VNNVF - Vonovia: On The Brink Of A Permanent Value Impairment

2023-03-28 07:15:23 ET

Summary

- There is a clear consensus among Seeking Alpha analysts that one should enter a long position in Vonovia. In my opinion, the underlying fundamentals justify making the opposite move (i.e., going short).

- In the past decade, Vonovia has thrived in the low-interest rate environment by owning properties at tiny yield levels, which slightly exceed its cost of financing levels.

- Now Vonvovia's debt is yielding ~6%, which is considerably above the ERPA net yield of 2.6%. Namely, properties are generating lower returns than the cost of debt.

- In 2022, Vonovia did make a slight fair value adjustment for its properties, but the magnitude of adjustment was much lower than market fundamentals justify.

- Inflated book values, the skyrocketing cost of debt, and a systematic tightness in the European banking sector lead to a clear sell recommendation.

Vonovia SE (VONOY) (VNNVF) is a European REIT, which manages a multibillion dollar portfolio of residential properties that are mainly located in Germany. Currently, there is a strong consensus among Seeking Alpha analysts for longing Vonovia.

SeekingAlpha

In my opinion, the underlying argumentation lacks basis and stems from the currently attractive dividend yield (albeit a significant part of it comes in script dividends), which might seem safe given Vonovia's portfolio and secular tailwinds for residential properties.

However, I strongly believe that the financial prospects for Vonovia are extremely weak and the Company will eventually be forced to issue a massive amount of new equity to close the financing gap.

Here are three reasons backing my expectation.

1. Portfolio yield significantly below cost of financing rate

Historically, Vonovia has successfully capitalized on the low interest rate environment by assuming significant amounts of leverage to acquire and develop new residential properties yielding on average 100 - 300 basis point above the cost of financing rate.

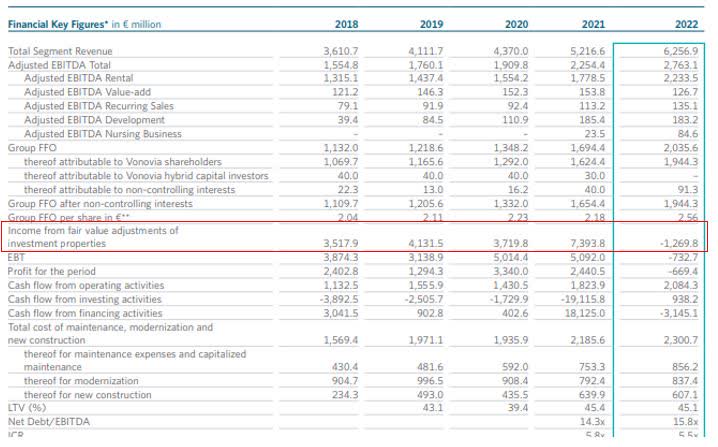

To see how the strategy translates in numbers, we can take a look at the ERPA net initial yield and weighted average cost of debt figure in 2022. Vonovia's ERPA net initial yield, which measure the net annualized yield against the gross fair value of portfolio, stood at 2.7%, while the average cost of debt was 1.5% in 2022. The positive spread between net initial yield and cost of debt leads to positive profitability and cash generation.

There have been several reasons why such strategy was at least historically justified (i.e., acquiring and developing properties at so low yield levels):

- Negative interest rates in Europe that made cost of debt very cheap. For instance, in 2021 Vonovia's average cost of debt was 1.1%, which is something unimaginable for the US players.

- Surging residential property prices consistently reaching all-time highs. This process allowed to recognize several positive fair value adjustments, thereby inflating the asset book values, which helped reduce the indebtedness at least on paper.

- Insufficient supply in the housing market that warranted an assumption of steady rent hikes in the future.

I think nobody can argue against it that Vonovia's average cost of debt level of 1.5% in 2022 is not sustainable and that it will likely take a significant upswing in 2023 and years ahead. An uptick of 1.3% in the cost of financing would automatically put Vonovia in a very difficult position. Assuming no material rent hikes and no new projects coming online, which yield considerably above the cost of financing, the portfolio yield would fall below the level, which is required to generate excess profit.

We know for certain that the average cost of debt will increase. At the same time, we should be cautious about Vonovia's ability to deliver positive like-for-like rent growth. There are three reasons for this:

- According to the German statistical bureau, the real earnings dropped by 3.7% in 2022 and carry a negative outlook for the upcoming year.

- The German construction cost index has increased dramatically from 110.7 in 2020 to 135.3 in 2022, making it more expensive to both finish existing development projects and embark on new CapEx activities.

- Currently, Europe is still suffering from elevated inflation levels, which will inevitably put a strain on Vonovia's operating expenses (e.g., labor, maintenance, energy costs for vacant properties etc.)

Given the above, I do not see how Vonovia could avoid landing at a negative spread territory between its ERPA net yield and cost of financing. Obviously, this does not automatically mean that in 2023 or even 2024 Vonovia should undertake a massive equity injection event, but it certainly does increase such probability in the medium-term.

2. Overly aggressive approach on fair value adjustments

Since Vonovia is based in Europe, it complies with IFRS accounting rules, which requires periodic fair value assessment and adjustments for the properties under management. Interestingly, that from 2018 to 2021 (including) Vonovia consistently recognized positive fair value adjustment for its properties, thus strengthening its financial leverage metrics.

{kind=link}

Finally, a negative adjustment took place in 2023, albeit at very insignificant level - 1.2% from total portfolio value. This is very hard to believe given that ECB's rates have gone from negative 0.5% in 2018 to 3% in 2023 (2.5% as of year end 2022).

For instance, looking at comparable European REITs operating in the residential segment such as Kojamo Oyj (KOJAF) and Heimstaden AB, they all have made more considerable fair value adjustments than 1.2%. The average adjustment percentage is between 6 to 10% from the total portfolio value. One could argue that even these levels are overly optimistic and that the underlying values should drop further, more in line with the overall share price development.

Moreover, the publicly disclosed valuation parameters for rental segment indicate a shocking and overly aggressive assumption. The risk-free rate used for estimating fair value of rental segment was set at 0.4% level in 2022 (see annual report 2022, page 179 ) even though as we know the real levels are much higher.

For Vonovia it is extremely important to hold favourable book value and avoid material adjustments to the downside. The Company's bond covenants for LTV and unencumbered assets-to-unsecured debt stipulate <60% and >125% levels, respectively. Ending financial year 2022, Vonovia had 44% of LTV and 157% of unencumbered assets-to-unsecured debt ratio.

While there is some headroom, it is definitely not ample and if there is a combination of material fair value adjustments and increased total debt, Vonovia could fall in a serious problem. At the 2022 financing levels, fair values should drop by 25% for Vonovia to breach its covenant metrics.

3. Tight financing conditions making debt rollover very painful

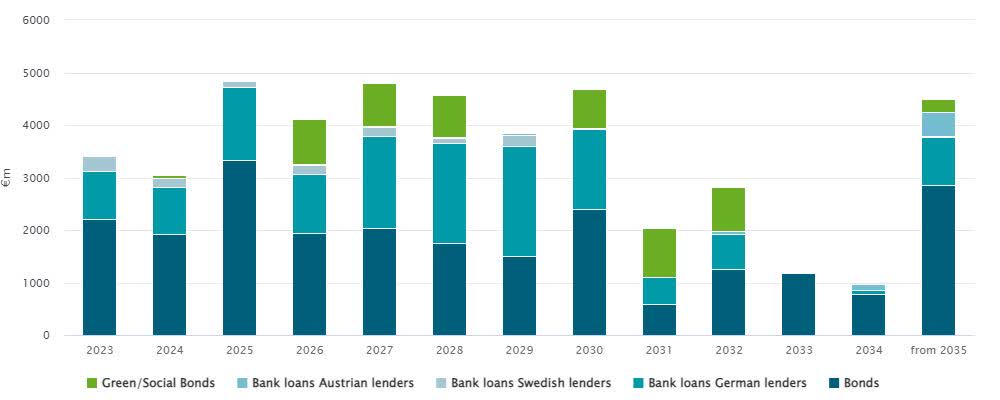

As mentioned earlier, Vonovia entered 2023 with a very strong average cost of debt comparable that will certainly be exceeded in a negative way. The prevailing cost of debt levels look very bad for Vonovia both from the historical and portfolio yield perspective. One of the most recent bond issuances held in late November 2022 resulted in ~ 5% YTM. Currently, this bond trades 6% below par indicating even more elevated cost of debt levels. Other outstanding bonds trade at very similar yields with longer dated at 7-8% YTM levels. The fact about positive spreads between shorter and longer dated instruments is important in the context of Vonovia's financial strategy. Historically, Vonovia has tried to assume a laddered (evenly distributed) debt repayment schedule to achieve stability and predictability in the refinancing rounds.

{kind=link}

With interest rates at these levels and Vonovia's sensitivity to changes in the financing costs, we could expect a significant shortening of the duration profile. In the short-term it could save some 100 - 200 basis points in the average cost of financing levels, but it still will not be enough to offset interest rate spikes in the 2 - 5-year debt financing instruments.

In 2023, Vonovia will have to refinance roughly EUR 3 billion of debt from which EUR 1 billion is hedged with swaption, which partially reduce the outright negative effect from higher financing rates. Assuming that EUR 2 billion is refinanced at 6% interest rate and that half of the bank loans become more expensive in line with the current EURIBOR levels, we would be talking of about ~ EUR 450 million in incremental interest cost. My assumptions about half of bank loans being subject to floating rate is purely discretional. Vonovia does not disclose its quantitative sensitivity to interest rate changes nor does Vonovia disclose the amount of outstanding debt linked to floating structures. Plus, in Europe it is a common practice among banks to prefer floating rate instruments.

If we instead took a very aggressive approach and applied the prevailing debt financing levels to all of Vonovia's outstanding liabilities, the result would land at an increase of ~ EUR 2 billion in an annual interest cost. This would in turn wipe out all of the generated FFO in 2022.

The previous scenario, which is definitely more realistic for 2023, implies a 22% reduction in FFO figures. In the short-term Vonovia can withstand such effects, but if it does not manage to reverse the course of a gradual convergence to the market-based interest levels, there is a high chance of value-destructive measures being implemented.

Lastly, Vonovia has to refinance EUR 1.2 billion and EUR 1.1 billion of secured bank financing in 2023 and 2024, respectively. This creates an additional challenge because European banks at the current moment are rather defensive and have a conservative stance against vulnerable sectors such as European real estate. The combination of tightened lending standards and falling collateral values implies that Vonovia will struggle in accessing full amounts of the required refinancing. Most probably, the Company will have to tap into the bond market space to source more flexible capital, albeit at more expensive levels.

The bottom line

Vonovia's previous business model was based on an ultra-low interest rate environment, where massive amounts of leverage were assumed to magnify the tiny spread between the property yields and cost of financing. Now, the cost of debt has skyrocketed for Vonovia increasing from ~ 1% to ~6%. Given more or less constant rents, the elevated financing costs in conjunction with an overall tightness in the European lending policies send a scary signal to Vonovia's shareholders. In the short-term due to a well-laddered debt portfolio and some solid hedges, the Company will manage to absorb the costs. However, in the long-run if the interest rate environment does not improve, Vonovia is subject to either massive share issuance or bankruptcy.

Going long Vonovia boils down to a pure play bet on the interest rates, which if not changed or decreased will likely disappoint investors.

For further details see:

Vonovia: On The Brink Of A Permanent Value Impairment