VTIP - VTIP: 2.6% Real Yield Is Exceptional Given The Alternatives

2023-06-22 11:07:35 ET

Summary

- The real yield on the Vanguard Short-Term Inflation-Protected Securities Index Fund ETF has risen to a new high of 2.6%.

- This real yield is significantly above its historical average and compares favorably even with much riskier assets.

- A huge Federal Reserve policy error would be required to cause negative returns on the VTIP ETF over the coming years.

The deeply inverted US bond yield curve suggests short-term bonds are highly attractive on a relative basis, and with the real yield on the Vanguard Short-Term Inflation-Protected Securities Index Fund ETF ( VTIP ) at 2.6% the risk-reward outlook is extremely strong. It would take huge Fed error to cause negative returns over the coming years.

The VTIP ETF

The VTIP tracks the performance of US Treasury Inflation-Protected Securities with less than 5 years remaining to maturity and has an average effective maturity of 2.7 years. The real yield to maturity now sits at 2.6%, meaning that investors should expect to receive 2.6% per year over the next few years in addition to the average rate of CPI over this period. The VTIP is ideal for investors looking to take advantage of high short-term yields while also protecting against continued elevated inflation. Despite the ETF rising 1.5% since I last covered it in February (see ' VTIP: High Yield With Minimal Risk '), the yield has risen a further 0.7%, making the risk-reward outlook even stronger.

2.6% Real Yield In Context

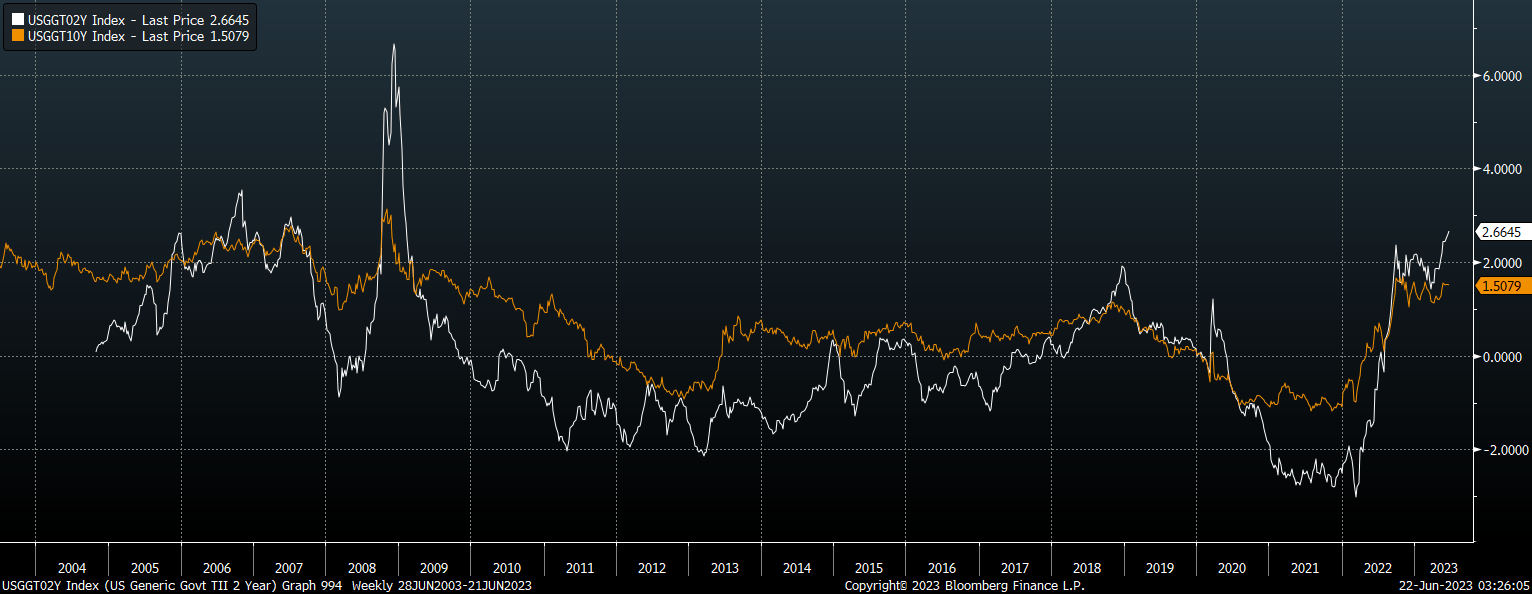

The 2.6% real yield on offer on the VTIP is a long way above its historical average. The chart below shows the yield on the 2-year US inflation-linked bond. At 2.7% it is now 250bps above its average going back to 2004. Yields were only materially higher at the height of the Global Financial Crisis, when a huge credit crunch caused a crash in inflation expectations and a collapse in demand for inflation protection. The VTIP's yield compares to a yield of around 1-2% on longer-dated TIPS. The iShares TIPS Bond ETF ( TIP ) for instance, which has an average maturity of 7.3 years, yields 1.8% in real terms, reflecting the extreme inversion of the yield curve.

{kind=link}

The yield is also attractive relative to other bond funds. The yield on US investment grade corporate bond yields is now just 5.4%, 2.8pp above the yield on 2-year TIPS. If we adjust this corporate yield for long-term inflation expectations, it falls to just 3.2% meaning that investors receive just 50bps for the added duration risk and default risk of corporate bonds relative to the VTIP.

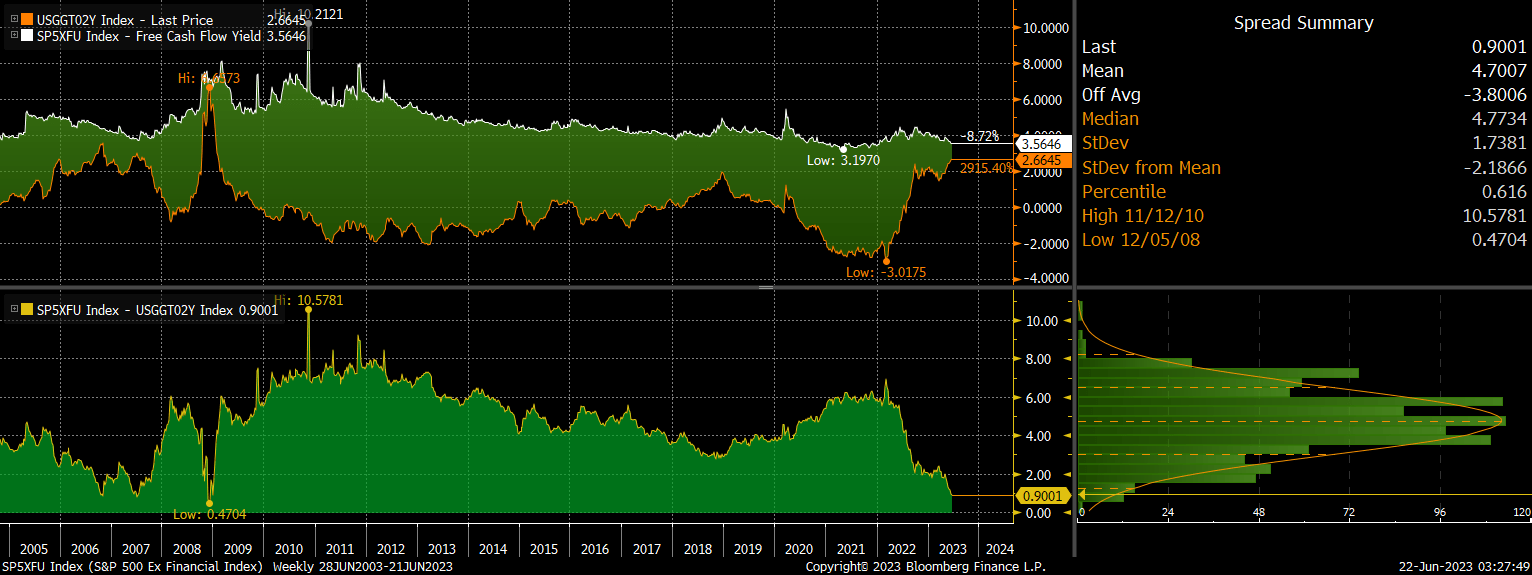

2.6% real returns are also high in the context of expected equity market returns. It is now just 90bps below the free cash flow yield on the S&P500 ex-financials, which is its lowest level since the height of the global financial crisis. With a dividend payout ratio of around 40%, this means that the VTIP yields more in real terms than the S&P500 at a time when real earnings and cash flows are contracting on an annual basis, and leading indicators of the economy point to a further slowdown in sales growth.

US 2-Year TIP Yield Vs SPX Ex Financial FCF Yield (Bloomberg)

{kind=link}

The 2.6% yield on the VTIP ETF is particularly attractive when looked at in terms of downside risks. The table below shows the yield to maturity on the VTIP relative to the yield to maturity on the TIP ETF, the real yield on corporate bonds, as well as the free cash flow yield on the S&P500, alongside their maximum losses seen over the past 20 years. Also shown is the current percentile of yields over this period. Note that the yield on the S&P500 is not adjusted for inflation expectations as free cash flows should rise in line with inflation, unlike bond coupon payments. The table speaks for itself in terms of the VTIP's risk-reward outlook. The yield on 2-year TIPS is now in the 4th percentile of observations over the past two decades and has seen a maximum drawdown of just 8% over this period.

| Current Real Yield |

| Yield Percentile |

| Max Drawdown |

| High Yield Bonds |

| 6.4% |

| 20th |

| -35% |

| Corporate Bonds |

| 3.2% |

| 19th |

| -22% |

| SPX Ex-Financials |

| 3.6% |

| 95th |

| -57% |

| TIP |

| 1.8% |

| 26th |

| -17% |

| VTIP |

| 2.6% |

| 4th |

| -8% |

Only A Huge Fed Error Would Cause Negative Returns

In order to see another 8% decline in the VTIP the real yield would have to rise significantly from here. With a duration of 2.5 years, an 8% decline would require real yields rising to around 6%. While we cannot rule out such a move, it would require a significant policy error by the Fed as they would have to keep rates elevated despite a collapse in inflation. If such a scenario were to play out, the VTIP would likely significantly outperform all other real assets.

For further details see:

VTIP: 2.6% Real Yield Is Exceptional Given The Alternatives