VNNVF - Vonovia: Market Is Pricing In Discounts Squared

2023-03-21 15:00:55 ET

Summary

- Vonovia's stock price is offering discounts of 66% on a book value that already seems to be discounted by 25%. Discounts squared!

- Cash production is 12% to market stock price.

- LTV is under control even under a stress test scenario.

- VNA is selling its properties at a 25% premium compared to its book value in the distressed market of Q4 2022, while the market is pricing in a 66% book value discount.

In this article, I present a Vonovia (VNNVF) (VONOY) analysis in two sections: Income position and Balance sheet.

1) The Income position:

FFO is an important measure of how much money a company like VNNVF is making. It mostly comes from the rent they collect from their properties. However, the rental income yield is not very high, with a yield of 3.4% based on the book value of their properties, which is 2.590 EUR per square meter. This means they make about 7.40 EUR per square meter of rental space per month, a multiplier of 29.2X.

Interest rate expense so far have NOT been the main cost for the company right now (sub 500 EUR million in 2022), even though they have a debt of 45 billion with an average maturity of 7.5 years and an average yield on cost of 1.5% (compared to 1.1% in 2021). This means they would now pay about 675 million in interest per year, while their rental revenue is more than 3 billion. The other major cost components are operating costs and capital expense costs, each of which is about 500 EUR million per year.

The company also makes money by selling properties at a premium to their book value (historical premiums of >25% to book value), which generated income of more than 100 EUR million, or 5% of FFO. This also generates net cash inflows of 500 EUR million, which can be used to improve the balance sheet by reducing debt. However, the size of these sales has not been very significant in the past, and the expectation of such sales being a game changer and improving income substantially in a distressed market condition is not realistic.

In summary, FFO is mainly composed of rental income. Interest expense has not been a major cost so far but about to change, and the company also generates revenue from property sales.

Two main challenges:

The company faces two main challenges in its business model. First , if the cost of financing is higher than the income they get from renting out properties, it could hurt their profits. Second, if the cost of maintaining and operating properties increases more than the income from rent, it could put pressure on their overall profits.

Currently, VNNVF is already facing the first challenge, as their new financing costs are higher than their rental income. While it's expected that rental income will increase over time, due to political and legal restrictions, it may happen slowly.

If VNNVF can't sell off assets as planned to decrease their debt, their financing costs could increase by about 0.3% each year (simulated at a stable interest rate environment as of March 20, 2022), i.e. an additional cost of 135 million per year. This will slowly deteriorate their profits unless they can manage to sell off assets as planned.

In 2022, VNNVF had FFO (key figure of operative income) of 2 EUR billion, and their guidance for 2023 is 1.85 EUR billion. In short, if interest rates stay the same or increase, VNNVF's profits will gradually decrease unless they can sell off assets to reduce their debt.

CHART Historical FFO yields to Market Price and Spreads over Bund

Historical FFO yields to Market Price and Spreads over Bund (Vonovia & Author)

{kind=link}

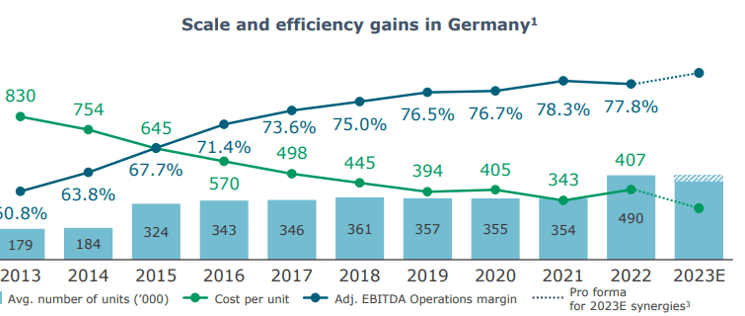

The second point to consider is maintenance and operating costs. VNNVF's management believes that the acquisition of DWNI will lead to synergies that will boost gross margins in the rental sector. Over the past ten years, gross margins have been improving significantly, and VNNVF is focused on controlling costs. They are also proactive in meeting energy efficiency renovation requirements, and are therefore not overly concerned about inflation, renovation costs, or increased capital and maintenance expenses. VNNVF runs an efficient operation with careful planning, scale, and experience, and the market and analysts may be overestimating the potential threat in my view.

CHART: Margin Dynamics and Operation Efficiency

Margin Dynamics and Operation Efficiency (Vonovia)

{kind=link}

In summary, the operating business of VNNVF is generating both cash and income. When investing, the goal is to purchase future cash flows at a discounted fair value, and VNNVF's cash flow production is currently yielding about 12% (FFO yield to market price). This is a relatively high yield for a conservative business. However, there is some substantial interest rate risk since it's uncertain whether rental increases will move in line with the interest rate environment. The interest rate spread of 10% over the bund yield makes this an attractive value investment with a good margin of safety.

Risks to operating income:

- A sustained interest rate environment above 4% for several years

- No rental yield increments

- Additional operational expenses (politically/energy-related or inflationary driven)

- No assets disposal at a book value -10% or higher

2) The Balance Sheet:

The total fair value of VNNVF's properties is around 95 EUR billion, with a net asset value of 45 EUR billion (according to EPRA definitions). This valuation is utilizing a square meter valuation of 2.590 EUR. Under these assumptions the book value per share of the company would be 57 EUR (currently it trades at below 20 EUR, a 66% discount to tangible book value, on the European stock exchanges). Considering that the company has almost 50% leverage the math works out that the current implied square meter price the market is giving to VNNVF's property is about 1.700 EUR (EV of 60 EUR billion / 35 million sqm). Considering that most of the properties are located in G7 German cities, with 25% of them in Berlin, this square meter implied value seems low.

While the value of the properties may be conservative on paper, the actual income they generate through rent is low at 7.5 EUR per meter. Rent growth has been slow in the past 5 years, so assuming that property values will increase based on rental income is uncertain. Additionally the current residential market in Europe is more focused on a multiple compression rather than on the increase of rents, which in some cases and cities is and will be showing double digit growth YoY.

However, it's important to take a step back and look at the bigger picture. Are VNNVF's assets desirable and would they have a market in the absence of interest rate shocks? The demand for housing in big cities has remained strong, but the way people access the market has shifted from purchasing to renting due to affordability issues. This means that the impact on the net present value of an asset is similar regardless of whether people are buying or renting properties, in theory.

To put it simply, VNNVF values its Berlin properties at 3.123 EUR per meter in its books, but it's difficult to find a property at that price on the web. In fact even VNNVF is selling its properties at a 25% premium compared to its book value in the distressed market of Q4 2022. This means that VNNVF is realizing values at a higher price than what it values its properties on the books. Currently, VNNVF trades at a discount of 66% to its book value, but it's actually selling at a higher price than its own book.

While property prices are expected to fall in 2023, it's difficult to predict what will happen due to the uncertainty of the rates environment. However, 7.5 EUR rent per meter is cheap compared to the market rents in cities like Berlin and Frankfurt, which are over 15 EUR per meter, suggesting there is more upside than downside from the rental market. The book valuation price of 2.590 EUR per meter also seems cheap. So, there may be discounts (book value) on discounts (market implied value) going on here on the market capitalization of VNNVF currently.

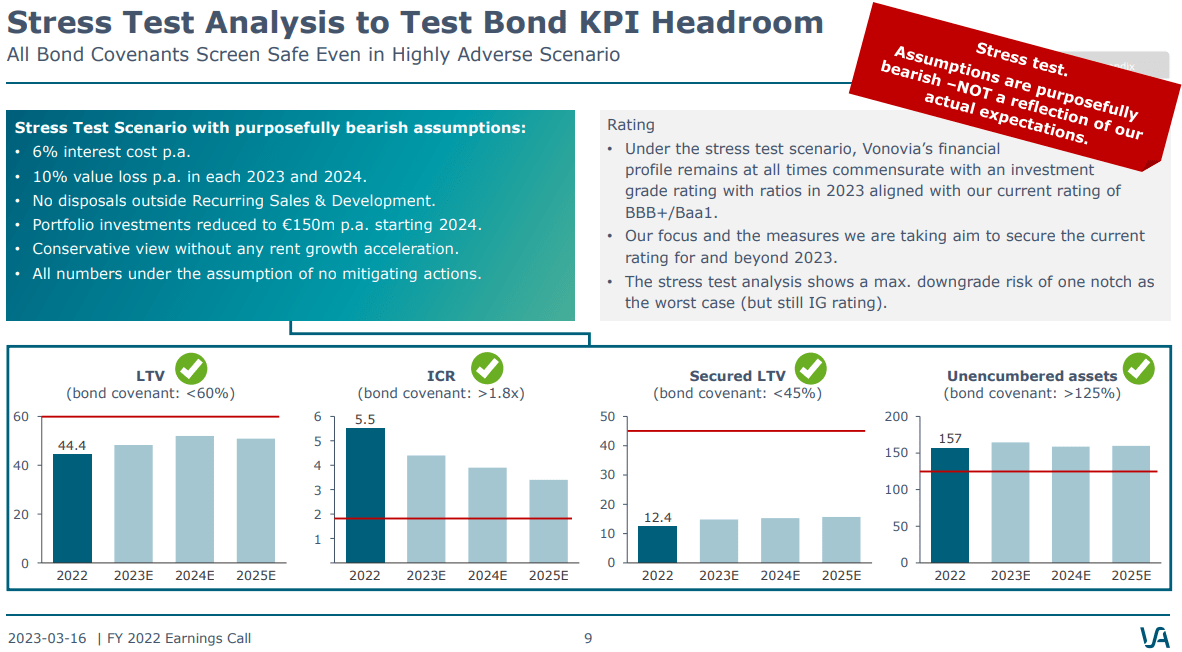

The balance sheet of VNNVF has two parts: assets and liabilities. The writer doesn't have an opinion on interest rates, so the following analysis will focus on the current facts. VNNVF wants to keep their LTV (loan-to-value) ratio below 45%. They have said that they will be able to meet this target even without selling any assets in 2023. Keeping the LTV ratio below 50% is important because if it goes higher, their bond rating could suffer, and things could spiral downwards.

VNNVF has done a stress test (chart below), which shows that they can maintain their LTV target without having to issue further equity. During the conference call, analysts questioned this stress test, especially the assumption of a 10% loss in value in 2023 and 2024.

However, VNNVF's liability side is not at risk for the next 18-24 months. They have an average debt maturity of over 7 years, and no significant maturity coming up. They plan to refinance their 2023 maturity through FFO (funds from operations). Therefore, VNNVF is not in danger of having to sell assets quickly to raise cash to roll debt. The liability side of their balance sheet is well-managed and doesn't pose any immediate risk.

{kind=link}

Conclusions:

The stock is pricing-in discounts on already discounted assets in my opinion. A lot of fear, some of it justified, is being baked-into the stock right now. Considering that the business is of a boring nature, the cash flow yield this company is producing right now is attractive. I feel very comfortable with the balance sheet composition and it provides me with ample margin of safety considering the quality of the assets and the deep discounts I am getting on the current market valuation.

For further details see:

Vonovia: Market Is Pricing In Discounts Squared