VNNVF - Vonovia SE: Undervalued And Possible Upside If Rates Drop

2023-03-07 04:40:59 ET

Summary

- In 2022, the shares of Vonovia suffered a loss of almost 50%.

- The number one reason for this selloff is the rate hike in the Eurozone, which forces Vonovia to change its business model.

- The management was quick to recognize the rising risk and adjusted the business model adequately.

- I spoke to their senior investor relations manager about the current problems and am assured they are making the right moves.

- The market was too harsh in its judgment, leading to a significant undervaluation. Since the start of 2023, the share price has gained almost 26% until declining to just +4%YTD.

Thesis

Vonovia SE (VNARF), (VNNVF), (VONOY) is Europe's largest real estate company, owning more than 550,000 residential units in Germany, Austria, and Sweden. Even though it doesn't have a REIT status, it is to be seen and analyzed as such. In the last few years, Vonovia laid its focus on debt-driven mergers & acquisitions (M&A), meaning they heavily bought and built units and acquired other real estate companies like the Deutsche Wohnen SE in 2021, which they purchased for 19B EUR. This strategy has helped them to generate peer-beating growth and returns for its shareholders. As a side effect, debt rose significantly, leaving them heavily indebted. This was fine in times of 0% rates as the debt was very cheap, and more cash was easy to get. Since the start of the year, this has dramatically changed, with rates in the Eurozone changing from 0% to 3%. The market feared that the rising costs of its debt would crush the earnings, potentially threatening the dividend for which Vonovia is known. Additionally, the increasing costs of energy in European countries and the risk of a recession also weighed on the stock price. The market did too much, and part of the sell-off is unjustified, generating a buying opportunity. In this article, I want to explain how these risks could develop in the coming months and years and why I see the sell-off as unjustified to this extent. To assess this, I spoke to Oliver Larmann, Vonovia's senior investor relations manager, to see if they plan to adjust their business model to the new market environment or want to sit this out until we see lower rates again.

Short company overview

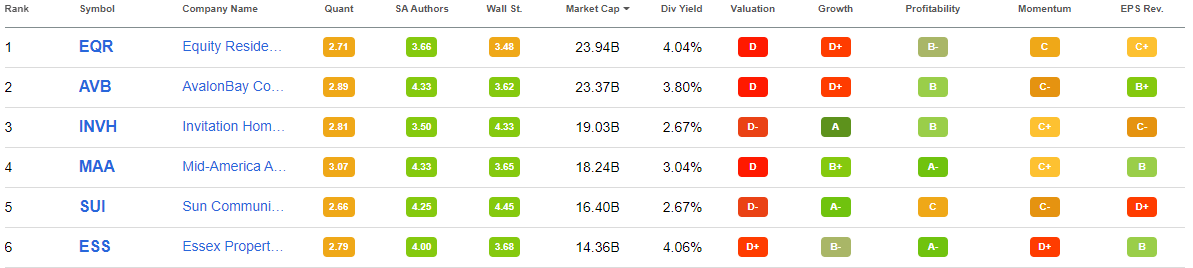

With more than 550K units, worth over $99B, spread over Germany, Sweden, and Austria, Vonovia is Germany's largest real estate company. I have searched for other residential REITs with the Seeking Alpha Stock Screener to understand how big Vonovia is compared to similar REITs. If you scan for "Residential REITs," you get 18 results. I sorted them for the market cap to see the biggest at first.

Result Seeking Alpha Stock Screener "Residential REITs" (seekingalpha.com)

{kind=link}

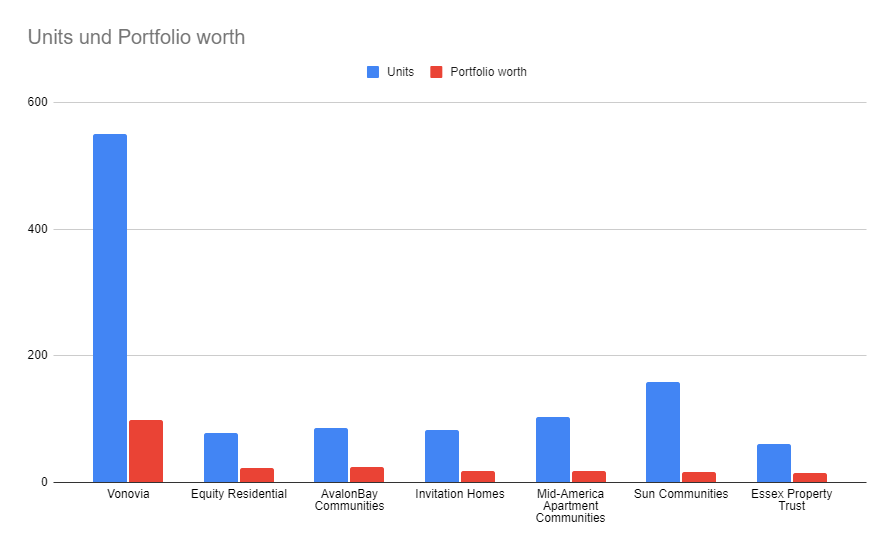

If you compare Vonovia with them, you get a picture of how big Vonovia is. Vonovia has nearly as many units, and portfolio worth as the six biggest residential REITs sorted for market cap. All the six REITS combine 565K units with a total value of $100.2B against Vonovia's 550K units worth $99B.

Vonovia compared to the six biggest residential REITs (Author)

{kind=link}

Contrary to this is the difference in market cap. Vonovia is worth $19.4B, while these 6 combine a $115.75B market cap. Seeing how big Vonovia is made much difference to me when first analyzing the stock. A market cap of $19.4B while holding assets worth $99B means you can buy a part of Vonovia's assets by paying 19.6% for it. In other words, Vonovia's current share price offers you a discount of 80.4% on real estate.

Furthermore, residential units are not the only thing Vonovia uses to generate revenue. It also manages over 72K units for other companies and owns almost 9K commercial units and over 160K garages and parking spaces. Beneath managing and renting these units, Vonovia has three more segments, including:

- Property development: building units to hold or to sell.

- recurring sales: regular and sustainable disposals of individual units and single-family houses

- Value-add services: housing-related services they offer their tenants, like multimedia, energy, and internal cost savings (from craftsmanship, for example)

These additional segments generate about 49% of Vonovia's revenue, while renting generates 51%. I like that revenue structure because it diversifies and means less risk due to rent-specific factors. Geographically, Vonovia is less diversified, with 80% of its revenue from properties in Germany and the other 20% from Sweden and Austria. Considering the strong housing market in Germany, I am fine with relying on Germany.

The debt-driven growth business model has helped Vonovia become the big player they are now. In 2013, when Vonovia came public, they had 175K own units and 26K, which they managed for others. Since then, they have grown their rental units by 24% CAGR to 550K units today. Including all the other properties, like garages and parking spaces, we get a CAGR of 32.6% since 2013. This massive accumulation and building of properties resulted in considerable cost-efficiency savings, as they portray for the German sector in their latest earnings presentation.

Scale and efficiency gains in Germany (vonovia.com)

In general, Vonovia is working quite efficiently, generating excellent profitability metrics, like the following:

- EBITDA margin: 46%

- FFO margin: 34%

Especially the FFO margin is relevant since Vonovia should be analyzed as a REIT, and the Funds From Operation ((FFO)) give the best picture of their earnings.

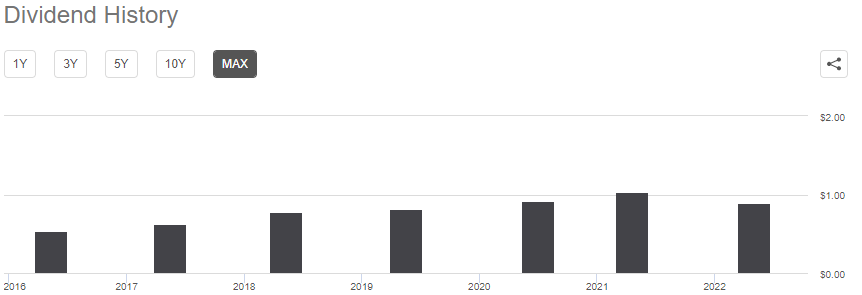

A big part of Vonovia's FFO is given back to shareholders as a dividend, for which Vonovia is well-known. It is high currently, yielding 7.2% as of the time of writing. As you can see below (for the ADR VONOY), Vonovia never missed a dividend and raised it yearly with a track record back to 2013 for the German-based ticker VNA.

Vonovia dividend history (seekingalpha.com)

{kind=link}

Vonovia pays out 70% of its Group FFO, which is why the dividend projection for 2022 is below the one for 2021. As soon as the year has ended and the exact Group FFO is known, this will be updated and should be higher.

Besides the above-mentioned internal growth of Vonovia, they also managed to generate market-beating returns for shareholders until the stock dropped 60% this year, down over 70% from its all-time high.

The reasons for the sell-off align with the overall risks, especially for the European market. Rising rates are the biggest threat that is waying the most on the share price. Furthermore, the market doesn't like the risks presented by the European energy crisis and a declining housing market. I will explain the market's reaction in more detail in the following.

Rising rates

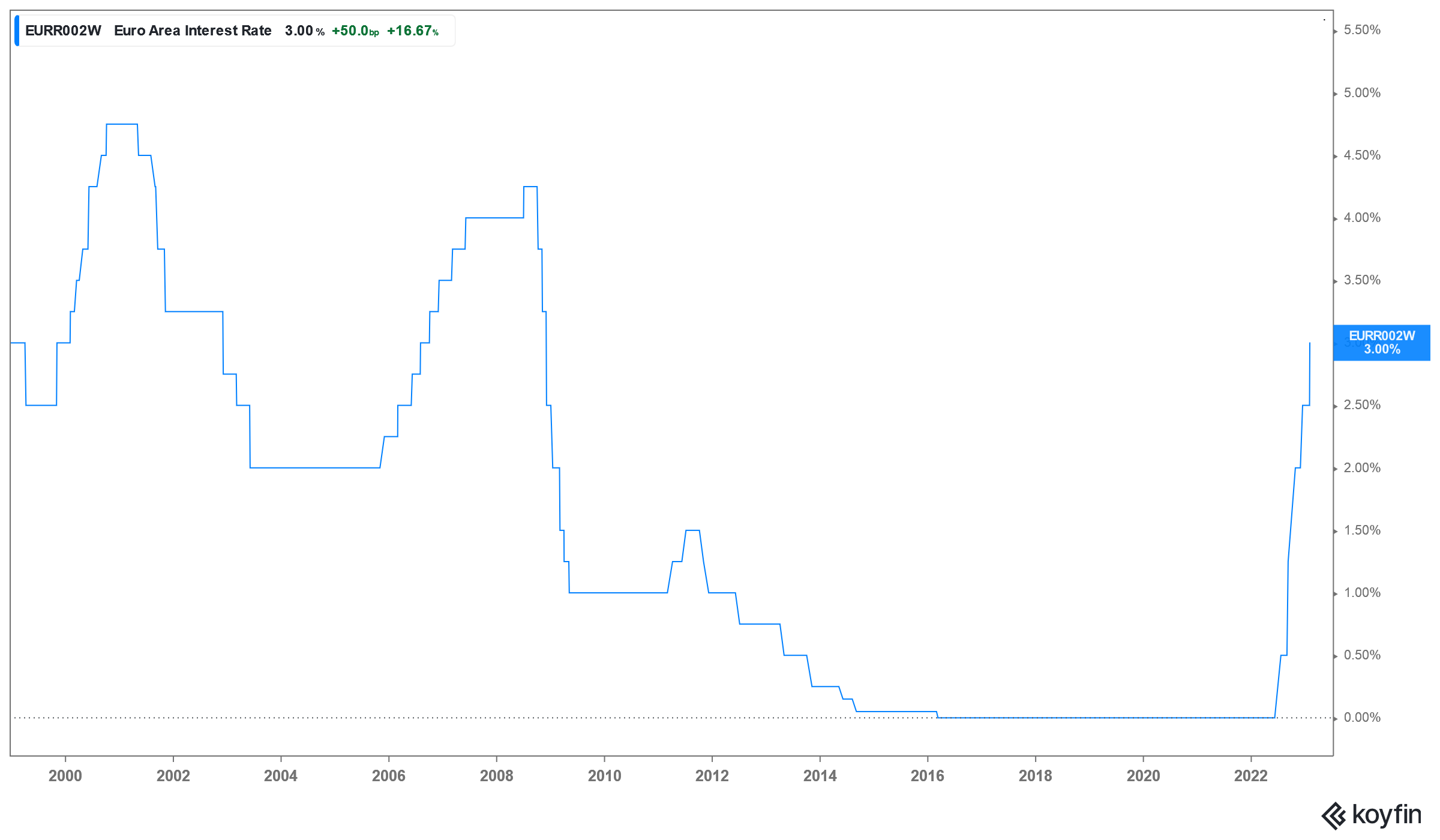

For the first time since 2016, the European Central Bank ((ECB)) raised rates due to 40-year high inflation. In doing so, the rate has reached 3%, a level the Eurozone hasn't seen since 2009.

Euro area interest rate (koyfin.com)

{kind=link}

The fear is that higher debt refinancing costs will impact Vonovia's earnings and danger the dividend. Considering the business model, the fear is understandable. Recently, Vonovia used cheap money to accumulate many units or whole companies like the Deutsche Wohnen SE in 2021. The result is obvious: Vonovia has a lot of debt. €43.6B to be exact.

What could rates do?

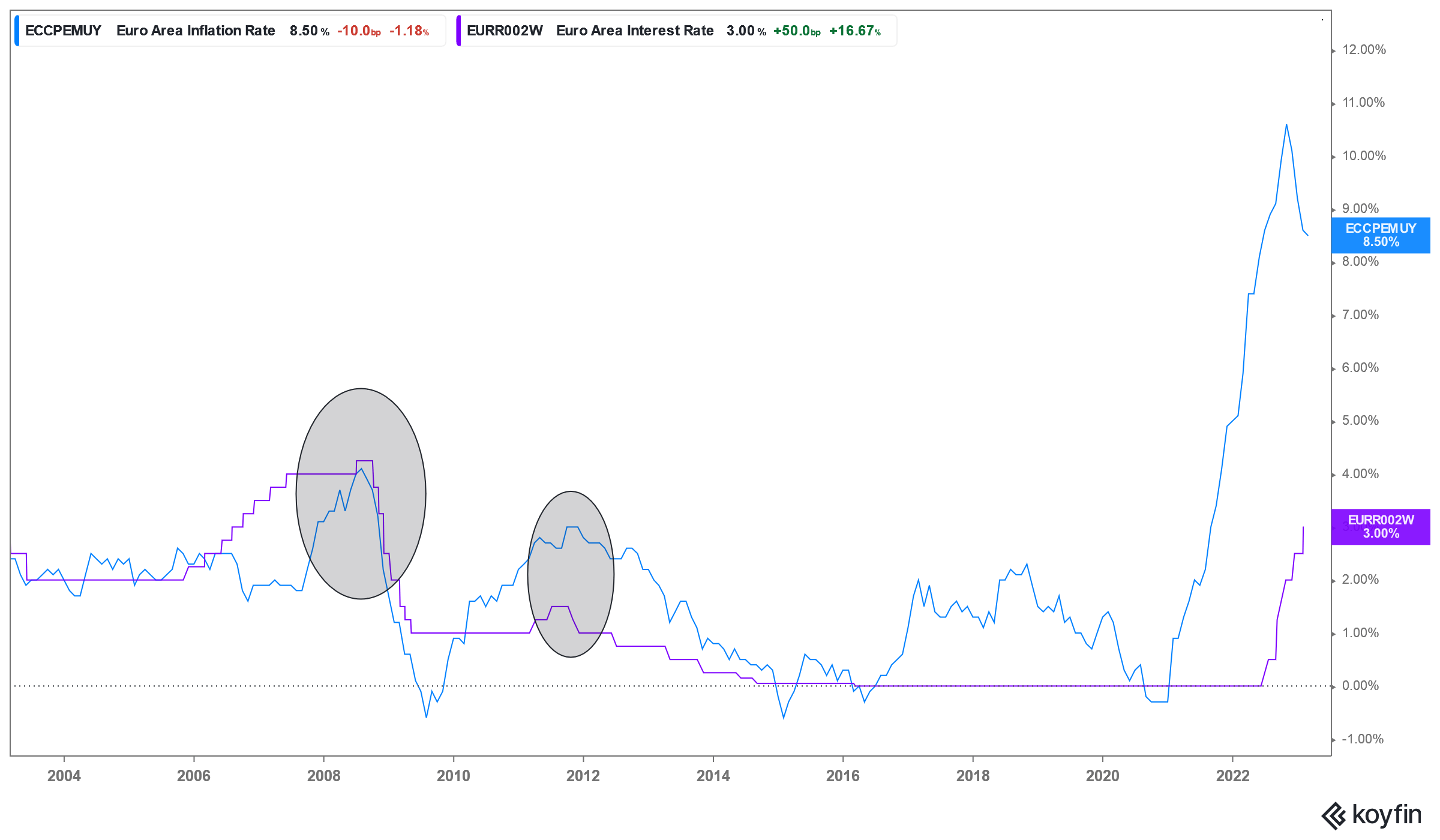

Rate hikes could peak as early as this year. Maybe even in the first half. Data on the past 20 years of Eurozone inflation and interest rates reveal that the interest rates peaked shortly before or after the inflation rate.

Eurozone inflation and interest rate (koyfin.com)

{kind=link}

Assuming the past will repeat itself, and the projections for the inflation peak at the end of the year are correct, the rate should peak either at the beginning of 2023. Considering that the ECB has to adjust the rate to be bearable for 19 countries instead of just one country like the FED, it convinces me more that the rate will drop, or at least stop rising, as soon as inflation is tamed. The Eurozone has countries like Spain, Italy, Greece, and now Ukraine, who are so indebted that they can't handle anything above 0% for a very long time. That is the main reason why the ECB was so hesitant to raise the rate at first. The first rate hike occurred when inflation was already at 9%. Through my job at a bank, I have access to research material from the second biggest bank in Germany and one of Europeans most prominent asset managers. In addition to the general public, these expect rates to stop rising and quickly fall again as soon as inflation seems to be under control. As you can see in the chart, inflation has already dropped sharply and is projected to continue declining. The Deutsche Bank ( DB ), Germany's biggest bank, expects rates to climb to 3.75% at max and stay there until mid-2024.

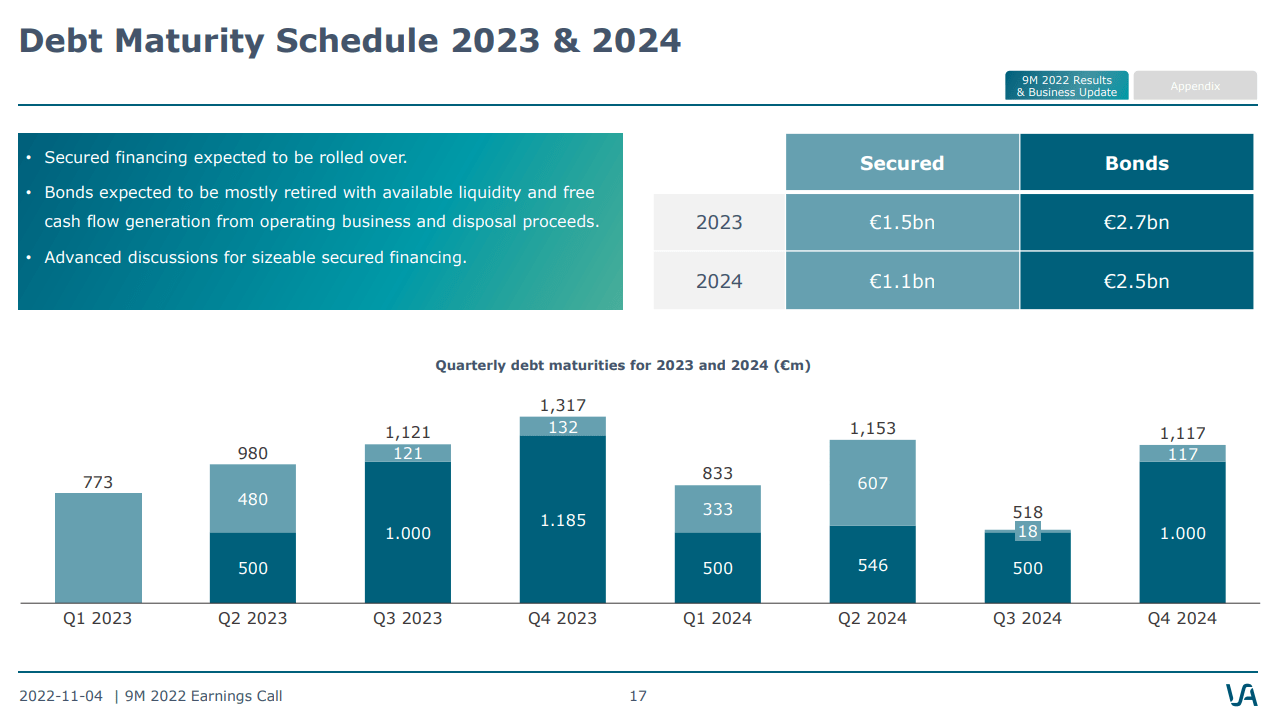

Debt Maturity

Debt maturity for 2023 and 2024 (vonovia.de)

{kind=link}

In the next two years, €7.8B of debt will mature, creating the refinancing risk the market fears. To assess how much the refinancing costs could change, I looked up rates of bonds Vonovia emitted in the past in correlation to the past and current market. Considering we currently have a 3% interest rate, my calculations result in a 4-5% refinancing rate. This is significantly more than the average cost of capital of 1.3% as of 09/30. The capital costs for the next two years could change from €101.4M (1.3% cost of capital) to €351M (4.5% cost of capital). Theoretically, we could apply this calculation to the whole debt of over €43B and would get an earnings-crushing result. Practically, the entire picture looks a lot better.

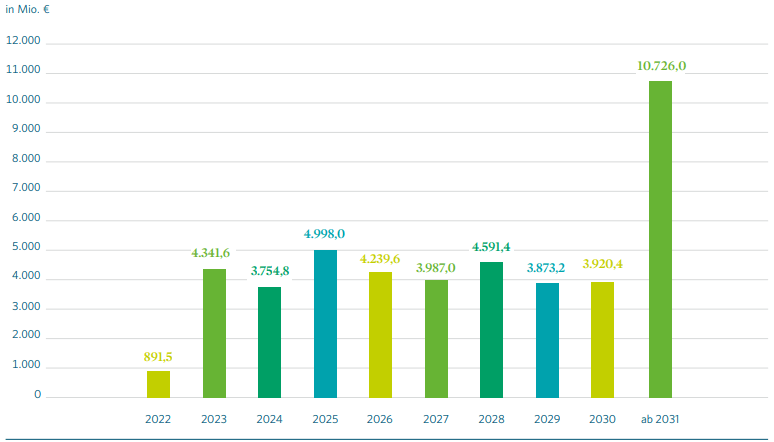

Vonovia debt maturity (vonovia.de)

{kind=link}

Vonovia has a very balanced maturity of its debt, with a fourth of all debt maturing after 2031.

Changes in the business model

When I first analyzed Vonovia's business and the rate hikes in mid-2022, I thought they would have to change their business model from a debt-fueled growth company to a low-debt asset manager. After talking to Oliver Larmann, Vonovia's senior investor relations manager, he told me Vonovia isn't planning to change its business model yet. Instead, they want to sit out the time of elevated rates, use sales proceeds to cover the debt, and continue with its original growth-focused business model as soon as rates decline again. Considering the high probability that rates will drop quickly, this is the right plan. Growth prospects are still excellent, considering the real estate market Vonovia works with. Especially in Germany, it got substantially harder for ordinary citizens to buy real estate, which makes it more accessible for companies like Vonovia.

Furthermore, Oliver Larmann told me they calculate with the current elevated rate for future refinancing. If I am right and the interest rate drops in the following months/years, that could mean that Vonovia will either raise its guidance or beat it.

Conclusion

Vonovia made the right choices and pursued the right path in managing the interest rate risk. I expect them to regain growth as soon as the time of elevated interest rates is over. The valuation gives you a significant discount on real estate assets and compensates for the risk of more prolonged and higher-than-expected interest rate levels. Compared to the six biggest US residential REITs, Vonovia is a good addition, especially if you seek some exposure to European stocks. As long as rates stay high, the share price will likely run sideways, but as soon as rates drop, I expect the share price to gain appropriately. Until then, you get rewarded with a dividend yield of over 7%.

For further details see:

Vonovia SE: Undervalued And Possible Upside If Rates Drop