VNNVF - Vonovia: Why The Bears Are Wrong

2023-05-13 06:42:06 ET

Summary

- Vonovia is trading at a distressed valuation of ~0.35x book value.

- The bear case is premised on a dilutive equity issuance and/or forced fire sale.

- The risk of above is remote in my view.

- Recent disposal transactions largely reduced the tail risks.

- This is a generational buy opportunity.

Vonovia SE (VONOY) (VNNVF) is one of my top conviction buys for 2023. It is currently trading at ~0.35x its book value which is certainly a distressed valuation for a German residential property company.

I also believe that this company is not very well understood and hence this is a generational opportunity for investors with a medium-term outlook.

In this article, I intend to unpack the bear case and explain why the bear narrative is wrong.

The Bear Case Explained

For a good summary of the bear case, I recommend that you read the following article from my SA colleague.

The key bear points are:

- Vonovia's portfolio has a net yield of 2.7% which is significantly below its cost of funds and is not sustainable against its marginal cost of debt (current bond pricing of ~5% to 6%)

- It is only a matter of time before Vonovia either raise equity or is forced to sell properties in a fire sale

- Vonovia is likely to breach its debt covenants due to the above points

- There are material red flags relating to the recently announced disposal transactions

- The FFO per share has already fallen by 20% which has proven the bear thesis even though Vonovia's cost of debt will continue to rise and is not factored in the current FFO metric

- The FMV of the portfolio will continue to decline precipitously in the next few quarters which will put upwards pressure on the LTV and other debt covenants

So in summary, even though the current share price equates to only 0.35x book value, the bears argue that more material downside is coming as Vonovia will be forced to raise equity in dilutive prices or engage in a forced fire sale and thus destroy value.

In this article, I will explain why I believe that the bear case is wrong.

The Cost Of Debt Will Only Rise Slowly

The cost of debt is something that the bears focus on as a key reason why the FFO is likely to decline. It only makes sense, right? The portfolio net yield is 2.7% whereas the marginal cost of debt (as measured by the bond market) is somewhere in the range of 5% to 6% currently.

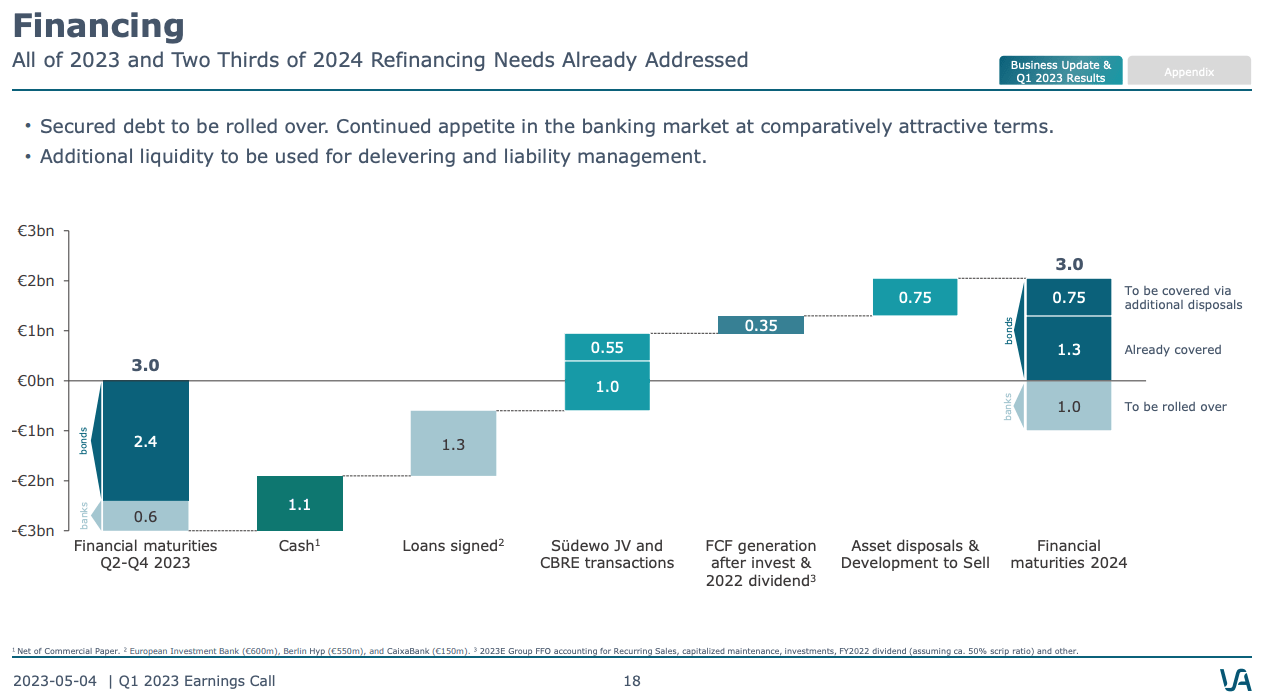

Well, except for a number of items. Firstly, the effective duration of Vonovia's debt is currently 7.2 years. Secondly, alternative financing other than the bond market such as collateralized lending from banks and/or green bonds is much more attractive at 4%. Finally, Vonovia will be retiring all bonds that are due in 2023 and 2024 utilizing cash on hand and disposals. In fact, by Q1 2023, it already covered all the bond maturities for 2023 and three-quarters of maturities for 2024. The below chart from Q1-2023 earnings calls summarizes its debt maturity trajectory:

{kind=link}

As you can see, for the remainder of 2023 Vonovia will only need to refinance an additional 600m as 1.3 billion has already been signed (and some of it is showing in the financials of Q1 already).

For 2024, Vonovia has only 1 billion of loans to be rolled over. Now the annual incremental cost for the loans is ~2.5%, so therefore for every 1 billion of loans refinanced, there will be an incremental 25 million annual interest cost.

At the same time, assuming rental growth (overall not like-for-like organic growth) at approximately 2% (which I believe is conservative), the top-line growth should be in the range of 70 million. This already played out in the rental segment where the adjusted EBITDA in Q1-2023 has grown by ~30 million year on year (or a positive 5.6%), driven by 2.6% overall rental growth as well as cost synergies.

How About The 20% Decline In FFO In Q1 2023?

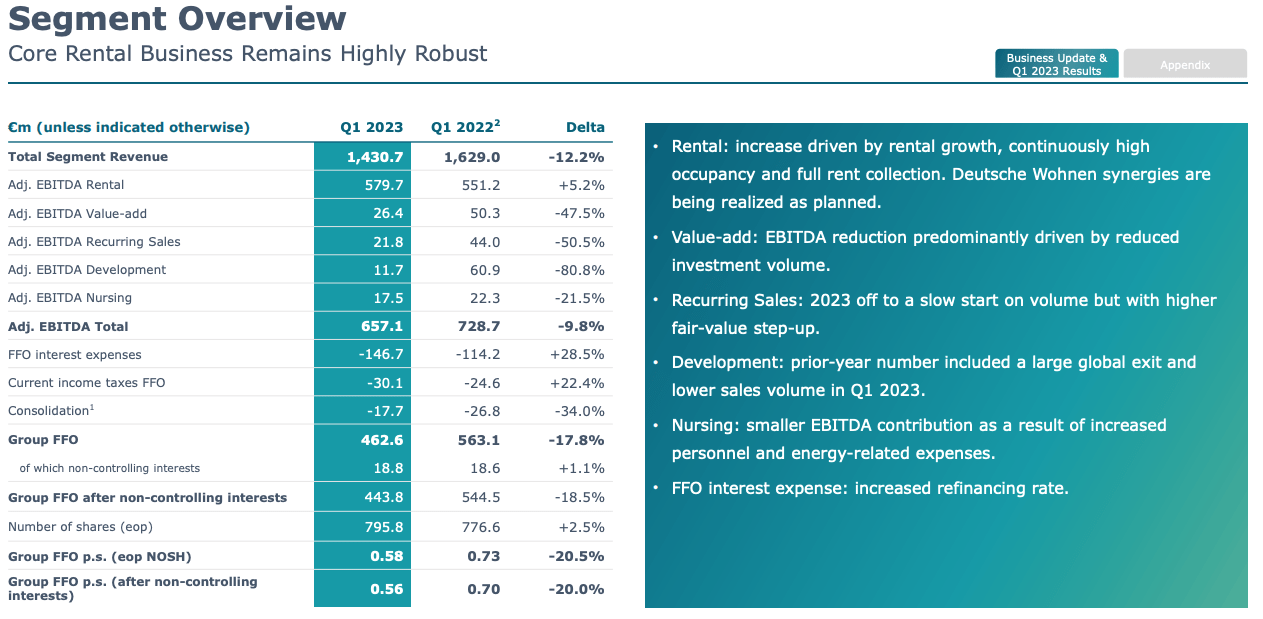

It is true that the FFO has dropped 20% year on year in Q1 as reflected in the below slide:

{kind=link}

However, it is important to note that the core business of the Rental segment has grown by 5.2% year on year driven by rental growth and cost synergies.

The other segments were clearly pressured in Q1 but temporarily so. For example, the Recurring Sales segment included 60% lower disposals than the prior-year quarter. Similarly, the Development segment lapped a strong Q1 last year that included a large global exit. Interest costs were also higher by ~32 million reflecting the issuance of bonds and liability management exercise undertaken in Q4 2022.

Going forward, however, these headwinds will dissipate once transaction volumes normalize. As noted above, the incremental interest rate cost will also slow down materially given the disposals and retiring of bonds in 2023 and 2024 with cash on hand.

The Large Transactions: Equity, Not Debt!

On April 26, 2023, Vonovia announced the sale of a minority common equity participation in its "Südewo" portfolio to Apollo for €1.0bn. The sale implies a discount below 5% of its fair value as of December 31, 2022.

There were special terms however where:

- Vonovia retains a long-term call option to repurchase the participation at an IRR of 6.95%-8.30% (including dividends received)

- The minority participation includes a higher-than-pro-rata share of the dividend distribution by Südewo (probably in the ratio of ~70/30)

- Vonovia will also pay the maintenance/CAPEX on the portfolio

Some investors saw the "special terms" as red flags implying the actual discount to book value was much higher than the 5% indicated.

In reality, however, this is not a disposal of properties transaction - rather it is effectively raising redeemable equity at an attractive cost of capital of ~6.9% to 8.3% compared to a cost of capital of 12%-13% implied by the current share price. Importantly, the call option has no expiry and thus Vonovia retains the upside in the portfolio. This transaction had no impact on the property valuation in the quarter given that it is a minority equity interest. Note some of the analysts completely misunderstood this transaction and even suggest the discount to book is ~30%.

The disposal of five assets with 1,350 residential units to CBRE Investment Management was an actual disposal and not an equity transaction. The book value of the sold assets was approximately EUR 600m and the agreed purchase price totals around EUR 560m, so a discount to book value of approximately 6% to 7%. This transaction had a read across to the valuation of the Vonovia assets and led to the value reduction of 4.4% in the German portfolio. The unscheduled Q1'2023 valuation was triggered by this transaction and not the Apollo transaction.

The State Of The German Property Market

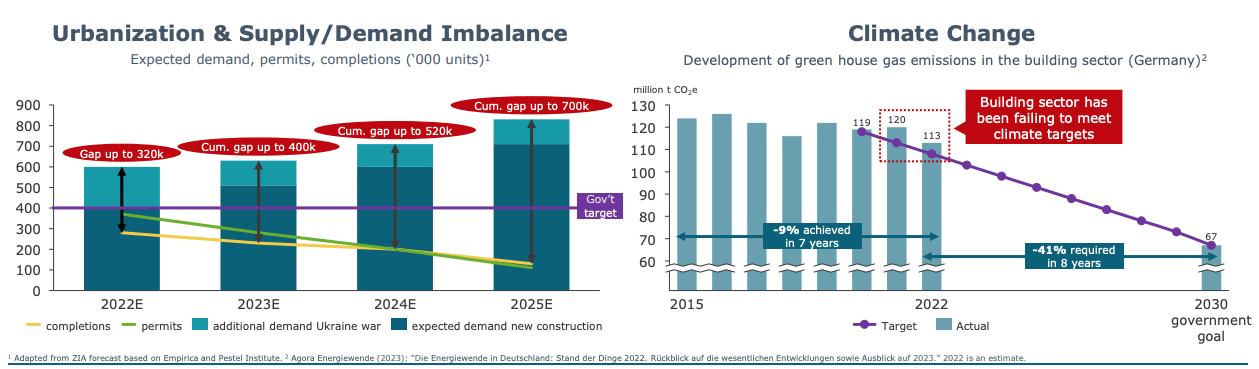

It is important to set the context around the current state of the German property market. The market is essentially frozen and the volume of transactions is historically low, however, the medium and long-term trends are further accelerated given the structural imbalance between demand and supply and the lack of new construction starts.

According to this recent Bloomberg article , the German property market is already stabilizing. This is not surprising as there is a clear supply-demand mismatch and alarmingly (for renters) new construction has effectively ceased due to high construction costs, inflation, and high cost of funds. The projected shortage (as illustrated by Vonovia) is shown below:

{kind=link}

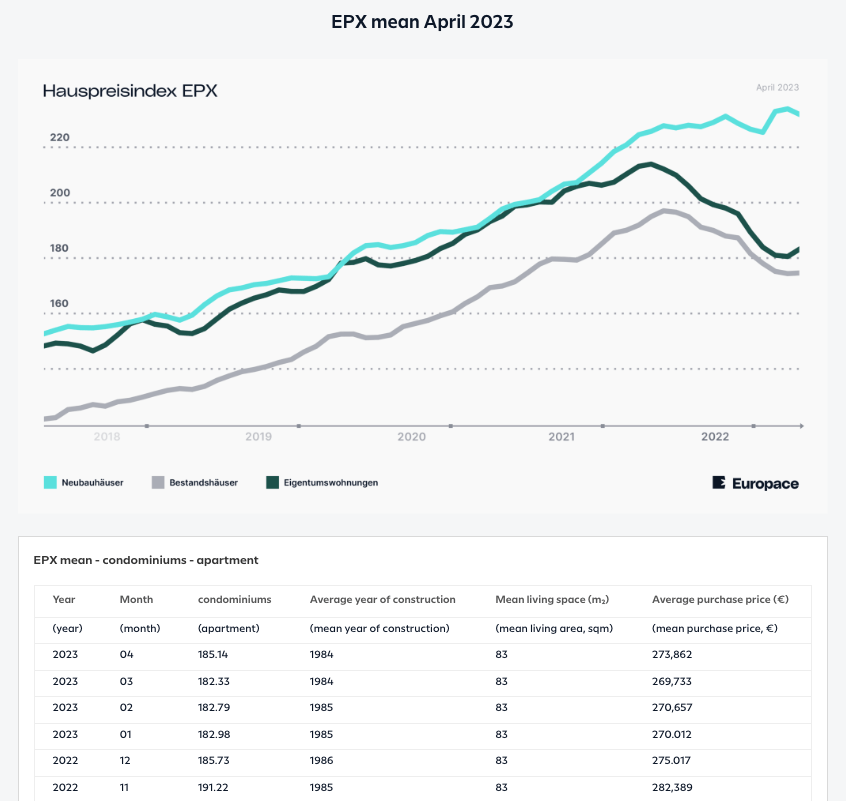

The German property market index is already showing signs of stabilization and modest growth in some sections as per the closely followed Europace German Property Index published for April:

{kind=link}

So Why Is The Stock Trading At 0.35x Book Value?

The stock price currently reflects a ~35% decline in Vonovia's assets value from here. I believe most readers, especially ones familiar with the German property market dynamics, would agree that this is a remote probability.

So why is it trading at such distressed levels?

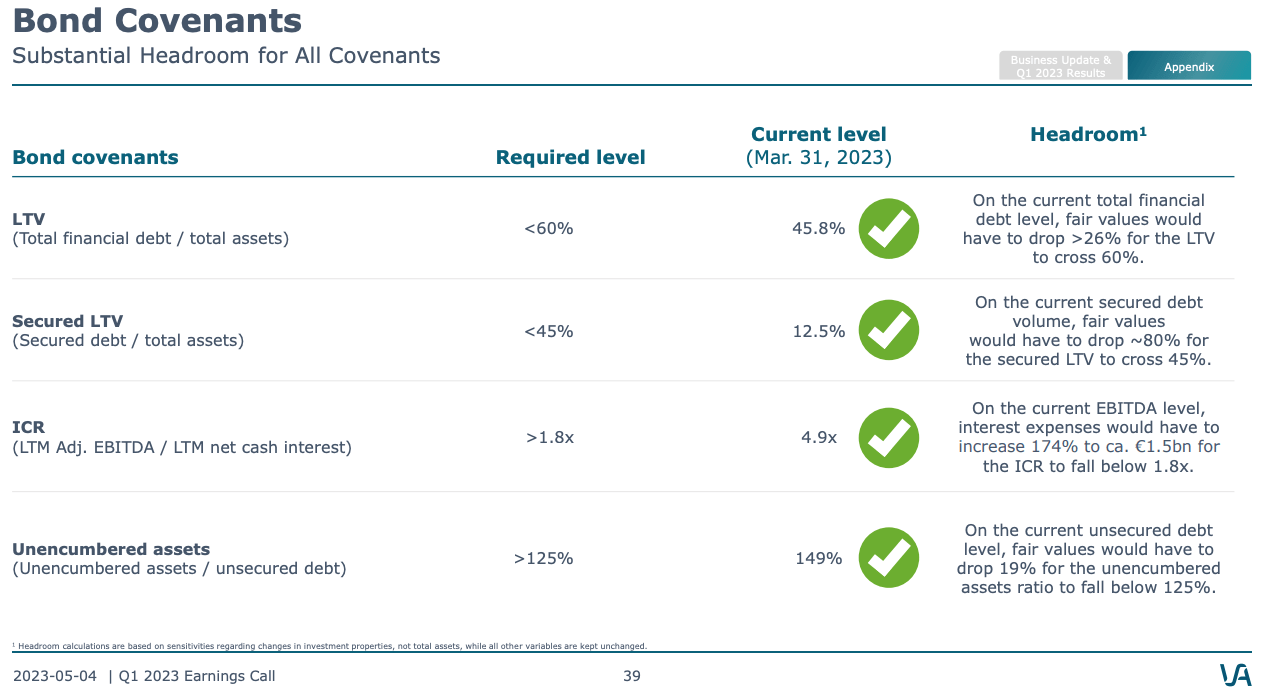

The key reason is fear of equity dilution and/or fire sale triggered by a breach of debt covenants. As illustrated by the below chart, Vonovia has plenty of headroom against its debt covenants:

{kind=link}

I see the probability of Vonovia even getting close to breaching any of these covenants as remote, especially in the context of its continued disposal program.

Vonovia's provided a target for 2022 of disposals (including JV equity transactions) of EUR2 billion. It already delivered three-quarters of the target and is now expecting to exceed that target by a long mile. The sources of disposals are highly diversified and thus provide Vonovia with flexibility around the type of assets it chooses to monetize.

Vonovia Investor Relations

I suspect the next disposal announcements will be announced from Municipalities (as negotiations have been taking place for several months now) and also DW Healthcare's portfolio should fetch in excess of EUR1 billion.

Final Thoughts

Vonovia is trading at a fraction of its book value and this will likely prove to be a generational opportunity to buy the stock. The bears are focused on so-called red flags and/or discounts provided in recent disposals.

I believe the bears are not seeing the forest for the trees.

The market is indeed frozen currently, so completing large transactions requires Vonovia to be creative and flexible on pricing. However, the biggest benefit is the reduction in the tail risks of equity dilution and forced fire sales. Naturally, the pressure to complete large deals quickly has now greatly reduced.

Notably, in the recurring sales segment, Vonovia is recording sales at 56% premium to book albeit on low volumes. It is now more likely that the next transactions (e.g. Municipalities, DW Nursing) will be completed at closer values to the book value.

The green shoots are indicating that German property prices are already stabilizing or even slightly growing. The rental growth in the outer years is likely to accelerate and this should grow the top line in the years to come.

Whilst I do expect the book value to still decline slightly in the next quarter or two given the backward view of valuations. The medium and long-term fundamentals are exceptionally attractive.

The tail risks are now largely reduced and therefore the risk/reward is asymmetric in my view. In two to three years from now, this would likely look as a once in a generation opportunity. I continue to add at these prices.

For further details see:

Vonovia: Why The Bears Are Wrong