VNNVF - Vonovia: Too Early For A Major Investment

Summary

- The Vonovia SE share price has been tumbling from low to low and, just a few weeks ago, was trading as low as it had last been in 2014.

- Nevertheless, the share price has recently recovered significantly, gaining more than 25 percent from its low in December.

- The question many investors are asking, however, is whether this is the beginning of a sustained recovery or just a trap to lure overly impatient investors into the stock.

- While the stock looks tempting, I think it is too early to take a full position, because if the current interest rate environment persists, Vonovia will have problems.

Since August 2021, the Vonovia SE (VONOY) (VNNVF) share price has been tumbling from low to low and, just a few weeks ago, was trading as low as it had last been in 2014.

What had been foreshadowed since the beginning of 2021 has become a certainty: interest rates are rising across the board; the Fed and the ECB have made it clear that they will continue raising interest rates to curb rampant inflation. This makes borrowed capital more expensive for Vonovia. This hits a key pillar of Vonovia's growth strategy, as the company has largely grown inorganically and has acquired more and more properties through takeovers.

Nevertheless, the share price has recently recovered significantly, gaining more than 25 percent from its low in December. The question many investors are asking, however, is whether this is the beginning of a sustained recovery or just a trap to lure overly impatient investors into the stock. Well, my view is that now is a good time to buy smaller tranches. Yet, I think it is too early to take a full position, because if the current interest rate environment persists, Vonovia will have problems.

Does the debt pile hinder growth?

Vonovia is currently sitting on a mountain of debt. Measured against the interest-bearing debt of more than 46 billion euros, the debt ratio is over 40 percent. The takeover of Deutsche Wohnen alone cost 17 billion euros . In order to operate sustainably, Vonovia is dependent on the return on its own properties being higher than its interest expenses. However, the high debt ratio lowers Vonovia's credit rating, which in turn makes taking on new debt, for example, to pay off old debts, even more expensive. This was also a reason for the credit rating downgrade by Moody's. It, therefore, becomes problematic when, on the one hand, interest rates rise and, on the other, rents fall and put pressure on rental yields.

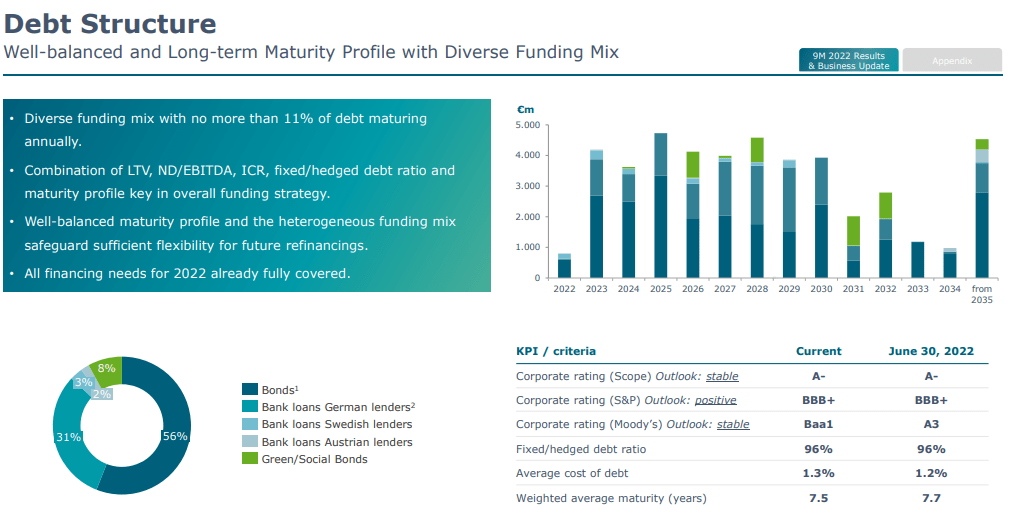

The fact that Vonovia has organized its own liabilities conservatively is a source of optimism. As a result, no more than 11 percent of the outstanding debt is due in any one year. Nevertheless, the next few years will remain challenging, as Vonovia has to repay an average of four billion euros per year to creditors by 2031.

{kind=link}

But 4 billion euros per year is also a lot of money. Unfortunately, even sales in the first nine months of 2022 amounted to just €4.6 billion, while FFO was €1.5 billion. In order to repay its debts, Vonovia is dependent on generating capital through new debt or the sale of residential units from its portfolio. The management has therefore already announced its intention to dispose of 66,000 flats and raise around 13 billion euros through the sale. CEO Buch cited the reduction of debt as the reason for this step. Vonovia is thus carrying out a strategic change. Bold takeovers such as the recent one at Deutsche Wohnen are a thing of the past.

Vonovia's capital allocation preferences (Vonovia investor relations)

As a result, Vonovia must now change course and focus on reducing its debt. But that's also challenging, as the next paragraph will show.

Does Vonovia have to write down the value of its real estate portfolio?

However, there is also the risk that Vonovia will have to sell these properties for less money than the Group would actually like. On the one hand, the management is under time pressure, which potential buyers can leverage in order to push down the prices for the properties. And indeed, while high energy prices in Germany affect 89 percent of all properties held by Vonovia, a potential buyer will discount the future cash flows through rents rather generously. In this regard, an interest rate increase of 0.25 percentage points already leads to a decline in the value of the properties of 8.7 percent . Vonovia is therefore not only under pressure to move, but may also have to sell during a falling market. The management appeases worried investors with two arguments. Firstly, it sets the market values of its own properties far below the market price. This ensures that there is still some room for manoeuvre in the valuation of the properties and that not every fall in prices is reflected in Vonovia's balance sheet. Secondly, Vonovia assumes that residential property prices will not fall due to the low vacancy rate. In the past, there have only been substantial price declines for flats when vacancy rates were high. Currently, however, vacancy rates are extremely low. At Vonovia, the most recent vacancy rate was just 2.1 percent. The management is therefore also trying to calm the fears of investors. According to a DPA report , Vonovia's CEO stated:

"The vacancy rate in cities is low. I have rarely seen prices fall when demand is higher than supply ... Of course, we won't see the value increases of recent years any time soon, but values will remain largely stable"

It plays into Vonovia's favor that the construction of new flats in Germany in recent years did not reach the politically set target. Increased costs and the shortage of raw materials also make it unlikely that significant new supply will flow onto the market in the future and take pressure off prices. In addition, warnings of a bursting real estate bubble have been issued for years without such a burst occurs.

How the market sees it

Some investors, unlike the management, expect more significant price declines. Moody's is even pricing in a 10 percent drop in property prices by the end of 2023. The analysts at the rating agency Moody's doubt that Vonovia will be able to sell the planned properties without higher price markdowns:

Given the current marginal cost of funding and a rising trend of interest rates, property value declines in Germany are inevitable in our view. […] We cannot forecast particular value declines, but we have included 10% value declines in our assumptions until year-end 2023. […]

At the same time, in today's market environment, we believe that substantial disposal volumes will be difficult to achieve without more material discounts. We have assumed a total of EUR 3-4 billion proceeds from disposals, individual unit sales or other types of exposure reductions until end of 2023 in our projections

The market also has doubts about the management's optimism. It is uncertain whether vacancy rates will really remain so low. In particular, demographic change, a possible urban exodus, and more dynamic residential construction could quickly cause vacancy rates to rise again. However, the huge mountain of debt surely causes the most stomachache.

How I see it

Well, here is my view. Vonovia expects strong growth for the current fiscal year. FFO is expected to rise from 1.7 billion euros to over 2 billion euros. However, the decline in investments from 1.4 billion in 2021 to around 800 to 900 billion euros already shows that the company is putting on the brakes due to the increased prices for building materials. From the 2023 fiscal year onwards, the management's forecasts will deteriorate further. Although Vonovia expects higher rental income, FFO is expected to be lower than in 2022. The management cites unfavorable tax and interest rate developments as the reason for this, although Vonovia does not elaborate on the reasons for the unfavorable tax development.

Forecast (Vonovia investor relations)

As a result, the effects of the turnaround in interest rates outlined above are gradually having an impact on capital-hungry companies such as Vonovia and are increasingly leaving their mark on business forecasts. In view of this environment, it cannot be ruled out that FFO will continue to fall in the years after 2023 if interest rates remain dynamic. On the other hand, the synergies from the takeover of Deutsche Wohnen could provide some relief. Vonovia puts the potential of synergy effects at around €135 million per year from 2025 onwards. However, this does not change the fact that organic growth is likely to be limited in the coming years.

From a fundamental point of view, Vonovia's low fundamental valuation is the main argument for a buy at present. Vonovia is clearly undervalued compared to the past ten years' historical multiples. The price/FFO ratio of the last 10 years is 18.8, while it is currently 10.4. The current Price/AFFO of 10.8 is also far below the historical multiple of 23. But this is the back mirror. In my view, the current interest rate environment and the possibility of a continued tight interest rate policy justify a significant discount to the historical multiples. Therefore, I have decided to adjust the average fair values of FFO and AFFO to 9.0. Based on this adjustment of the valuation ratios, the Vonovia share is actually overvalued. By the end of the 2023 fiscal year, with a view to the AFFO of 2.34 euros per share expected by analysts, there is a downside potential to the current share price (around 25 euros) of almost 20 percent.

What's left? Sure, the dividend. Overall, Vonovia has a dividend yield of just under 6.5 percent, which is well above the historical corridors and therefore suggests an undervaluation. However, analysts do not expect dividend increases in the next few years for the time being. In fact, the air is getting thin, as Vonovia already distributed more than 78 percent of FFO to shareholders in the form of dividends in the last fiscal year. In view of falling profits in the coming year, I also consider generous dividend increases as in recent years to be unlikely. Whether there will also be dividend cuts will depend on how quickly the interest rate spiral turns and how well management manages to reduce debt without weakening its own property portfolio.

Conclusion: what does it need?

The Vonovia stock has been one of the basic investments in the real estate sector in recent years and is also in my portfolio . The share would be an absolute dream investment at the current prices and the current dividend yield. But now the wind has changed, which poses some challenges for the management. At least in the medium term, priorities are shifting away from growth and the market is reflecting this in the share price.

A calming of the current inflation and interest rate trend is therefore crucial for a repeat purchase. Should inflation rates fall substantially again, for example, due to falling energy prices and high base effects, a trend reversal in the real estate sector could quickly occur as interest rates fall. Currently, this seems to be exactly the case. That was one reason why I invested in a new tranche in December. I remain committed to Vonovia with my highly diversified portfolio, and I am keeping an eye on the company. For investors who expect inflationary and interest rate pressures to ease, Vonovia is a clear buy. All other investors should stay on the sidelines.

For further details see:

Vonovia: Too Early For A Major Investment