VLRS - Volaris: Strong Cost Control Lifts Stock Price

Summary

- Volaris has shown strong cost control in 2022.

- Building on that cost control, lower fuel prices, and higher unit revenues, the airline is aligned for a better year in 2023.

- VLRS stock has returned 44% since I initiated coverage, and there seems to be more in it for the Mexican airline.

In November 2022, I covered Volaris ( VLRS ) for the first time and what I noted was that while there were significant cost pressures from higher fuel prices, the company showed extremely strong cost control and that is something we see back in the full-year results discussed in this report.

Volaris: A Mexican Airline With Popping Stock Return

Seeking Alpha

While I did point out the risks that Volaris faces like any other airline, I provided a Buy rating on the stock and what we see is that this has played out quite well with the stock returning 43.8% compared to a positive return of 2.4% for the broader stock markets.

Volaris: Strong Cost Control On Display

{kind=link}

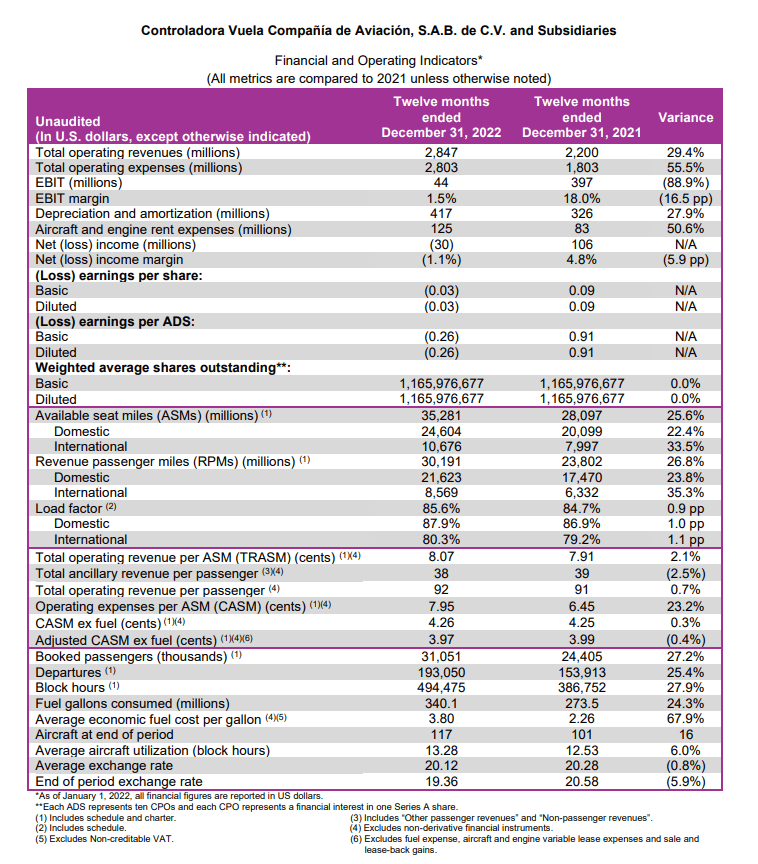

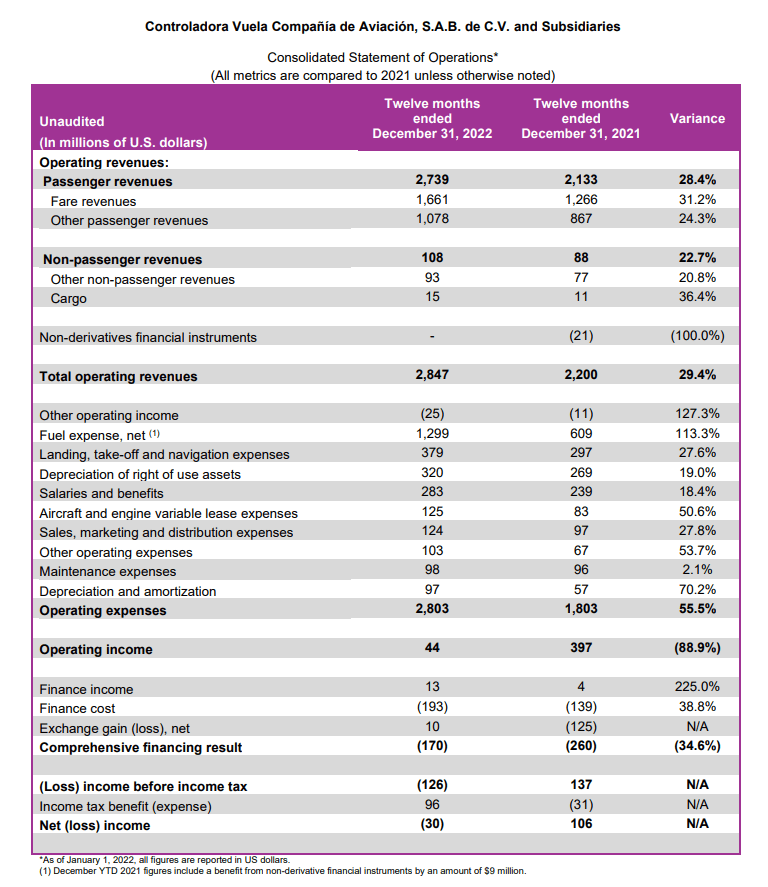

Year-over-year, EBIT declined by nearly 90%. What we see is that revenues rose by 29.4%. This was primarily driven by a 27% increase in passenger volumes while revenue per passenger was up less than a percent. So, what we see is that the growth is not driven by unit revenues passing the higher costs to the passengers. CASM per available seat mile was up 23%. So, we see that profitability during the year was eroded by higher fuel prices.

{kind=link}

Taking a deeper look at the costs what we see is that Volaris managed costs quite well. With around 25% more departures you would expect total costs to at most rise roughly the same. When we apply that to the $1.8 billion in costs for the year, we would get to roughly $2.2 billion in costs. Actual costs were $2.8 billion driven by higher fuel prices and lease expenses. So, what we see is that despite 7.8% annual inflation in Mexico, unit costs excluding fuel were stable which I think is impressive and shows strong cost control. Especially for low-cost carriers, which are somewhat hesitant to raise fares having strong cost control is important and Volaris has shown a strong execution on costs. In fact, it has one of the lowest ex-fuel unit costs among low-cost carriers worldwide.

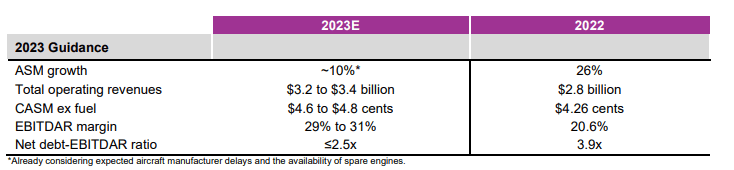

2022 Outlook More Or Less The Same

{kind=link}

In 2022, Volaris delivered on its guidance. For 2023, we see that the company expects a 10% and an 18% increase in revenues at the midpoint signaling that revenue per passenger is going to increase. Unit costs at the midpoint will be around 10% higher. While there is growth in the unit costs despite capacity expansion, it is important to note that this is not driven by labor costs or inflationary pressures but by pre-delivery and redelivery expenses during the year as the company expects first deliveries of the Airbus A320neo aircraft ordered by back in 2017. EBITDAR margins will increase from 20.6% to around 30% driven by higher unit revenues and significantly lower unit fuel costs.

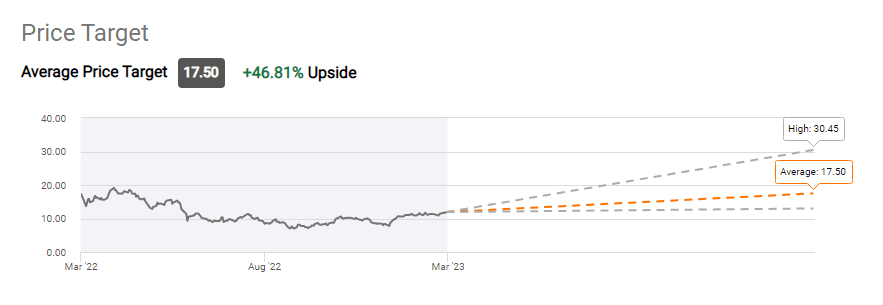

What Price Target Does Wall Street Have On Volaris Stock?

{kind=link}

Wall Street analysts are expecting a lot from Volaris in the coming 12 months with a 47% upside from current price levels, and if we look at the strong cost control, easing fuel prices and continued growth in volumes as well as unit revenues I can understand why.

Conclusion: Volaris Stock A Buy On Strong Cost Control And Growth

In November, I already highlighted the strong cost control and that will also benefit the carrier this year as revenue growth is expected to outpace capacity growth and significant EBITDAR margin expansion driven by this as well as lower fuel prices. As a result, I do believe that shares of Volaris remain attractive in 2023.

For further details see:

Volaris: Strong Cost Control Lifts Stock Price