VNNVF - Vonovia: There Is Still Room For More Gains In The Long Run

2023-07-26 16:09:17 ET

Summary

- Vonovia SE, Europe's largest real estate company, has seen a 23% gain in the last month and a 35% gain from its low in March, despite being down 7.5% YTD.

- The might be more gains to come considering the current situation of the real estate market and interest rates.

- Despite a booming DAX40 index, key indicators suggest the German economy is slowing down, questioning whether the ECB can risk further rate hikes.

- The European Central Bank (ECB) is likely to halt rate hikes, indicating that the worst may be over for the real estate sector.

- Analysts predict significant return potential for Vonovia, backed by a recent rating upgrade from Deutsche Bank, making it an attractive investment opportunity.

Thesis

With over 23% gain in the last month and over 35% gain from its low in March, Vonovia ( OTCPK:VNNVF ), ( OTCPK:VONOY ) had a good rally in recent months. Considering the stock is still down 7.5% YTD and 65% from its high in September 2020, the underlying business/real estate market in Germany could further improve and rates in the Eurozone have still to drop, I see the potential for further gains.

In this article, I will describe the newest development in the German real estate market, rather than talking extensively about the specifics of Vonovia's earnings or company profile. I did this in my last article which I will give a brief summary about.

I maintain the thesis that the real estate market has already improved and could improve further. The newest data about the German economy could be a sign of the rate drops I also talked about in my last article. Therefore, I see Vonovia's stock in a favorable position right now.

Summary of my last article

In my last article , I wrote about Vonovia SE, Europe's largest real estate company, which employs a debt-driven growth strategy. The strategy has enabled Vonovia to expand its portfolio to over 550,000 residential units in Germany, Austria, and Sweden and deliver robust returns to shareholders. However, the recent interest rate hikes in the Eurozone have raised concerns about the sustainability of this approach.

Vonovia not only rents units but also operates in property development, recurring sales, and value-added services sectors, diversifying its revenue streams. Even though the company heavily relies on Germany, the strong housing market offers a degree of security.

Since its public offering in 2013, Vonovia has grown its rental units by a 24% Compound Annual Growth Rate ((CAGR)), demonstrating its efficiency with a 46% EBITDA margin and a 34% FFO margin. Its consistent and annually raised dividend, yielding 7.2% at the time of writing, further strengthens its appeal.

However, Vonovia's stock recently dropped by 60% due to concerns about the European energy crisis, a potential housing market downturn, and rising interest rates. Although these challenges are real, the likely peak in rate hikes and a subsequent fall once inflation is under control could create a buying opportunity.

Vonovia will need to refinance €7.8B of its €43.6B debt in the next two years, potentially at higher costs due to current interest rates. Yet, the company intends to weather the elevated rate period and continue its growth-focused strategy once rates decline.

In conclusion, I expressed optimism about Vonovia's strategic approach to interest rate risks and its potential for future growth. I believe the current valuation could offer a substantial discount on real estate assets, and the high dividend yield further enhances its investment attractiveness.

Current developments in the real estate market

There are several German reports that analyze the German housing market and its possible future. In the following, I will tell you my takeaways from The Deutsche Bank report to assess what the German housing market could possibly do in the future. I chose the report from Deutsche Bank because in my opinion here in Germany they have one of the greatest and most high-class talent pools when it comes to real estate analysis.

Deutsche Bank report published 04/18/2023:

Triggered by rising interest rates and a more stringent regulatory environment, the German housing market is currently experiencing a downward phase. This comprehensive report examines the market's trajectory from 2010 to 2021, highlighting a significant price surge followed by its current decline.

As part of the European Central Bank's monetary normalization, the authors analyze the impact of rising interest rates on property prices. They suggest that while the inflation and corresponding higher interest rates have temporarily halted the price boom, fundamental supply shortages and other factors will ultimately keep prices supported.

There is a growing discussion about tightening exchange and renovation obligations, which could also have a price-dampening effect. The regulatory environment, particularly the implementation of the climate package and CO2 levy, has caused renovation costs to factor into prices, thereby dampening them.

Throughout the entire decade, supply shortages are expected to persist in major cities such as Leipzig, Stuttgart, Munich, Berlin, Heidelberg, Hannover, Cologne, and Frankfurt. In 59 out of 126 cities, demand exceeds supply in 2023, and this trend will continue with 35 cities still experiencing supply shortages by 2030. Prices, despite temporary reductions, are ultimately driven by the underlying supply shortage.

The stringent regulatory environment and the incentive for investments due to very negative real interest rates and the inflation protection that properties offer during periods of high inflation rates are also discussed in the report in relation to the increase in rents.

Compared to the stock and bond markets, the German housing market is seen as less risky and more secure. Even though prices have been declining, they have not dropped as drastically as other markets. In the years to come, institutional investors are predicted to find the housing market more appealing than the bond market.

In the first quarter, the authors foresee a 2% decline in price followed by a small recovery. They propose that this recovery may be prompted by the ECB taking a more wary approach to communicating about potential interest rate hikes and continuing to cautiously decrease bond purchases.

Burdening the real estate market, another interest rate shock could present a risk scenario if there continues to be high inflation. In such a case, property prices could come under pressure again. However, it is noted that in this scenario, almost all capital investments could suffer losses, and investments in the German housing market may still fare relatively well compared to other asset classes.

Source: Deutsche Bank report as PDF

Conclusively, the Deutsche Bank, which combines a lot of talent in the real estate market, says that the German real estate market's sole risk lies in further rate hikes. This was the most significant risk all along, but I would say that other risks, or better said the questions and uncertainties regarding the real estate market in general have subsided.

Consequently to this report, Deutsche Bank recently issued a new buying recommendation for Vonovia and a more optimistic evaluation of TAG Immobilien ( OTCPK:TAGOF ), ( OTCPK:TAGYY ), revitalizing both real estate stocks on Tuesday. Despite a largely unchanged Dax, Vonovia was among the biggest winners with an increase of 1.6 percent, while TAG Immobilien in the MDax index reported a modest price increase of 0.5 percent.

Thomas Rothäusler of Deutsche Bank believes that the German residential real estate market has reached its bottom. In a sector study, the analyst noted, "We are becoming more positive about German residential real estate." Consequently, Rothäusler upgraded Vonovia's shares to "Buy" and TAG Immobilien papers from "Sell" to "Hold."

He estimates that residential property prices in Germany will likely not fall more than 20 percent from their peak to their trough. In this scenario, the companies should weather the downturn without capital measures. Even though strengthening the capital stock is one of the most urgent tasks for the companies, he expects this process to proceed in an "orderly" manner. Market discounts of up to 35 percent are considered exaggerated, and "Vonovia still has the highest discounts," the analyst added.

Rothäusler's purchase vote aligns him with a long list of optimists: Of the 21 experts who evaluate Vonovia's share according to Bloomberg, 16 recommend buying and only 3 advise selling. A significant reason for the optimism of many experts might be the enormous price losses the sector has suffered since late summer 2021. For example, Vonovia lost about two-thirds of its value from the end of August 2021 to the end of March this year. The rapidly and sharply rising capital market interest rates heavily burdened the industry. TAG Immobilien shares even lost around 80 percent from August 2021 to March 2023.

Rate hikes are still the biggest danger for the real estate market.

In my last article, I argued that I see a stop of rate hikes and maybe even declines in rates that could come sooner as the market expects. I also said that I don't expect the real estate market to crash as steep as the market expected it to. Both arguments were criticized a lot in the comment. It seems like at this point, investors were mainly pessimistic towards both these things. I think the report from Deutsche Bank shows that it possibly might not be that in the real estate market. Let's see what the "rate situation" looks like.

Current projections are that the European Central Bank ((ECB)) probably raises the rate one more time by 0.25% to an overall 4.25%. After this, I think the rate level probably stays like this for a few months to maybe a year before we could possibly see rate declines. In other words: the worst is over for the real estate market, as long as these projections turn out to be true.

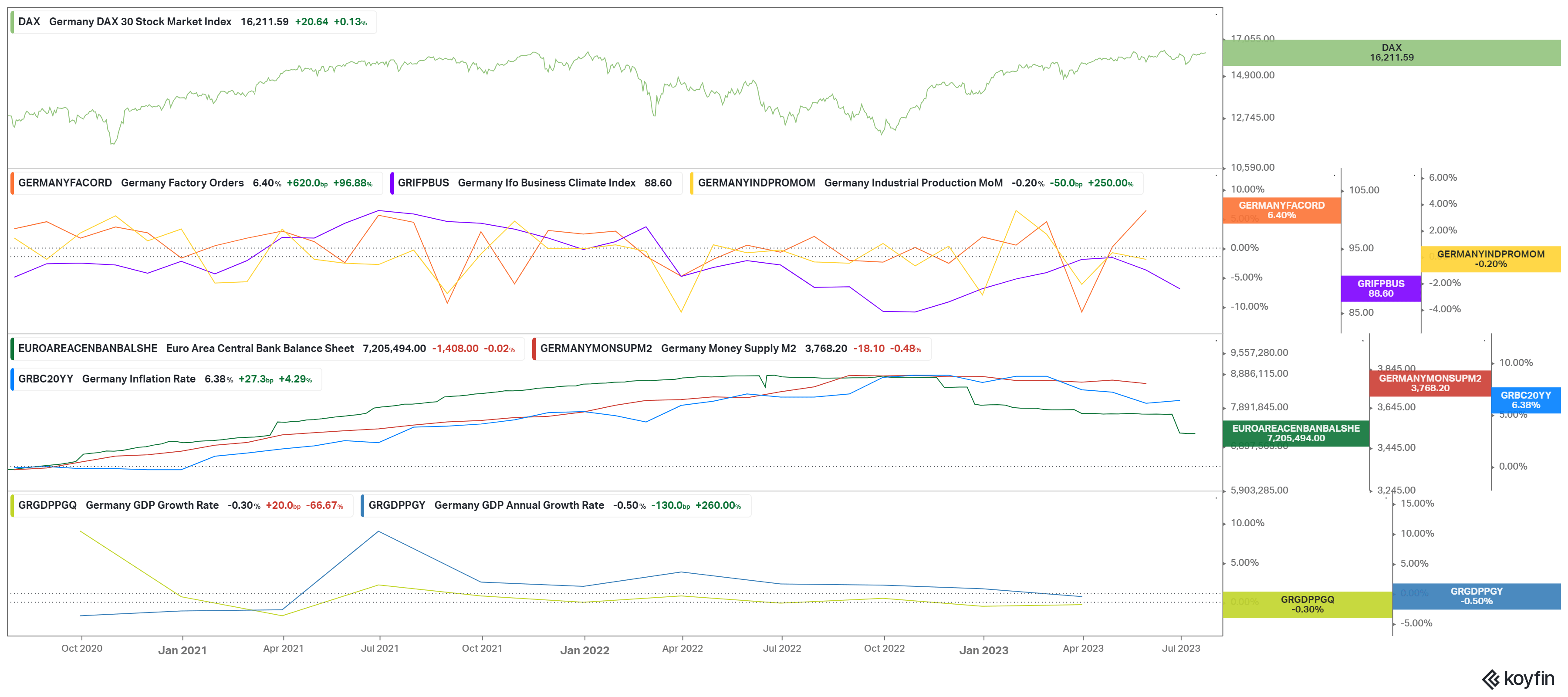

Looking at the current economic development in Germany, I think the ECB does not have the foundation to overcome these projections and raise rates even further. Even though Germany's most significant index, the DAX40 index (the 40 greatest German companies) just made a new all-time high in June and currently is +16.45% YTD, the development of the German economy doesn't look as good.

Germany's economic development (Koyfin.com)

{kind=link}

The chart above shows that even though the DAX40 is at all-time highs, most of the lagging and predicting indicators for the economy's health are looking bad, or at least worse than in the years before. The ifo business climate index is lower than the average of the last few years. Even lower than during the pandemic. The GDP growth rates are significantly lower than the average. Industrial production output is also quite low and significantly declined since the start of the year. Factory orders, one of my favorite indicators are looking good here, but the data isn't actual. More on this in the following.

Just yesterday, some new economic indicators were published and Seeking Alpha reported on it: Germany's Manufacturing PMI drops to 38.8, the steepest deterioration since May 2020

The manufacturing purchasing manager index ((PMI)) "is an index of the prevailing direction of economic trends in the manufacturing and service sectors. It consists of a diffusion index that summarizes whether market conditions are expanding, staying the same, or contracting as viewed by purchasing managers." (Source: Investopedia ). This index dropped to 38.8 from 40.6 while consensus thought it would rise to 41. This marks the steepest pace of deterioration in the manufacturing sector since the aftermath of the COVID pandemic in May 2020. Factory output shrank at the fastest pace for over three years, while new orders contracted further and payroll numbers fell for the first time since January 2021. Furthermore, there are some more indicators that I will just quickly list here:

- Composite PMI: 48.3, down from 50.6 vs. consensus of 50.3.

- Services PMI down to 52 from 54.1 vs. consensus of 53.1.

So what we can see here is a significant slowdown in the economy. While this is the expected consequence of rate hikes, it begs the question if the ECB can risk putting more pressure on Europe's greatest economy.

The only thing that could lead to more rate hikes is the still high and persistent inflation. We got new readings on the Eurozone and German inflation just a few days ago. While German inflation picked up again and increased to 6.4% in June from 6.1% in May , Eurozone inflation, which is more relevant to assess what the ECB might do next, came in at 5.5% down from 6.1% in May . The decline is mainly due to lower energy prices. The core inflation is increased to 5.5% from 5.3% in May, close to its all-time high of 5.77%. Consensus thought it would come in with 5.4%.

So from my view inflation is persistent and even worse than expected, which could be a reason for the ECB to consider more rate hikes.

Risks to my thesis

The biggest risk to this is that rates could be hiked further than expected, making real estate significantly less important and crushing the demand. Real estate prices in Germany could fall as a consequence, pressuring Vonovia to write off some of its portfolios and, in the worst case, trigger credit reassessments by the creditors. As I laid out earlier, I don't think the risk of further rate hikes is pretty big, but it is there. Another potential risk could be a general market sell-off. Most indexes and stocks did pretty well this year so far, and a potential 'pause' on the market could be close. As we all know, stocks never move in one direction for an unlimited amount of time. Every rally is accompanied by sell-offs in between. We could maybe have reached a time at which such a sell-off could occur.

Vonovia's Valuation

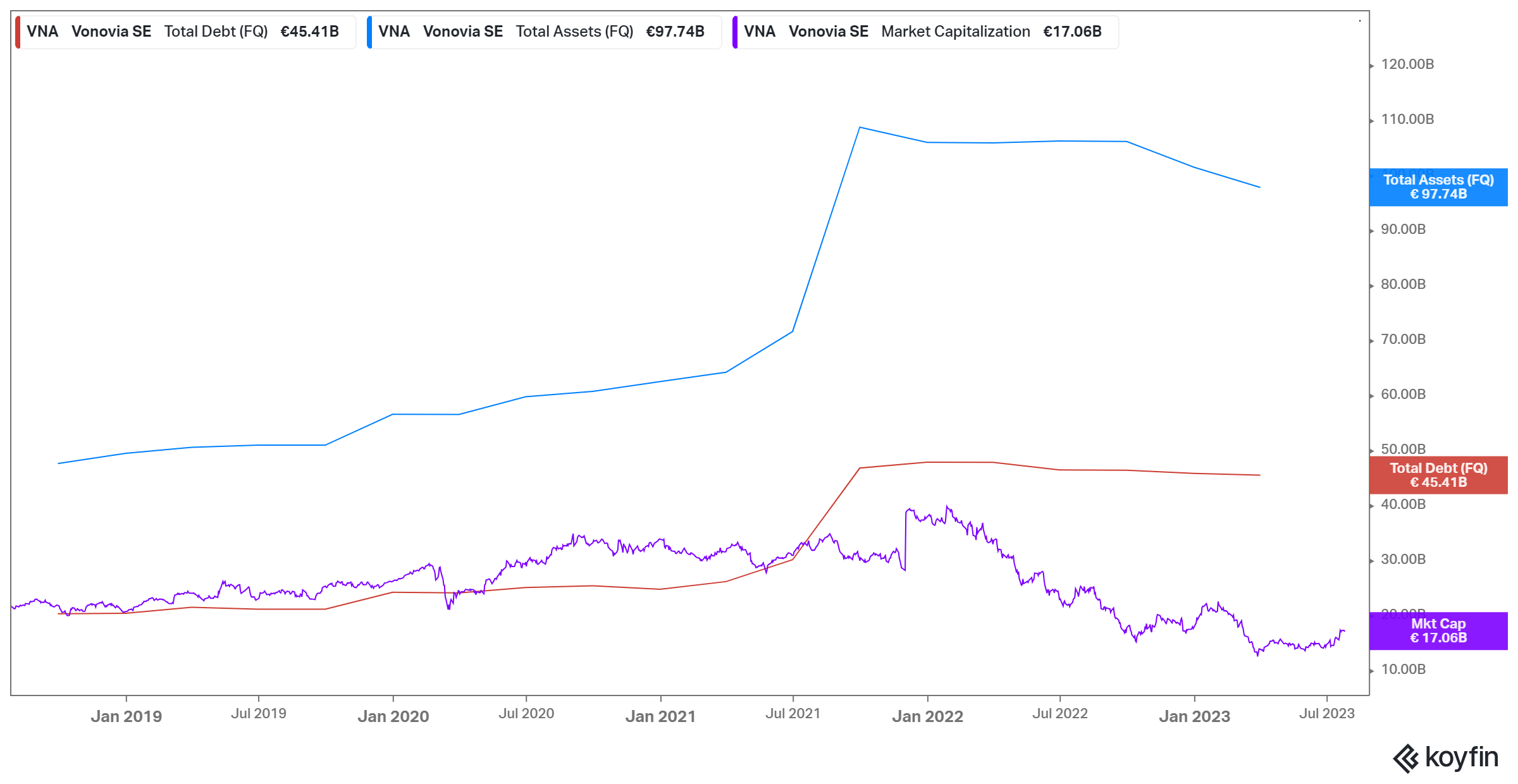

In my last article, I said that total assets are way higher than the current market cap of Vonovia:

A market cap of $19.4B while holding assets worth $99B means you can buy a part of Vonovia's assets by paying 19.6% for it. In other words, Vonovia's current share price offers you a discount of 80.4% on real estate.

This doesn't include the debt Vonovia is currently in, if we take this into effect and use the current market cap, things look like this:

{kind=link}

If we subtract the debt off the assets, we are leaving with 52.33B€ debt-free assets for which we have to pay a market cap of 17.06B€. This means currently, you can buy Vonovia's debt-free real estate portfolio with a discount of 67.4%.

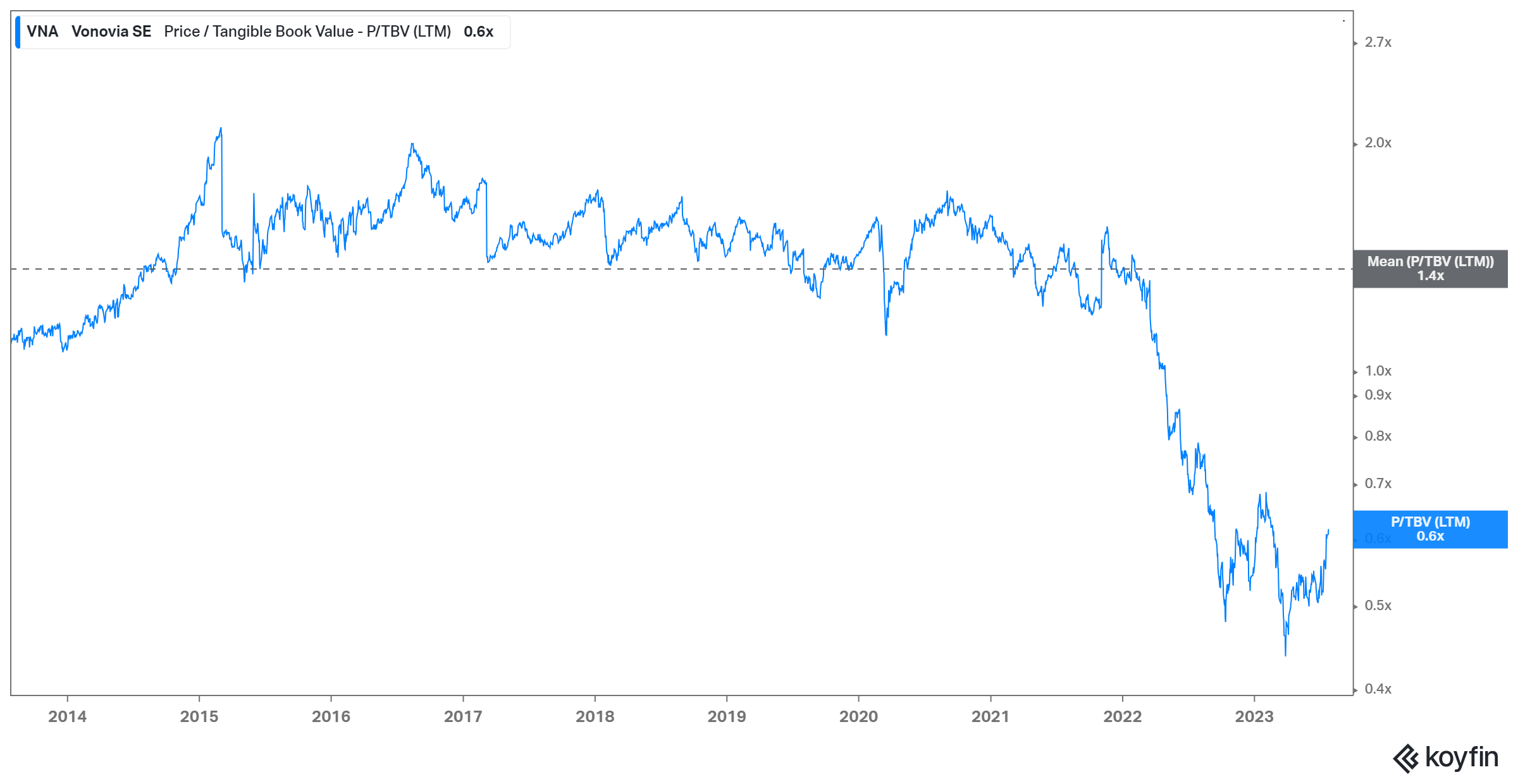

The price to tangible book value is close to its all-time low and way below the 10-year mean. I think this puts the discount Vonovia trades at currently into better perspective.

{kind=link}

Conclusion

If we trust the experts, it is fair to say that the real estate market is in better shape than initially thought and that we might see a bottom soon without the dramatic decline many investors thought of earlier this year. When it comes to rate hikes, there are reasons against further hikes and for further hikes. I, personally, think that we won't see more rate hikes than the projection of one more 0.25% rate hike. The pressure on the economies is already pretty high and cracks are showing. I don't think the ECB would willingly risk the well-being of the economy more than they have to.

What this means for Vonovia is this: I think that even though there has been a good rally in recent weeks, there could be more gains ahead in the long run. Vonovia still pays a nice dividend and still seems highly undervalued (as I explained in my last article). In its newest rating upgrade, Deutsche Bank gave a price target of 25€ which is 18.4% above the current price of 21.11€. The average consensus is even higher with a 12-month price target of 30.37€ which would be a return potential of almost 44%.

Vonovia 12-month average price target (Koyfin.com)

Considering all of this, I still rate Vonovia as a buy.

For further details see:

Vonovia: There Is Still Room For More Gains In The Long Run