VNNVF - Vonovia: Likely Further Pain Ahead But Appears To Be Priced In

2023-06-13 12:27:02 ET

Summary

- Vonovia, Germany's largest residential landlord, reported decent Q1 2023 results with 3.4% YoY rental growth and a healthy 2.2% vacancy rate.

- Rental segment is expected to remain strong due to increasing demand and a severe housing shortage in Germany, offsetting weakness in Recurring Sales segment and Development segments.

- Tailwinds from anticipated easing interest rates from next year onward.

- Long-term fundamentals are intact as migration and inadequate housing supply support structural growth.

Vonovia ( VONOY ) is Germany's largest residential landlord and one of the largest in Europe. The company's portfolio is largely concentrated in Germany, and to a lesser extent in Sweden and Austria.

Q1 2023: Good rent growth, rent collection, and vacancy rates support cash inflow

In Q1 2023, Vonovia generated 3.4% YoY rental growth. Vacancy remained very healthy at just 2.2%, and rent collection was stellar at 99.9%. Vonovia's Rental segment accounts for the bulk of the company's FFO and a solid rental contribution helped offset declines in other segments.

Vonovia

Looking ahead…

Rents may possibly increase, vacancy rates unlikely to deteriorate

Asset disposals may shrink Vonovia's portfolio, but rent growth and steady vacancy rates could help offset this decline. In Q1 2023, Vonovia's Rental segment revenues increased driven by rental growth, despite a marginally smaller portfolio.

Vonovia Q1 2023 investor presentation

Rents tend to lag inflation and may possibly increase given the higher demand for rental units due to migration as well as an exacerbation of housing supply due to declining residential construction. Between January 2023 and March 2023, Germany reported record high rent increases nationwide - 7.4% for existing flats and 7.7% for newly built flats, according to data from real estate platform ImmoScout. Compared to a year ago, nationwide asking rents for existing properties rose by up to 12%, and 20% for newly built units. Management expects 2023 organic rent growth to be higher than 2022.

Given Germany's severe housing shortage, vacancy rates are not likely to deteriorate as higher financing and construction costs deter house buyers. Vonovia's vacancy rates in fact dipped in Q1 2023 to 2.2% from 2.4% the same quarter a year earlier.

According to a Reuters survey, rents are expected to increase 3.5% this year and 4% in 2025. Management expects rent growth to accelerate for the remainder of the year. Overall, this points to a favorable outlook for Vonovia's Rental segment, its biggest cash generator.

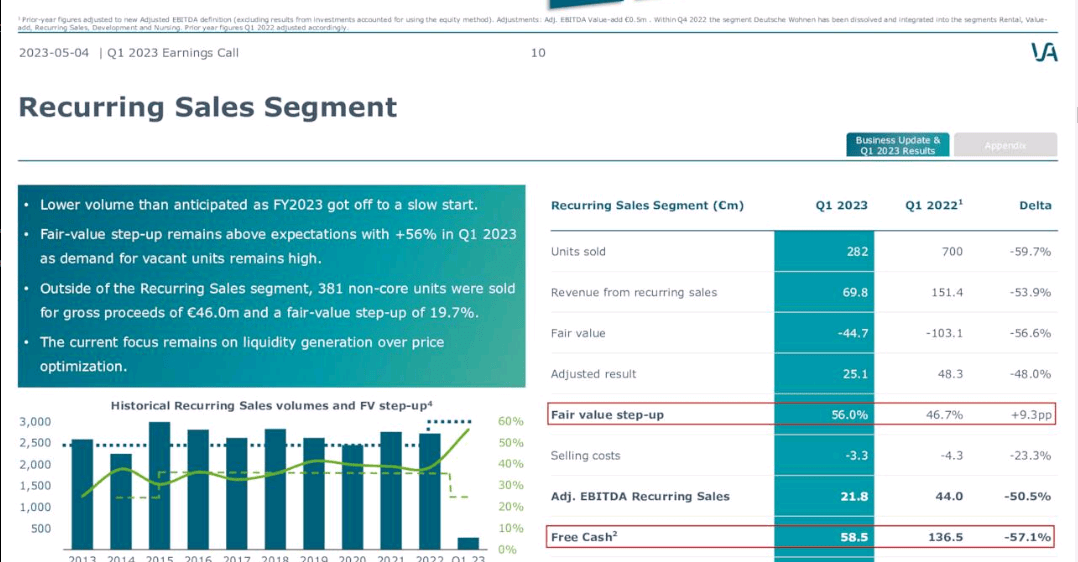

Recurring Sales segment and Development segment likely to remain a drag on FFO

Offsetting strong rental segment performance is continued weakness in Vonovia's Recurring sales and Development segment as Germany's high financing and construction costs dampen near-term house buying activity. In addition, management has indicated that the focus is on liquidity generation rather than profit and so these segments would remain a drag on group FFO.

Vonovia Q1 2023 investor presentation

{kind=link}

Nevertheless, they collectively account for a relatively small share of group FFO and profit declines could be partially offset by growth in Vonovia's considerably larger Rental segment. Overall, management expects group FFO to decline to EUR2.6 billion to EUR2.85 billion in 2023, from EUR2 billion in 2022.

Continued asset write-downs likely as interest rates remain elevated and demand environment remains weak

Following a revaluation, Q1 2023 resulted in a EUR3.4 billion value decline in Vonovia's German portfolio, down 4.4% YoY on a like-for-like basis. Further declines cannot be ruled out amid continued market weakness. Germany's house prices are expected to decline 6% this year and 2.5% next year. The declines could be manageable considering Vonovia company remains within targeted LTV corridors and fair values would have to drop significantly for the company to overstep their targets.

Vonovia Q1 2023 investor presentation

Encouraging progress with asset sales to free up capital and support deleveraging

In April, Vonovia sold off a EUR1 billion stake in its Sudewo portfolio to private equity firm Apollo and last month, Vonovia announced it was selling 1,350 apartments to CBRE. The purchase price of EUR560 million is only a slight discount to the EUR600 million estimated book value, including estimated costs for completion. Free cash after tax and all transaction costs represents an 89% conversion.

Possible easing of interest rates expected next year, a tailwind

While interest rates are expected to continue rising and remain elevated in 2023, rates are expected to decline slightly next year and decline even further in 2025 according to the second quarter ECB Survey . Falling interest rates could be a significant tailwind for Vonovia in terms of property revaluations and house buying activity which in turn could ease asset disposal pressures to meet debt obligations, and could shore up cash inflows from their Recurring Sales and Development segments through higher sales volumes and fair value step-ups.

Long-term market fundamentals remain unchanged

Germany has a severe housing shortage, a situation that could only get worse due to supply-side shocks. Interest rate hikes and spiraling construction costs have curtailed construction activity, with developers and home builders putting construction projects on hold or canceling them altogether. Deutsche Bank projects the number of residential construction permits to fall to 303,200 and the number of completed homes to fall to just 246,000 this year, far short of the government's target of 400,000 units a year.

Risks

Inability to dispose of assets in a timely fashion at favorable terms to meet maturing debt obligations

The company has fully covered 2023 maturities and two-thirds of 2024, but Vonovia has a bigger block of debt maturing in 2025 (the bulk of which is comprised of unsecured bonds), and if interest rates remain elevated (or for unforeseen reasons even increase) next year, any necessary asset disposals to meet 2025 debt maturities may be a challenge as demand weakens and property valuations fall further.

Vonovia Q1 2023 investor presentation

Conclusion

Analysts are mostly bullish on the stock.

WSJ

With a market capitalization of USD16 billion (~EUR15 billion), Vonovia is trading at a P/BV of about 0.50 which suggests the market has already priced in the disposal of much of Vonovia's portfolio (possibly on the basis that negative revaluations amid a weak housing market mean continuously increasing LTV despite ongoing asset disposals barring any material improvement to house buying activity and property valuations).

All of this year's, and most of next year's debt obligations have been covered however and headwinds from rising interest rates are expected to decline next year onward, a positive for Vonovia in terms of cash flows from Recurring Sales and Development segments, portfolio revaluation and therefore easing asset disposal pressures to meet debt obligations. The stock may be worth a look for investors willing to tolerate the risk.

For further details see:

Vonovia: Likely Further Pain Ahead But Appears To Be Priced In