VNNVF - Vonovia: Discount To Book Value Offers A Buying Opportunity

2023-08-01 07:12:46 ET

Summary

- Debt remains too high, and time is needed to deleverage the balance sheet, but Vonovia is financially healthy. However, the market was pricing in solvency problems.

- Rent increases will compensate for higher interest costs, and the market isn't pricing this in.

- Investors shouldn't mind an equity injection if needed at the current discount to book value.

- Despite the current bull run, I think there is still plenty of upside left for Vonovia to shine.

Editor's note: Seeking Alpha is proud to welcome Robin van Spankeren as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Vonovia ( VONOY , VNNVF ) is being weighed down by its debt as central banks raised interest rates at an unprecedented speed. An era of cheap financing created a perfect storm for real estate stocks that have cut their dividends. The uncertainty about where interest rates will be in the future keeps affecting investors' sentiment for real estate stocks. However, the current discount to book value creates a long-term no-brainer investment. Rent increases can compensate for higher interest costs and the market is not pricing this in. It will when inflation cools down and the company can return to its original pay-out policy.

Vonovia

Vonovia is a residential real estate company currently holding around 550,000 units in mostly German cities. In 2021, Vonovia acquired Deutsche Wohnen. It aims to pay 70% of the FFO (funds from operations). The current book value of Vonovia is as of Q1 2023 €53.75 compared to the current share price of around €20. In 2022, the FFO was around €2 billion (€2.50 per share).

Business Model

Vonovia manages its business in four segments: rental, value-add, recurring sales, and development.

In 2022, the rental segment accounted for 80% of the total adjusted EBITDA. This increased to 88% in Q1 2023 since the sector development of new houses is lacking. The organic rent increase was 3.4% in Q1 2023. In June 2023 LEG Immobilien SE ( LEGIF ) , a direct peer, increased their rental growth expectations to 3.8 - 4.0% (previous expectation: 3.3 - 3.7%). A 3.4% rent increase in Q1 2023 led to an increase in adjusted EBITDA for the Rental segment by €28.5 million. Note that this is only 1 quarter. Despite the rental segment is performing excellently, overall FFO declined in Q1 2023.

The rents in Germany are controlled by the government . Take into account higher building costs and financing rates and the segment development became unprofitable at current market conditions. Vonovia postponed all new construction in 2023 in line with their goal to lower investments and use cash flow for operations to pay back debt. I believe that this segment will come to a standstill for a long time. At least till interest rates are at a low level again or the German government comes with a subsidy cannon. But even if this sector becomes profitable again, the management board will prioritize paying back debt rather than starting money-intensive projects for a low yield when interest rates are high.

The Value-add segment includes both the maintenance and modernization of buildings and offering services to make the life of tenants easier.

The recurring Sales segment includes disposals of individual units of the portfolio. Despite challenging market conditions and declined profitability and activity in this segment, Vonovia manages to sell these single units above the current book value.

LTV is around 44%. This is an important metric for bond covenants and thus creditors and rating agencies monitor this closely. Vonovia is trying to lower the LTV by retaining cash flow from operations and shrinking the balance sheet by selling assets. However, depreciation on the assets is also increasing the LTV.

Vonovia's business model is built on cheap money. The current German 10Y yield is approximately the same as EPRA's Net Initial Yield of Vonovia in 2022 (2.7%) . 2.7% is reasonable when you hold 91 billion rental properties, but not when this is based on a 1.5% financing rate while the current refinancing rate is around 5%. In other words, the refinancing rate is twice its yield on rental properties. If Vonovia was fully financed with free-floating debt with their current LTV, there would be almost no money left for shareholders. This happened with Samhällsbyggnadsbolaget (no ticker).

Real Estate Sector

After years of cheap financing, real estate investors should prioritize long-term stability and closely monitor where real estate companies are heading.

New financing rates are at a temporary 5% minimum. The new finance rate is even close to my required return on equity of 7%. 7% is a realistic required return for European stocks. It implies a small risk-free rate and an average risk premium. Leveraging up also adds risk. In just a small time frame debt went from real estate's biggest friend to its enemy. The NIY (Net Initial Yield) of European real estate companies is extremely low in comparison to the US peers. Hence rolling over debt will significantly impact profitability. This sets the sector up for a decade of low earnings growth or even a decline if rates don't come down from their current levels. The only measures real estate companies can take are lowering CapEx, retaining income, and deleveraging their balance sheets by asset disposals.

LTV And Asset Disposals

A lower relative yield to the risk-free yield also leads to less demand for rental properties, making property value and LTV drop. This sets the management board in an awkward position. While investors are losing their money, the management board is and should prioritize its relation with debtholders over shareholders.

The market is currently pricing in further asset depreciation. I think the market is exaggerating a bit. Due to the relatively low yield, the book value of rental properties is low compared to their face value on the open market. The book value of the apartments in Berlin is valued at €3,000 per square meter. The average asking price in Berlin is above €5,000 per square meter and can even increase to €8,000 for new buildings. Although building permits plummet while demand is increasing, building costs aren't decreasing and this should further boost the price of real estate in the medium term. Despite financing costs being higher, as wages increase overall, house prices aren't going to decline significantly. The housing shortage in Germany will increase further, partly driven by Ukrainian refugees that aren't returning to Ukraine. Residential real estate might get less attractive since bond yields are higher, but you can't print real estate from thin air.

The rise of interest rates and building costs made affordable housing unprofitable under the current German law. Thus Germany keeps failing to hit its projected target . Long-term investors that want to buy residential real estate are only able to buy existing units from real estate companies like Vonovia. Long-term investors such as pension funds are required to diversify their portfolios and match their cash flows with their future obligations. This is where residential properties beat bonds; you can determine you want higher rents but you cannot ask the government or a company to increase the coupon. So far Vonovia already made two large transactions during the first half of 2023.

So let's zoom in on the previous property deals of Vonovia. Firstly, the €1 billion deal with Apollo. Investors weren't that excited despite a '5%' discount to book value. This seems odd, since the share price of Vonovia offers an almost 70% discount to book value and disposing assets at a 5% discount to book value should close a proportion of the valuation gap. But Apollo receives with their minority stake a higher yield than Vonovia, as they won't pay management fees and receive a higher dividend. What Vonovia also didn't disclose is that Apollo might leech on Vonovia's low financing rate, while the market rate is much higher. The management board plays down the enormous discount to book value that was offered with a forever call option, which could be exercisable maybe in 2035. It is important to state that Vonovia only sold a minority stake. Being the bigger shareholder can have some perks. Thus making the higher portion of the dividend less relevant. Despite the discount to book value, the deal injects €1 billion of equity into Vonovia. This is a positive thing in my opinion. Of course, the media exaggerates the deal as Apollo is the big winner, but it also proves the almost 70% discount on the share price is exorbitant in my opinion.

The CBRE Investment Management deal was at more favorable terms with only a slight discount to book value. However, this deal included freshly built apartments, resulting in lower CapEx for the coming years. But the gross yield was in line with Vonovia's assets. Overall, I would say shareholders are better off with those two transactions. Vonovia almost hit its 2023 asset disposal target in the first half of 2023. This should also improve bargaining power a bit for future deals.

I think assets might depreciate 3% further, maybe 6% in total, before stabilizing. And note that S&P Global affirmed a BBB+ credit rating with a stable outlook for the long-term, even under the assumption Vonovia won't succeed in shrinking the balance sheet. Which it did.

Financing And Debt

As mentioned in the introduction, Vonovia is weighed down by its debt. Refinancing debts lowers FFO and adds risk to the business. But the crash to €15 was exaggerated, in my opinion.

Vonovia was one of the better-performing stocks on the DAX 40, fuelled by the negative interest rates from the ECB. The ECB lowered its interest rates in response to the financial crisis in 2008 and lowered it even further after the European debt crisis. When debt is cheap, it increases the price of what it finances: real estate and stocks. The low rates made leveraging up on debt to increase profits very accessible. It also made you a genius if you did; hang yourself in debt at a 1.5% financing rate and make a small spread. Naturally, when interest rates rise, debt becomes too heavy.

A share price of €15 is a 70% discount to book value, while the assets have a NIY of 2.7%. After all, you buy assets that yield 2.7% of the book value for 30% of the price. As my required return on equity is 7%, this should create alpha. Let's say one would buy Vonovia at €15 and one second later, Vonovia announces it will raise €10 equity per share. The investment of €25 generates €2.4 FFO per share (including lower interest costs) and a < 35% LTV and a further €11 billion worth of disposals of non-core assets. In this scenario, Vonovia wouldn't need to access the debt market until 2028.

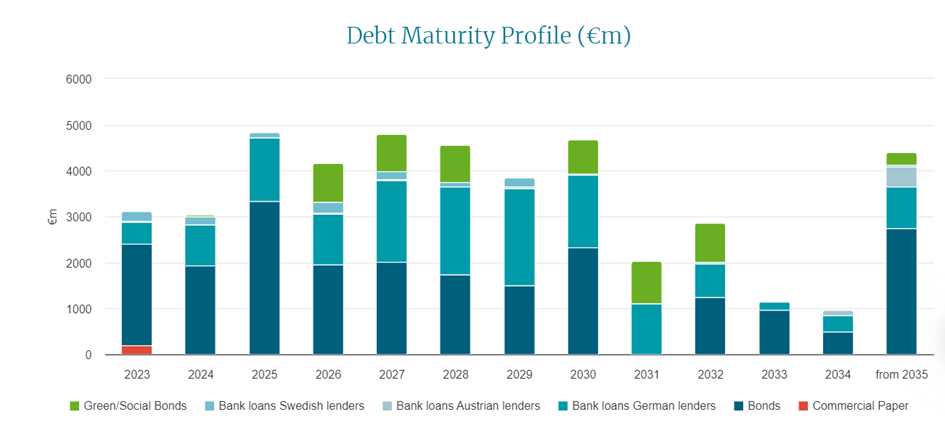

The debt maturity profile is approximately* as follows :

Debt maturity profile (Vonovia)

{kind=link}

* Approximately because Vonovia successfully completed a tender offer for outstanding bonds.

Vonovia has around €42 billion net debt that I like to categorize into the following three categories:

- 25% debt that will be paid with disposals and retained earnings (0% interest rate);

- 25% debt expiring in 2030 and beyond (1,5% interest rate).

- 50% new loans rolled over at higher rates (3% - 6% interest rate);

Under the assumption Vonovia will refinance its debt with bank loans and bonds at an average 4.5% rate till 2030, I am not that worried about the liabilities. And note that it is unlikely that the interest cost will be 4.5% or higher. This would mean the ECB would barely cut rates after they stimulated consumers, companies and countries to take on record amounts of debt.

Taking into account CapEx, dividends, and other costs at €1.5 billion, FFO around €1.8 billion, and disposals at €2 billion (excluding higher taxes), interest costs per year will increase by a maximum of €80 million per year. This is completely compensated by rent increases. But I would like to emphasize that FFO will decrease if Vonovia keeps succeeding with selling assets and interest rates don't drop. Therefore, I believe the management board shouldn't pay dividends under these market conditions.

Risks

As I pointed out earlier, a possible equity injection isn't a risk. After all, the assets currently have a NIY of 2.7% and generate a higher cash flow each year due to rent increases. Taking into account the discount to book value, the return on the assets is well above the required return on equity.

But there are two risks I like to point out. Firstly, despite inflation cooling down, inflation might stay well above the ECBs target for longer than expected. This will put further pressure on the balance sheet as interest rates stay higher for longer than already anticipated. Secondly, the rise in interest rates shocked investors. This limits future growth by financing it with debt and investors demand a higher return for extra risk. Therefore, it is unlikely that the share will hit its all-time high in the coming years.

Outlook

FFO will decrease if interest rates don't drop down again, but rent increases can compensate and keep FFO at a respectable level. The uncertainty where interest rates will be in the future, keeps affecting investors sentiment for real estate stocks. However, it is likely that interest rates will drop in 2024. Higher interest costs slowed down purchases and investments. However, consumers are still not saving their money since the compensation from banks is lower than the current inflation rate. The full effect of the rate hikes is yet to come.

Vonovia will keep increasing its rent and as there is a housing shortage, the book value of the assets will increase again in the medium term. Since Vonovia is managing an enormous portfolio, a 1% increase in book value of assets will yield a non-cash income of €1 billion. Therefore, it is possible that Vonovia will make €5 billion profit in 2026 (current market capitalization is just over €15 billion). Depending on the share price, investors will push the management board to close the valuation gap between book value and market capitalization. For this reason, I think Vonovia is a long term no-brainer investment. However, even if interest rates would go into the negative territory again, investors are traumatized by the current rate hikes and will pay less attention to value the share price based on book value. This is nothing new in the real estate sector. Even when interest rates were negative, shopping malls had an enormous discount to book value. Thus, I will only value the future cash flows on Vonovia.

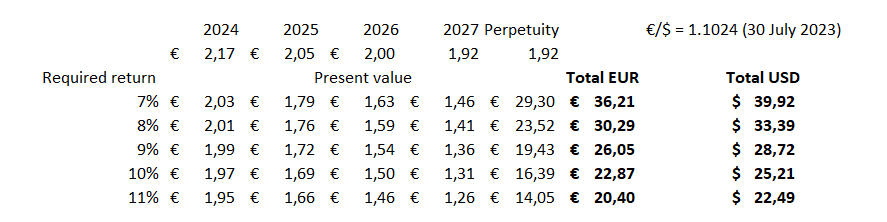

If I take into account my assumptions:

- Future debt is financed at a 4.5% rate (on average);

- Impact of higher interest rates is limited due to rent increases and retained earnings;

- FFO will decline due to asset disposals;

- 2% growth rate for the perpetuity (significantly below the current rent increases).

I come to the following discounted cash flow model:

{kind=link}

Even though those assumptions are already pessimistic in my opinion, Vonovia's share price is currently suggesting that the return on equity is around 10-11%. As I find an 8% or 9% return on equity would be more reasonable when I take into account pessimistic assumptions, my price target comes in a range of €26 - €30 ($29 - $33). As inflation will decrease further and Vonovia potentially makes more deals, the share price should move towards this target. If the assets will increase in value again, and they will someday, investors might also pay more attention to the valuation gap. In this scenario, my price target is above €40 ($44).

For further details see:

Vonovia: Discount To Book Value Offers A Buying Opportunity