VONOY - Vonovia Is A 'Buy' Here Due To Confirmed Upside And Undervaluation

2023-12-02 04:36:17 ET

Summary

- Vonovia is a German residential real estate company with a strong portfolio and solid financials.

- The company has experienced pressure but also has significant potential upside based on yield coverage and undervalued price.

- Vonovia's core business is performing well, with high occupancy rates and rent growth, and it is making strategic moves to improve its capital structure.

Dear subscribers,

It's time to update my thesis on German company Vonovia (VONOY). The company represents a non-trivial position for me in my conservative investment portfolio - both the private and my commercial portfolios. ADR investment isn't something I recommend here. I would argue that it's an advantage to look at using an international broker like IBKR to invest in the native German ticker.

Looking at the company's financials, it seems very clear to me that the business is going to experience pressure for the next few years - but at the same time, the company is also poised to see significant potential upside based on solid yield coverage, and a very undervalued price even at this time.

Because I added the lion's share of my investments in the company when the company was significantly below €24/share, I'm actually in the green of all of my Vonovia positions at this time.

Let's see what we have going for us here.

Vonovia - We're realizing the upside.

So, for part of my position, I'm already up more than 15%. I view this as only being the beginning. I have made no secret of my investments and exposure to Vonovia here, having covered the business for over a year at this point, and I believe the eventual upside potential to be massive, despite interest rate, macro, and Germany-specific challenges to the stock.

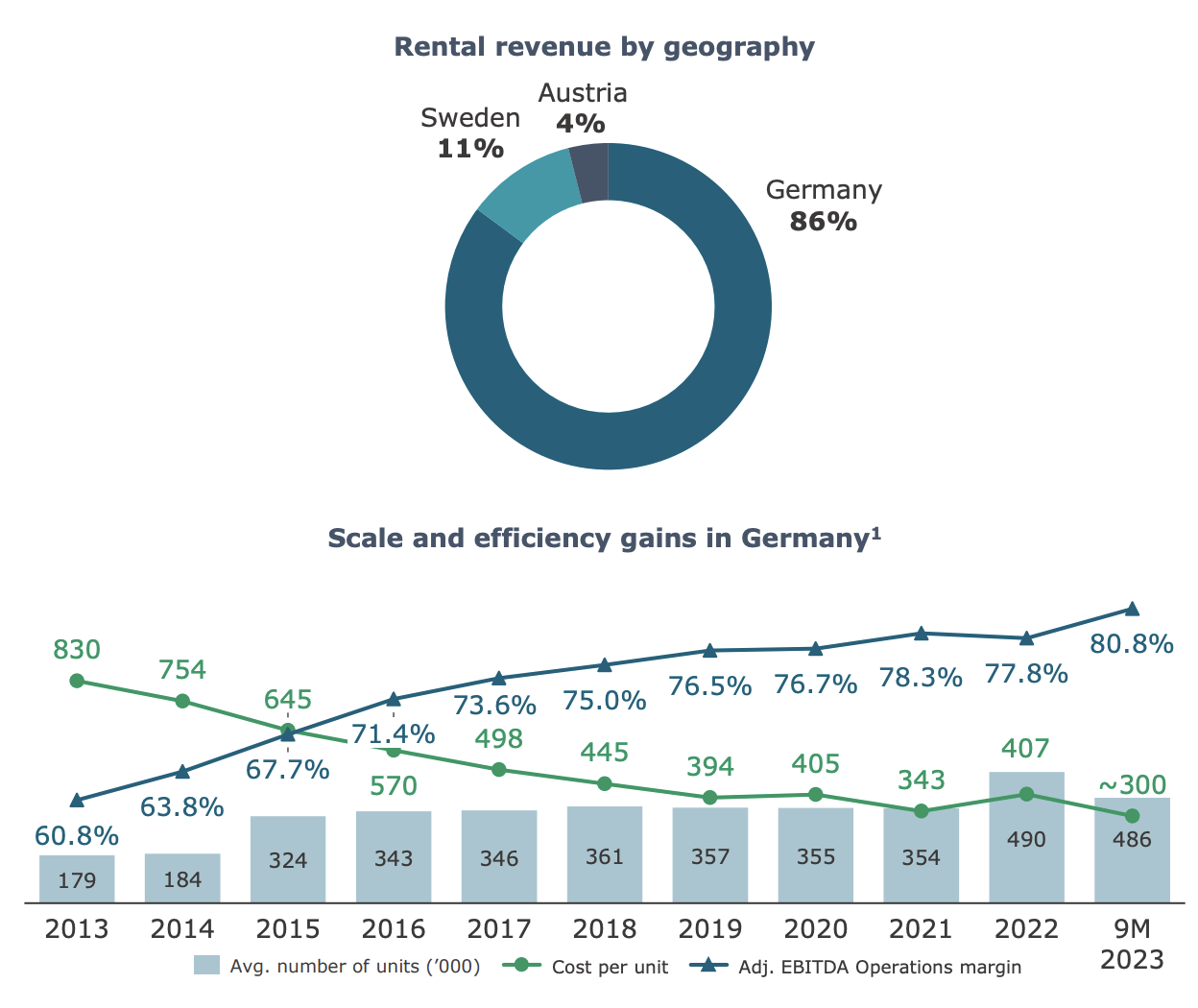

Vonovia remains Europe's leading residential real estate company. This is not an exaggeration. The company manages over 540,000 residential units in attractive areas not only in Germany but also in Sweden and Austria, as well as managing over 70,000 apartments. The portfolio, even with re-evaluated NAV, is worth over €85B, and the company offers an attractive mix of development, management, services, and the like.

It cut the dividend to remain conservative and currently yields a bit less than 4%, but this comes at the advantage of a BBB+ credit rating, which you might not guess if you look at the company's recent share price trends. Granted, that 4% dividend yield is no longer as attractive when you can get 5-6% from any REIT, but the upside potential here is second to very few companies out there.

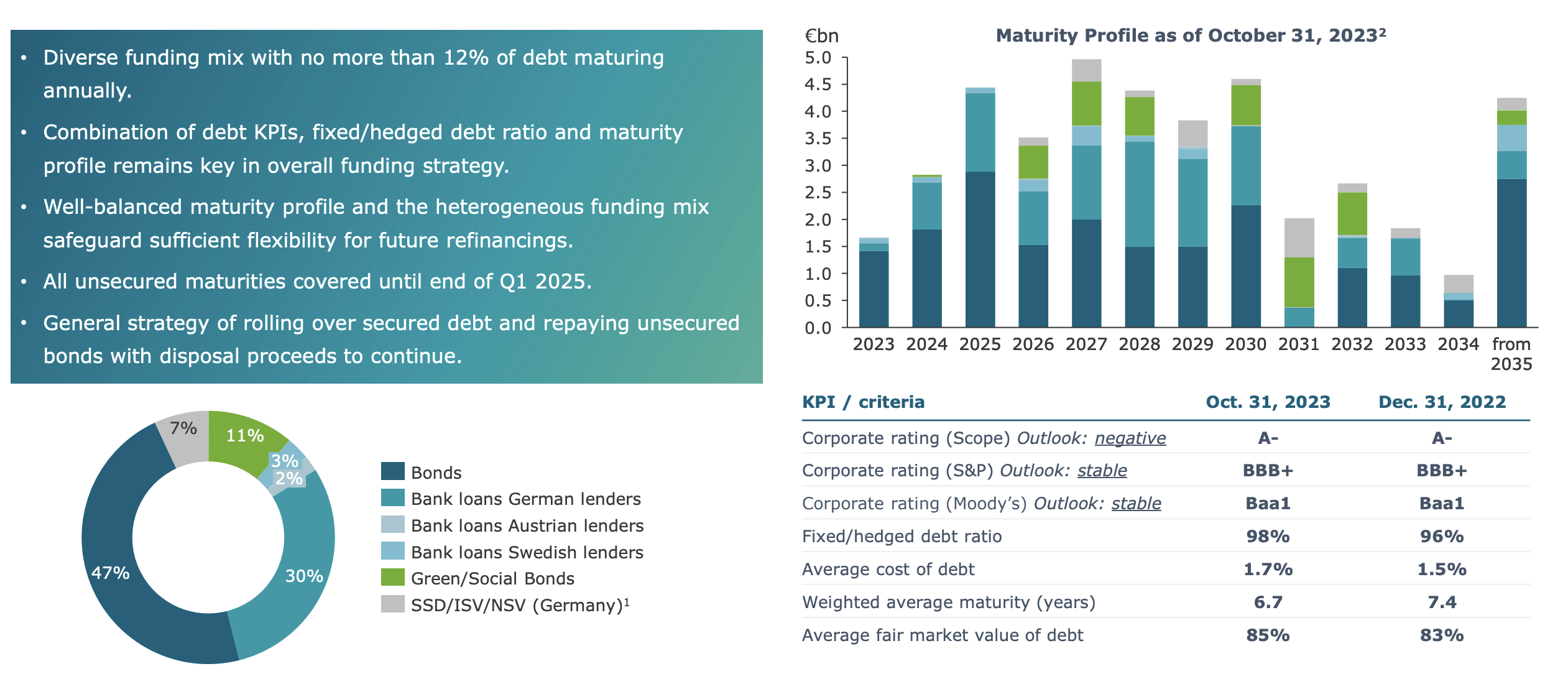

It also remains in the company's favor, that any worries for Vonovia are pretty ethereal - I'm talking about fundamental worries here. The company's 2023 and 2024 financial maturities are 98% covered, over 1 year in advance. The company has refinanced loans and ensured new loans, most of them unsecured.

We have 3Q23 results to look at and to give us an idea of where things might be going next year.

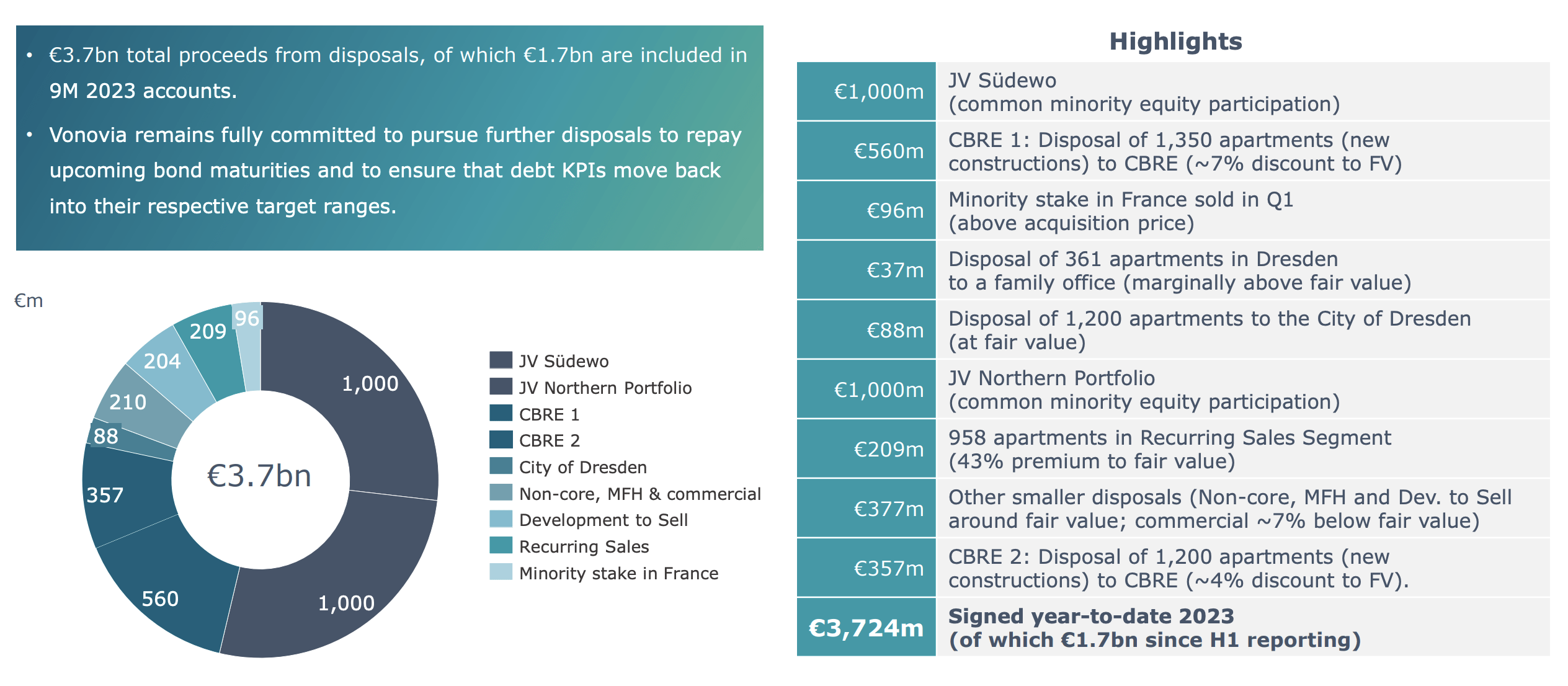

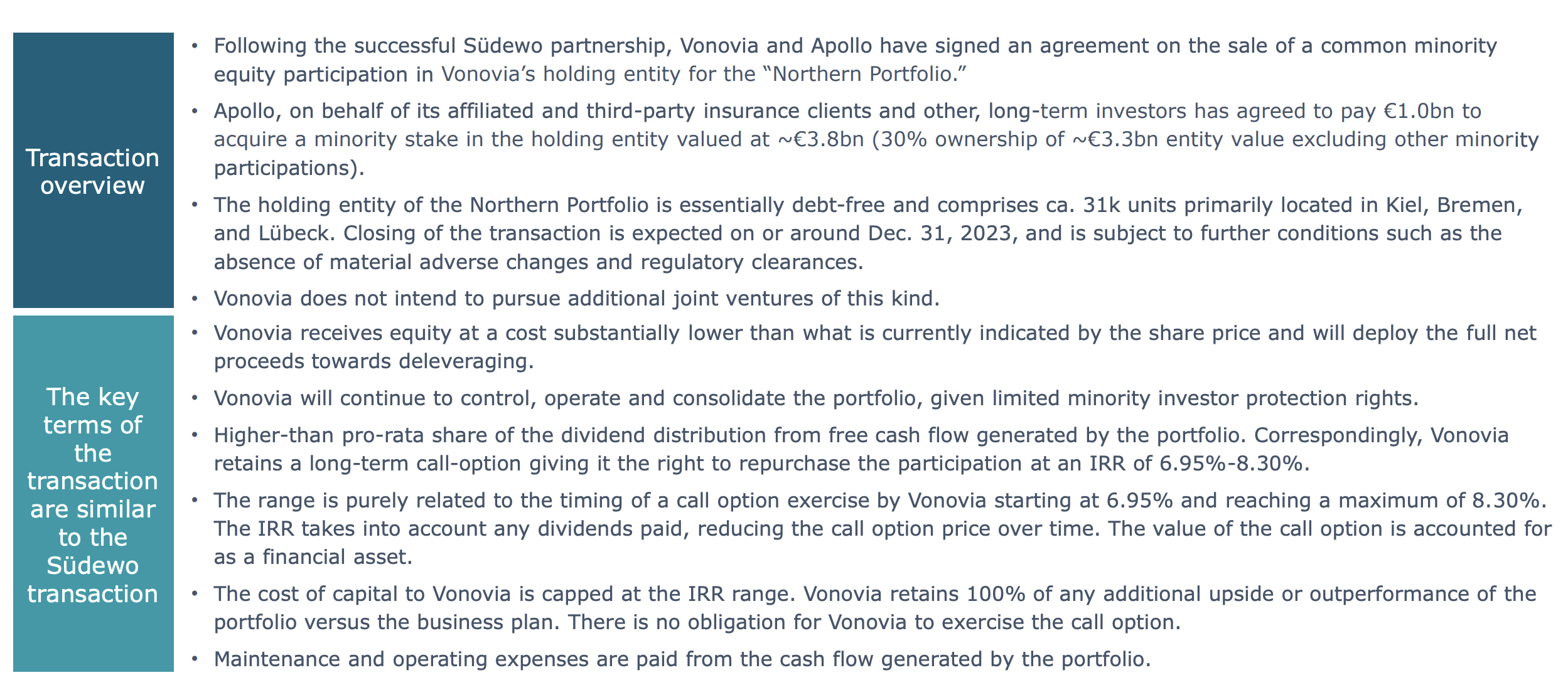

During the current 3Q23 period, the company has focused a lot on disposals of non-core assets. As of 9M23, this volume amounts to just south of €4B in sales, of which €1.7B was sold since August of this year. The company also signed a second JV, with Apollo acquiring a 30% equity stake in the company's northern Portfolio for proceeds of €1B. This brings sales and JV proceeds to close to €5B for 9M.

The company is also divesting/selling constructions - 1,200 sold at a 4% discount to fair value. This is not great - but the company is in a position, despite all the positives, where cash in and improving the structure is more important than holding onto what the company views as underperforming. That's also why the company sold 1,200 units to the city of Dresden at a fair-value estimate of close to €90M.

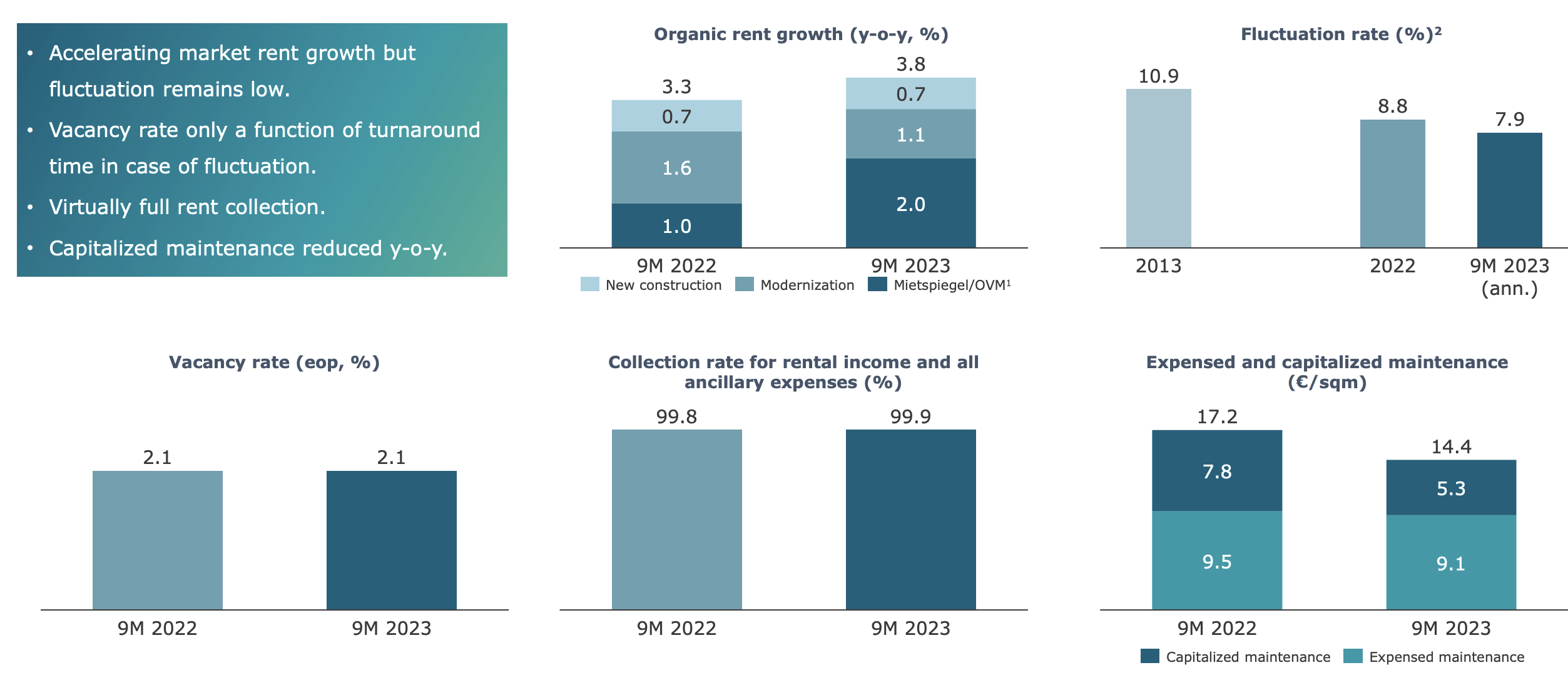

Vonovia is making moves here - and there are no negative fundamental indicators worth mentioning in 3Q. The company's financing needs are solid. Vonovia reports 3.8% organic rent growth, less than 2.2% vacancy portfolio-wide, and rent collection of 99.9%.

Worries in this company are minor on the fundamental side. EBITDA is up for the year, on a rental-adjusted basis, although the EPRA numbers, such as EPRA NTA are down - but that's to be expected in this environment.

EPRA NTA is the metric you want to focus on here. This is the value of the company's assets less its liabilities, which for now comes to just over €50.5/share, and that's after going down 12% this year so far. I also remind you, that the current share price is less than half this.

On the financial guidance side of things, the company is guiding for below-CPI rent growth, as expected around the 3.8% level on an organic rent growth amount. EBITDA and group FFO are expected to come in at the lower end, with an overall lower rental revenue due to asset disposals. The company expects over €3B incoming from further, already-signed disposals.

Disposals this year are as follows.

{kind=link}

The company has in fact overachieved its initial disposal target, with the very clear goal of getting its fortress-grade KPIs back in line following the massive M&As and expansions over the past few years. This also includes, if the options are right, the use of JV's, such as the rent one, to improve capital structure and spread out risk.

{kind=link}

On a high level, it can be clearly stated that the company's core business, rental residential, continues performing at a stellar level. We're seeing a rent growth of 7% with basically 100% rent collection and very high occupancy. The company's relatively low cost base and low OpEx continues to imply a high overall upside here - and already many of the forecasted synergies with Deutsche Wohnen are being realized here.

Actual issues?

Cost of capital. The company's overall group results remain impacted due to financing costs and limited transaction volume in an unattractive market (for the most part). While I don't expect any material downturn for the company in the near term - there's too much safety in Vonovia, it's also in what timeframe the company will capture some of those targets that I considered likely and base my investment thesis on.

Remember, I base my investment thesis on the fact that Vonovia will significantly outperform the market based on its degree of sheer undervaluation. The rising interest rates and reevaluations and overall macro trends have put a bit of a sock in that in the short term, but for the longer term, things still look stellar.

Rental segment KPI's are not just "good", they're excellent.

Vonovia IR (Vonovia IR) Vonovia IR (Vonovia IR)

{kind=link}

{kind=link}

Also, remember a part of the calculation of the "mietspiegel", which the company is subject to in Germany, similar to how it is in Sweden, means that growth implementation of rental increases is delayed. There is a local, maximum over 3 years time that the rent can go up, meaning it's spread out, but this means that the growth is coming, just delayed.

It means that even if inflation and other factors slowdown in some ways, rents are subject to time lag, meaning they'll actually continue growing as much or faster than inflation if it slows down. This is the case in Sweden as well, where the various organizations decided upon a time-delayed model in order to spread out risks and inflation impacts over time - something the rental associations are likely regretting now that we see demands for multi-year, double-digit rent increases due to inflation impacts.

Vonovia is so large at this point that it's a play on living/housing megatrends. The company is currently not moving into new constructions or developments in any major way, and its legacy portfolio can be held with less than €300M worth of investment needed in 2024 to finish ongoing projects. In short, we have very good overall visibility.

{kind=link}

The company's debt is well-structured and laddered, with a limited amount maturing yearly. The BBB+ should be indicative of the risks that are being seen here. Covenants for the company are very generous here, and despite everything, the company has a proforma LTV of 45% here, with the required level from covenants being below 60%, meaning that assets would have to drop more than 26% in terms of fair value here for the company to be in any danger.

Possible? I suppose so.

Likely? No, I think not.

Let's look at the valuation and the upside I spoke about seeing here.

Vonovia - Not the best upside in real estate, but very high at this time.

So, Vonovia still has a significant upside. That's why my PT as of this article remains completely unchanged at €48/share, which implies close to a 100% upside from today's level. Even on an adjusted operating income basis, the company has an upside compared to the typical 14.5x P/E, currently trading below 12x. However, FFO is the best proxy we have to the company's metrics here, and Vonovia typically warrants around 20-22x, with a current FFO multiple of 10x. I do not think it warrants 20-22x, but 17-18x based on the size of its portfolio and its significant operational leverage even in this market, proven by the recent set of both sales and results. The company is also expected to, much like REITs I cover, see only a slight growth of 1-2% per year over the next few years for this.

Still, even just at a 12-13x P/FFO equivalent, this presents a 16% annualized upside based on a 12.5x 2025E P/FFO and a PT of €31, which is below my current one. Based on the continued strength of the company's asset portfolio and how far the company has fallen despite earnings being intact, I would say 16-18x P/FFO is fair for the company here. This implies at least a 33% upside at 17x and a PT of €43, or around €48/share at 18.5x with a close to triple-digit upside.

It may be some time before we see this realized - but much like other very conservative real estate companies I cover on a continual basis, the safety here is often underestimated. Even some of the worst trends we've seen for the past two decades have not caused this company's fortunes to decline in any material/significant way. Income is still high and cash flows are solid. Even if the company is going to see a slight decline in earnings and cash flow, this would not impact the overall appeal of the business in the long term.

Anyone investing in Vonovia today is, as I see it, doing so at a material and significant discount to fair value here. S&P Global still considers Vonovia to be significantly undervalued. The spread in targets is still extremely high here - 16 analysts go from a low of €17.25 to a high of €55/share. That's one of the highest differences currently on my coverage spectrum. However, the vast majority of analysts agree that the company is worth a lot more than €25/share, with 13 analysts out of 16 being at "BUY" or equivalent positive rating, and an average target of €30/share, conservative (but too low in my view).

Traditional US REITs still have a definite advantage over Vonovia when comparing them as investments given withholding taxes and some other stability-related variables. However, if you fully include what once was Deutsche Wohnen's portfolio in the company, then the company's current NAV, even updated for 2023 comes to 0.6X.

There's a massive discount on Vonovia 2023E here, and given that I know exactly what sort of properties we're talking about, I know I want to own them cheaply - and that is exactly what I am doing.

My thesis stands as of November, and it's as follows.

Thesis

-

This is the largest, most significant real estate company in all of Europe is at a great discount looking at every single perspective you could possibly consider.

-

I've been investing in Vonovia for over a year at this point and accelerated my investing as the company saw trough-level valuations.

-

Based on its fundamentals and valuation, I view Vonovia as one of the most appealingly valued real estate companies in all of Europe. Coupled with its credit rating of BBB+, this makes it a "BUY" to me.

-

My target PT is €48/share. I am not changing this PT for now, and I haven't changed it since I covered this company early in 2023.

Remember, I'm all about:

-

Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

-

This company is overall qualitative.

-

This company is fundamentally safe/conservative & well-run.

-

This company pays a well-covered dividend.

-

This company is currently cheap.

-

This company has a realistic upside that is high enough, based on earnings growth or multiple expansions/reversions.

For further details see:

Vonovia Is A 'Buy' Here Due To Confirmed Upside And Undervaluation