VLVOF - Volvo Car: Transforming With BEVs And DTC Changes

2023-04-30 04:31:18 ET

Summary

- BEV sales have been strong the last two quarters and they now account for 18% of overall unit sales.

- The UK is their third biggest market and management is hoping it will soon be 100% direct.

- There is so much interest in the new EX90 BEV that Volvo Car had to close the order book.

Introduction

My thesis is that Volvo Car Group ( OTCPK:VLVOF )( OTCPK:VLVCY ) is in the midst of a transformation. Along with delivering more battery electric vehicles ("BEV") units, Volvo Car is investing heavily in software and they are moving to a direct-to-consumer ("DTC") model. Volvo Car CEO Jim Rowan explained in a June 2022 interview that the automobile industry is going through a transformation with tech and electrification on one side and a shift from dealers to a DTC model on the other side. He summed things up by talking about what we learned when transforming from old phones to smartphones:

The smartphone enriched that product to a level that no one had envisaged. The [number] of things that you could do with the smartphone that you couldn't do [with] a feature phone - and how it became a part of your everyday life - was transformational. And the same thing is going to happen in the auto industry, or the next generation mobility industry, as I prefer to call it.

Sometimes it seems smoother to shorten "Volvo Car Group" to just "Volvo Car" and other times it seems fitting to quote statements that use "Volvo Cars." Much of this can be explained by the general definitions in the 1Q23 report :

Volvo Car AB (publ.) together with its wholly-owned subsidiary Volvo Car Corporation and its subsidiaries are jointly referred to as "Volvo Car Group" or "Volvo Cars".

At the time of this writing, 100 SEK is about $9.74.

Shifting To BEV Units

This statement in the 2022 annual report jumped out at me:

It is now widely accepted that the age of the internal combustion engine is coming to an end.

It's one thing for new electric-only companies to say things like this but hearing it from a legacy OEM like Volvo Cars is different. At about the 19:00 mark of the 1Q23 webcast , CEO Jim Rowan answers a question about e-fuels by saying they're a distraction as Volvo Car and the rest of the world move towards electrification. He states that the technology in electrification and the underlying efficiencies are completely different from ICE, citing percentages that an ICE is only about 35% efficient regardless of fuel type whereas a BEV is over 90% efficient. He also points out the obvious fact that BEVs require far less in terms of servicing for customers.

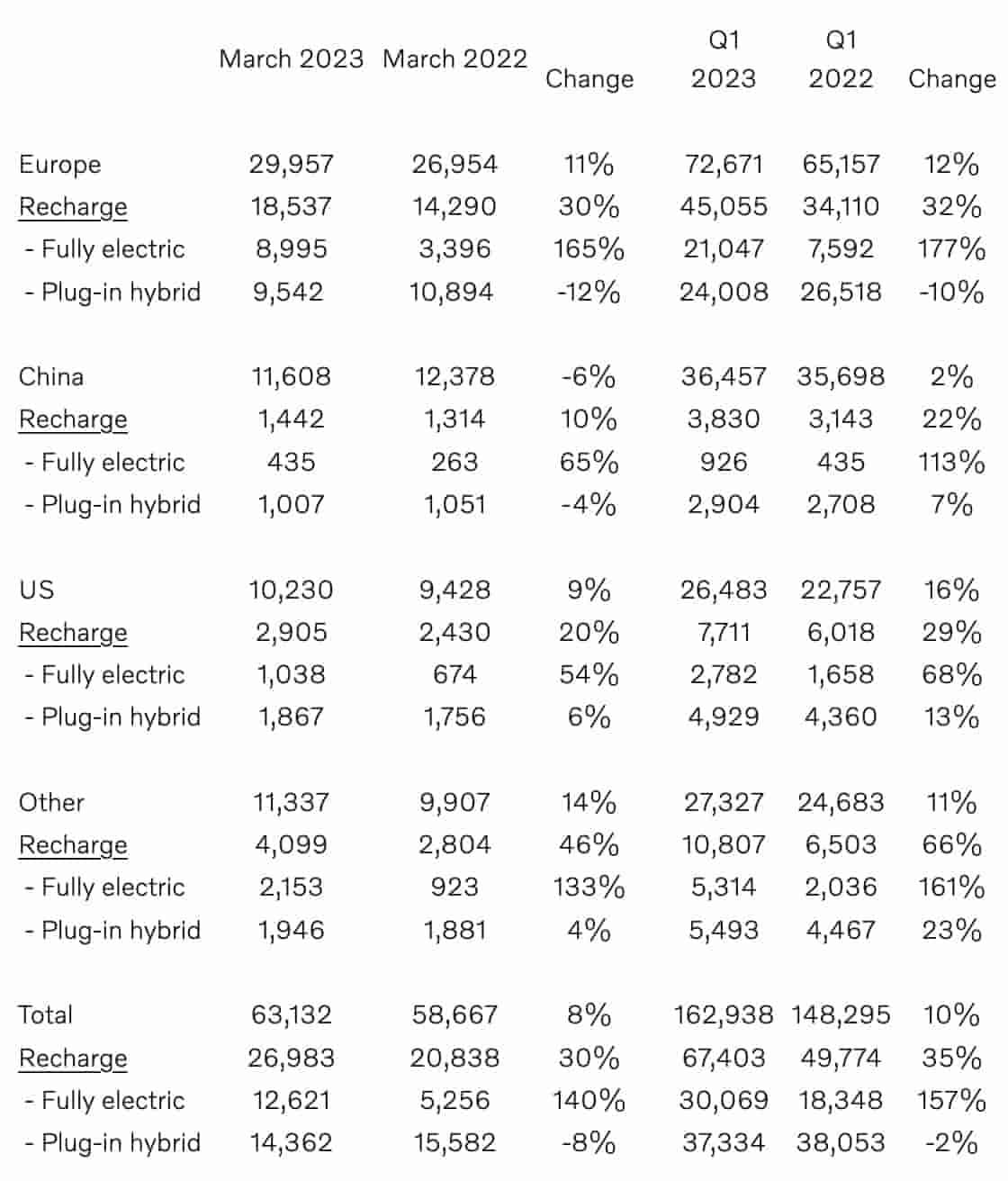

The annual report shows the XC40 BEV improved from 24.5 thousand units in 2021 to 42.5 thousand in 2022. The C40 BEV went up even more dramatically from 1.2 thousand units in 2021 to 24.2 thousand in 2022. As a percentage of overall units, BEVs were only 1% of overall sales in 2020 but this increased to 4% in 2021 and 11% in 2022. The March 2023 delivery press release shows BEVs going up 157% from 18,348 units in 1Q22 to 30,069 units in 1Q23 and they have been close to 18% of overall sales in 4Q22 and 1Q23:

Volvo Car Deliveries (March 2023 delivery press release)

{kind=link}

Talk of upcoming SUV BEV models in the 1Q23 report was exciting. Having to close the order book for the new EX90 BEV is an encouraging sign with respect to demand:

Speaking of our ongoing transformation, last year we took a decisive step into the future with the global launch of our new born-electric flagship SUV, the Volvo EX90. And I feel proud that the customer response to that car has surpassed our boldest and most ambitious internal projections. As a ??result, we have now had to close the order book for the time being because the model year is sold out, but we will re-open again soon. This tremendous reception to the Volvo EX90 gives us renewed confidence in our strategy and roadmap for the future.

The 1Q23 report goes on to talk about a small SUV BEV (emphasis added):

2023 will be another crucial year in our transformation. In a few months, we will reveal a new fully electric small SUV to the world, which will take us into a new demographic and with a competitive price point. This new car will build on the strong customer response to the Volvo EX90 . With these two new state-of-the-art SUVs, we will cover both the top end of the premium electric market and the entry level premium segment. Together, they will complement our existing line-up of fully electric XC40 and C40 . This sets us up for a future with strong growth and improved profitability on our fully electric cars.

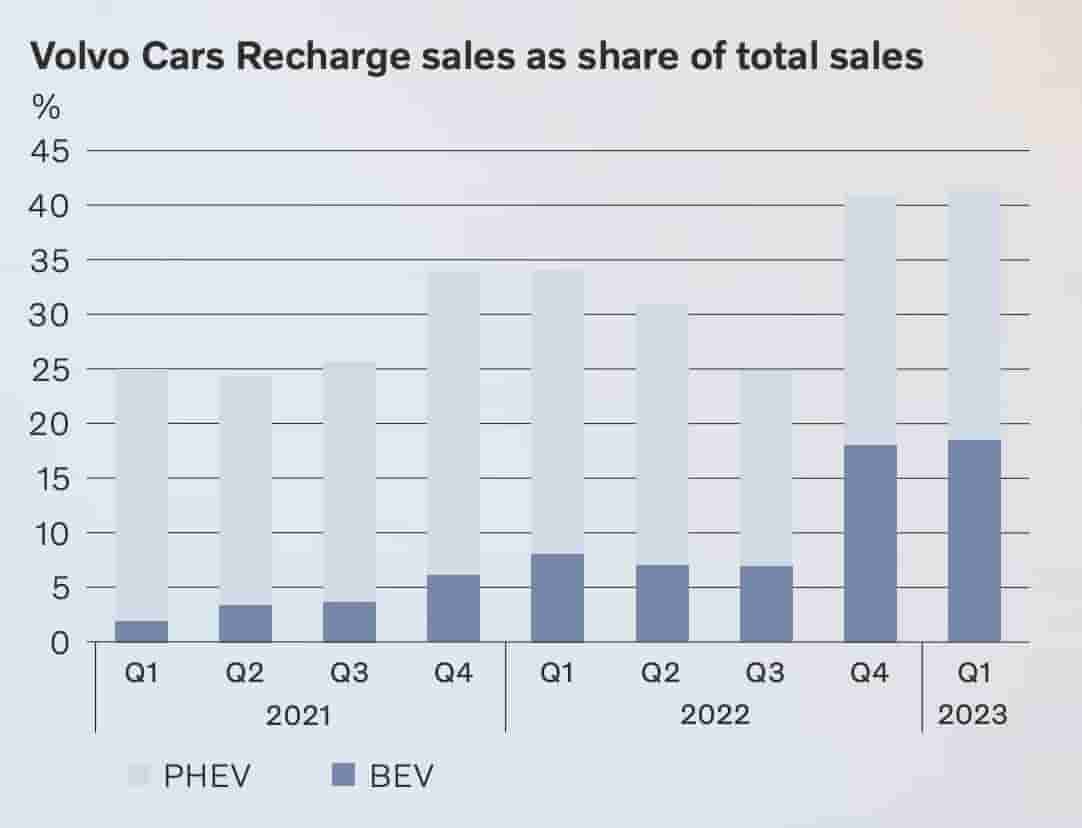

Per the 1Q23 report, BEVs are now about 18% of overall unit sales for Volvo Car. The inflection point was when we jumped from far less than 10% in 3Q22 up to well more than 15% for 4Q22:

{kind=link}

Unlike ICE vehicles with limited batteries, BEVs have enormous batteries such that digitalization is going to a new level. Volvo Car is taking advantage of the enormous batteries in their BEVs by making substantial software investments.

Moving Towards DTC

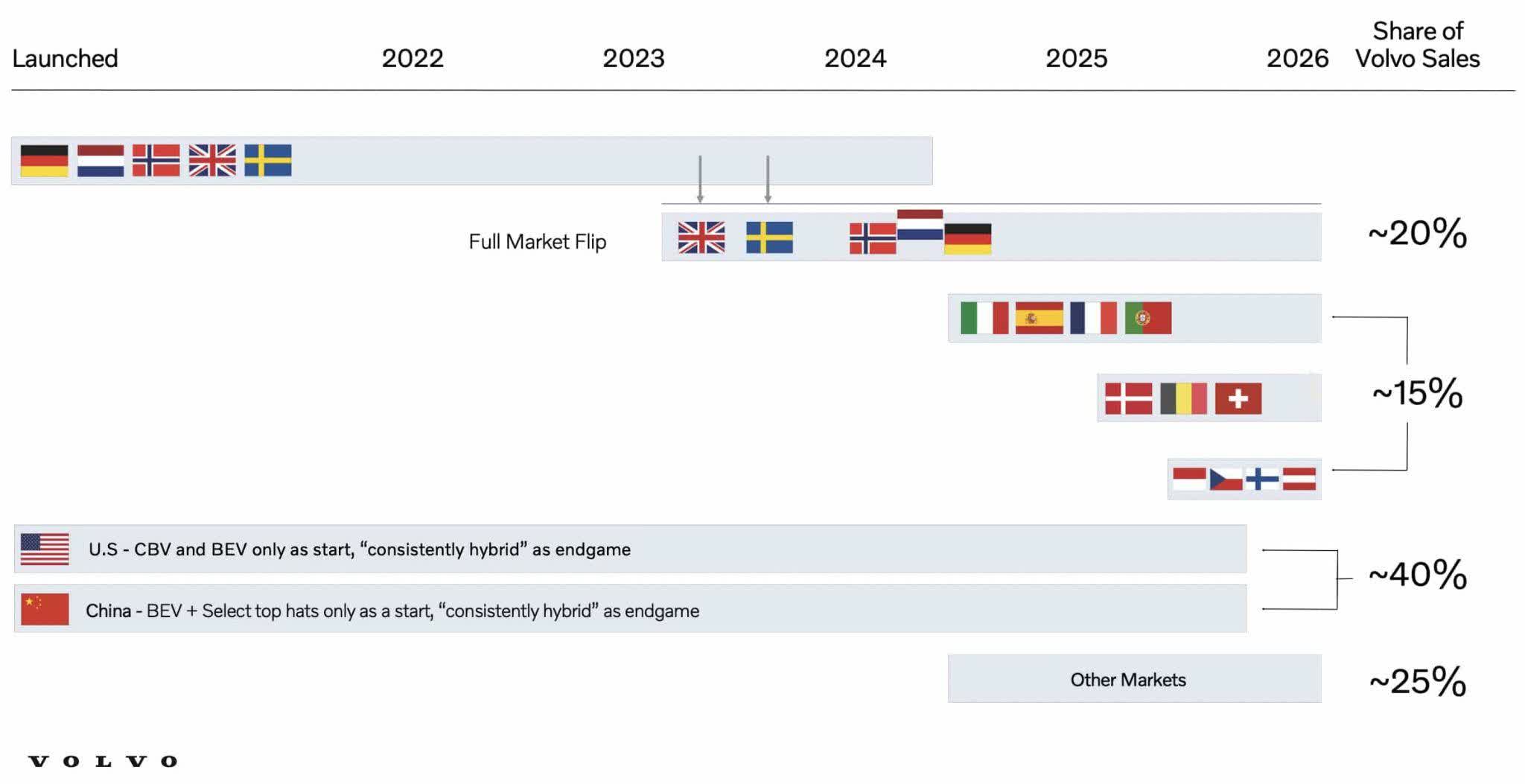

The UK is Volvo Car's third largest market and 2023 will be a pivotal year per the 2022 annual report because the UK will become the first 100% direct market. Volvo Car aims to have 50% of their global sales online by mid-decade. The commercial capabilities presentation from the November 2022 capital markets day shows that Sweden is joining the UK soon with this full market DTC flip:

DTC flip (November 2022 capital markets day)

{kind=link}

The 1Q23 report describes the way this DTC is happening and it reveals that the online/direct percentage will be an important metric moving forward:

Our strategy is to establish direct relationships with our customers, something we do by using an omni channel approach with online being an important route. The online/direct business model is available in 10 markets and is defined as a car ordered online with transparent online price and direct invoice where available. For US and Canada, the transaction is executed by our retail partners as per our agreement with retailers and in line with franchise laws. For Q1 2023, the share of online/direct business in the markets where the offer is available amounted to 8 (10)% of total sales in those markets and expressed as share of total global sales, it was 5 (6)%.

Valuation

Entrepreneur Li Shufu controls Zhejiang Geely Holding Group ("Geely Holding") which has vast interests including Geely Automobile (GELYF)(GELYY)[GELLY]. Additionally, Geely Holding has an enormous interest in Volvo Car per the 2022 annual report:

The largest owner, holding 82% of shares and capital, is Geely Sweden Holdings AB, owned by Shanghai Geely Zhaoyuan International Investment Co., Ltd., registered in Shanghai, China, and ultimately owned by Zhejiang Geely Holding Group Ltd., registered in Hangzhou, China.

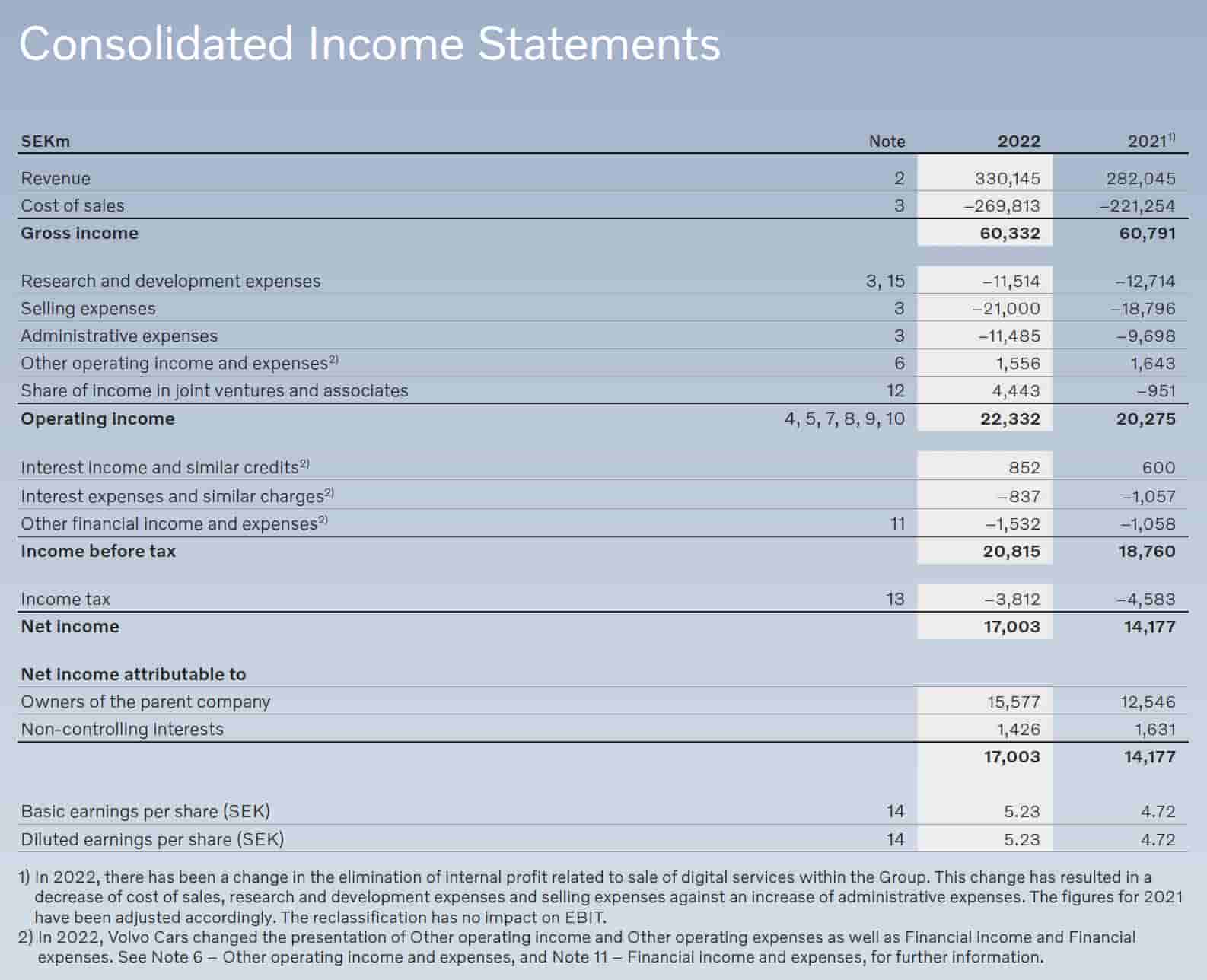

The 2022 annual report shows improvements in net income, operating income, gross profit and revenue from 2021 to 2022:

Income statement improvements (2022 annual report)

{kind=link}

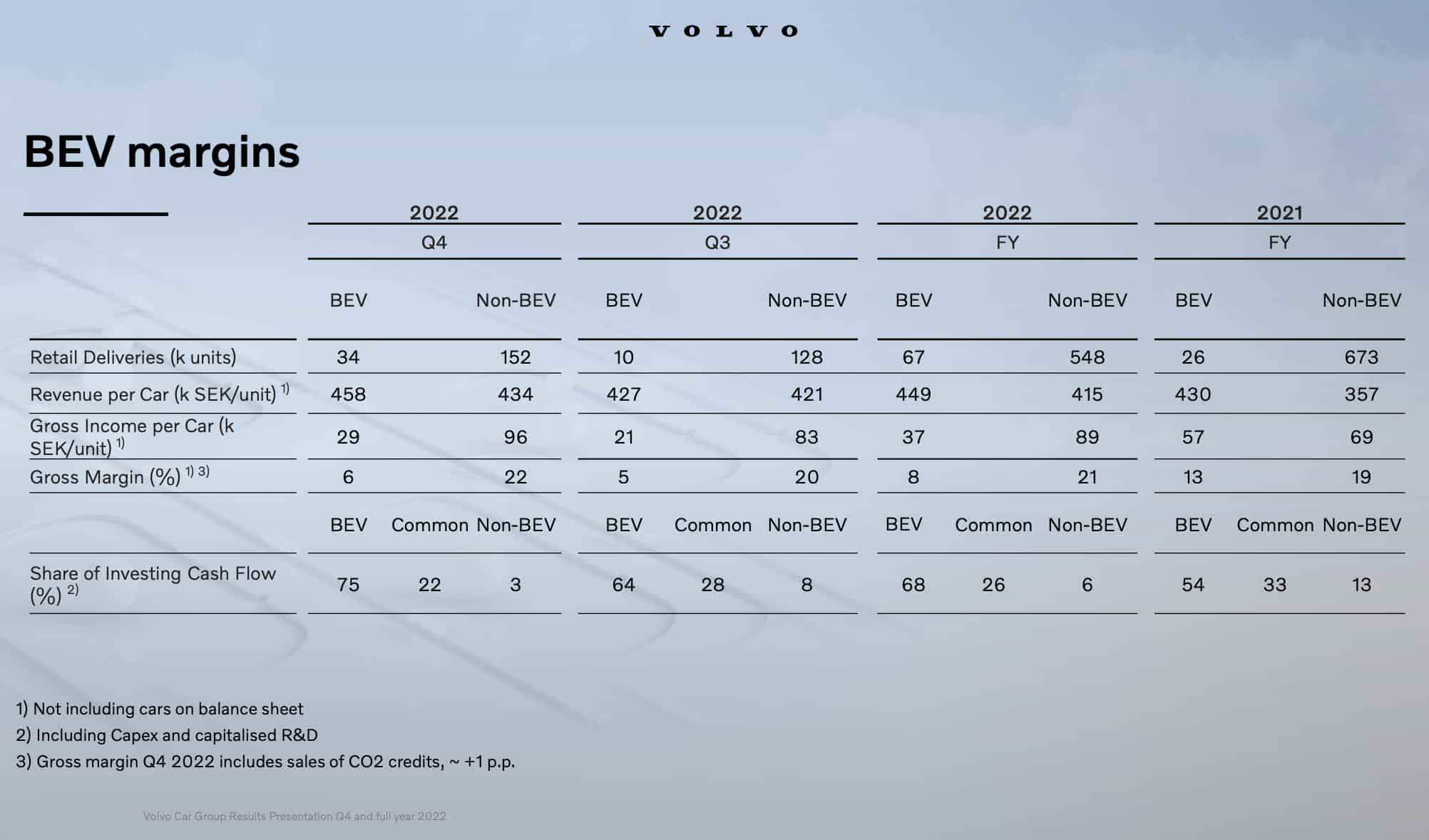

Volvo is one of the only legacy OEMs I've seen that breaks out the gross margin for BEVs. Per the 4Q22 presentation , their gross margin for BEVs was 13% for 2021, 5% for 3Q22, 6% for 4Q22 and 8% for 2022:

BEV margins (4Q22 presentation)

{kind=link}

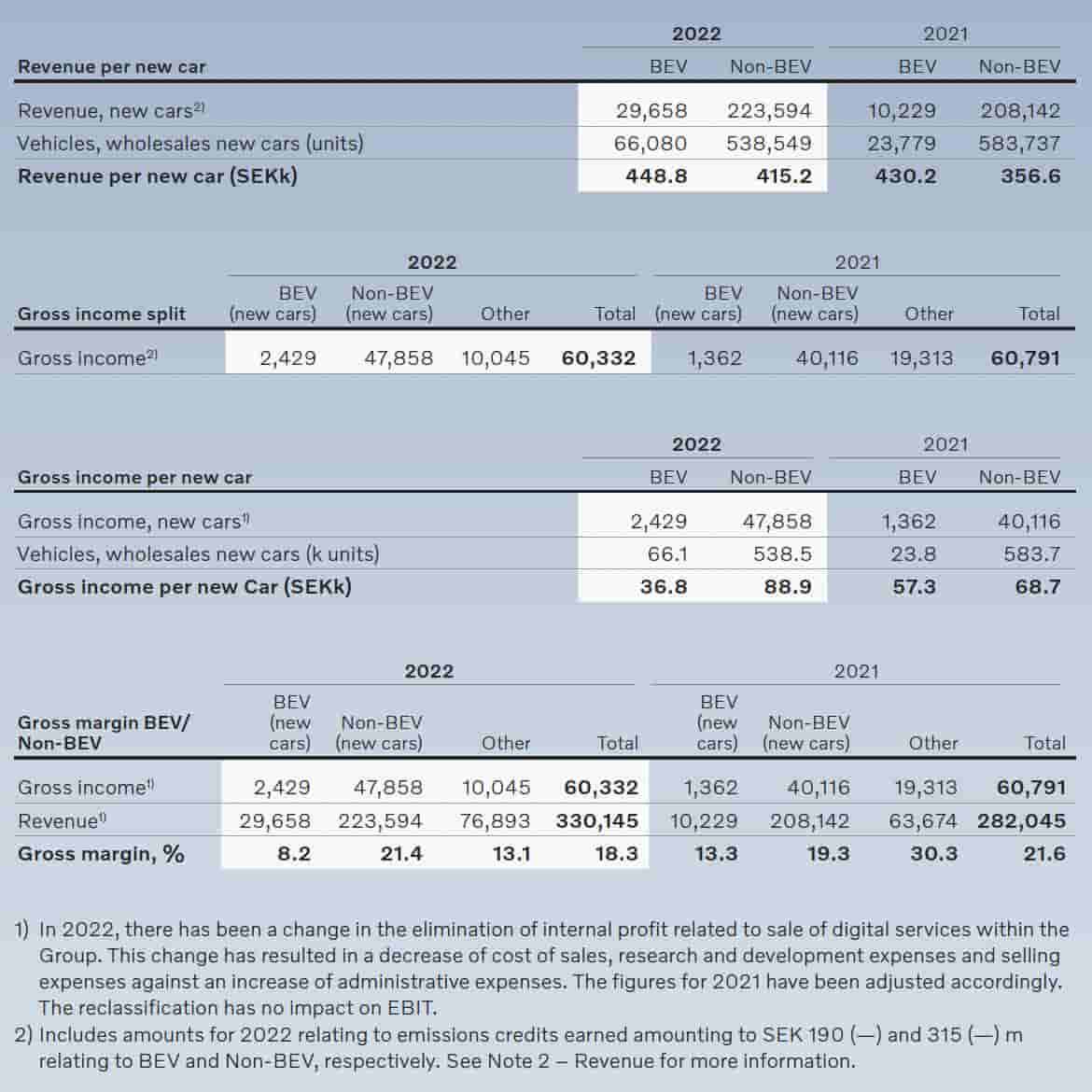

Looking at BEV and non-BEV margins on an annual basis, we see in the 2022 annual report that the BEV gross margin was 13.3% in 2021 while the non-BEV was 19.3%. Things got worse for BEVs in 2022 as their gross margin dropped to 8.2% while the non-BEV gross margin was at 21.4% which was a slight improvement:

BEV results (2022 annual report)

{kind=link}

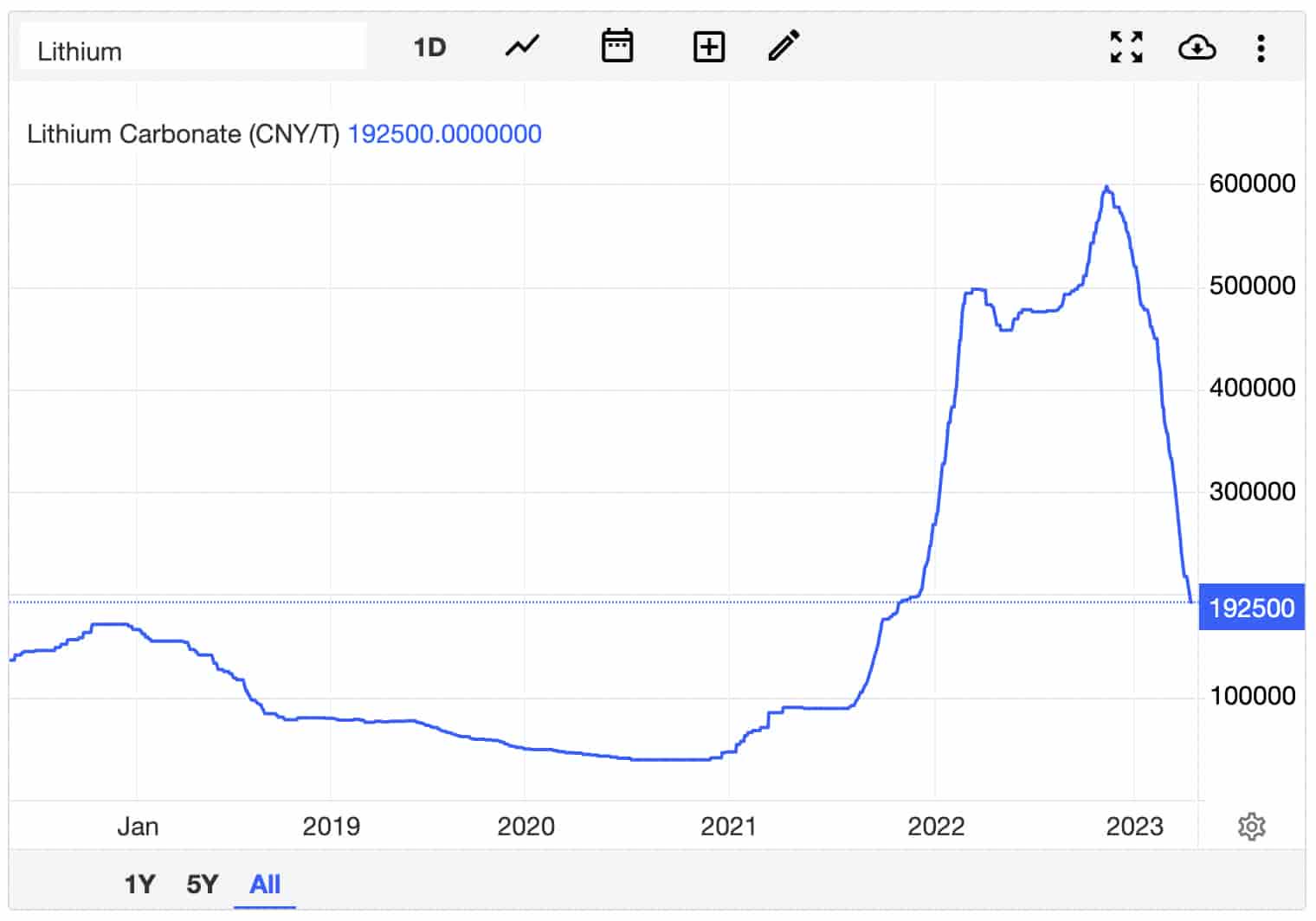

In the 1Q23 presentation , we see BEV gross margins improving slightly from about 6% in 4Q22 to about 7% in 1Q23. Forward-looking investors need to watch the BEV margins carefully for the remaining 2023 quarters. A question was asked during the 4Q22 webcast about hypothetical BEV margins without elevated lithium prices. The answer was that 4Q22 was absolutely impacted heavily by lithium prices. The price of lithium has dropped substantially since the end of 2022 per Trading Economics and we should see benefits from the drop in the remaining quarters for 2023:

Lithium prices (Trading Economics)

{kind=link}

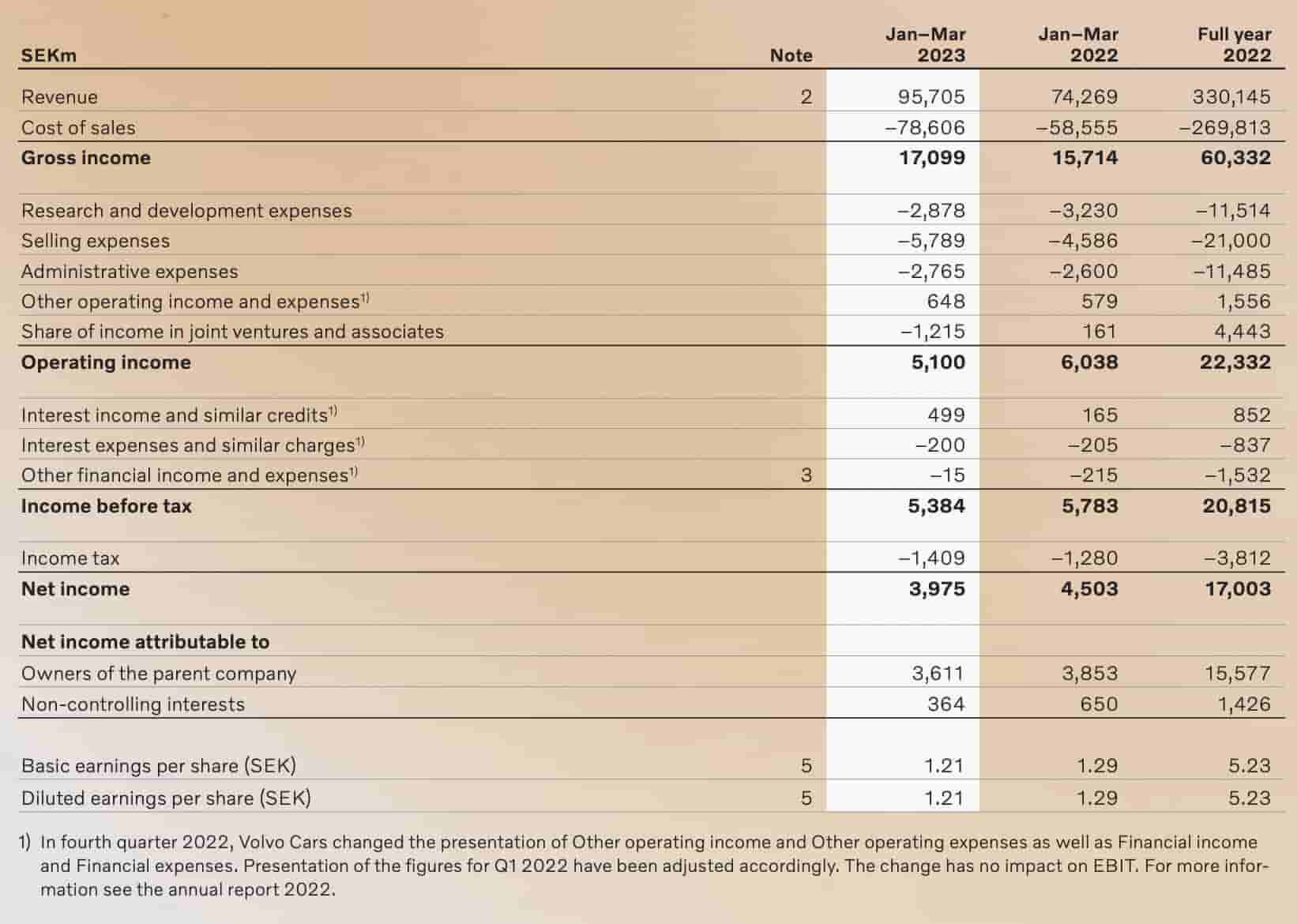

Per the 1Q23 report, operating income dropped from SEK 6,038 million in 1Q22 down to SEK 5,100 million in 1Q23 due to the change in the share of income in joint ventures and associates which fell from SEK 161 million in 1Q22 down to SEK (1,215) million in 1Q23:

Income statement (1Q23 report)

{kind=link}

One piece of encouragement that stood out to me in the 1Q23 report is the fact that pricing actions can be taken when EBIT improvements are needed (emphasis added):

Our EBIT, excluding joint ventures and associates, increased 7 per cent in the first quarter, compared to the corresponding period last year, to reach SEK 6.3 bn, translating into an EBIT margin of 6.6 per cent. The increase in EBIT was delivered despite raw material prices remaining at elevated levels. This performance was the result of higher volumes sold during the period, increased price realisation per car, a favourable geographical mix and the effects of pricing actions initiated last year especially in Europe.

I like to think about valuation with a sum of the parts framework seeing as Polestar doesn't do much in terms of helping with net income to shareholders. Volvo Car owns nearly half of Polestar whose market cap is a little under $8 billion. If we discount what Mr. Market says about Polestar down to $6 billion then it's fair to say Volvo Car has about a $3 billion interest.

Trailing twelve months ("TTM") net income to shareholders, gross profit and revenue were SEK 15,335 million, SEK 61,717 million and SEK 351,581 million, respectively. This stems from SEK 3,611 million + SEK 15,577 million - SEK 3,853 million, SEK 17,099 million + SEK 60,332 million - SEK 15,714 million and SEK 95,705 million + SEK 330,145 million - SEK 74,269 million, respectively. My valuation range is 5 to 7x net income to shareholders which is SEK 76.7 billion to SEK 107.3 billion or $7.5 to $10.5 billion.

Summing up with the Polestar consideration, I think Volvo Car is worth about $10.5 to $13.5 billion.

The 2022 annual report says the market cap was 141,170 million SEK back on December 30th when the share price was higher. Doing a little algebra, this works out to a little less than 3 billion shares:

Based on the closing share price on 30 December 2022, SEK 47.38, the Group's market capitalisation was 141,170 million SEK.

The VLVCY share price was $7.42 on April 17th. FactSet says the VLVCY ratio is 2:1. so we divide the 2,979,524,179 shares outstanding by 2 and multiply by the share price to get a market cap of a little more than $11 billion.

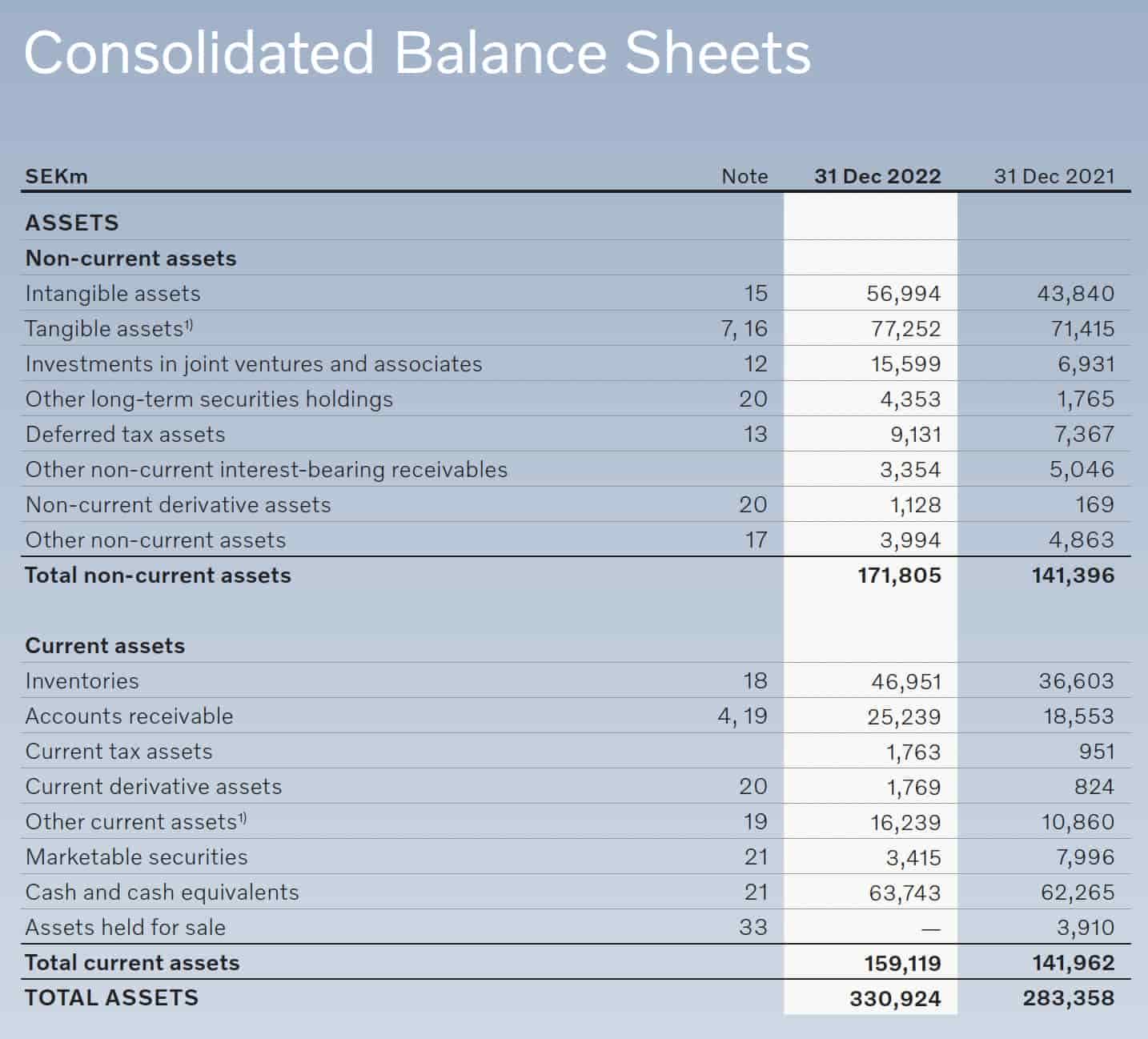

Regarding enterprise value, the cash and securities subtotal of SEK 67,158 million stands out. It comes from the SEK 63,743 million in cash and equivalents plus the SEK 3,415 million in marketable securities:

Balance sheet (2022 annual report)

{kind=link}

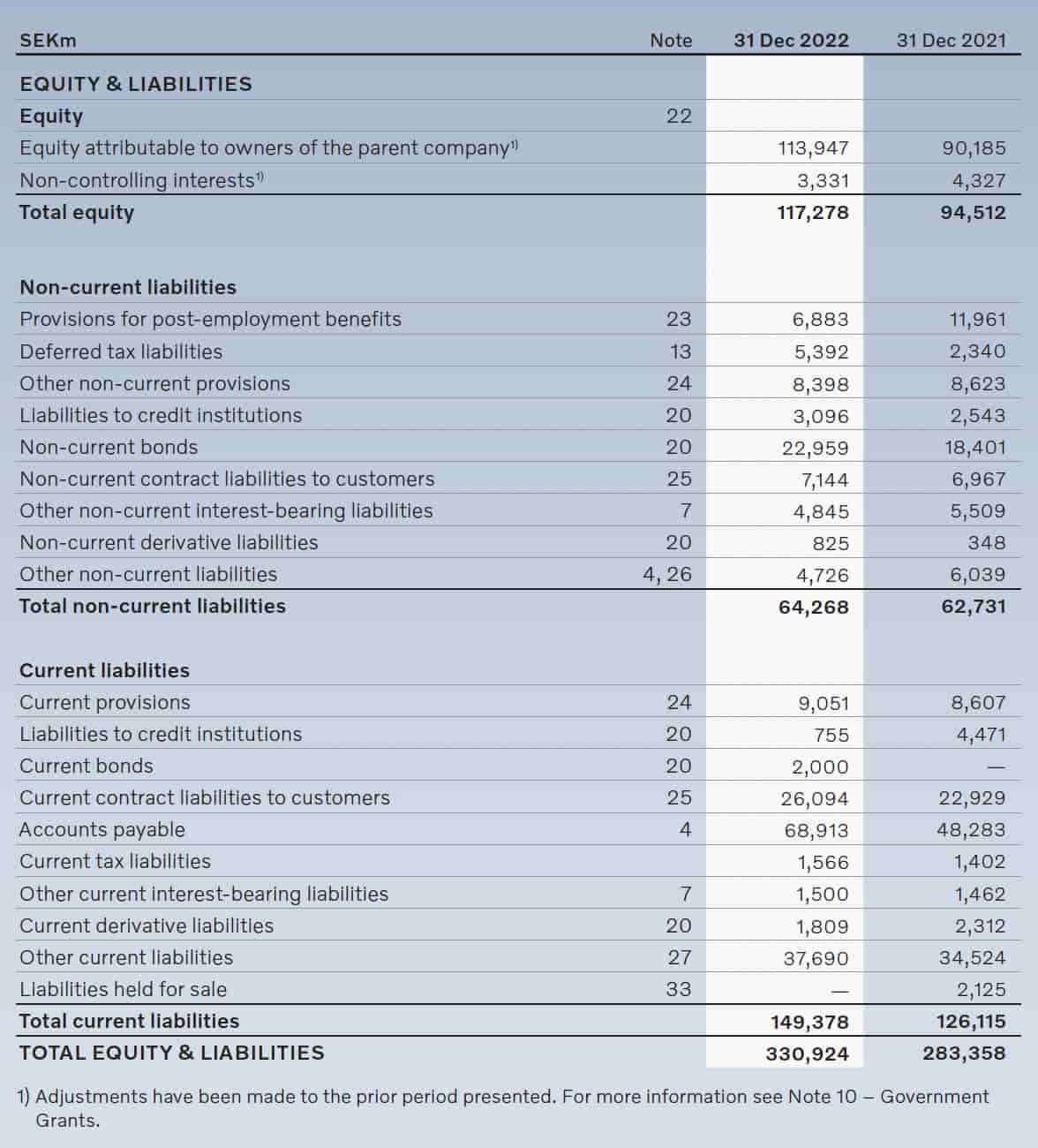

I like the way Ford ( F ) differentiates between debt and auto debt from Ford Credit and the rest of the company in their ROIC table because I like to exclude debt from Ford Credit when thinking about the auto enterprise value. Unfortunately I don't see a lot of differentiation on Volvo's debt types at a glance:

Liabilities (2022 annual report)

{kind=link}

I don't see outsized debt standing out above. The cash flow statement says net debt is SEK 38.1 billion and the amounts shown for non-controlling interests and retirement obligations are minor in comparison. As such, it looks like the enterprise value is less than the market cap.

The market cap is within my valuation range and I think the stock is a buy for long-term investors willing to hold it for 3 years or more.

Disclaimer: Any material in this article should not be relied on as a formal investment recommendation. Never buy a stock without doing your own thorough research.

For further details see:

Volvo Car: Transforming With BEVs And DTC Changes