VSEC - VSE Corporation: Divestitures Electronic Commerce Could Enhance The Stock Price

2023-10-02 16:06:40 ET

Summary

- VSE Corporation reports growing operating income in the fleet segment, benefiting from increases in electronic commerce.

- The company may divest certain parts of the business to lower the net debt/EBITDA ratio.

- VSE Corporation is undervalued, with positive expectations for future free cash flow and recent stock price declines.

VSE Corporation ( VSEC ) continues to report growing operating income mainly in the fleet segment, in which VSEC currently benefits from increases in electronic commerce. The growing operating income is beneficial for the recent M&A activity, and VSEC appears to be willing to divest certain parts of the business to lower the net debt/EBITDA ratio. I do see risks from the total amount of debt, M&A integration, or equity dilution. However, with other analysts expecting positive FCF in 2024 and 2025 as well as recent stock price declines, VSEC does look quite undervalued.

VSE Corporation

VSE Corporation is a company with a diversified portfolio of products for end markets and services. It offers repair and logistics and supply chain management services to clients in the land, maritime, and air transportation industry for both private sector companies and public institutions.

Among its clients is the United States Ministry of Defense. The company, in addition to repair and maintenance services for fleets as well as supply chain and logistics management, also offers, to a lesser extent, consulting services for clean energy, data management and interpretation, and engineering support.

Operations are divided into three segments: aviation, fleets, and services for defense institutions. The first of these, which represented 43% of the company's income in 2022, is the one with the greatest business flow, and is aimed at providing supply chains and pieces of equipment to the airline industry in general, including airlines, international, and domestic aircraft manufacturers.

The fleet segment, conducted through Wheeler Fleet Solutions, offers similar logistics and supply services along with inventory management and e-commerce channel management for public and private sector clients.

The services for defense institutions segment serves only defense and military agencies in the repair and maintenance of aircraft and vehicles in general. Regarding the scale of this business, in 2021, the company acquired HAECO Special Services, for tank maintenance among other services. In this regard, it is also worth noting that VSE recently decided not to sell the VSE Federal and Defense segment.

VSE Corporation announced today that it has entered into a mutual agreement to terminate the agreement to sell the VSE Federal and Defense segment to Bernhard Capital Partners, which was originally announced on May 1, 2023. Source: VSE Corporation Announces Mutual Agreement to Terminate the Sale of the VSE Federal and Defense Segment

In May 2023, we entered into a definitive agreement to sell our Federal and Defense business to Bernhard Capital Partners Management LP for a total consideration of up to $100.0 million. Source: 10-Q

I believe that the market overreacted to the recent news about the failed deal, which may have created an opportunity in the market. In my view, the company may be trading a bit undervalued right now.

Source: Seeking Alpha

Further Acquisitions And Divestitures May Bring Further FCF Generation

VSE Corporation currently has an ongoing growth strategy guided mainly through acquisitions. In February 2023, the company acquired Precision Fuel, which allowed it to expand its product line as well as grow its customer base within the aviation segment. The results expected for this year are positive in this sense, and the current objective is set on long-term agreements to serve its clients.

In July 2023, we completed our previously announced acquisition of Desser-Graham Partnership, L.P. ("Desser Aerospace"), pursuant to the terms of the purchase agreement dated May 3, 2023, for a preliminary purchase price of $124.0 million, subject to post-closing adjustments. Source: 10-Q

Considering the failed agreement to sell the defense unit, I believe that VSE may try to sell other business segments to reduce its total net debt/EBITDA ratio. Under this case scenario, I believe that expectations about cash in hand increases could bring substantial demand for the stock.

The Fleet Segment Could Bring Further Net Sales Growth Driven By E-commerce Fulfillment

Regarding the fleet segment, activity within the commercial circuit grew by double digits q/q. I think that the growing trend may continue.

Source: 10-Q

I believe that the increase in activities within electronic commerce and the contracting of logistics services will most likely accelerate business for VSE. In this regard, it is worth noting that the global e-commerce market is expected to grow at a CAGR of 14.7%.

The global e-commerce market size was valued at USD 9.09 trillion in 2019 and is expected to grow at a compound annual growth rate ((CAGR)) of 14.7% from 2020 to 2027. Source: E-commerce Market Share, Growth & Trends Report

Balance Sheet

As of June 30, 2023, VSE Corporation reported $4 million in cash, $114 million in receivables, and inventories worth $427 million. The current ratio is larger than 1x, so I do not see any liquidity crisis in the coming months. The asset/liability ratio is also larger than 1x, so I would say that the balance sheet appears solid.

Source: 10-Q

The total amount of debt is not small, which may explain why management decided to execute certain divestitures. With short-term debt close to $10 million and long-term debt of $365 million, total liabilities stood at $604 million.

Source: 10-Q

I did study a bit the recent decline in the financial debt/EBITDA levels, which currently stands at close to 3x, but it was 6x in 2021. The decline in financial debt appears beneficial. I think that a further reduction in the total amount of debt or increases in EBITDA will most likely bring demand for the stock.

Source: YCharts

Expectations Of Other Analysts, And My Financial Model

2025 net sales stand at close to $1.025 billion, with 2025 EBITDA of about $143 million, 2025 EBIT close to $113 million, and 2025 net income worth $69 million. Finally, it is worth noting that 2025 free cash flow is expected to be close to $61 million, which represents a significant change as compared to previous financial figures. In my view, growing beneficial expectations about future FCF growth could bring further demand for the stock. My numbers are not far from the numbers delivered by other analysts, so I believe that investors may want to have a look at them.

Source: S&P

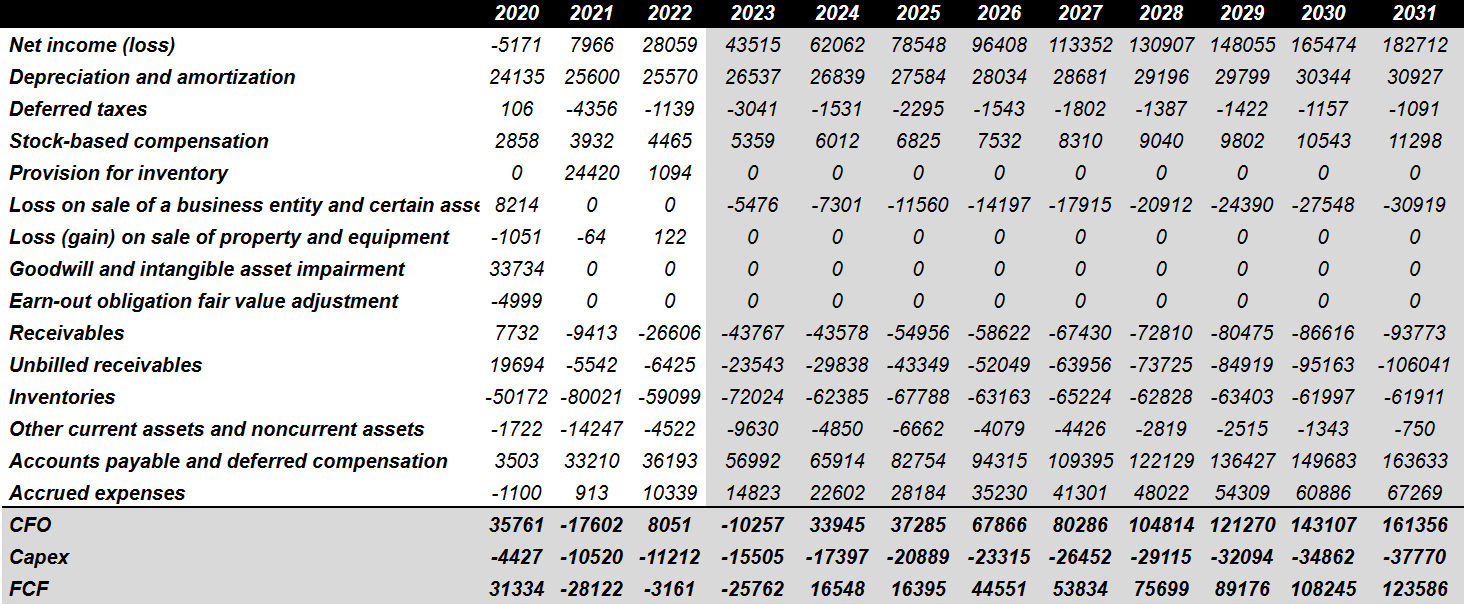

I ran a cash flow model with expectations from 2023 to 2024. My numbers include reasonable net income growth, with positive FCF from 2024. In my view, my numbers are quite conservative and quite in line with previous financial figures and expectations of other market participants.

I assumed 2031 net income close to $18 million, with 2031 depreciation and amortization of about $3 million, deferred taxes of -$1 million, and stock-based compensation of close to $1 million.

I did not include provisions for inventory, loss on sale of a business entity, changes in goodwill, and intangible asset impairments. However, I did assume changes in receivables of -$10 million, with changes in unbilled receivables close to -$11 million, and changes in inventories of -$7 million. Finally, with changes in accounts payable and deferred compensation of $16 million, 2031 CFO would be close to $16 million. I also assumed 2031 FCF of $12 million.

{kind=link}

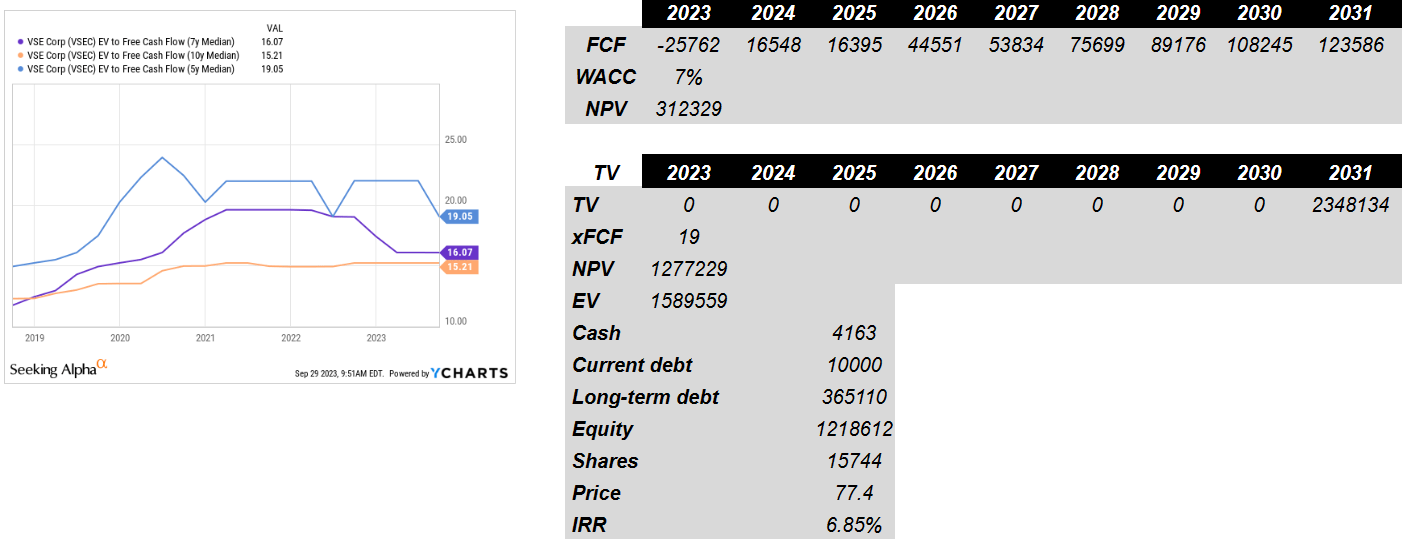

Assuming cost of capital of 7%, net present value of future FCF would be close to $312 million. Previous EV/FCF stood at close to 19x FCF, so I believe that a terminal EV/FCF of 19x would make sense. Now, the implied enterprise value would stand at about $1.58 billion. Adding cash in hand, and subtracting current debt and long-term debt, the implied equity valuation would be $1.2 billion. Finally, we would be talking about a fair price of $77 per share, and the IRR would be close to 6.8%.

{kind=link}

Competitors

In all areas of activity, competition is high, and has participants with greater resources and operational scope. In addition, a series of smaller competitors that offer specific services make up the market environment for VSE Corp. Much of the competition involves government tenders, and depends directly on the allocation they make in this regard. In any case, the signing of a contract of this type does not ensure a flow of activity since its compliance is subject to a large number of factors. It implies that the company has no certainty about its activity in the future.

Risks

In addition to the series of risks arising from competitive factors, the company is currently affected by global economic uncertainty, specifically the logistics and transportation activity. Along with this, some programs it maintains with the federal government concentrate a large amount of the company's revenue, and in view of the next elections, these contracts will be subject to review with the possibility of unilateral termination by the institutions.

On the other hand, the acquisition strategy implies a series of risks in the integration of businesses, particularly in the cases of companies in the aeronautical sector, whose activity makes up a large part of VSE's income and operations.

In July 2023, the company announced a new sale of equity at $48.5 per share. I believe that without new divestitures, shareholders may suffer from time to time equity dilution, which may lead to stock price decreases. I am not really concerned about these risks because VSE works with large clients, and runs an innovative business model.

In July 2023, we entered into an underwriting agreement with William Blair & Company, L.L.C and RBC Capital Markets, acting as representatives of several underwriters, relating to the issuance and sale of 2,475,000 shares of the Company's common stock at a public offering price of $48.50 per share. Source: 10-Q

Conclusion

VSE Corporation continues to deliver increases in the activities within electronic commerce and the contracting of logistics services, which may bring further net sales growth in the coming months. Besides, the company appears to be making acquisitions in growing industries, like aerospace, as well as making some divestitures. Even taking into account risks from the total amount of debt, equity dilution, or failed M&A integration, I think that VSE appears undervalued. Like other analysts, I am expecting that positive FCF may show up in 2024 and 2025, which may bring back stock demand.

For further details see:

VSE Corporation: Divestitures, Electronic Commerce Could Enhance The Stock Price