VNNVF - Vonovia: Even More Bullish After The Dividend Cut

2023-03-20 13:28:53 ET

Summary

- Vonovia has declined since my last article due to a broader market selloff, allegations made against their employees, and a dividend cut.

- Regardless of stock price movements, the operational performance has remained solid, and management is actively working to repay their high level of debt.

- I reiterate my strong buy rating and discuss the way forward for Vonovia.

Dear readers/followers,

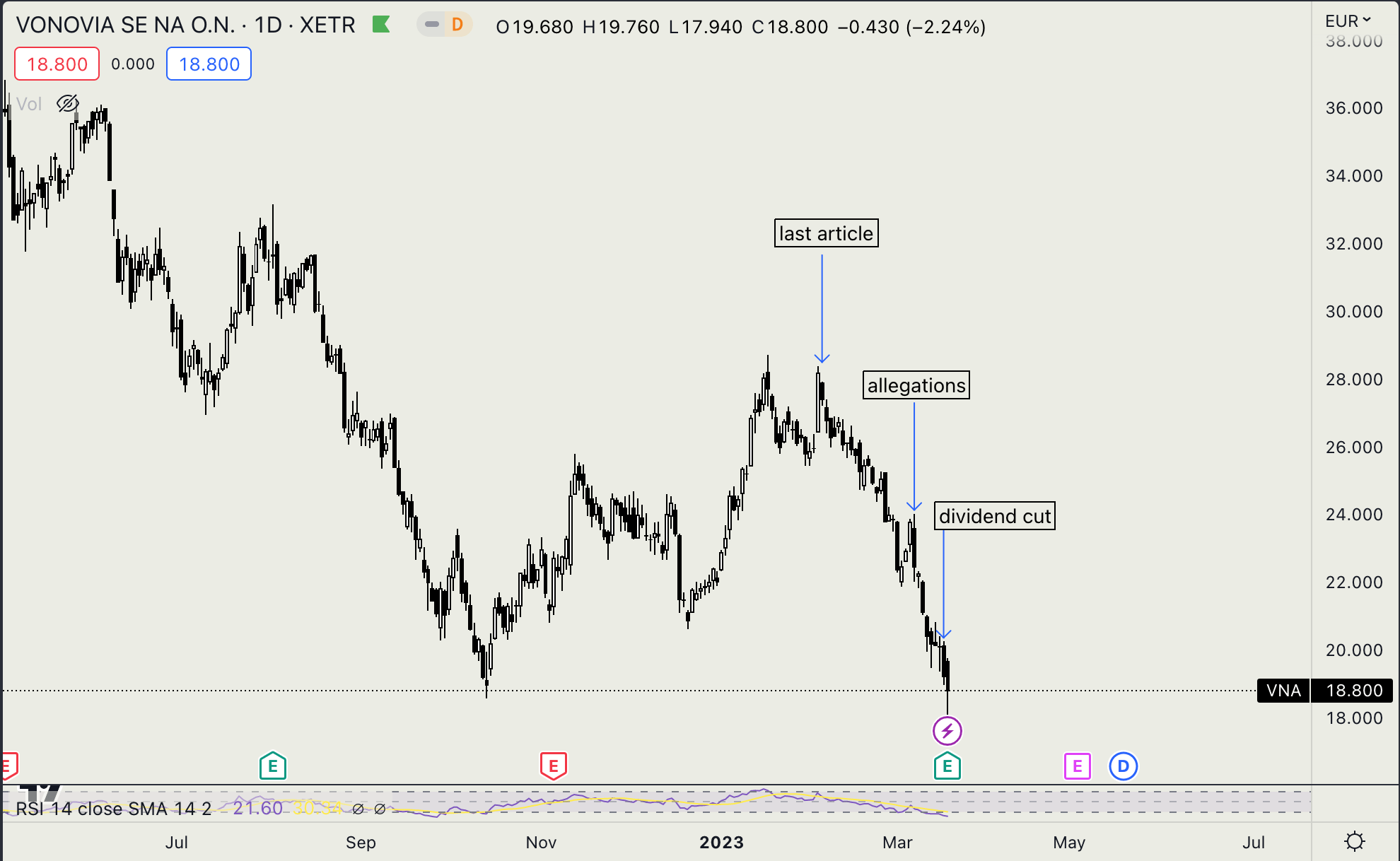

There have been several key developments since my last article on Vonovia ( VONOY ) that have resulted in a significant price drop. And although my strong buy rating of the company hasn't changed, and I continue to hold a full 2% position (with BE at EUR21.76), I think an update on the company is warranted.

Note: As with all of my articles on European stocks, the security discussed in the article is the native share. The ticker is VNA and it is EUR-denominated. There is also an ADR available for anyone not wanting to invest in the native shares. Always do your own research on tax implications.

Allegations

Firstly, on March 7th, regulators searched two of Vonovia's offices due to allegations against employees of fraud and bribery related to the awarding of contracts to subcontractors. Importantly, these allegations have been made against now former employees, not Vonovia directly, and have likely affected less than 1% of investment volume as confirmed by the company in their official statement :

Based on the information currently available to Vonovia, the maximum order volume with third-party companies potentially affected by the investigations for 2022 is less than 1% of the maintenance and investment volume and at similarly low levels in prior years. The actual impact is expected to be only a fraction of that. Vonovia and our auditor therefore agree that the allegations do not have a material impact on the company's net assets, financial position and results of operations.

Following the incident, Vonovia has mandated Deloitte to conduct a comprehensive internal investigation, including a review of internal control systems. In summary, whether the allegations against former employees turn out to be true or not, the impact on the fundamentals of the business should be negligible (the worst outcome I expect is a small fine). I suspect that the allegations may have been made by short-sellers, because they were timed in line with a broader market selloff, and overall, I don't see this development as a threat to my buy thesis.

2022 Results

Secondly, the company announced its Q4 2022 earnings on March 16. To start, their operational results have been pretty good. Group FFO increased by 20.1% YoY to EUR2 Billion, though this is largely attributable to the Deutsche Wohnen acquisition which took place in Q3 2021 (and was therefore fully included in 2022 but only included in one quarter of 2021). As far as same-store operational metrics, the company has seen some of the best numbers ever with rent growth of 3.3%, occupancy of 98%, and rent collection of 99.8%. This confirms that the rental business is very stable, even in times of economic turmoil, and is not really the issue here. In 2023, management expects organic rent growth to accelerate slightly, but Group FFO guidance for 2023 came in lower than consensus at EUR1.85 Billion, primarily due to higher interest expense.

Debt is really the main issue for Vonovia. The company has EUR45 Billion of debt at a very low average interest rate of 1.5%. The worry is that if interest rates remain high for a long time, the cost of debt will go up over time as the company refinances its debt due each year. Management is of course aware of this and plans to roll over (refinance) their secured debt and repay their unsecured debt from free cash. While the rollover of debt will definitely increase their interest expense, the effect will be somewhat offset by a EUR1 Billion zero cost swaption collar which the company put in place to hedge part of their 2023 refinancing needs. In 2023, they plan to refinance EUR1.2 Billion in secured debt and repay EUR2.2 Billion in unsecured debt.

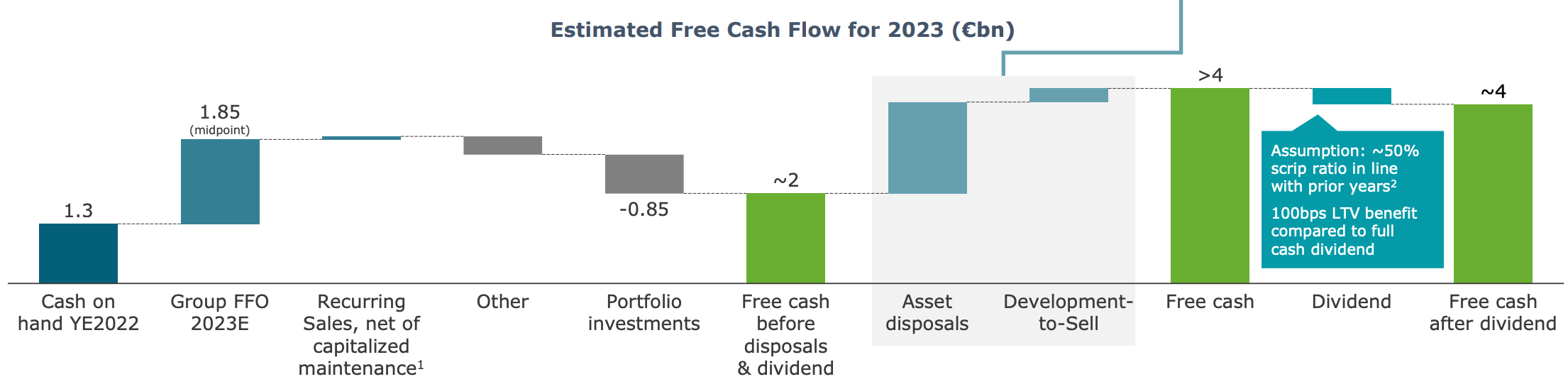

Management has reiterated its cash flow guidance for 2023 which is positive because it will be essential to paying down their unsecured debt. The chart below shows their plan to generate sufficient cash flow in 2023. As you can see, the plan is reliant on net disposal proceeds of around EUR2.0 Billion.

{kind=link}

Unfortunately, there has been no progress on disposals to this day (except for recurring sales in the fourth quarter). I believe that any positive news on a potential divestment will act as a significant positive catalyst for the stock price, but in the meantime, this remains the major risk. If management cannot sell a significant part of the portfolio to pay down debt and high interest rates prevail, the gradual increase from the rollover of debt will eat into the FFO. My base case is that rates will come back down over time, so personally, I am not too worried about this over the medium term, but management's progress with disposals is definitely something to watch.

Management has also cut the dividend by about 50% YoY to EUR0.85 per share (35% of Group FFO) citing an appropriate balance between capital discipline and returns to shareholders. The cut was somewhat expected and is definitely the right move, given the need to repay debt. If anything, I think it's quite bullish that the dividend hasn't been scrapped all together and that management has kept its policy to payout 70% of Group FFO from 2023 onwards. At the current share price, the yield stands at 4.5%.

Takeaway

Since my last article, the stock price has declined by 30%. I explicitly said in that article that I wasn't calling the bottom, and the stock price could easily revisit the low. Unfortunately, that's the reality of being in a bear market. The decline was driven by a broader market selloff related to inflation and the banking crisis, the allegations made against Vonovia's employees, and to a smaller extent, by the recent dividend cut. In the meantime, the rental portfolio has been doing exactly what it's supposed to do and recorded some record operational figures. It's never pleasant to see a position in the red, but my conviction for Vonovia remains unchanged over the medium to long term with a PT of EUR45 per share, so we're going after some serious upside here.

The fundamentals haven't really changed and a lot of negativity has been priced in, so investors should be more bullish now compared to two months ago. Although 2022 results haven't been exciting as management postponed disposal plans, lowered their Group FFO guidance, and cut the dividend in half, Vonovia remains extremely undervalued for what it is and although it can go lower in the short-term (though I'm fully invested here already), this is a great entry point if you're looking to hold for 3-5 years. The main thing to watch for 2023 remains the disposal of assets and anything related to interest rates.

I, therefore, reiterate my " strong buy " rating here at EUR18.80 per share and have recently doubled down on my position at EUR21 per share (I shared this in the comment section of my last article). I look forward to your questions and comments below.

{kind=link}

For further details see:

Vonovia: Even More Bullish After The Dividend Cut