VNORP - Vornado Realty: Top Real Estate At Bottom Prices

2023-04-18 09:46:33 ET

Summary

- While sector headwinds persist, Vornado's well-located, class A assets have largely insulated it from leasing risks, as demonstrated by its robust leasing pipeline. Its PENN district developments offer further upside.

- Vornado has a liquid balance sheet, few upcoming maturities, and its floating rate debt is largely hedged. Both interest expense and dividend are well covered.

- Vornado's valuation is cheap relative to peers and its forward earnings. It trades below liquidation value and is cheap on a book value, cap rate, and FFO multiple basis.

Editor's note: Seeking Alpha is proud to welcome JPS Capital as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Vornado Realty's ( VNO ) recent selloff has presented a compelling opportunity to acquire world class real estate assets at an attractive valuation.

VNO owns and operates an impressive portfolio of office and retail property predominantly in Manhattan. With close to 20 million square feet of office space, across 30 properties, they are the second largest office landlord in New York City and are leading the major PENN District development in Midtown. They also own or have an interest in 2.6 million square feet of Manhattan retail and over 1,600 residential units with additional office and retail holdings in Chicago and San Francisco. A full catalog of their portfolio is available here .

Down 77% from its pre-pandemic levels and 28% year-to-date, the stock has been strewn into widespread panic selling in the office REIT market. Work-from-home trends have redefined the need for office space and ongoing layoffs have sparked fears of tenant downsizing. Interest rate volatility has also pressured VNO given its highly levered portfolio.

History indicates that well located, well operated and well capitalized real estate will weather the storm. At current prices, Vornado's class A portfolio, diverse tenant base and lucrative valuation offer significant upside.

Leasing Risks Overblown

A driver of the recent sell off has been concerns of declining NYC office leasing demand and heightened vacancy. Headlines of leasing activity "plummeting" are reminiscent of the Great Recession when NYC office rents dropped 25%+, however Class A Manhattan rents have actually held steady this year, according to CoStar. In fact, Vornado's weighted average office rents have actually increased 10% from 2019 to 2022, despite the citywide pandemic vacancy jump.

Given its well located, class A product, Vornado has navigated this occupancy risk quite well with its properties 93% occupied compared to market wide 87%, according to CoStar. While there certainly exists a temporary oversupply in the market, there exists no long term structural threat to Vornado's business, as price action implies.

NYC office space has endured many cyclical downturns, recessions and periods of oversupply throughout the decades. Its status as the money center of the world has entrenched long-term demand for office space across a wide breadth of industries.

Unlike West Coast office REIT counterparts Kilroy Realty ( KRC ) and Hudson-Pacific ( HPP ), which have 60% and 39% , respectively, in technology tenant concentration, Vornado's lease concentration risk is largely insulated from the most credit-risky, work-from-home-prone companies.

{kind=link}

While Vornado's largest tenant, Meta, cut back on its NYC presence recently, it opted to maintain its footprint at Vornado's 770 Broadway and Farley building, a testament to quality of Vornado's new construction product. Zuckerberg also recently encouraged employees to return to office , joining a wider trend that has seen office utilization rise steadily in recent months.

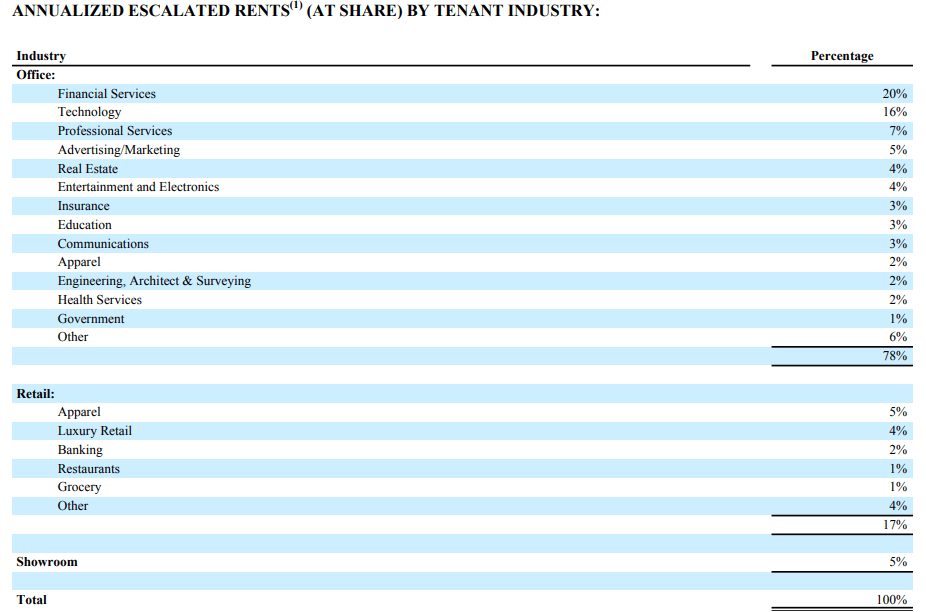

According to Kastle data, NYC average physical office occupancy is near 50%, up from 35%, a year ago. Some of Vornado's largest industry composition are financial services, professional services and real estate tenants, which have all been among the most vocal proponents of a full return to office. Further, fears of layoffs and a loosening job market may tilt an acceleration in return to office.

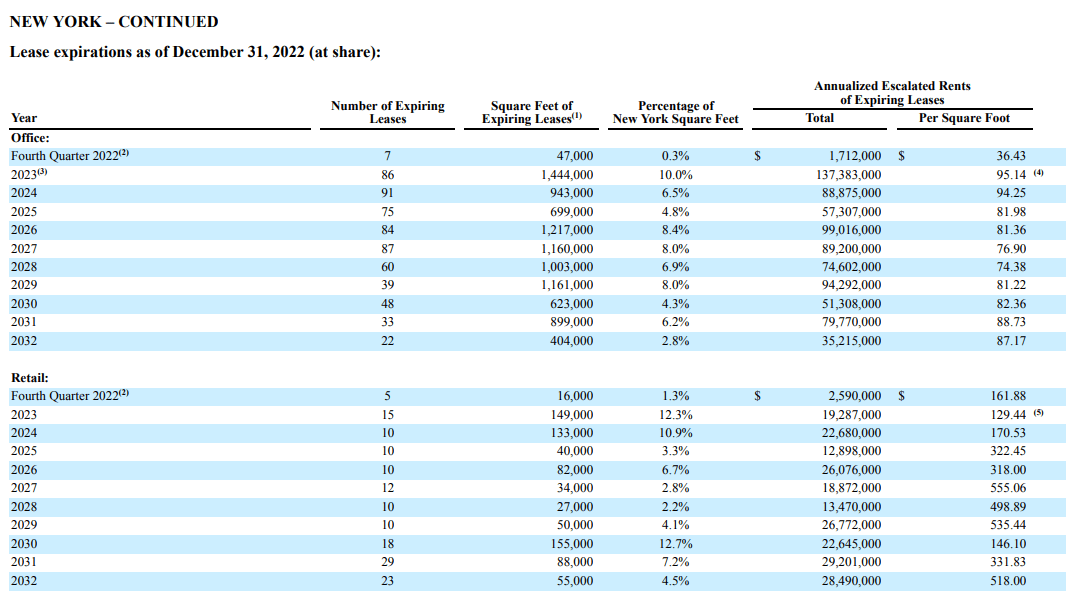

While VNO has over 1.5 million office square feet (10% of square footage) up for renewal in the next year, management stated they already have 1.2 million square feet in the leasing pipeline. They also guided to lease office space at $85-$95 per square foot (psf) this year, a modest decline on expiring leases and a premium Vornado's NYC office in-place $84 psf. Management is also guiding retail rents at $125-$150 psf, a potential mark up from in-place rents at $129 psf.

Vornado Lease Roll (Vornado 10K)

{kind=link}

A main reason why Vornado has fared better than competitors is its asset quality. General market office demand for NYC has softened, but tenants are now fleeing to high quality, class A offices , often paying a large premium to do so. Vornado, whose portfolio is highly amenitized, and a large portion of which is newly constructed or recently redeveloped, will benefit.

As CEO Steven Roth noted on the Q4 earnings call : "We believe quality product wins today...not long ago new construction commanded a $20 premium, now it commands a $100 premium or more ."

Those premiums could apply to over 1.4 million square feet that is currently under development in Vornado's PENN district projects, a large-scale Vornado-led redevelopment of office and residential space around Pennsylvania Station. Vornado accordingly raised their return projections last quarter for PENN 1 and PENN 2, projecting 13.2% and 9.5% incremental cash yields, respectively.

Rendering of PENN 2 (New York YIMBY)

{kind=link}

As a further mitigant to leasing headwinds, Vornado also recently announced the master lease of 585,000 square feet at 350 Park Ave to hedge fund Citadel. The deal included a creatively negotiated 7-year option for Citadel to either:

- 1) hire Vornado as a developer on a 1.7 million square foot tower on 350 Park Avenue and the adjacent 40 East 52nd Street, which would value Vornado's share of the joint venture at $900 million. This option would see Citadel lease half the space at a formula-based rent based on project return and cost of capital.

- 2) exercise an option to purchase the site for Vornado's share of $1.4 billion ($1.085 billion). Vornado equally has the right to put the site to Citadel for $1.2 billion through the option period.

The 7-year option structure also gives management time to execute development once financing conditions are more favorable and will allow Vornado to capitalize their land contribution as equity .

The Citadel deal indicates both strong sustaining interest in New York office space among top financial services companies and offers significant future non-spec development upside that many office REITs do not offer.

While the marginal oversupply of office is a concern, investors are overreacting to its fundamental impact on VNO. Even in a stressed scenario, if we assume 50% of next 2 years' expiring square footage is renewed (2.4 million SF) at $75 psf, the incremental impact on revenues is less than 7% , excluding potential upside from new PENN development square footage coming online.

In sum, Vornado's large 2023 lease roll and softening demand have spooked short-term investors who look past Vornado's asset quality, good management and the long-term inevitable rebound in NYC office demand.

High Liquidity Balance Sheet

VNO, like any REIT, is a highly levered business. A major benefit of investing in REITs is that, much of the leverage are non-recourse mortgages, backed by the properties, rather than a guarantee from the joint venture or VNO. This insulates VNO's credit rating and corporate debt from the performance of a few lagging properties. It also gives VNO the ability to walk away from a property if an agreement cannot be reached with lenders via loan modification, extension, forbearance, etc.

While their $8.5 billion net debt figure seems daunting, management re-financed over $3.2 billion in near-term debt in July, swapping much of it to fixed and pushing out maturities. As a result, there is only $378 million of debt due in 2023 and another $2.4 billion due in the next 3 years.

VNO has ample liquidity to handle these upcoming maturities. Across marketable securities and cash, they have close to $1.5 billion , with an additional $1.9 billion available on revolving credit facilities.

This balance sheet strength also means VNO can stave off asset sales in a potentially cold market. While competing NYC office landlord SL Green ( SLG ) plans $2.5 billion of dispositions of property in 2023 to pay down debt, VNO will de-lever through earnings growth, strategic re-financings and proceeds from operations, as the CFO recently touched on .

Assuming a conservative NOI of ~$1.1 billion in 2023, Vornado has a high margin of safety to finance $360 million in interest expense, $250 million in recurring capex (per guidance) and $285 million in common share dividends, leaving nearly $200 million to de-lever or finance remaining growth capex without tapping into existing liquidity.

Debt Outstanding (Vornado 10K)

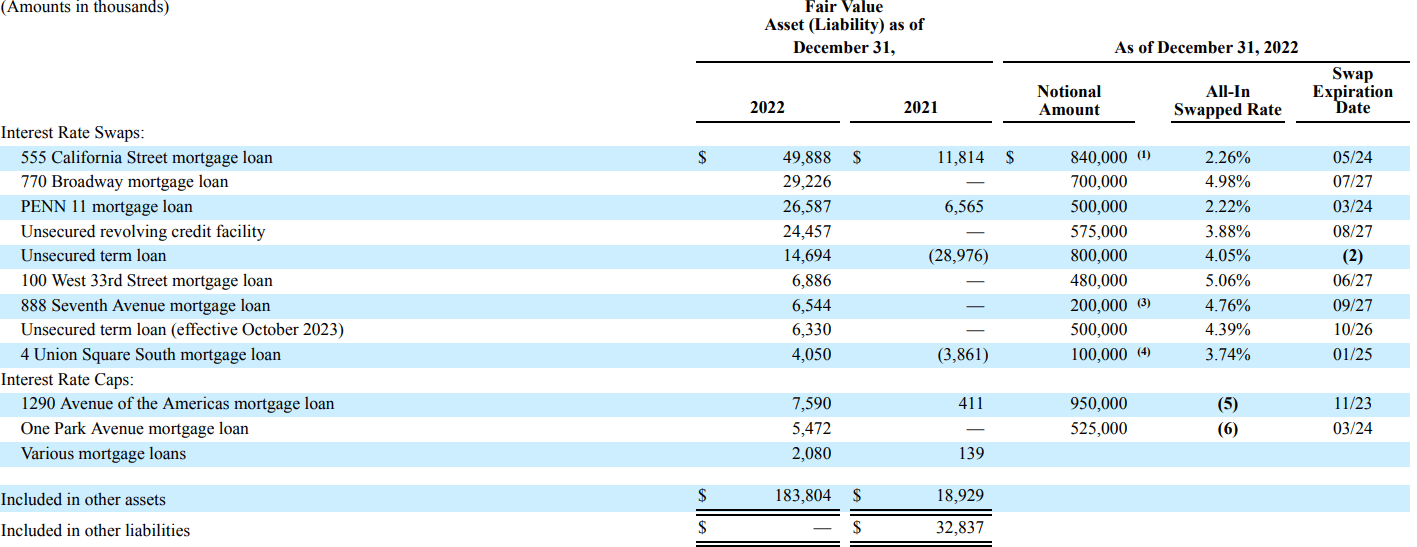

Their floating rate exposure is also limited. VNO wisely swapped many of their mortgages to fixed rate via rate swaps and caps in 2022. $6.1 billion (73%) of their debt is fixed at a weighted average rate of 3.59%. This includes Vornado's 70% share, or $800 million, of the Bank of America tower loan in San Francisco, maturing in 2 months (with several extension options) that has been swapped to an all-in rate of 2.26% and remains 95% occupied, despite its watchlist status . The remaining variable debt, as of Dec 31 2022, accrues interest at 5.67%.

Much of these swaps do not expire until well into 2024 and beyond when the SOFR forward curve implies a steep drop in rates. Management also implied that future expiring swaps will be rolled forward and that the dividend cut will allow for an additional $130 million to be set aside this year.

Interest Rate Swaps (Vornado 10K)

{kind=link}

Their T-bill position also doubled from 2021 and $1 billion was rolled into higher yielding securities which further offsets their floating rate risk.

Management has not released guidance for 2023, however, when pressed on the Q4 earnings call, Roth mentioned FFO performance will be "comparable to this year." Needless to say, VNO's annualized 2022 Q4 interest expense of $360 million is well covered by its 2022 NOI of $1.15 billion and FFO of $640 million, figures far from insolvency.

Vornado already has expended close to $2 billion in ongoing developments in the PENN District, with another $500 million expected to be spent on growth capex in the next 2-3 years, primarily on PENN 1 and PENN 2. These developments have been solely financed with cash pre-funded from the outset of the development, giving Vornado flexibility to finance out of these investments at attractive rates when capital markets loosen.

Overall, although highly levered, VNO's prudent debt management will enable the company to withstand capital market pressures that many landlords may struggle with.

Trading Well Below Liquidation Value

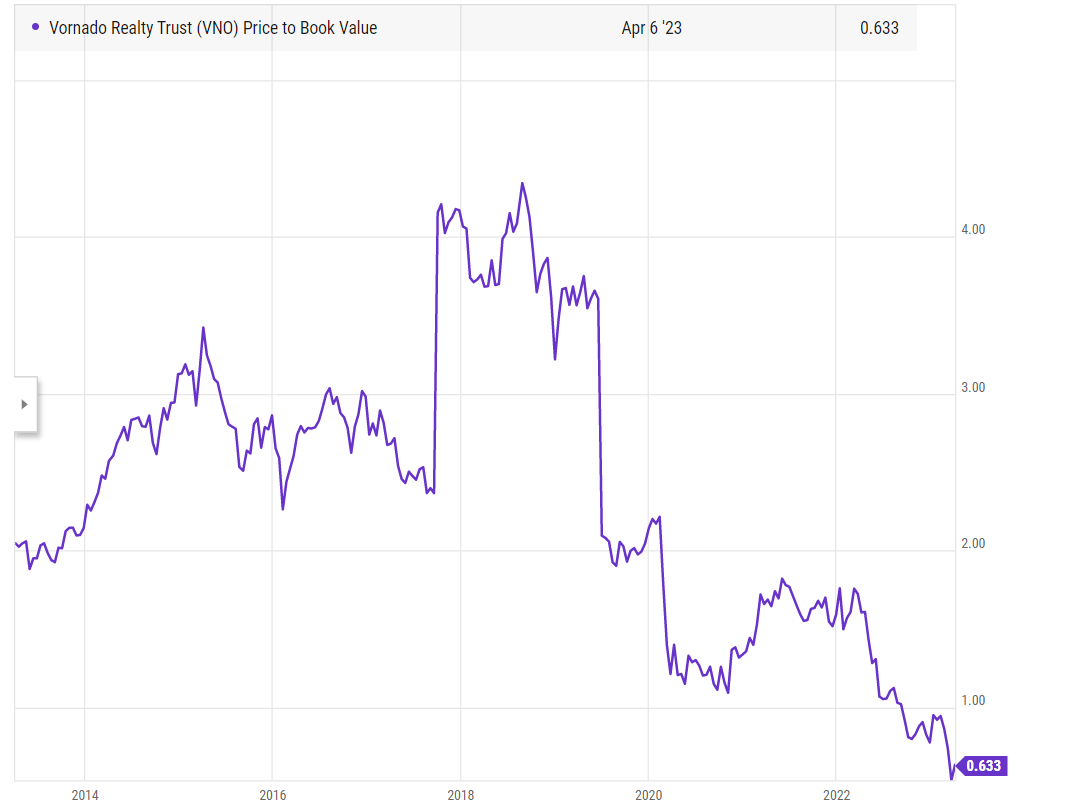

The sharp selloff has seen VNO drop to levels not seen since 1996, presenting the opportunity to own VNO's portfolio at a bargain valuation. The company now trades well below its historic price to book value at 0.63x , implying that Vornado's real estate trades at a 37% discount to original cost, net of accumulated depreciation.

Vornado Price to Book Value (YCharts)

{kind=link}

Vornado's cost basis for its portfolio, including capital improvements, is over $13.3 billion per the company's 10K. Many of its acquisitions and developments date back to the late 1990s. After netting out debt and cash equivalents, you are essentially buying a portfolio that cost nearly $5 billion in equity to assemble and improve over three decades, for under $3 billion. And that is before accounting for the cost inflation to replace those assets and the market price appreciation of those assets.

Indeed, according to consultants' Turner & Townsend 2022 International Construction Market Survey , the hard costs to build a new Class A office tower in New York City ground-up is $850 psf, exclusive of soft costs and the cost of land, an all-time high. On Vornado's current enterprise value of $13 billion, you are acquiring over 27 million square feet of top retail, multifamily and office space for under $480 psf, a nearly 50% discount to hard replacement costs.

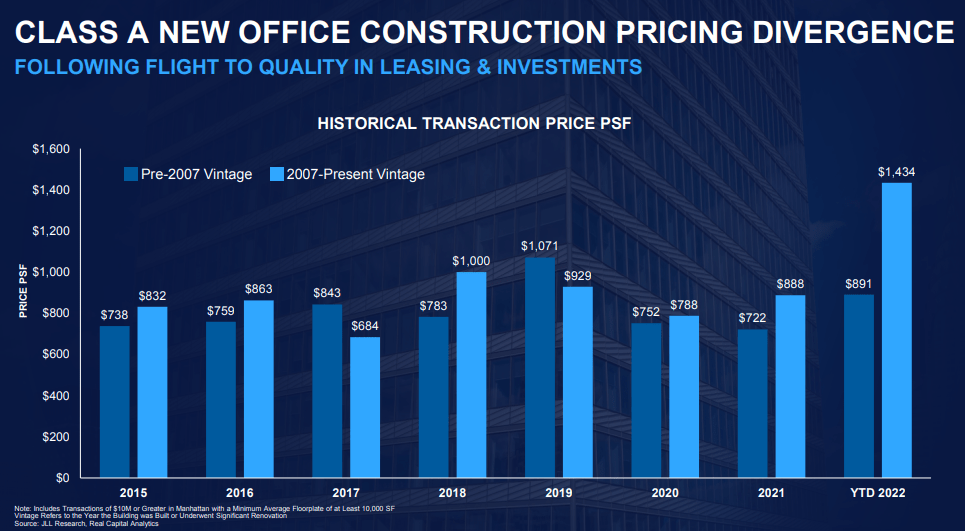

Further, the stock price implies a major dislocation between actual real estate transactions of Class A office buildings in Manhattan and the implied $450 psf enterprise value of VNO. According to data from JLL Research and RCA, presented by SL Green, newer vintage assets are trading north of $1,400+ psf .

SL Green Investor Presentation

{kind=link}

Even as recently as last quarter, class A office real estate traded hands at well over $1,000 psf. Boston Properties purchased a 27% stake from L&L in 200 Fifth Ave in the Flatiron District for $1,400 psf. SL Green purchased 450 Park Ave and 245 Park Ave from Oxford Properties and HNA group for $1,320 and $1,100 psf, respectively. Earlier this year, Meadow Partners purchased West Village 2017-renovated asset 95 Morton St. for $1,350 psf. All these transactions occurred at 4.0-4.5% going-in cap rates and rival Vornado's portfolio in quality and location.

With materials and labor inflation unlikely to subside and the increasing cost of construction financing, it is likely there will be no new starts for the foreseeable future. To give an idea of future supply of office, Vornado itself recently hit pause on several PENN district projects that have yet to break ground due to hard cost inflation and higher rates.

This means that when leasing momentum inevitably picks up again, landlords that withstand current market conditions will have the pricing power. The beauty of Vornado's current valuation is that you do not have to wait for that time to come.

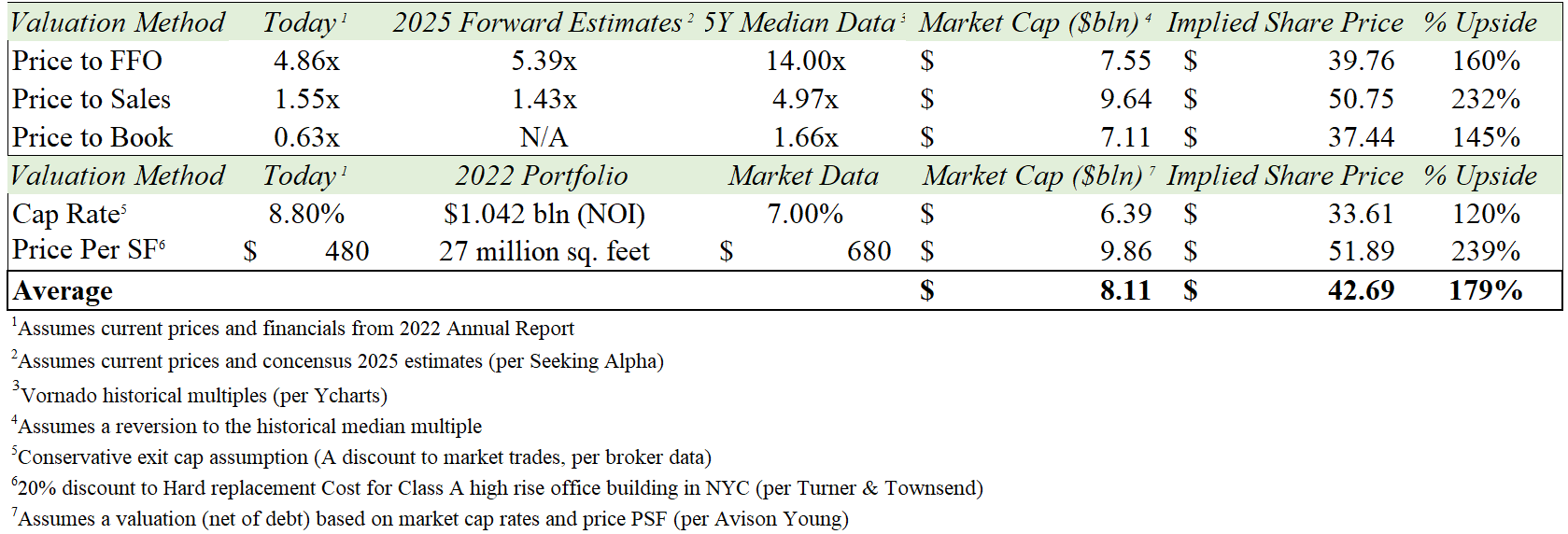

In addition to trading cheap to book value and replacement cost, Vornado also trades at a steep discount to cash flow. Based on 2022 NOI of $1.15 billion ($1.042 billion net of dispositions and ownership changes) and a $13 billion enterprise value, VNO trades at an implied 8.8% cap rate . According to broker Avison Young , the most recent sales data indicate that Manhattan office space transacts at an average 4.6% cap rate. Assuming a 7% exit cap rate (a 34% discount to the market), Vornado could liquidate its portfolio today and fetch $16.4 billion , implying an equity value, net of debt, of $8 billion, or $40/share .

Even on a forward price-to-sales basis, VNO is trading at levels not seen since the depths of the Great Recession, within 2 years of which, VNO delivered a 223% total return, inclusive of dividends.

On a FFO multiple basis, Vornado currently trades at ~5x P/FFO, a 60% discount to the sector, and nearly 3 times lower than its historical 5-year average of 15x and the sector median of 14x. This multiple is similarly cheap on a forward basis, trading nearly 5.4x P/FFO, based on consensus analyst 2025 estimates provided by Seeking Alpha . These estimates imply a 2025 FFO estimate of $2.84/share. Applying a conservative exit multiple of 12x to 2025 FFO implies a $34/share fair value.

That discount is steep when you consider that the company's 10% dividend yield is well covered by FFO at a payout ratio of 45% - you are essentially getting paid generously to wait for Vornado to re-rate to its true valuation.

Various Valuation Methodologies (Author's Calculation)

{kind=link}

On various methods of valuation, VNO is trading well below its intrinsic value with a significant margin of safety. While this gap to NAV offers significant upside, historically during similar times of stress (9/11, the Great Recession), it has taken between 2-3 years before this gap is closed. Depending on the Fed's rate policy, it may take longer for Vornado's true value to be reflected in the price, hence it is to be viewed as medium to long term play.

While the current market environment for office landlord is not necessarily "business as usual," the market is giving no credit for Vornado's asset quality, balance sheet and cheap valuation.

Risks and Considerations

While Vornado is intrinsically cheap based on its assets and cash flow, there are number of short-term risks that have driven much of the panic in the price action.

First, the recent dividend cuts and potential further cuts to the dividend are a headline risk. Dividend sizing decisions are made by Vornado's board and are subject to their discretion and do not necessarily reflect the forward performance of the company. While this risk is opaque, it is important to view Vornado as a capital appreciation value play, rather than an income play, in which Vornado's preferred shares may be a more suitable investment.

Second, given the vast majority of Vornado's liabilities are on the property level, there could be risk with individual properties are unable to cover their debt service. While much of these risks are mitigated by interest rate hedges, there may be volatility and impacts to earnings through impairment charges, such as their recent Fifth Ave and Times Square JV impairment . These risks are mitigated by their ability to work out these impairments with lenders and the portfolio-level ability to service the debt and de-lever in the manner best suited for shareholder interests.

Finally, Vornado's margins are heavily dependent on long-term rates that are out of management control. Higher rates could impact commercial real estate valuations by pushing cap rates higher and stressing their FFO margins. This is the pre-eminent risk that has led REITs lower in recent months. Vornado can confidently weather this risk, given the lack of upcoming debt maturities and low cost basis for many of these investments. Their ability to re-finance their new developments enable them to shore up the balance sheet, further buffering this risk factor.

In a bear case, in which rates rise further than priced in (short-term rate of 500-525 bps in May), Vornado may experience significant volatility. Financial services tenants (20% of Vornado's rent roll) may vacate or downsize, posing significant risk to NOI. While unlikely to cause insolvency, Vornado could drop below a $2 billion market cap. Indeed, the pre-eminent risk to Vornado applies sector-wide, rather than idiosyncratic.

In spite of these risks, it is important to remain steadfastly bullish given Vornado's historic ability to manage fluctuations in office demand, rate volatility and recessionary risk. Vornado has a strong balance sheet to weather rate risk and quality assets to withstand a temporary dip in office demand.

Short sellers, which comprise nearly 11% of float , are fixated on these short-term risks. In the long-run, Vornado has produced impressive shareholder returns by owning and operating world class assets in the strongest office market in the country and will continue to do so. Sellers are overlooking Vornado's valuation relative to its forward cash flow, replacement cost and top tier management which have successfully navigated the company through a global pandemic, the Great Recession, and 9/11.

Conclusion

While sector headwinds may compress margins temporarily, Vornado has an irreplicable portfolio serving top tenants in the most valuable real estate market in the world. Leasing and liquidity fears are overblown and those who endure the short-term volatility will be rewarded with long-term price appreciation. The stock is trading at least 40% discount to its book value and significantly its replacement cost and its historical multiples, even on a forward basis.

Ultimately, VNO's 80% drop since February 2020 has been driven by fear rather than a rational view on fundamentals. At current prices, Vornado is well-positioned to outperform the market once the dust settles.

This opportunity is well-summarized by Warren Buffett's approach, " Whether we're talking about socks or stocks, I like buying quality merchandise when it is marked down."

For further details see:

Vornado Realty: Top Real Estate At Bottom Prices