VWAPY - Volkswagen: New CEO Is Taking The Right Steps On Software

Summary

- The way Volkswagen developed software over the last few years caused the group to fall behind its competitors, especially in China.

- The new CEO does a lot of things right; there is a renewed focus on developing features for customers/cars instead of announcing partnerships and investments with an unspecified outcome.

- Aside from software, which is very important, Volkswagen has been making progress in terms of its EV transition.

- Key risks like the macro environment in 2023 and dependency on China remain, but Volkswagen AG seems mispriced and I think it's undervalued.

- The group's market capitalization is less than its stakes in the publicly traded subsidiaries Porsche and Traton.

Over the last few years, Volkswagen AG (VWAGY)(VWAPY)(VLKAF)(VLKPF) developed software in a way that made it fall behind its competitors, especially Tesla (TSLA) and Chinese auto manufacturers. Multiyear initiatives within the group, but also with partners and vendors that cost billions, were begun with big announcements, but delivery dates for the vaguely specified value were years out. The initiatives were usually late and underdelivered, if they were not cancelled after huge sums had been wasted and not much was achieved.

The new CEO does a lot of things right, and he seems to understand the software problem. Large and high-profile programs are being cancelled. There is now a clear focus on delivering value and features that customers want quickly and iteratively. In China, where the software problem is especially acute, Volkswagen has taken steps to develop unique features for the Chinese market locally instead of from the German delivery centers.

For investors who are aware of the challenges and risks, this might be a good time to buy. The risk/reward ratio seems compelling right now. The Group's market capitalization is less than its stakes in the publicly traded subsidiaries Porsche (POAHY) and Traton (TRATF).

Recent mistakes on the software side

I want to start with a personal note and disclosure: I am a software engineer and have run engineering teams. I provide advice to companies on how to set up their technology teams for a digital transformation. I freely admit, however, that Volkswagen AG is above my pay grade. Still, as a practitioner it hurts me to see how Volkswagen almost created a textbook example of how not to do it: align hard product roadmaps to the success of large software development initiatives that have a vaguely defined scope and delivery dates that are years in the future.

Based on his actions, the new CEO Oliver Blume understands the problem. The lack of progress on the software side was supposedly a major reason his predecessor Herbert Diess was fired. But before we examine Blume's actions, first let's look at three examples what went wrong to help explain why the future looks better.

1. Argo AI

Oliver Blume replaced Herbert Diess as Volkswagen CEO in September. Blume is a Volkswagen insider and also simultaneously the CEO of Dr. Ing. h.c. F. Porsche AG. Blume went to work quickly - one of his first major decisions was to shut down Argo AI, an autonomous driving technology joint venture together with Ford (F).

Argo AI was founded in 2016. In 2020, Volkswagen invested USD2.6bn in the company (1bn in cash and its own Autonomous Intelligent Driving unit - valued at USD1.6bn billion). Ford and Volkswagen each had a 42% share.

Argo AI was supposed to develop a Level 4-capable self-driving system (with ridesharing and delivery as the main applications), but delivery for production use is still years out. Instead of the moonshot, both Ford and Volkswagen said they want to focus on creating more immediate value through L2+ and L3 applications that can be delivered to customers in a much shorter time frame. In my opinion, this was completely the right thing to do. But for Volkswagen it was an expensive USD2.6bn lesson.

2. Trinity Project

While Argo AI just wasted a lot of money, the Trinity project did more harm than that. The project was started in 2020 to develop a completely new electric car together with fully networked production processes in the factory (so a new factory was also planned). Completely new car software - 2.0 (1.2 and 1.1 are used currently) - was to be introduced for the whole group. The new software was supposed to be developed by the subsidiary CARIAD (more on that company later).

The new car platform was originally planned for 2025, then moved to 2026. At the beginning of 2022, Audi CEO Markus Duesmann brought in external McKinsey consultants to assess the status of software development. The result was devastating: All projects that were planned for software 2.0 designed for Trinity were delayed and significantly more expensive. The implications for product roadmaps are quite negative. The new Porsche Macan, designed as a purely electric car, will be launched around two years later than originally planned. The first electric car from Audi's future project, Artemis, will likely arrive in 2027 instead of 2024.

In mid-November, Blume cancelled the Trinity project for the time being. Instead, Blume is now preparing VW to keep maintaining the current software platforms, 1.1 and 1.2. Software version 1.2, which is particularly important for the premium brands Porsche and Audi, will now be upgraded so that it can remain in place until the end of the decade. According to the German newspaper Handelsblatt , that alone costs significantly more than one billion euros. There is no information available on how much money has been spent so far, but we should assume that it is again a number in the low billions.

3. CARIAD

In 2020, VW founded "Car.Software.Org," a software project house for all brands of the group. The Volkswagen Group should not only build the best and most efficient electric cars - VW, Audi, and Porsche should also develop the best software together to beat Tesla. The company was later renamed to CARIAD:

{kind=link}

The emphasis was on developing a completely new Volkswagen software stack in house, and to do it centrally in one place for all brands. CARIAD has around 5,000 software developers, mostly in Germany as this is where the existing Volkswagen teams are located. From CARIAD's website :

We are an automotive software and technology company that bundles together Volkswagen Group's software competencies and further expands them, building upon a heritage of bringing automotive innovation to everyone.

Not surprisingly, the initiative was plagued with issues from the start. Brands were reluctant to hand over their engineers to CARIAD and everybody argued about responsibilities, priorities, and co-determination rights. Instead of software, CARIAD produced frustration at all levels of the group. The entire thing also spilled into the public through LinkedIn posts, such as this one from the now-replaced CEO Herbert Diess :

We have to scale down the influence from the VW Group into CARIAD processes. We need a culture which is customer-oriented, fast, and agile. I will support this as new CARIAD Supervisory Board Chairman from now on - looking forward!

Meanwhile, CARIAD continued to make announcements about big things coming in several years instead of delivering now. Press releases in November 2022 still included statements like this one :

From the middle of the decade, we aim to have one uniform, global platform that will connect all customer cars from all Volkswagen Group brands.

In the present time, Volkswagen brands have been late introducing even essential features like over-the-air-updates . By way of comparison, Tesla introduced the feature in 2012 with its Model S Sedan. Volkswagen is also falling behind Chinese EV competitors , with China being Volkswagen's largest market.

Changes the New CEO Is Making

CEO Oliver Blume presented a new software strategy to the Volkswagen Board on Dec. 15, when it was approved. It was reported that the group is aligned on the postponement of Trinity and incremental development of the current software platforms 1.1 and 1.2.

For the time being, development of L4 and L5 autonomous driving will be moved to a development within the VW Commercial Vehicles subsidiary that is more focused on the business value of autonomous robotaxis and delivery. VW Commercial Vehicles might have a boring name, but they have released the ID.Buzz in 2022, which shows that Volkswagen has not lost the ability to build exciting and even iconic cars.

For the other brands, the focus will be on developing L2+ and L3 autonomous systems - good advanced driver assistance systems. I agree with these moves and they should help Volkswagen to be at least on par with competitors.

Local Development in China

The place to examine to see whether or not Blume is making progress is probably China. China is Volkswagen's largest and most important market, but Volkswagen is losing market share there. In the first nine months of 2022, Volkswagen market share dropped to 14.1% from 17.5% the year before. If this continues, it will be very difficult to make up for those sales in other regions.

There are obviously more factors here at play than just the lack of digital features in its electric vehicles. On the software side, the company has reacted and decided to develop software for the Chinese market locally. It also announced a joint venture with Horizon Robotics "to speed up customization of automated driving solutions for the Chinese market," realizing that developing software for the Chinese market from Germany (and the U.S. to a lesser extent) is not going to work.

Current Valuation

Outcomes remain to be seen and investors should look what happens over 2023 to evaluate the investment thesis. But Volkswagen's current valuation makes the risk/reward ratio appear very compelling, in my opinion. After a 19.5% drop in 2022 and the recent special dividend due to the Porsche IPO, Volkswagen AG has a market capitalization of EUR 70.1bn.

The 75% stake in Dr. Ing. h.c. F. Porsche AG is worth EUR65.6bn at a share price of EUR96. The IPO included only preferred shares that have no voting rights, so this even assumes that shares with and without voting rights are worth the same, which is obviously understating the value. In addition, Volkswagen AG also owns 89.7% of Traton, which currently has a market cap of EUR7.1bn. So, the rest of Volkswagen AG - aside from Porsche and Traton - is valued at a negative number (EUR-1.7bn).

Risks

The valuation argument rests on a sum-of-the-parts calculation. Obviously, if the parts are worth less than what the calculation assumes, the argument fails. In this case, it's the valuation of Porsche AG that is the biggest risk. With a 2022 P/E around 17 Porsche is not very cheap for an auto manufacturer. Also, Volkswagen does not have a good track record with its IPOs. Traton has lost 47% since its IPO in June 2019.

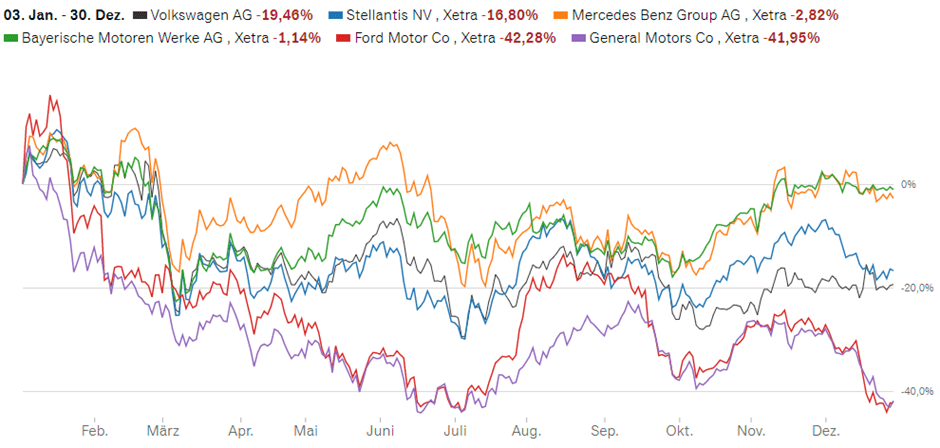

As a matter of fact, Volkswagen shares have not dropped less in 2022 than other auto manufacturers. The chart below compares Volkswagen preferred shares to Stellantis (STLA), Ford, GM (GM), and the two other large German auto manufacturers, Mercedes (MBGAF) and BMW (BMWYY).

{kind=link}

The drop is in line with Stellantis; Ford and GM have dropped significantly more - although this is seen from a euro perspective. 5.7% of the drop is due to the stronger U.S. dollar. Only the two luxury car manufacturers held up better in 2022.

I think the biggest risk is that the macroeconomic environment deteriorates significantly in 2023. This will affect Volkswagen, just as it will other auto manufacturers.

Conclusion

Execution is key here and there is tremendous pressure on the new CEO to deliver. So far, he has shown an inclination for decisive and quick action and, in my opinion, done the right things.

This has not been rewarded by investors yet, making a Volkswagen a good investment with a compelling risk/reward ratio. It could take some time, so investors should have a time horizon of one to three years depending on market conditions and the macroeconomic situation. The preferred shares were trading at their high at EUR246 in Q2 2021. I see this as the target price, which means investors could double their investment.

For further details see:

Volkswagen: New CEO Is Taking The Right Steps On Software