VOPKF - Vopak: Still Trading At An FCF Yield Of Almost 10%

Summary

- Vopak is a logistics provider offering storage and terminal services.

- Vopak's second half of 2022 was stronger than I had anticipated, and the company is guiding for further growth.

- I sold my position but I should get back in on weakness: Vopak still isn't expensive.

- I expect the sustaining free cash flow per share to come in at 2.80-2.85 EUR this year. The dividend could increase further to 1.35-1.40 EUR per share.

Introduction

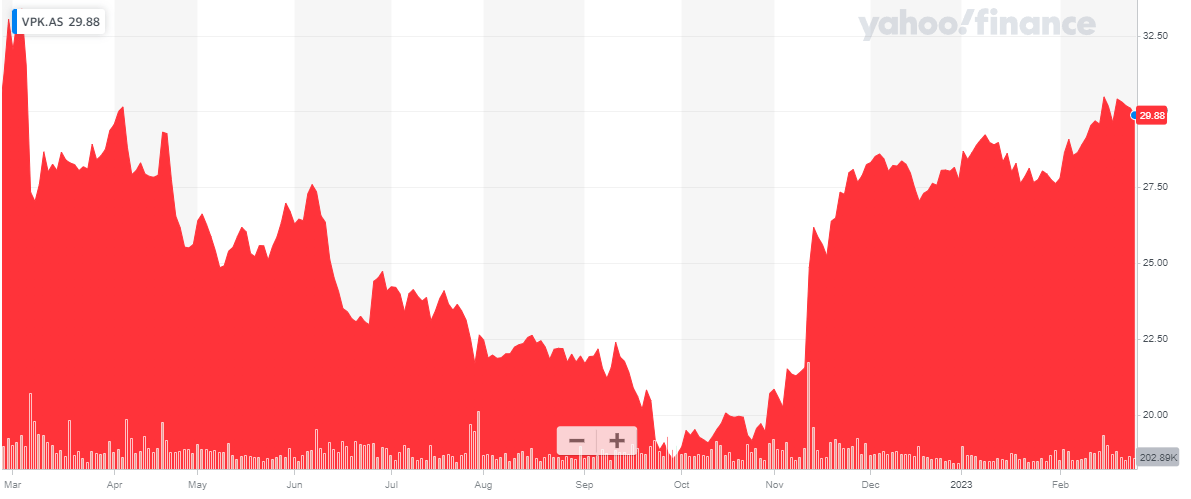

Back in August, I was very surprised to see the market punishing Vopak ( VOPKF ) ( VOPKY ) for what I thought was a robust set of results for the first semester of the year. I was scratching my head to understand the market’s reaction as the underlying sustaining free cash flow (the free cash flow excluding growth investments) was still pretty strong and for sure didn't warrant the weak share price.

We are now just over six months later and the stock is up about 30% (in Euro. It’s up almost 40% in USD but as Vopak’s primary listing is in Euro, it’s only fair to use that as the base currency) thanks to a gradual share price increase in the second half of last year. Vopak recently released its financial results for 2022 and that gives me a good excuse to fine-tune my thesis.

{kind=link}

Vopak is a Dutch company and its listing on Euronext Amsterdam is a better option than its OTC listing. The ticker symbol in Amsterdam is VPK , and with an average daily volume of approximately 250,000 shares, the Amsterdam listing clearly offers the most liquid listing. Additionally, there are options available.

The full-year results are now in, and they compare favorable to my expectations

As this article is meant as an update to previous articles, feel free to check the older articles to get a better understanding of how the storage and terminal company works.

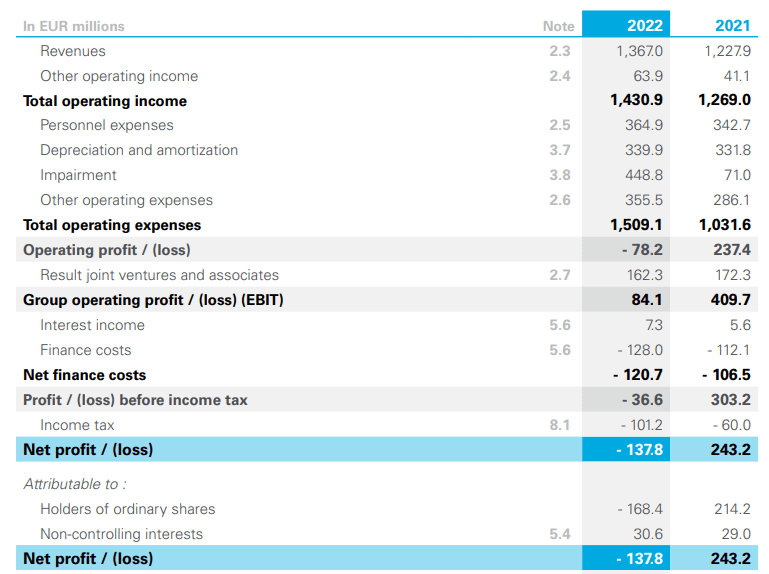

Vopak reported a total revenue of 1.43B EUR in the financial year 2022, which is an increase of more than 10% compared to the preceding year. While the operating expenses increased by in excess of 45%, it’s important to note this is mainly related to the impairment charges which increased from 71M EUR to 449M EUR. Excluding these impairment charges , the 2021 operating expenses would have come in at around 960M EUR versus the 1.06B EUR in FY 2022. This actually means the underlying margins were very stable as the adjusted EBIT margin, which was almost 38% in FY 2021 came in at 37% in 2022 and that difference was attributable to the slightly lower result from joint ventures and associates.

{kind=link}

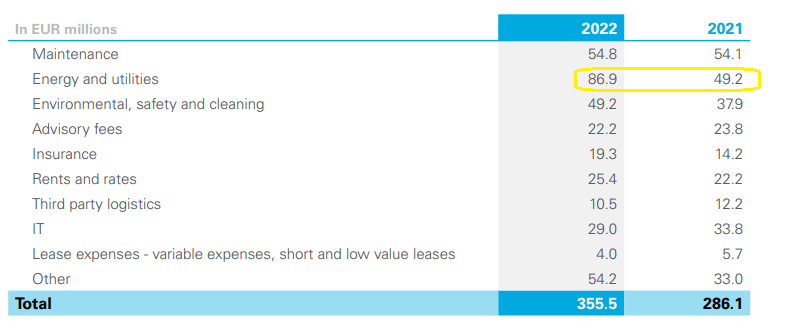

I discussed the reason for those impairment charges in my previous article so I’d recommend you to read up on this element there. I was also a bit worried to see the ‘other operating expenses’ increase from 286M EUR in FY 2021 to 356M EUR in FY 2022 (an increase of almost 25%) but according to the footnotes this was mainly related to higher energy expenses. As the cost of energy has come down, I expect Vopak to be able to reduce its ‘other operating expenses’ this year.

{kind=link}

In the August article, I focused on Vopak’s free cash flow performance. Not in the least because the impairment charges are obviously hiding the underlying strength of the company. That also is why you shouldn’t be too worried about the reported net loss of 138M EUR and a net loss of 168M EUR attributable to the shareholders of Vopak. The EPS of a negative 1.34 EUR is irrelevant due to that impairment charge as the company even had to include a tax bill on a negative pre-tax income. This was related to some non-deductible expenses but mainly to the derecognition of tax losses and tax credits.

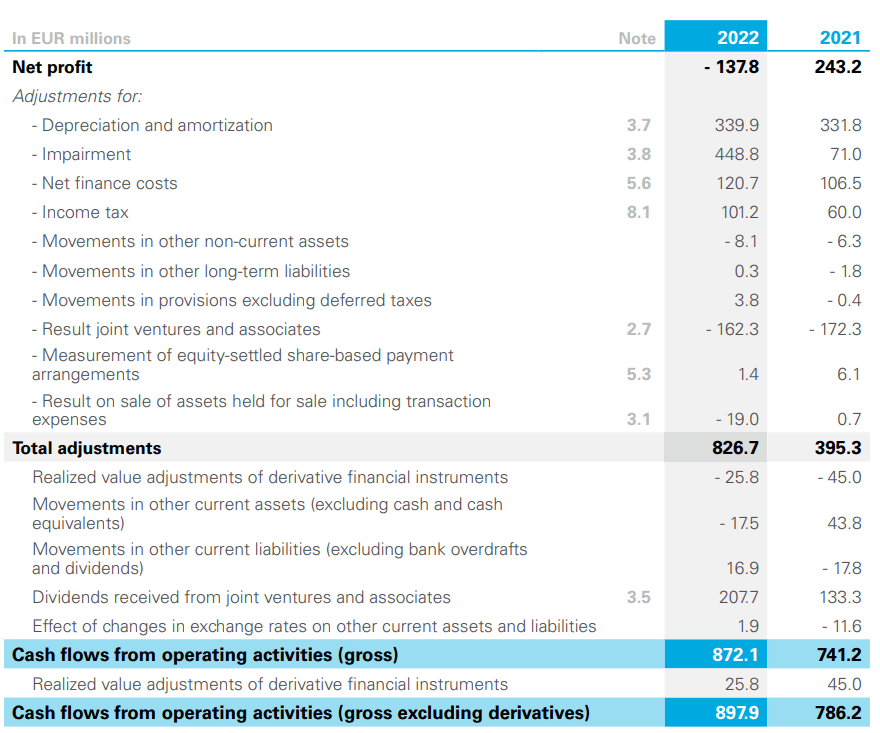

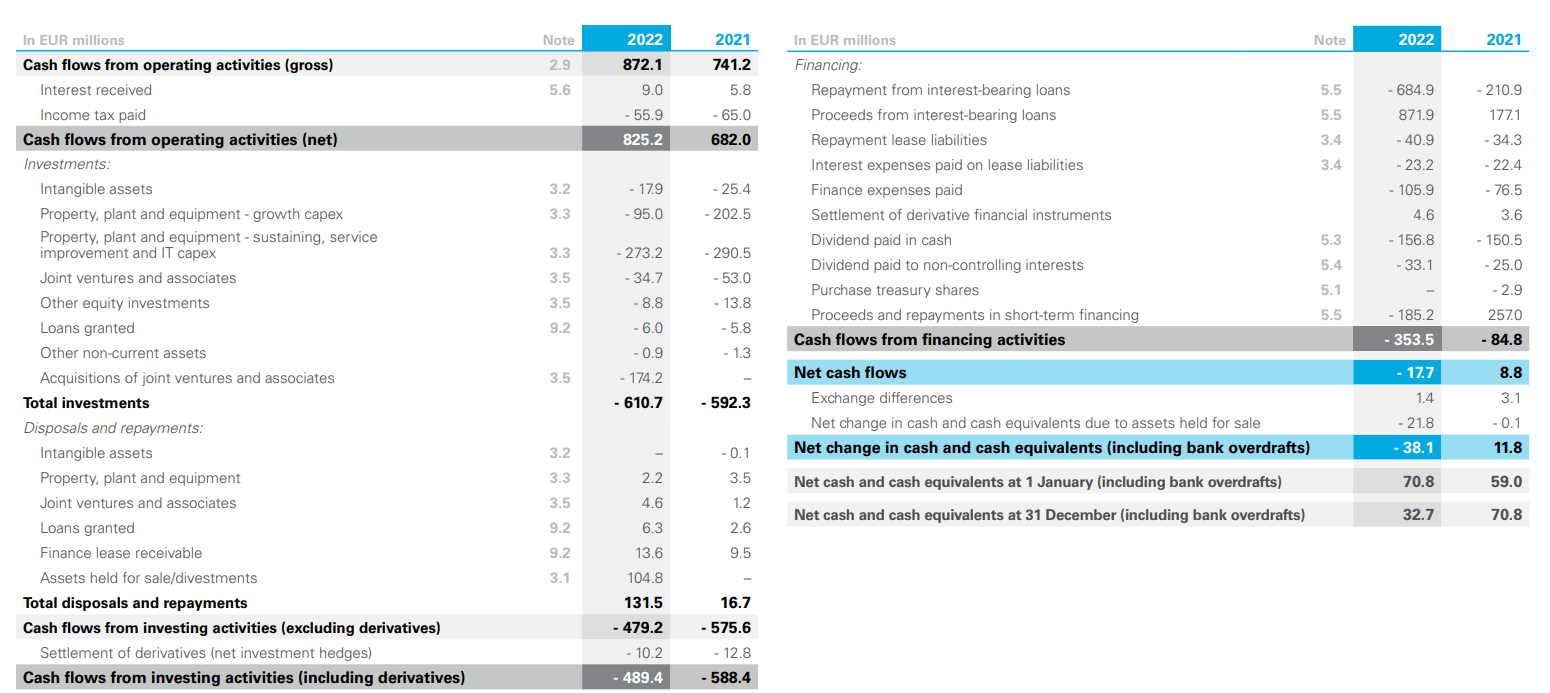

The cash flow statement paints a more clear picture. The starting point of the cash flow statement (see later) was the ‘cash flows from operating activities’ of 872M EUR, but I first wanted to see the details on that.

And as you can see below, the 872M EUR includes the dividends received from JVs and associates, but excludes the net finance expenses and the tax payments.

{kind=link}

That doesn’t have to be an issue as those are subsequently deducted from the 898M EUR. After deducting the amount of taxes that were actually paid and adding the total amount of interest received, Vopak posted an operating cash flow of 825M EUR.

{kind=link}

Sounds great, but from that amount we still need to deduct the lease payments (41M EUR), the interest and finance payments (129M EUR) and the 33M EUR dividend payment to non-controlling interests. The underlying operating cash flow was 622M EUR.

The investing cash flows show a total capex of 386M EUR but Vopak does a great job in dividing the total capex in sustaining capex and growth capex. We see Vopak spent about 95M EUR on growth, and the sustaining capex was just 273M EUR. I will also include the intangible capex and will thus use 291M EUR as sustaining capex. That’s in line with the total depreciation and amortization expenses. The underlying free cash flow was 331M EUR. Divided over 125.4M shares outstanding, the free cash flow result was approximately 2.64 EUR per share. Which means that even at the current share price and after the recent share price increase, Vopak is still trading at a free cash flow yield of 9% which is pretty attractive.

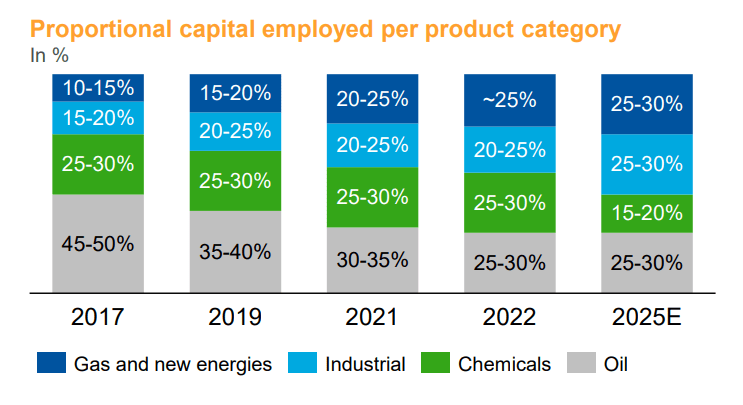

Meanwhile, the company continues to invest in non-oil applications. As you can see below, the percentage of the capital employed in oil-related services continues to decrease.

{kind=link}

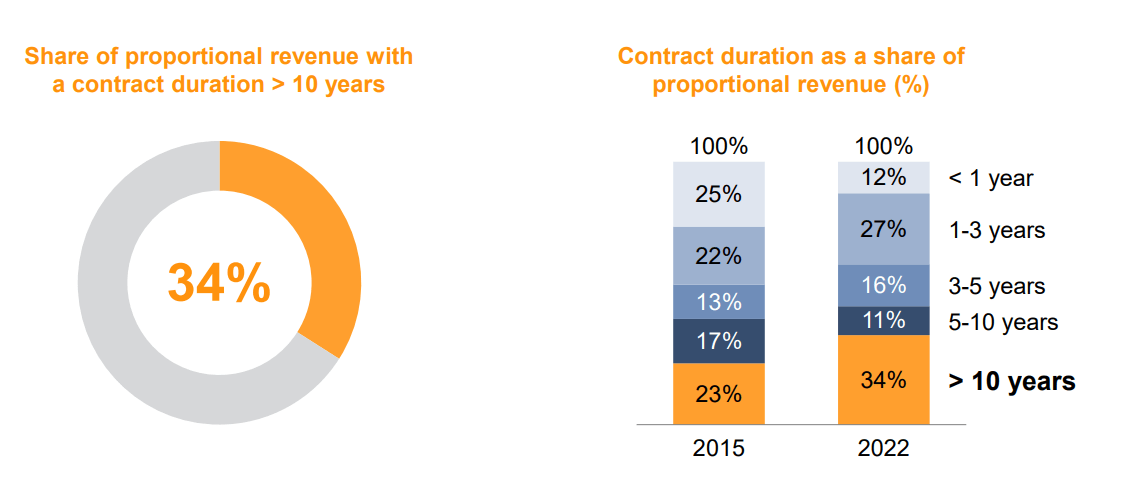

Additionally, Vopak has steadily been increasing the average contract duration rate. Right now, about a third of the revenue is locked in with contracts that last for at least 10 years and about 45% of the revenue comes from contracts with a remaining term of at least five years.

{kind=link}

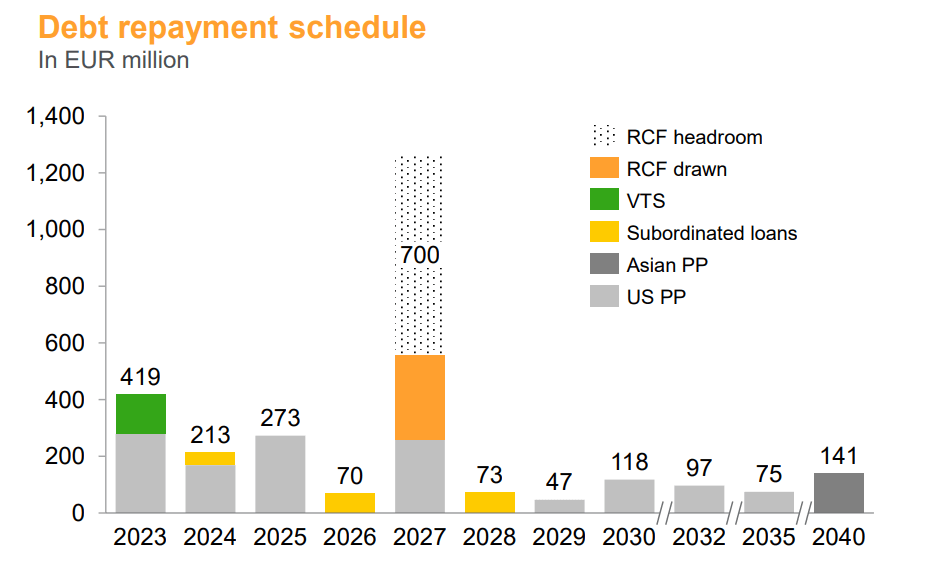

One of the main risks I see is the interest rate risk. Fortunately Vopak has a strongly diversified debt repayment schedule.

{kind=link}

I’m not too worried about the interest rate risk though. As you can see below, the vast majority of the debt has a fixed interest rate and there’s just a relatively small portion of floating rate debt. And sure, fixed rate debt will have to be refinanced one day but considering Vopak’s average cost of debt is already almost 4%, I think the total impact will be pretty benign. Even if Vopak needs to start paying 6% (which I don’t think will happen), the free cash flow will be impacted by just 40M EUR per year (assuming an average tax rate of 20%).

Vopak Investor Relations

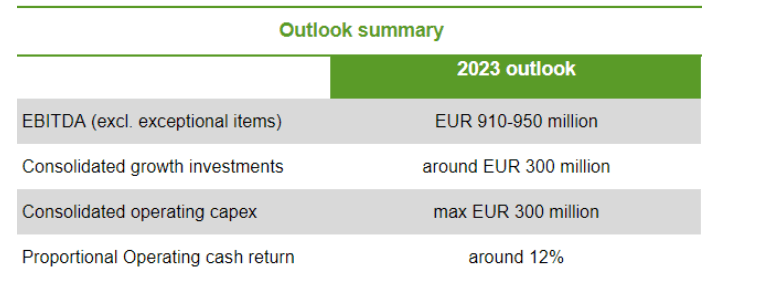

It's all looking pretty good and for 2023 Vopak is guiding for an EBITDA of 910-950M EUR. Considering the FY 2022 EBITDA was ‘just’ 887M EUR, Vopak expects its EBITDA to increase by 3-7%. And considering the interest expenses won’t increase by much, the operating cash flow will likely increase by 20-25M EUR, using the midpoint of the EBITDA guidance.

{kind=link}

Investment thesis

I put forward 30 EUR as initial target when my August article was published and I sold my entire position for an average profit of around 30% in six months. I was happy with that performance but I do have to admit Vopak performed better than I had expected while its guidance for FY2023 is better than expected as well. Using the midpoint of the EBITDA guidance, I expect the sustaining free cash flow (excluding growth investments) to increase to 2.85 EUR per share and that makes the current share price still reasonable. And in hindsight, I should have held on to the stock as the increased dividend of 1.30 EUR per share offered a 6%+ dividend yield on my average purchase price in the low-20s.

I won’t buy at these levels (despite the implied 9.5% free cash flow yield). But I may write a fresh series of out of the money put options in an attempt to establish a position at a lower share price again. And I would for sure be a buyer on any weakness.

For further details see:

Vopak: Still Trading At An FCF Yield Of Almost 10%