VNNVF - Vonovia: Major Discount To NAV And Downside Limited

2023-06-09 11:24:30 ET

Summary

- Vonovia, a European apartment landlord, is trading at a 60-70% discount to net asset value due to its debt exposure and market concerns.

- The company has strong operational performance, with 98% occupancy, rent increases of 3.4%, and 99.9% rent collections.

- I present my analysis leading me a to a buy rating.

I've covered a number of US residential REITs here on Seeking Alpha, some of which trade at very meaningful 30 to 40% discounts to net asset value. Today I want to cover a European-based residential landlord - Vonovia (VONOY) which, although it's not formally a REIT, functions like one.

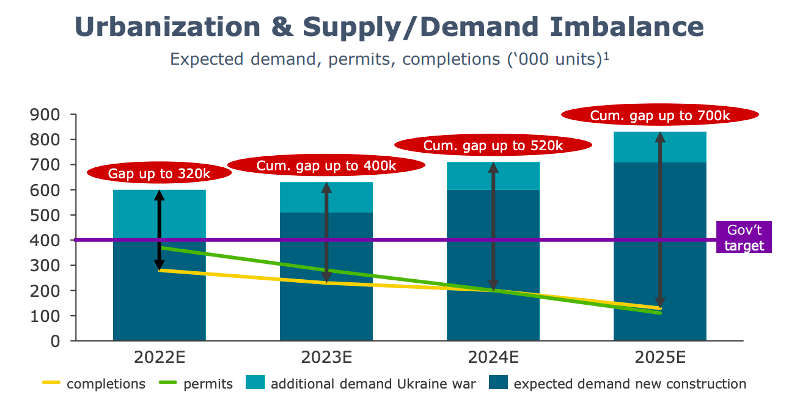

Vonovia is a German apartment landlord which owns over 500,000 apartment units in Germany and about 30,000 units in Sweden. What's really interesting about it is that it currently trades at an extremely depressed valuation of 60 to 70% discount to net asset value, as outlined by a fellow author Jussi Askola in his article . As a European myself, I am quite familiar with the real estate dynamics in Germany and I can tell you that the housing shortage there is much worse than in the US. This is partly because of stringent regulations which have resulted in lower than needed levels of supply, partly because of intense immigration that Germany has seen over the past decade, first with refugees from Syria, and now from Ukraine and also because of the ever rising cost of construction that has been especially now accelerating due to high inflation.

These are structural reasons that are not going to change anytime soon, and it is expected that the gap between supply and demand will widen over time and will reach 400,000 units within just a couple of years. With such a shortage of housing, anyone (including the Vonovia) that owns residential apartments will surely benefit.

{kind=link}

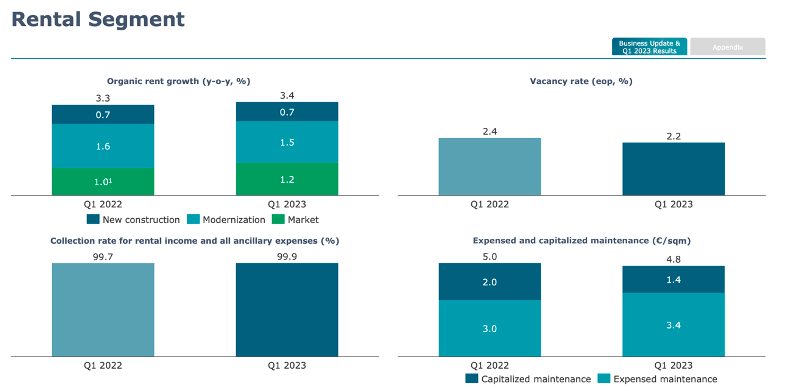

At the same time, the company is trading at an extreme discount because of its debt exposure. It's understandable that high leverage has the market worried, but you should know that operational performance has been nothing, but extremely good over the past year while its share price has plummeted. In particular, occupancy remains at an all-time high of 98%, they have been able to increase the rent over the past year by 3.4% on a portfolio wide basis despite rent regulations in Germany and their rent collections remain at 99.9%. So despite what the share price is suggesting, on an operational level, the company is doing very well and cash flows are increasing.

{kind=link}

Of course, the company does have EUR 43 billion in debt, which is a lot even for their size and represents an LTV of roughly 45-50%. They also have significant debt maturities between 3 and 5 billion EUR each year over the next few years. With group FFO of just EUR 2 billion, the market is rightfully worried that they will not be able to repay these, especially as the refinancing market is essentially frozen and interest rates are really high.

The worries are that they could face a technical default. Management's plan to deal with this has been to dispose of a certain part of their assets to generate about EUR 2 billion in liquidity to repay their bonds due this year and next year. This has been the plan since last fall, but recently they finally achieved it when they signed a deal with Apollo to sell a 30% minority stake in their Suedewo portfolio. This portfolio is a portfolio of properties located in the western part of Germany which are definitely above average apartments when it comes to Vonovia's portfolio, but what really matters is that this deal allowed the company to generate EUR 1 billion in liquidity it desperately needed. Moreover, because there is a long-term option for Vonovia to repurchase the stake back at an IRR of approximately 7 to 8, Vonovia retains all potential upside from the portfolio. This means that this is not a true disposal, but more of a redeemable equity offering. So this didn't trigger a portfolio wide revaluation, which is very important.

The revaluation was, however, triggered by a second disposal, which was recently announced . This was a disposal of some units to CBRE Investment Management which allowed the company to generate an additional EUR 560 million in liquidity and what's important is that this disposal happened just 5% below book value. Again, these were some of the highest quality apartments that Vonovia had on its books, both in terms of their value per square meter as well as in-place rents, but still, it shows that the asset value is not overly inflated.

The company has almost met its EUR 2 billion disposal target which means that all of its 2023 bond refinancing needs are met, as well as two thirds of 2024. Vonovia is now in a position where it trades at a steep discount, essentially trading at $0.40 on the dollar, they pay a solid dividend, which has already been cut which makes it a little bit safer and the downside has been severely limited as their debt repayments are already covered. This in my opinion presents a great opportunity to buy one of the largest landlords in Europe and benefit from the rebound in real estate which is why I rate the company a BUY.

For further details see:

Vonovia: Major Discount To NAV And Downside Limited