VONOY - Vonovia Trades At Less Than Its Land Value - Strong Buy

Summary

- Vonovia has become extremely oversold in the current market environment, creating an asymmetric risk/reward opportunity.

- The company is highly leveraged and might need to sell some properties to pay down unsecured debt in 2023 and 2024, but management is dealing with the issue.

- In the meantime, the valuation has become much too cheap to ignore, trading at a discount to NAV of 67% and at less than the value of its land.

- Investing in Vonovia is essentially like buying an apartment at USD97 per square foot.

Editor's note: Seeking Alpha is proud to welcome David Ksir as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Vonovia ( VONOY ) is a gigantic German apartment landlord. Although the company operates similarly to the way a REIT would (its sole activity is developing, owning, and leasing real estate), technically it is not a REIT. This can be important for some investors, especially when considering taxes, as dividends from REITs are taxed differently in some jurisdictions. But given that the operational nature of the company is quite similar to a standard REIT, I believe it's appropriate to use metrics that would normally be used to analyze REITs (such as FFO, NAV, etc.). This will give you a better understanding of the underlying business of the company, and make for better comparisons with its peers.

The company reached valuation levels that are simply too good to ignore, hence deserving a strong buy rating here. The company currently trades at a steep discount when compared to:

- its net asset value, which is already quite conservative compared to market values for comparable real estate,

- its historical price to FFO multiple, and

- the multiple of apartment REITs in the U.S.

I believe the potential upside largely outweighs the risks (which mostly have to do with the ability to refinance/repay debt) at this price level, making Vonovia a good asymmetric risk/reward opportunity for investors. My thinking is that if/when the management announces significant progress on a partial disposal of their portfolio to pay down debt due in 2023 and 2024, the stock price will surge.

Moreover, with a potential recession on the horizon, I believe the company is a good "recession buy" or a hedge. The reason is that should a recession happen, the ECB will likely be forced to cut interest rates, which should have a major positive effect on the company and its stock price.

How I like to evaluate companies

My background in real estate private equity and real estate development allows me to view investments in REITs - and real estate investments in general - through a slightly different lens. Many analysts focus mostly on the dividend yield and its safety, and the relative valuation of a stock usually based on the price-to-funds-from-operations (P/FFO) multiple relative to its historical average. Don't get me wrong, I too love Fast Graphs and believe it's a great tool to quickly analyze the valuation of a company - I use it in all of my analyses. But I also like to look two other parameters - discount to NAV (preferably adjusted NAV) and debt (in particular FFO/net debt and interest expense/FFO), which I believe are equally important in determining long-term success.

The reason is simple: We've just gone through one of the fastest growth periods for real estate ever, and as the cycle turns and the new one starts (which I believe is happening), past multiples could be skewed to the upside - especially the nearer term ones (say three to five years). Making sure we buy under the current NAV essentially creates a margin of safety, should the downtrend continue. It also allows us to compare the price we are paying to real life examples in a particular city to get a better feel for the price.

The basics

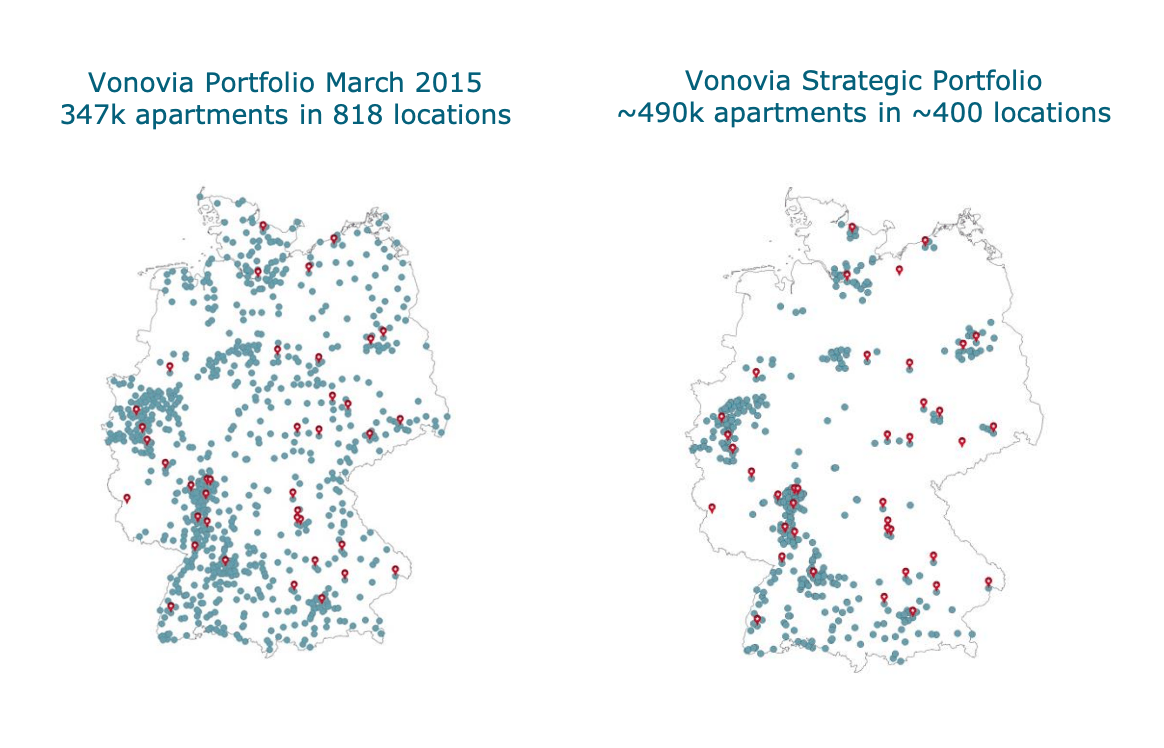

Vonovia is giant apartment landlord headquartered in Germany that holds more than 550,000 apartments. Yes, you read that right. They have a market cap of about EUR100 billion (USD109 billion), which makes them one of the largest holders of real estate in Europe and worldwide. Vonovia's portfolio is well diversified across most of Germany's main urban centers, as well as in Sweden and Austria. Over the past few years, management has successfully shifted away from more rural locations toward locations that are expected to grow.

Vonovia Investor Presentation Q3 2022

{kind=link}

Operations

Management stated in their Q3 2022 investor presentation that "the portfolio's operational performance is in line pre-crisis expectations." Notably, key operational metrics have improved throughout 2022. As of Q3 2022, Vonovia had a record low vacancy of 2.1% (down from 2.7% a year prior) and a solid organic rent growth of 3.3% (slightly down from 3.5% a year prior).

In low inflationary times, annual organic growth of 3% was all right. What is potentially worrying now is that Vonovia might not be able to raise rents fast enough to keep up with inflation - that is, if inflation persists. The reason is that Germany is a heavily regulated market. The regulation requires each city to publish a "fair rent" called Mietspiegel, which is calculated for comparable apartments over the last six years. Understandably, this regulated rent follows market rents, but with a lag. And in times of high market rent growth, it can start to lag significantly. Eventually it will catch up, but it can make the following few years difficult for the company.

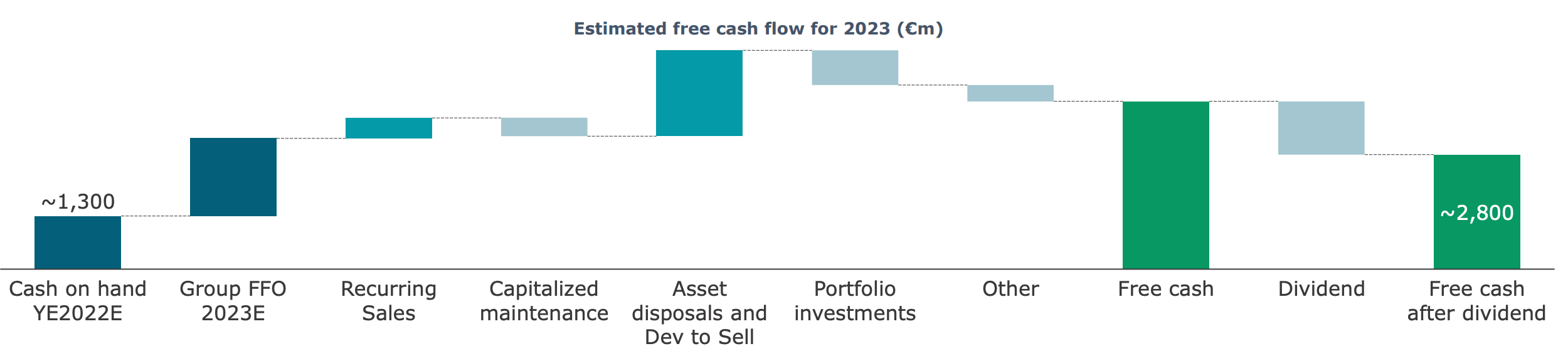

As far as guidance is concerned, management is confident that 2023 will be a cash flow positive year. They expect EUR2.8 billion (USD3.0 billion) of free cash before any proceed from planned disposals - this comes from cash on hand of EUR1.3 billion (USD1.4 bilion) and EUR1.5 billion (USD1.6 billion) of expected free cash flow from operations. This is good news, because it means that dividends that total around EUR1.2 billion (USD1.3 billion) should be safe in 2023, especially as the company has announced that it will reduce investments to a minimum given the increased return hurdles (i.e., higher rates) to preserve cash. Of course, this ignores the fact that Vonovia has a significant junk of debt due over the next two years.

Balance sheet

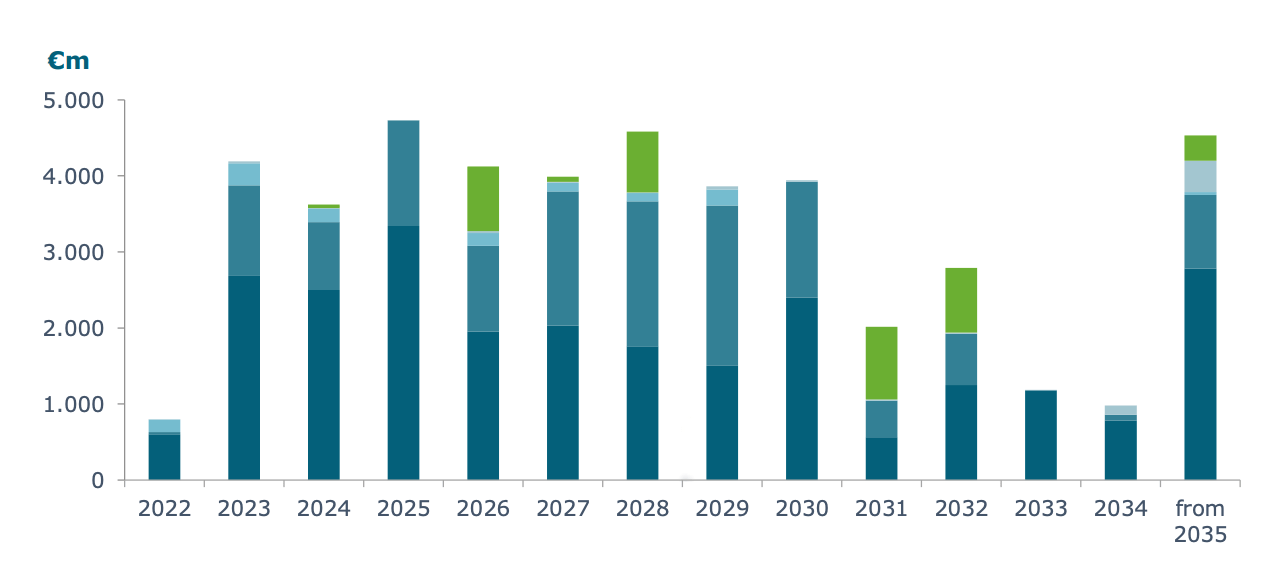

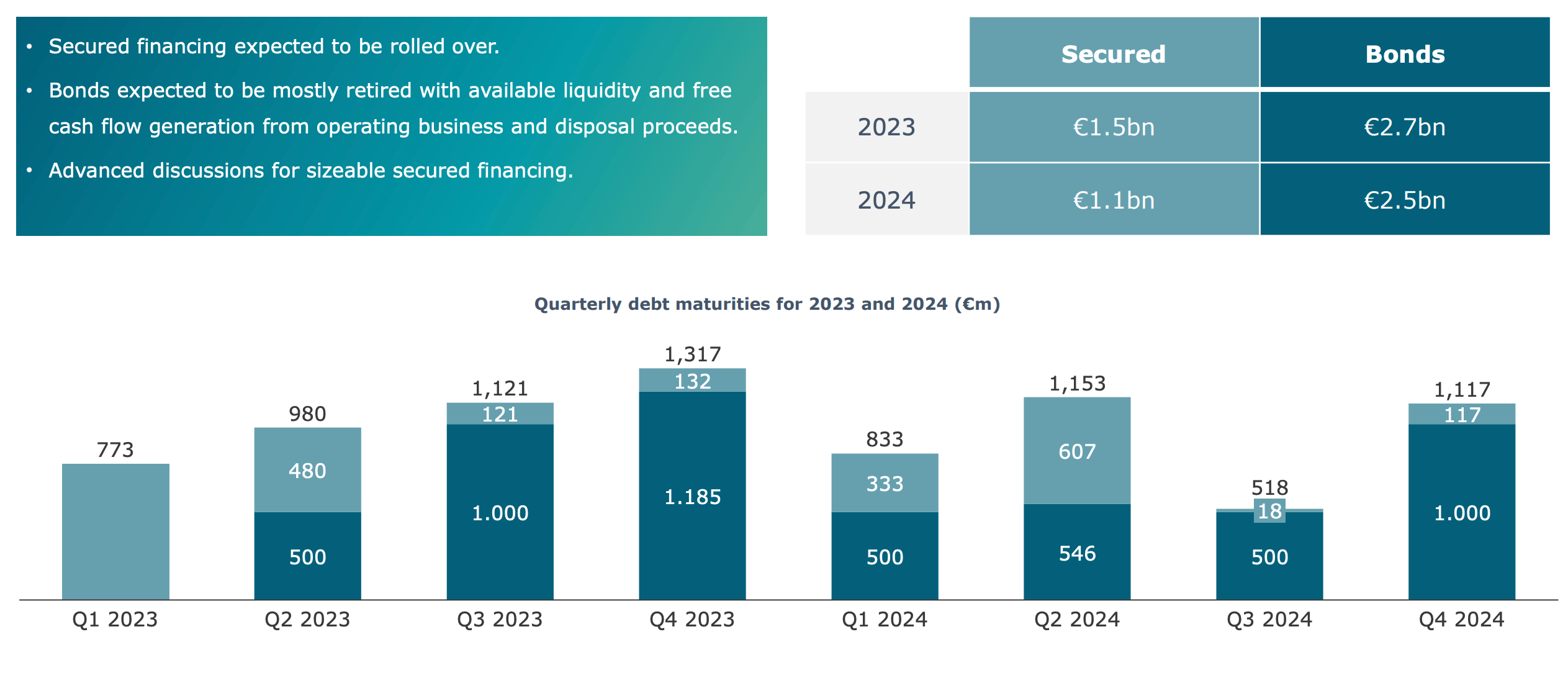

The stock has taken a hit for basically one reason - a high level of debt, some of which is due relatively soon. Let's be honest, the company has a lot of debt: EUR45 billion (USD49 billion) to be exact. This represents an LTV of 45% and net debt/EBITDA of 15.4x. The debt is spread over time, but there are large parts of it due in 2023 and 2024, which understandably makes the market nervous.

Vonovia investor presentation Q3 2022

{kind=link}

A closer look actually makes things worse, because the majority of debt due over the next two years is unsecured debt (i.e., bonds), which is not expected to be rolled over.

Vonovia Investor Presentation Q3 2022

{kind=link}

There is no way the company can repay all of this from cash available and cash from operations, so they are left with only two options:

- refinance part of the debt at a significantly higher rate, or

- sell part of their portfolio to pay down the debt.

Management made it clear during their Q3 earnings call that they're planning to sell at least EUR1.5 billion (USD1.6 billion) worth of assets in 2023, but hasn't announced any progress to date. With relatively low book values (as discussed below) I believe they will be able to achieve this target, and when they do, the announcement will likely cause a surge in stock price.

Below is management's plan to increase their cash position through 2023, mainly through reduced investments and disposals so that they can later use this cash to repay their debt.

Vonovia Investor Presentation Q3 2022

{kind=link}

Also, a recession could potentially be bullish for the stock as it will force the ECB to drop interest rates, making Vonovia a solid hedge or recession play.

Asset value on books

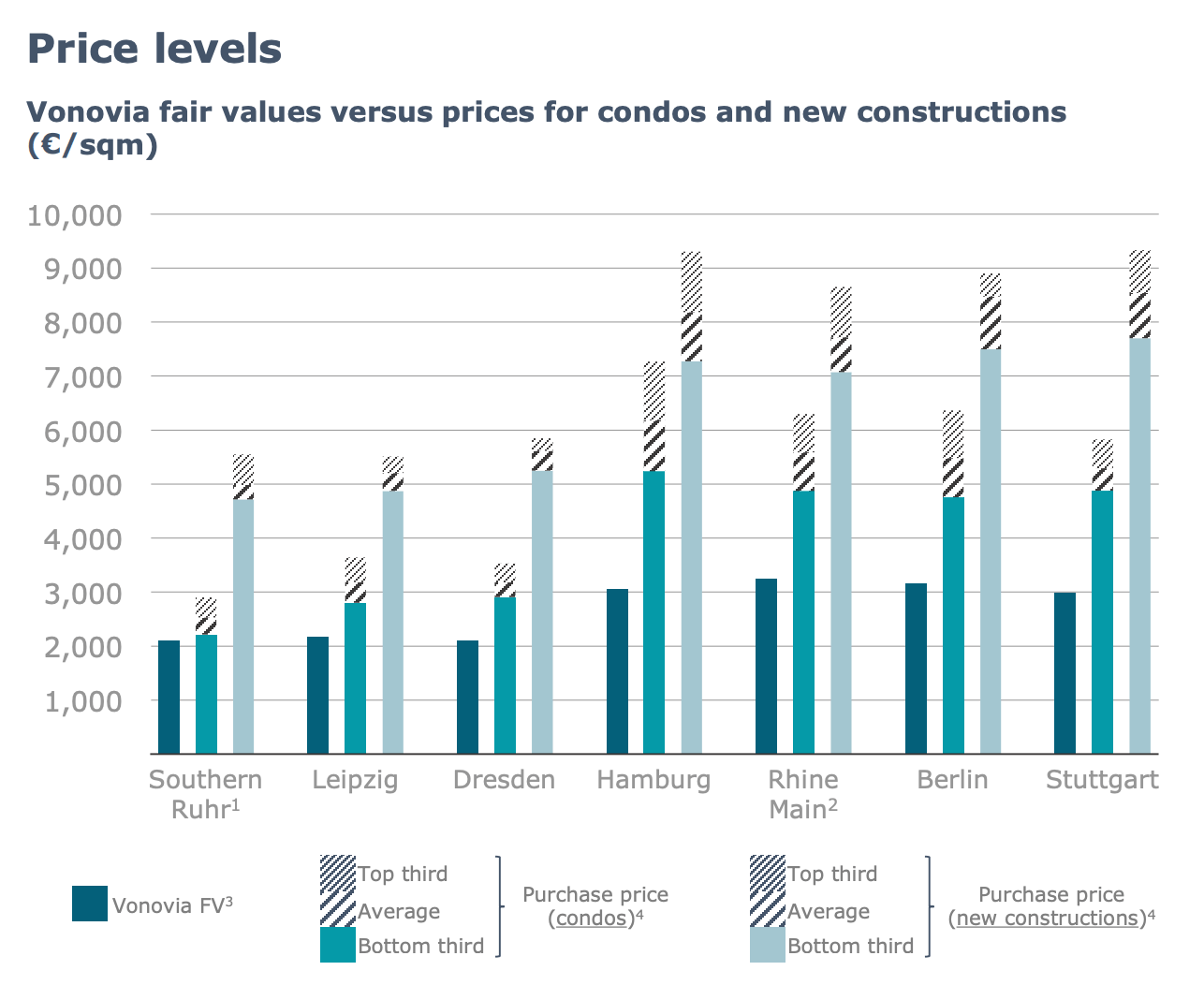

Vonovia's units are reported at a book value of roughly EUR93 billion (USD101 billion), which translates to a 170,000 EUR (185,0000 USD) per unit or 2,600 EUR (2,800 USD) per square meter of residential space (average size of a unit according to their presentation is 63 square meters - roughly 600 square feet). These are by no means exaggerated numbers, and while it's true that most of Vonovia's buildings are not brand new, there is a considerable buffer in the value reported. This will be especially important if Vonovia wants/needs to sell part of their portfolio, as the disposal will likely be done at values equal to or higher than the book value. Below is a comparison of book values vs. market values for multiple markets in Germany.

Vonovia Investor Presentation Q3 2022

{kind=link}

Valuation/net asset value

So, this brings us to valuation. Remember that Vonovia's business is no different from you buying a rental unit with a mortgage, so let's treat the valuation that way.

With a book value of EUR100 billion (in addition to units, they also hold EUR7 billion of developable land) and debt of EUR45 billion, we get NAV of EUR65 billion (USD71 billion). At the current price of EUR26.00, Vonovia has a market cap of EUR21 billion (USD23 billion). This means that the shares are trading at a 67% discount to NAV.

This also means that if you buy Vonovia today, you are essentially buying a 63-square-meter (600 square-foot) apartment in a major German city for EUR56,000 (61,000 USD) or EUR890 per square meter (USD97 per square foot). This is extremely cheap and represents at least 3x-4x the average market level of about EUR3,000 (USD3,300) per square meter (see chart above). Sure, the company is in trouble, but management is acutely aware of this issue and has presented a plan to deal with it going forward. I'd argue that the risk has been more than priced in and it absolutely makes sense to buy Vonovia here.

Fast Graphs paints a very similar picture. The stock is currently trading at just 11x FFO compared to a long-term average of 27x, representing a solid upside if things normalize. In particular with rents and consequently FFO expected to grow between 5% and 7% until 2025, it's realistic to expect an FFO of EUR1.49 per share by 2025. Using the average historical multiple, we get to a price target of roughly EUR40.00 (USD43.60).

At this level the company would still trade at a discount to its NAV - in particular, at EUR40.00 the market cap would be EUR32 billion (there are 800 million shares outstanding). Assuming an unchanged NAV of EUR65 billion, you can see that the stock would still trade at just half its assets.

By now you're hopefully starting to see that Vonovia is a great asymmetric risk/reward opportunity. To be clear, I am not calling a bottom here - we could certainly revisit the bottom near EUR20.00 per share - but with the company already trading at a steep discount to the value of assets it holds, I'd argue that any positive news we get, especially related to the disposals, will shoot the stock price up.

{kind=link}

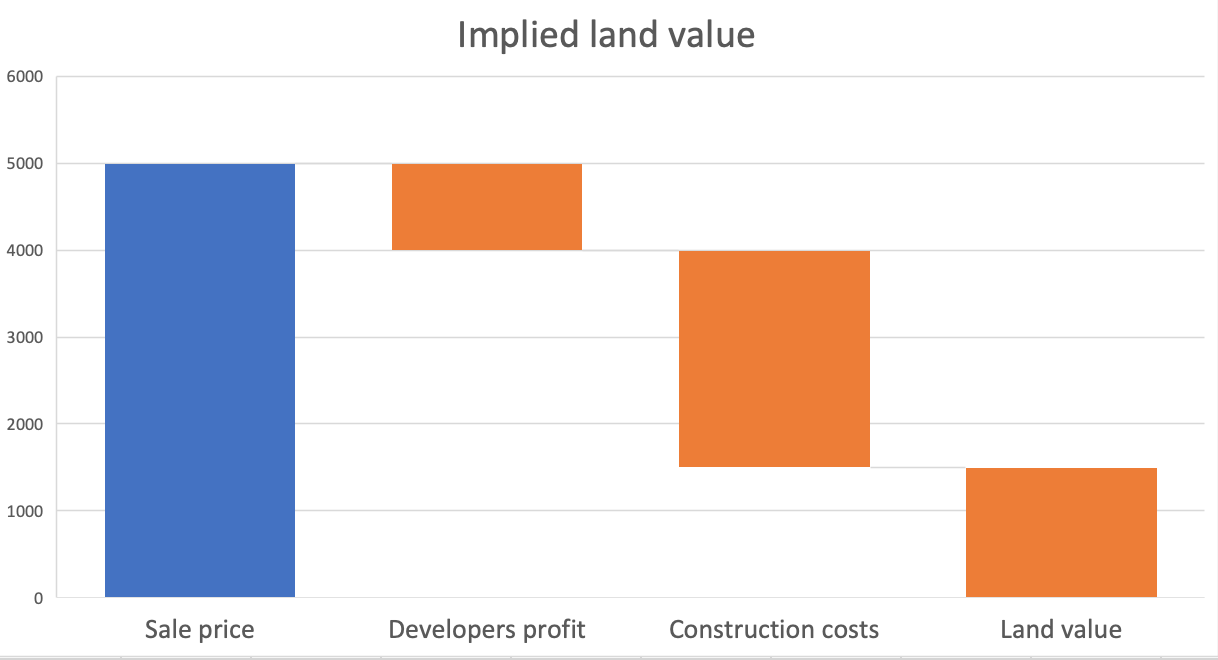

Now, if this isn't convincing enough, let me go through an example using my real estate development background and benchmarks from Vonovia's presentation to illustrate that you are not just buying the apartments at a discount, you are buying them for cheaper than the price of the land alone.

Let's assume that a newly constructed condo sells for EUR5,000/square meter (USD550/square foot), the developer has a margin of 20%, and construction costs (soft costs plus hard costs) are EUR2,500/square meter (USD270/square foot). So we get an implied land value of about EUR1,500/square meter (see chart below).

This means that for each square meter of residential space that Vonovia holds, the land alone is valued at EUR1,500.

Immediately we see two things:

- Vonovia keeps the properties on their books for 2,600 EUR/square meter, but it costs 4,000 EUR/square meter to build new ones (land value plus construction costs). This reiterates that the value on the books is conservative.

- At EUR26.00 per share we are paying 890 EUR/square meter, but the land alone is worth 1,500 EUR. That's almost double what we are paying. So the price you pay today is less than the value of the land alone.

Created by Author using data from Vonovia and adjusted based on his Real Estate background

{kind=link}

Risks

Don't get me wrong, there are risks here. In particular, management might not be able to dispose of part of the portfolio to repay the debt in time. Frankly, they have made little progress on this since October, with no major announcement regarding the disposal. Given the relative low book value of properties and an experienced management team, I am willing to give them the benefit of the doubt here. But this is definitely something to watch.

Additionally, as with REITs in the U.S. - and especially residential ones - a prolonged period of high inflation or a significant, prolonged increase of rates by the ECB would put the company in a difficult situation, as rents would likely not increase fast enough (due to regulation) to offset the increased level of debt service. This could seriously jeopardize the dividend and likely force the company to dispose of a larger part of their portfolio, which could prove especially difficult under those macro conditions. My view is that central banks will succeed in fighting inflation, but again this scenario is something to watch for the short to medium term.

Verdict

All that said, I rate Vonovia a strong buy with a price target of EUR40.00 (USD43.60) . Simply from a valuation standpoint, I believe the market has priced in a severe (almost apocalyptic) decrease in the German property market or a complete failure of management to execute. Trading at under 1,000 EUR per square meter of residential space means that the market could fall 66% from the current average market price of 3,000 EUR per square meter, which would undoubtedly be unprecedented. I believe that any positive news will catapult the price up, especially if management succeeds at achieving their target of selling EUR1.5 billion of assets.

Moreover, I believe this can be a good "recession play" as the ECB would likely decrease interest rates during a recession, which would benefit the stock immensely. Adding Vonovia to your portfolio can therefore act as a hedge in case of a recession, while providing a solid dividend yield and upside when things normalize.

For further details see:

Vonovia Trades At Less Than Its Land Value - Strong Buy