VSEC - VSE Corporation: A Lot Of Potential But A Little Pricey

2023-12-07 02:26:23 ET

Summary

- VSE Corporation's financials show accelerated revenue growth and potential for inorganic growth through strategic acquisitions.

- The company provides aftermarket products and services for airplanes, including parts, engineering services, and training.

- VSEC's financials have improved since the pandemic lows, but the high debt and lower efficiency metrics should be considered when valuing the company.

Investment Thesis

I wanted to take a look at VSE Corporation 's ( VSEC ) financials, as the acceleration of revenues from historical averages has caught my attention. The company 's management seems to have made some good acquisitions recently, which lifted the company 's revenues to the next level. The company 's financials have improved considerably since the pandemic lows, and are trending upwards, while revenues seem to be growing rapidly still and the company has a lot of potential to grow inorganically with strategic acquisitions.

Briefly on the Company

VSEC is a diversified aftermarket products and services company. It provides parts and fixes airplanes, like engines and landing gear. Replace old parts with new ones and make sure everything works smoothly. They also provide engineering services to make sure the planes are safe to be flown. The company also provides training to mechanics on how to maintain airplanes. The company serves many different airplanes, including commercial airlines, cargo, military, and private jets. It also serves other modes of transportation, including ships and trucks. Its Fleet segment focuses on USPS vehicles and trucks. Overall, it's a company that has a good reach in logistics and has been very successful so far, as you will see in the next sections.

Financials

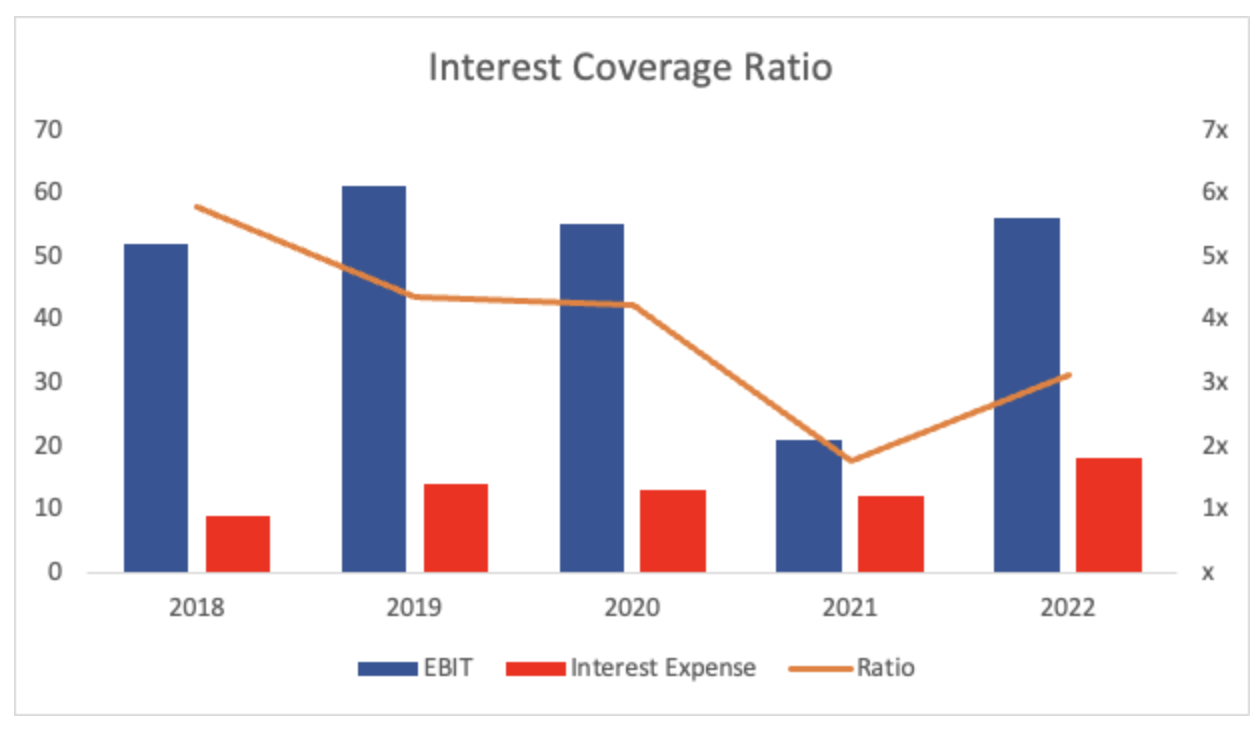

As of Q3 '23 , the company had $20m in cash and equivalents, which is quite an improvement from the end of FY22, when the company had only $300k. In the press release, the management said as of the latest quarter, the company had around $89m in liquidity , which is an even better position. Unfortunately, long-term debt has also increased massively since FY22 to $441m, which is half of the company 's market value. Usually, I don't mind when companies use leverage to fund their operations, but I am a little cautious here because the average interest rate on the debt is around 9%, which is very high. They are hedging some of that risk by entering into an interest rate swap which fixes the rates to 2.8% on $150m and 4.5% on another $100m. One way I measure if the debt the company takes on is worrisome is by looking at the interest coverage ratio, which checks how easily the interest expense on debt is covered by EBIT or operating income. Historically, this ratio has fluctuated quite a bit over the last few years, going as high as almost 6x to as low as around 2x. As of nine months ended September 30, the ratio stood at around 3x, which according to analysts is a healthy ratio. I prefer to approach it more conservatively, so I consider 5x to be much safer. 3x leaves very little room for a bad year of performance when operating income is not going to support interest expense, while with 5x, there is a lot more room for those bad years and still be able to meet all the debt obligations. Nevertheless, the company seems to be at no risk of insolvency right now, but the high debt will have to be taken into account when valuing the company.

{kind=link}

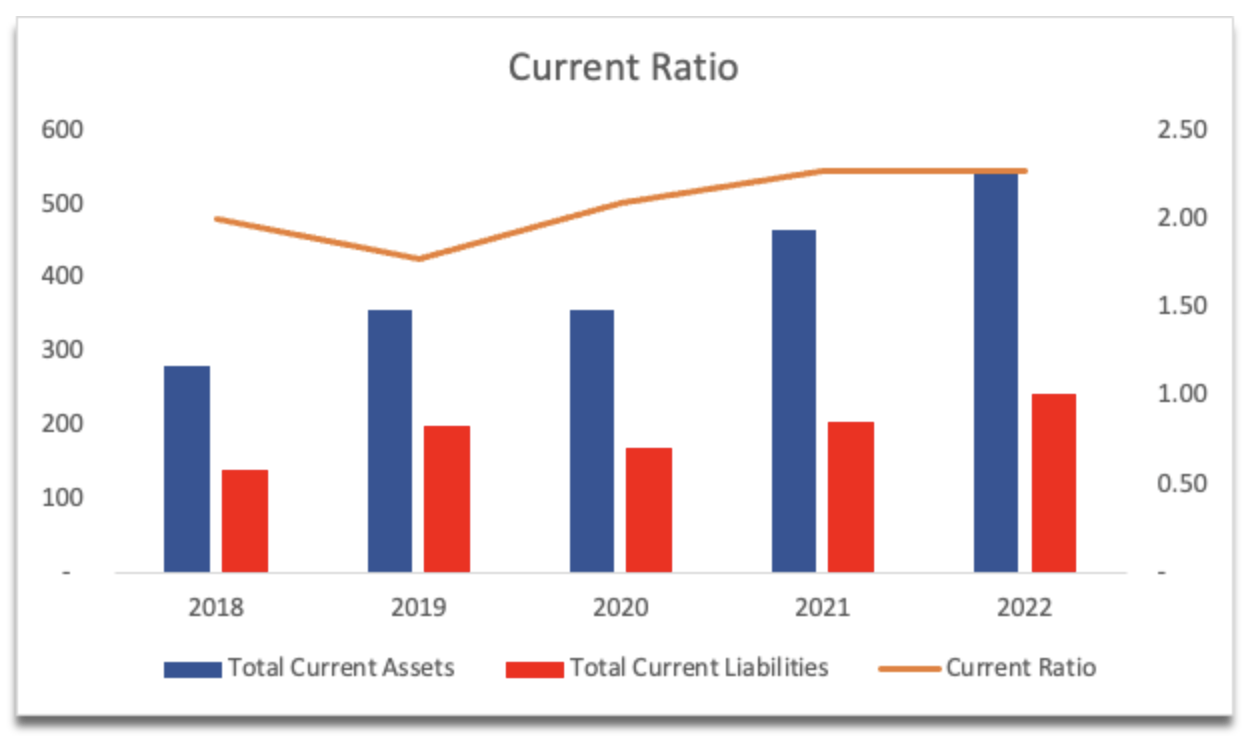

VSEC 's current ratio has been steady over the last few years and in the most recent quarter increased to around 3. This is not a bad ratio of course; however, I prefer the ratio to be in the range of 1.5 to 2.0 as that I believe is more efficient use of the assets and capital. Anything too much over 2 I feel is a wasted opportunity to expand the company footprint and to further growth of the company. Nevertheless, the company has no liquidity issues as it can easily cover its short-term obligations.

{kind=link}

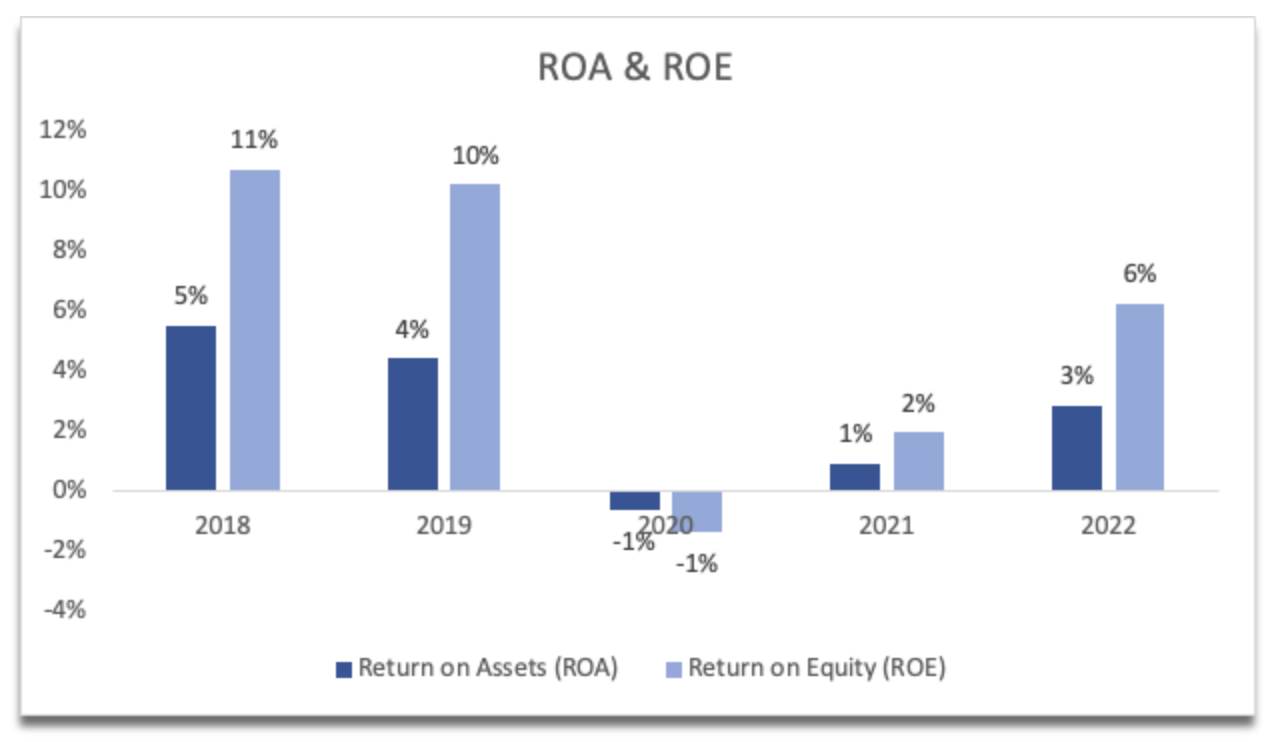

In terms of efficiency and profitability, the company has seen better days, but also worse days during the peak of the pandemic. ROA and ROE were not the worst in FY19, however, once the pandemic hit, the company saw its bottom line suffer dramatically due to a goodwill impairment charge in their VSE Aviation reporting unit. Over the next two years, things have started to improve, however, the situation is not back to pre-pandemic levels just yet. I would like to see the management being more efficient with the company 's assets and shareholder value in the future, until now, I will have to consider the low numbers in the form of an extra margin of safety to take on the risks.

{kind=link}

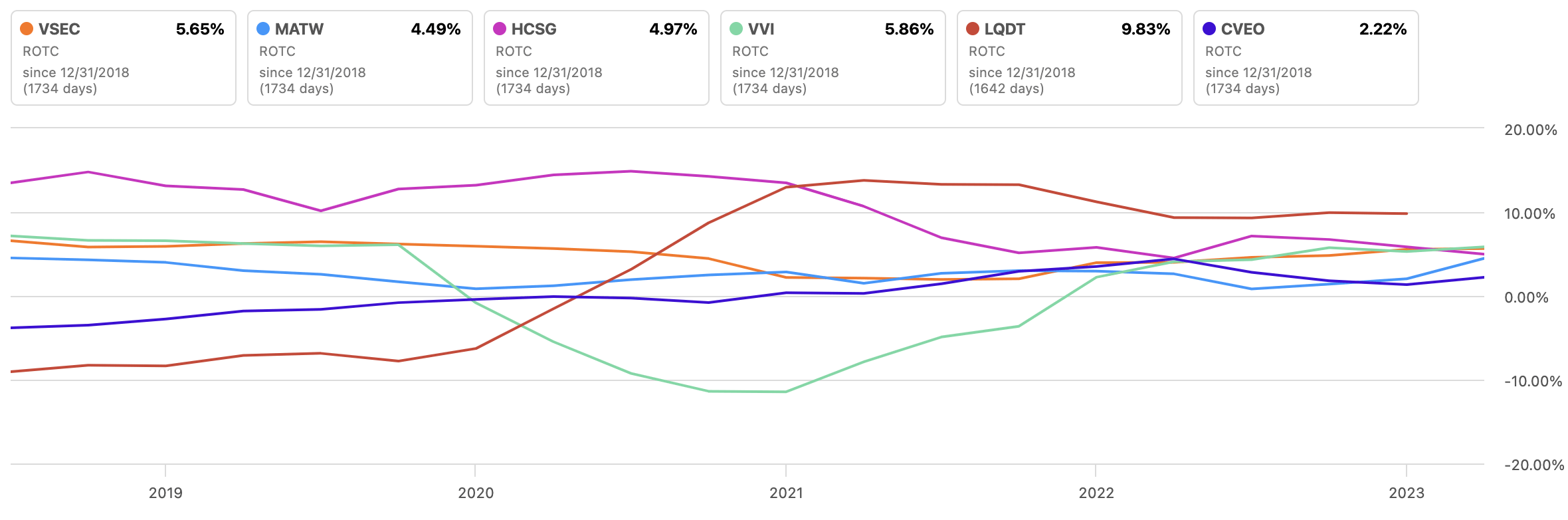

The same can be said about the company 's return on invested capital. It 's not terrible, however, I usually look for at least 10%. This would tell me the company has some pricing power, a competitive advantage, and a strong moat. It would tell me the management can reinvest capital at high returns. 6% as of FY22 isn 't very high, however, if we compare it to some competition, the company sits somewhere in the middle, so it all depends on the industry. I would like to see the management improve the returns here over the next couple of years.

{kind=link}

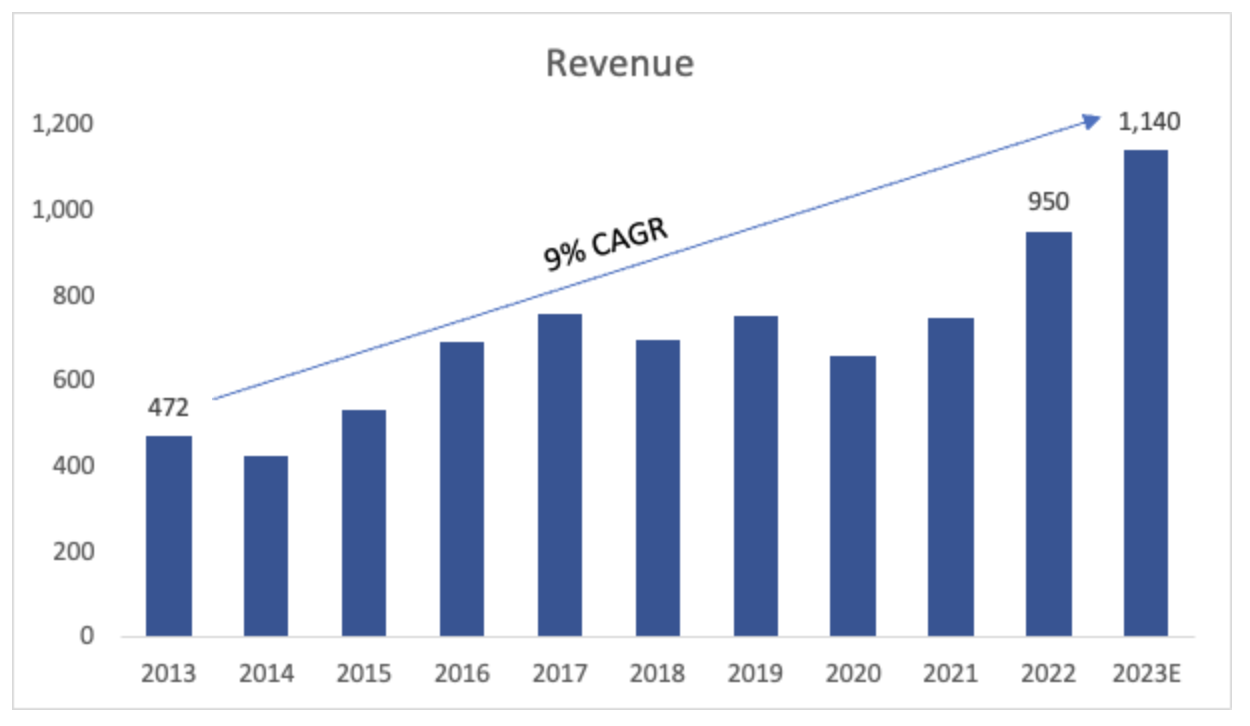

In terms of revenues, VSEC managed an 8% CAGR over the last decade, while growing 13% and 26.5% in FY21 and FY22, respectively. This is quite an improvement from the historical averages, as all segments have performed very well in the latest quarters. The management expects around 20%-25% revenue growth for FY23, which is very impressive. Analysts on Seeking Alpha have -9% for FY23 , which seems to be incorrect (unless I’m missing something).

{kind=link}

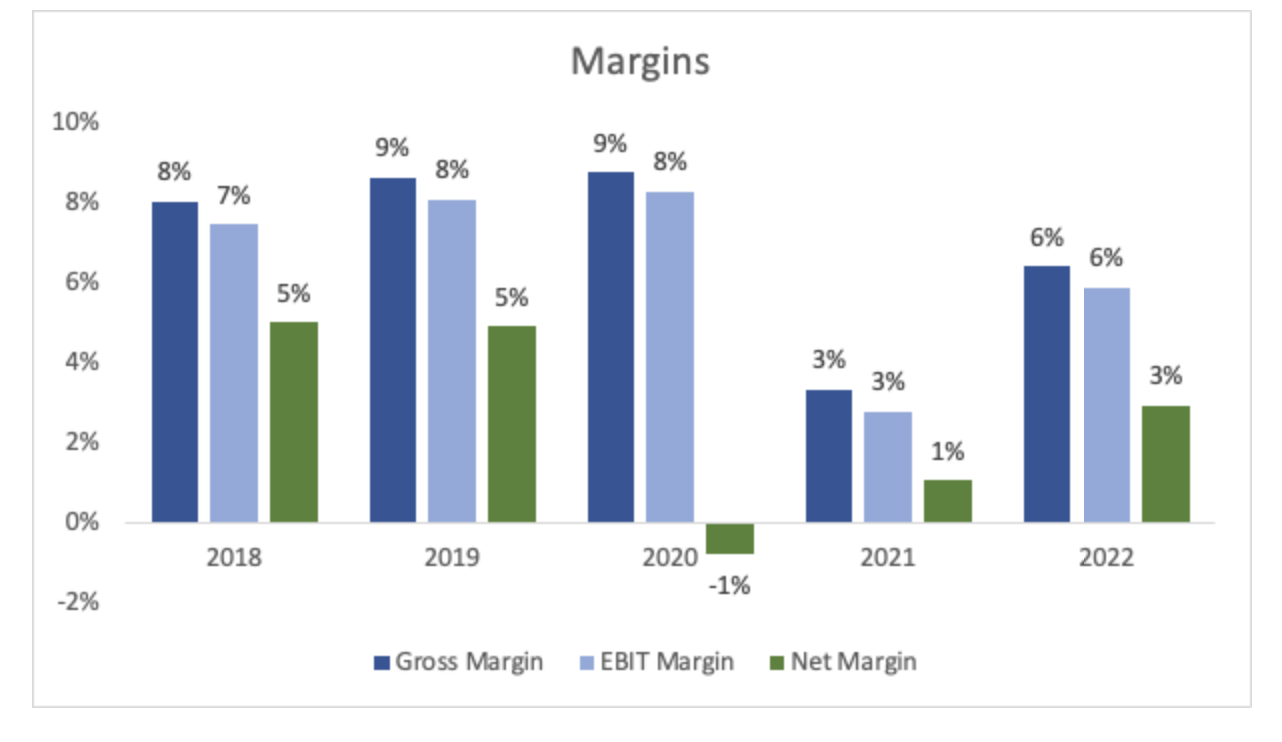

Looking at the historical margins, we can see that the company has still ways to go before returning to its previous efficiency, however, as of Q3 '23, the company 's operating margins stood at around 10%, while net margins at 4.4%, which is an improvement over FY22. There is still one more quarter left, which could bring down these margins or improve them further, but that remains to be seen once they report full-year results in March of next year.

{kind=link}

Overall, I see a company that is growing at a rapid pace, and every metric seems to be a vast improvement compared to FY22. I would like to see the next quarter be stellar too, so the uptrend may continue. The pandemic did not devastate the company 's performance for long, which means the management did a commendable job at navigating the rough waters, and it looks like the company will continue on this upward trajectory for now.

Comments on the Outlook

It seems the management is very competent in the M&A field. The most recent acquisitions of Global Parts in March, Precision Fuel Components in April, and Desser Aerospace in July have been very successful at helping the company propel its subpar historical revenue growth to new levels. I believe that in the future, the management is going to continue to pursue further inorganic growth through various acquisitions. Some may not work out, but if recent history tells us anything, is that the management knows what they 're doing. These acquisitions have been the catalyst that may end up changing the company 's growth trajectory for the better, however, only time will tell right now as it is still too early to judge.

The company is still looking to divest its Federal and Defense Business segment 's assets, which will bring volatility to the share price as it had in the past. That may present a buying opportunity if the share price comes down on an unsuccessful sale, like it did before, or may propel the share price further. Either way, expect volatility on this thinly traded stock.

Valuation

I decided to go with the more conservative outlook for revenues, to give myself a decent margin of safety. For FY23, I went with the company 's lower range of guidance, after that I am reducing the growth down to 5% by FY23, giving me around 11% CAGR for the decade. Below are those calculations for the base, optimistic, and conservative cases, and their respective CAGRs.

{kind=link}

In terms of margins and EPS, I decided to go with improvements from FY22, because the last 9 months showed how much EBIT margins have improved already. I will assume that the company will maintain this level of profitability and slightly improve further over time. Below are those assumptions.

{kind=link}

For the DCF analysis, I decided to use the company 's WACC of 9.3% as my discount rate, and 2.5% for my terminal growth rate. On top of these assumptions, I decided to add another 25% margin of safety to the intrinsic value, because of the outstanding debt and because of the efficiency and profitability metrics that are still rather uncertain but are trending up.

With that said, VSEC 's intrinsic value is around $58 a share, which means that the recent run-up in share price makes it a little expensive right now.

{kind=link}

Closing Comments

The company seems to have been trending in the right direction. The management has done a commendable job of improving operations considerably since the pandemic lows. The company is on the way to overcoming the recent performance peaks of FY18 and FY19. I am curious to see how FY23 is going to unfold. The acquisitions it made along the way seem to justify the use of leverage as it propelled the company 's revenues considerably. The big question for me is if the company will manage to maintain double-digit operating margins going forward or even improve upon as my model suggests.

The recent run-up in share price makes it a little unattractive right now and I would like a slight pullback before deploying some capital and holding the position for a couple of years to see how the operations evolve. I will be setting a price alert at around the $50-$55 price level as that is the range where risk/reward seems optimal for me. The company had a lot of massive swings during the year, so I wouldn’t be surprised if at one point the company comes closer to my PT or even below it.

For further details see:

VSE Corporation: A Lot Of Potential But A Little Pricey