| Cash and equivalents [$ bn] |

| $ 0.7 |

| Total Enterprise Value [$ bn] |

| $ 3.5 |

| EBITDA 2023 [$ bn] |

| $ 0.9 |

| EV/EBITDA |

| 4.1x |

| WACC |

| 9.2% |

| Current price |

| $ 10.73 |

| Median |

| Current |

| Industry |

| EV/EBITDA |

| 7.61 |

| 55.88 |

| 8.29 |

| Price target |

| $18.32 |

| $134.53 |

| $19.96 |

| Upside |

| 71% |

| 1154% |

| 86% |

With a market capitalization of $1.2 billion, debt of $3.1 billion and cash and cash equivalents, we get to a $3.5 billion enterprise value and with $3.4 billion in revenues and a margin of approximately 25%, we get to 2023 EBITDA of $866 million putting the EV/EBITDA multiple at 4.1x. Using the median EV/EBITDA multiple of 7.6 for Volaris that provides 71% upside. We will reject the current EV/EBITDA multiple of nearly 56x which is unrealistically high for proper valuation while the 8.3x industry multiple provides 86% upside. With that in mind, I do feel comfortable putting a strong buy rating on Volaris stock with an $18.30 price target, which is slightly higher than the $17.96 target that Wall Street Analysts have.

Conclusion: Volaris Stock Is A Strong Buy

While Volaris stock might be trading down today due to some weaker-than-expected results, management indicated that these results were in line with expectations and reconfirmed its full year guidance. CASM will remain elevated this year and there is some weakness on the domestic market, but the international market does offer an opportunity for Volaris to shift capacity into these markets and if a Category 1 rating is achieved, we will see more international expansion which also allows for the new Volaris airplanes to be providing even more efficiency as they are utilized on longer routes. Looking at the expectations for this year, I do believe that Volaris is significantly undervalued.

For further details see:

Volaris Stock: Strong Buy On Huge Undervaluation