VNNVF - Vonovia: My #1 Recession Pick With 8% Dividend Yield

Summary

- Vonovia is Germany's leading residential real estate company.

- It is trading at ~0.35x net asset value.

- The current valuation reflects a German property market collapse of biblical proportion.

- This is an asymmetric risk/reward opportunity.

- Vonovia should outperform in a recession given its defensive characteristics.

This is an update to my previous article on Vonovia SE ( OTCPK:VONOY ) ( OTCPK:VNNVF ) to reflect developments in the macroeconomic environment (expected deep recession in the eurozone), property price index movements discussion and progress on disposals of properties.

I recommend purchasing the stock in the German stock exchange (primarily listing) and not through the U.S. listed ADR.

Background

Vonovia is Germany's leading residential real estate company. Vonovia currently owns and manages ~550K residential units, mostly in Germany, but with some apartments also in Austria and Sweden.

Whilst rental income from holding residential apartments is its main business, Vonovia also has additional segments that include:

- Property development segment

- Recurring sales (disposal of non-core apartments)

- Value-add services (e.g., craftsmen, media, etc.)

Thesis

Vonovia SE is trading at a distressed valuation of ~0.35x net assets. This reflects a well over 30% decline in the German property market. To date, the decline in property prices in Germany has been marginal. Supply of new build properties and modernization are rapidly declining due to skyrocketing construction costs and higher interest rates. Demand for rental properties remains exceptionally strong in urban areas and the shortage of properties has been exacerbated by strong immigration due to refugees from the Ukraine war as well as immigration arising from an acute shortage of labor in Germany. It appears that Germany is on the precipitate of a rental crisis.

Given the high cost of debt capital, Vonovia had to change its strategy and materially reduce its investments in modernization and acquisition of units. On the flip side, it has designated EUR13 billion of properties to be sold over time, with the proceeds utilized to reduce debt and/or deploy towards share buybacks. It is a dynamic capital allocation methodology, so as circumstances change (e.g. interest rates) so will its capital allocation.

However, in the current situation, the strategy is crystal clear. Vonovia has to deleverage and conserve capital to reduce debt and/or buy back shares at well-below intrinsic value. Given the rapidly rising interest rates in the eurozone and macroeconomic uncertainties, the transaction volume in the market reduced materially (more on that later).

So in a sense, what Mr. Market is not seeing as yet is credible execution in terms of large disposals. The market seems to assume based on the current valuation that Vonovia will be forced to launch a fire sale.

Investors must also recognize that the German property market is highly regulated (otherwise known as the Mietspiegel rental index system) and consequently the rental income earned by Vonovia is well-below market rates. The way the Mietspiegel operates is that every two years the rental prices are updated based on the average market rent of the last 6 years. This gives rise to a material lag in rental growth. Rents will and do catch up, but it takes time.

So there are a number of cross-currents in place, including:

1) High cost of debt and inflation in construction costs, which is leading to structural demand/supply imbalance in the medium term. Germany is just not producing sufficient units to support housing formation.

2) Rents will take time to catch up with inflation and shortage of units (albeit recent Mietspiegels have been very strong)

3) High cost of debt is a disincentive for investments in the modernization of apartments as well as the acquisition of units

4) Transaction volumes in the market have come down materially. Prices though have only shown a moderate decline (but more on this later)

From Vonovia's perspective, there are several paths to a strong recovery of the share price:

- Disposal of a large number of properties at or near book value. Either directly in the market or through a tax-efficient JV structure

- Interest rates will come down materially (e.g., 10-year bond below 1.5%)

- Through rental income growth in the medium term

A recession is bullish for the stock

A serious recession in the eurozone is likely to bring down long-term rates materially. This should enable Vonovia to refinance its debt at lower interest costs. Importantly, given rental levels are materially below market and strong demand due to chronic under-supply, Vonovia's top line should not be adversely impacted. In other words, Vonovia is a defensive investment that should work well in a recession, assuming interest rates will decline.

State of the German Property Market

The new mortgage contracts indicator provides a snapshot of activities in real estate and house construction by private households. The most recent reading (as of calendar week 22, 2022) shows that the number of new mortgages is about 25% lower than a year ago. It was as much as 40% down during the 4th quarter. This is not unexpected given the rapidly rising interest rates that flow through to mortgage costs and affordability.

{kind=link}

How about the transaction prices?

There are several providers with different data points.

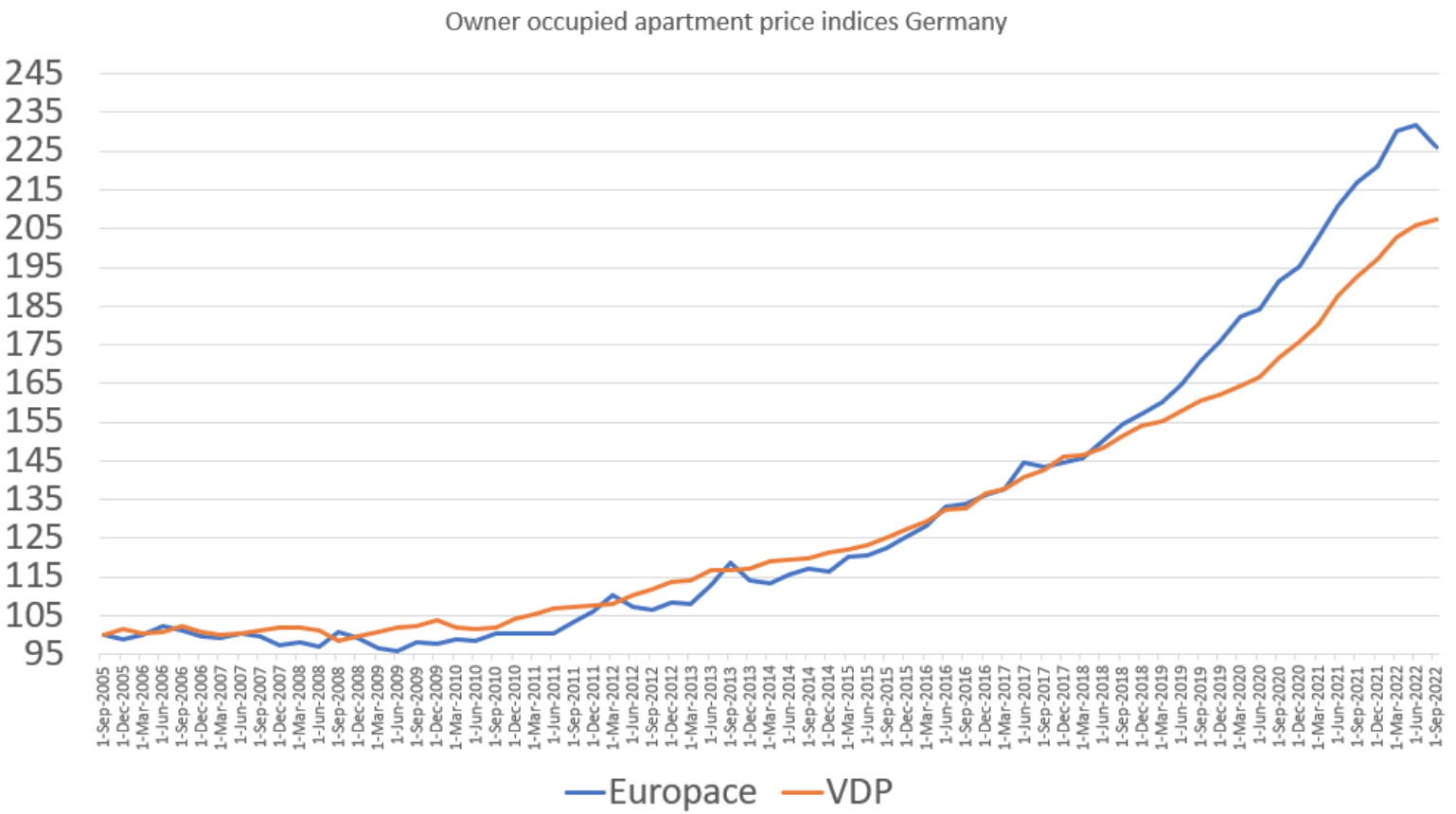

The Europace housing index's latest release is showing that prices have dropped by 1.8% in November, following a drop of 1.26% and 0.51% in October and September respectively. Year over year, the overall index is showing gains of 1.5% in November.

The commentary provided in the report is as follows:

The Europace house price index shows clearly falling real estate prices in November. Only the segment of new single and two-family houses shows stable prices. The real estate market is in a state of upheaval, with prices continuing to fall, interest rates rising and inflation also high, and the next few months will show how quickly the market will find a new balance

Note that the Europace House Price Index EPX is based on actual real estate financing transaction data from the Europace financing marketplace. With around EUR 85 billion annually, more than 20 percent of all real estate financing for private customers in Germany is processed via Europace.

Other official Federal government statistics are showing slightly different trends, with prices in the 3rd quarter down 0.4% quarter on quarter and up 4.9% year-on-year.

A comparison of the relevant indices is shown in the below chart (thanks to @Hhnwg who regularly posts insightful information on Twitter relating to the German real estate market):

{kind=link}

The Europace index appears to be more volatile than official Federal government statistics.

Nonetheless, it appears that there is certainly a decline in the German real estate market due to interest rate shocks. However, at this stage, it appears to be quite minor with declines of between 0% to 5% from the peak. Given the backdrop of a chronic shortage of supply, I do not foresee peak-to-trough declines that will materially exceed 10%. Currently, the share price is factoring in a decline of greater than 30%. Additionally, Vonovia marks its assets rather conservatively. For example, recurring condo sales are routinely disposed of at a premium of 35% to 40% of book value.

So in short, the margin of safety is wide, even if the decline becomes much more significant than I expect.

Progress on assets disposals

This is clearly a key catalyst, and frustratingly there is not much to report as yet.

Having said that, If Vonovia will announce a major disposal, for example, a JV partnership with a pension fund with the consideration agreed at or near book value, the share price will literally melt up.

The JV option is uniquely attractive for several reasons. Firstly, it is tax efficient as there is no disposal of the underlying property. Secondly, Vonovia remains the asset manager and should generate a risk-free income stream in the form of a management fee. Finally, it provides a quasi-equity source of capital to buy other distressed assets. This could be a win-win scenario for both Vonovia and a would-be capital provider. So I am keenly waiting for an update from management on this point in the next earnings call.

Other than that, the only notable disposal that is currently in progress is the sale of ~3000 units to the City of Dresden . This should generate proceeds of ~EUR300 to EUR350 on a pre-tax basis.

Final thoughts

In my view, this is an asymmetric risk/reward opportunity.

There are several paths for a material share price appreciation. It could progress on the disposal program (EUR13 billion portfolio now designated as held-for-sale), interest rates coming down (with or without a recession), or simply waiting (in the medium term) for rental growth to catch up with inflation. In the interim, shareholders are paid to wait with a dividend yield of ~8%.

Importantly, Vonovia should outperform the market in a deep recession, as I expect interest rates to decline in such a scenario and acknowledge the defensive nature of its assets portfolio.

Vonovia remains my #1 pick in the real estate space.

For further details see:

Vonovia: My #1 Recession Pick With 8% Dividend Yield