VTIP - VTIP: Losing To Inflation In The Long Run

2023-09-20 01:43:43 ET

Summary

- The Vanguard Short-Term Inflation-Protected Securities ETF invests in short-duration TIPS bonds.

- Although VTIP pays an attractive 5.1% yield, the ETF has underperformed CPI inflation since its inception.

- Investors interested in true inflation protection should consider constructing a ladder of individual TIPS bonds matched against their specific maturity needs.

Readers who follow my writings will note that I am cautious on long-term interest rates, as I believe there are a number of technical and fundamental reasons why long-term interest rates may continue to rise. In light of my stance, a reader recently asked whether I would recommend an investment in the Vanguard ShortTerm Inflation-Protected Securities ETF ( VTIP ), as it is a short-duration fund that also protects against inflation.

While the VTIP ETF's 5.1% trailing distribution yield looks attractive, I am concerned that the VTIP ETF has a poor track record of beating CPI inflation, as it has delivered 16.9% compounded return since inception compared to 32.7% for CPI.

So while in the short-run, I prefer the VTIP ETF compared to other long-duration TIPS fund, I would not recommend the VTIP ETF as a long-term buy-and-hold asset.

Fund Overview

The Vanguard Short-Term Inflation-Protected Securities ETF provides investors with a straightforward, low-cost way to gain exposure to a basket of short-duration inflation-protected U.S. Treasury securities. VTIP is a popular ETF with almost $53 billion in assets across various classes and charges an ultra-low 0.04% expense ratio.

Strategy

The VTIP ETF achieves its investment objective by tracking the investment returns of the Bloomberg U.S. 0-5 Year Treasury Inflation-Protected Securities Index (“Index”), an index of short-term Treasury Inflation-Protected Securities ("TIPS").

TIPS are bonds issued by the U.S. Treasury that protect investors against inflation. TIPS achieve this by adjusting the principal of the bond higher for inflation (or lower for deflation), as measured by the Consumer Price Index ("CPI"). When a TIPS bond matures, investors receive the greater of the adjusted principal amount or their original principal.

TIPS pay bi-annual interest that is calculated on the adjusted principal, so when inflation increases, interest payments increase as well.

By investing in a portfolio of short-term TIPS, the VTIP ETF is designed to generate returns that are correlated to realized inflation over the near-term while having less interest rate (duration) risk compared to longer-duration TIPS funds.

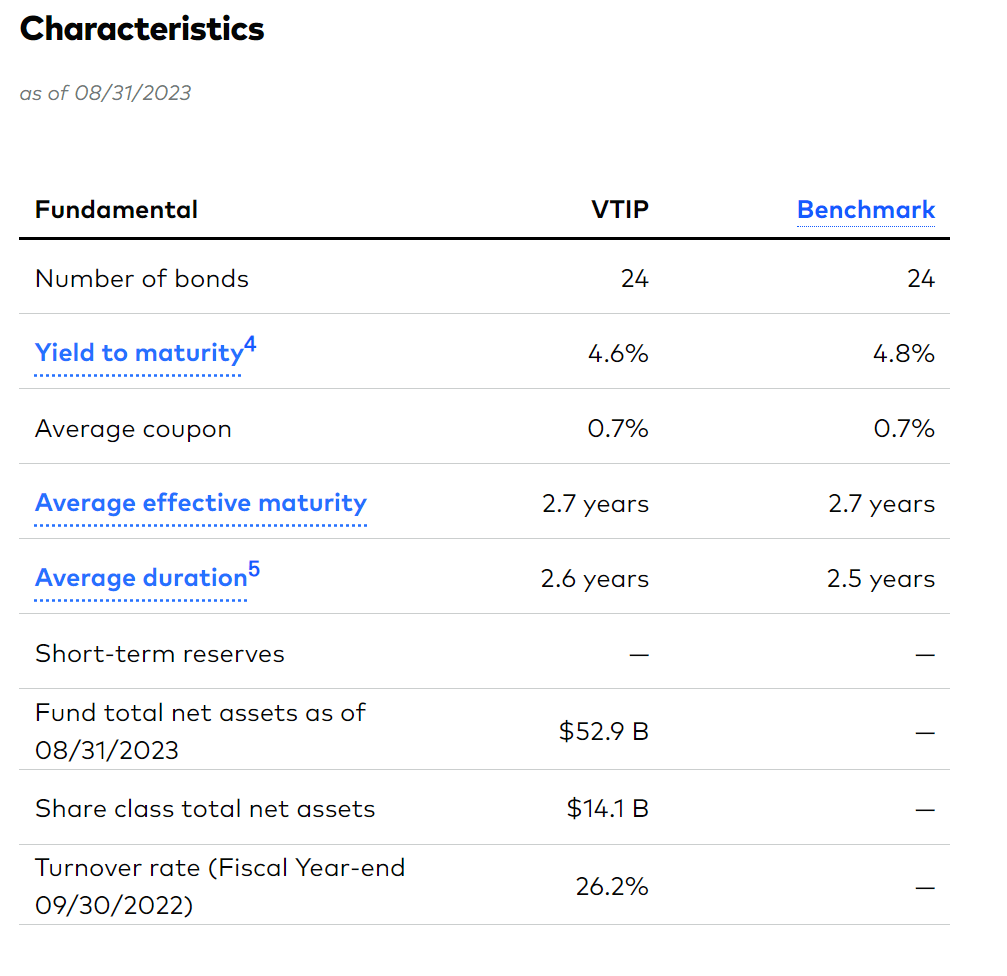

Portfolio Holdings

The portfolio of the VTIP ETF currently holds 24 TIPS bonds of varying maturities and coupons. Overall, the portfolio has an average duration of 2.6 years and a yield to maturity of 4.6% (Figure 1).

{kind=link}

Figure 1 - VTIP portfolio overview (vanguard.com)

Distribution & Yield

The VTIP ETF pays a trailing 12 month distribution yield of 5.1% (Figure 2). VTIP's distribution is paid quarterly.

{kind=link}

Figure 2 - VTIP pays an attractive quarterly distribution (Seeking Alpha)

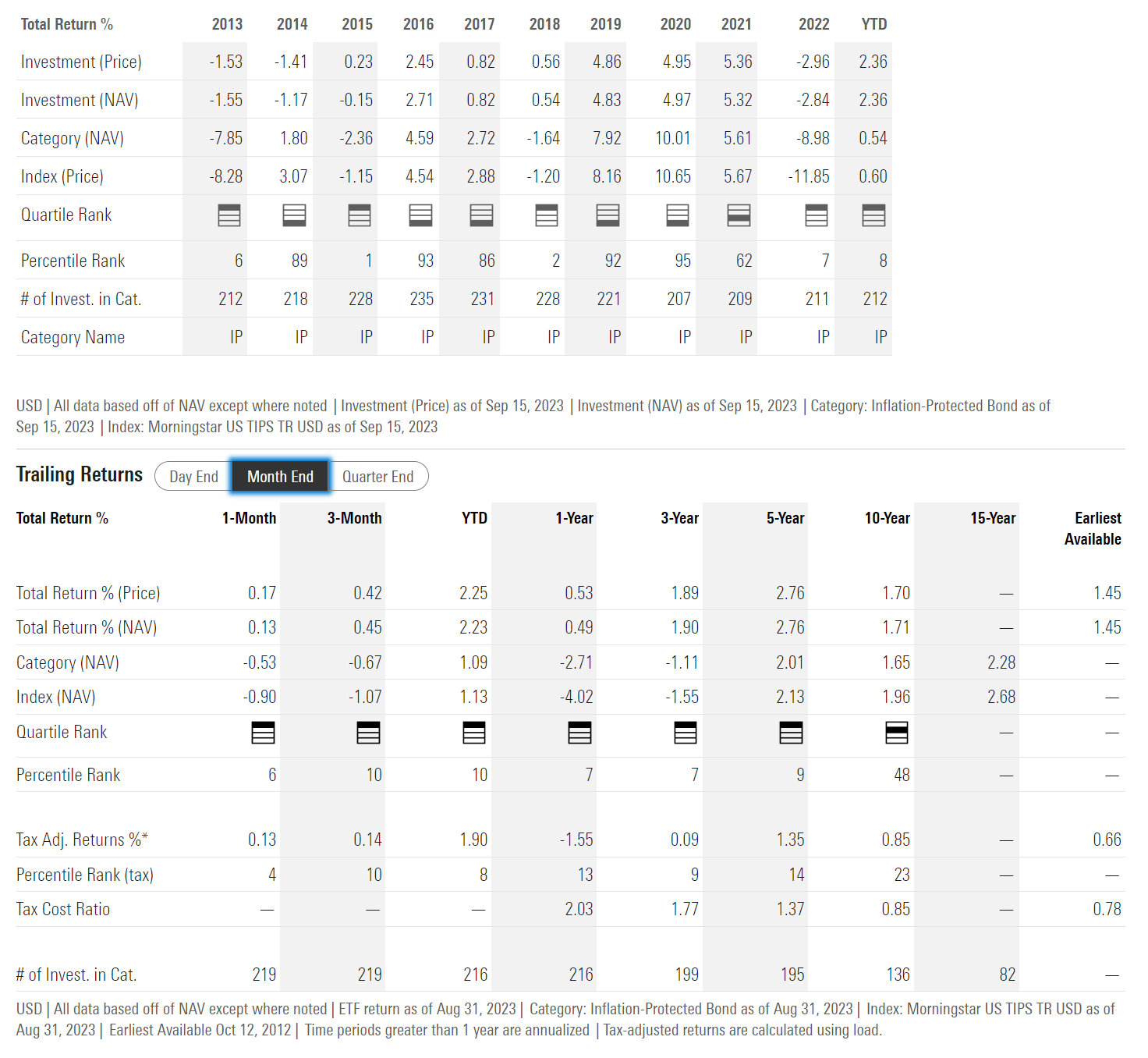

Returns

Overall, the VTIP ETF has delivered modest historical returns, with 3/5/10Yr average annual returns of 1.9%/2.8%/1.7% respectively to August 31, 2023 (Figure 3).

{kind=link}

Figure 3 - VTIP historical returns (morningstar.com)

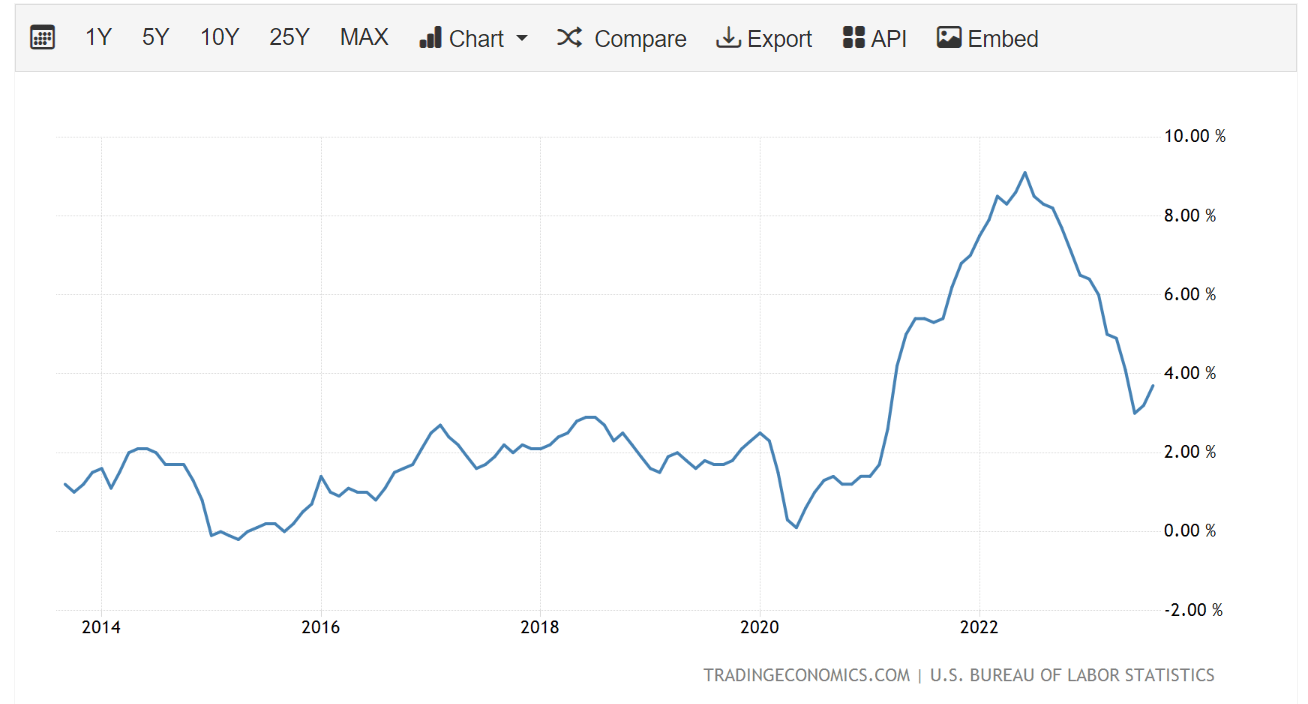

The VTIP ETF was notably weak in 2022, when it returned -2.8% while inflation soared to over 9% YoY (Figure 4).

{kind=link}

Figure 4 - VTIP failed to protect against inflation in 2022 (tradingeconomics.com)

VTIP's poor 2022 relative performance was primarily driven by its duration exposure. Even though the fund is marketed as a short-duration fund, it still had a 2.6 year average duration, so when the Federal Reserve raised short-term interest rates aggressively in 2022 to combat inflation, the VTIP ETF suffered a relatively large drawdown in 2022.

Does VTIP Truly Protect Against Inflation?

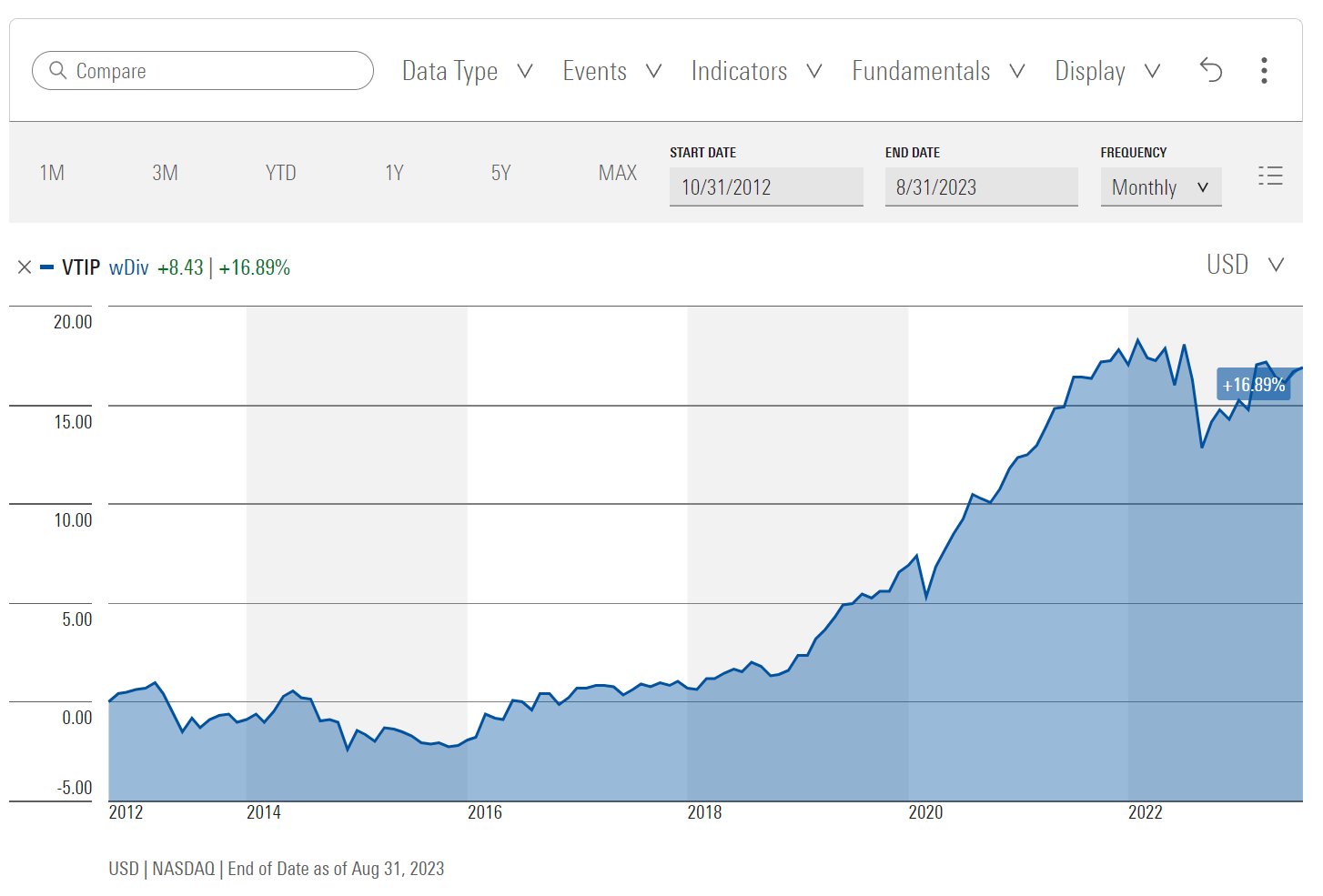

However, VTIP's poor 2022 performance this brings up an important discussion topic. Does the VTIP ETF really protect investors against inflation?

The VTIP ETF was incepted in October 2012, and since October 31, 2012, the VTIP ETF has delivered total compounded returns of 16.9% to August 31, 2023 (Figure 5).

{kind=link}

Figure 5 - VTIP has delivered 16.9% compounded returns since inception (morningstar.com)

This performance has significantly lagged CPI inflation, which has increased 32.7% as measured from October 2012 to August 2023 (Figure 6).

{kind=link}

Figure 6 - VTIP has lagged CPI, which increased 32.7% from October 2012 to August 2023 (BLS Inflation Calculator)

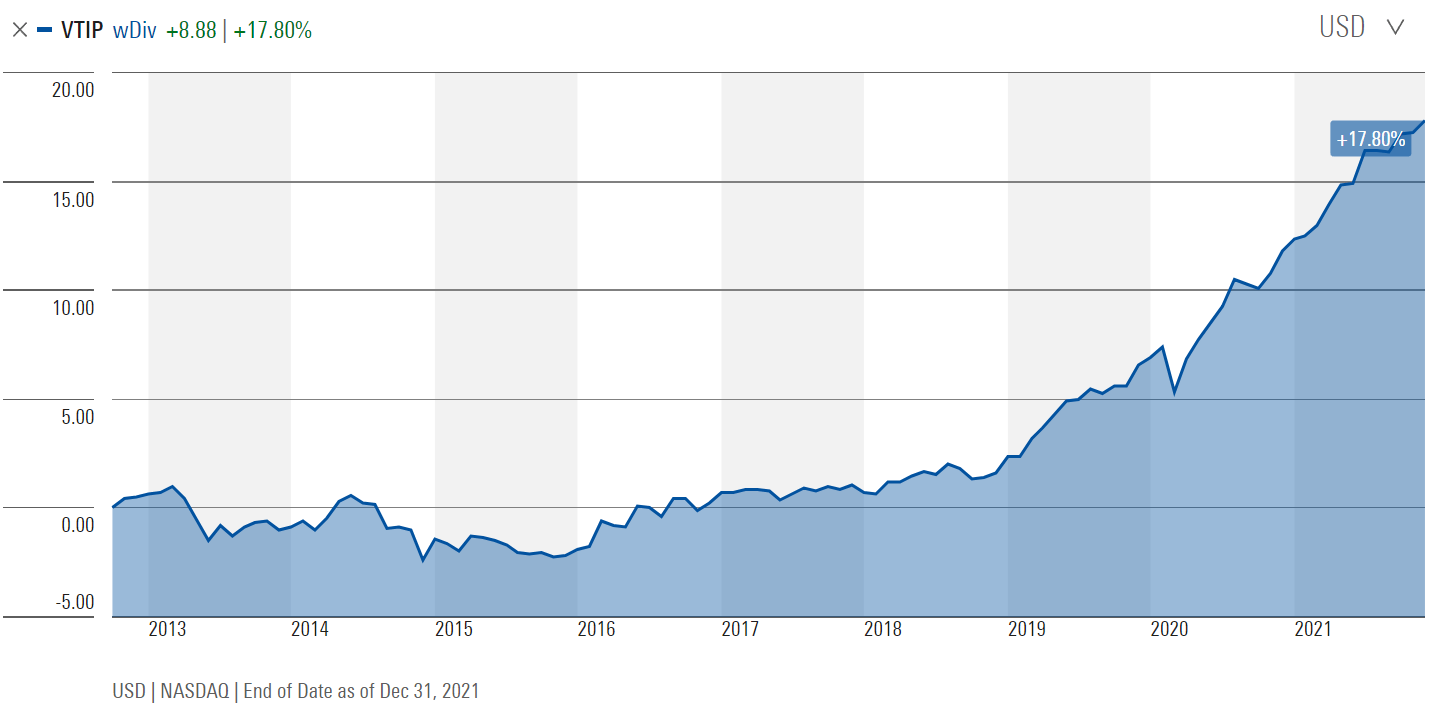

Even if we ignore the 'extraordinary' inflation period since 2022, the VTIP ETF only returned a compounded 17.8% from October 2012 to December 2021 compared to CPI inflation which increased by 20.5% (Figure 7 and 8).

{kind=link}

Figure 7 - VTIP delivered 17.8% return from October 2012 to December 2021 (morningstar.com)

{kind=link}

Figure 8 - While CPI increased by 20.5% from October 2012 to December 2021 (BLS Inflation Calculator)

So there are legitimate concerns as to whether the VTIP ETF delivers returns that are sufficient to offset realized CPI inflation.

While an individual investor who buys a single TIPS bond and hold it to maturity will indeed obtain protection against CPI inflation for the time the bond is held (via principal and interest payment adjustments), the same cannot be said of a portfolio of TIPs bonds like the VTIP ETF.

The main issue is that the VTIP ETF maintains a relatively fixed portfolio duration, which means that it must trade in and out of different TIPS bonds (26% portfolio turnover), crystalizing mark-to-market ("MTM") losses in the process, especially during rising interest rate environments like 2022.

Investors who want true inflation protection should consider constructing a bond ladder of TIPS bond matched against their specific maturity needs. By holding individual TIPS bonds to maturity, investors will receive the adjusted principal and MTM fluctuations from duration will not matter.

However, there are 2 drawbacks to a TIPS bond ladder. First, if the bond ladder is a rolling ladder (maturing bonds used to acquire new bonds at the end of the ladder), then it more or less is the same as a bond fund. Second, prior to maturity, individual TIPS bonds can fluctuate in price according to prevailing interest rates, so if investors have liquidity needs beyond the maturing bond principal, they may have to sell their TIPS bonds at inopportune times.

Investors interested in TIPS bond ladders should be interested in the writings of Boston University Professor, Zvi Bodie.

Conclusion

The VTIP ETF invests in a portfolio of short-duration TIPS securities that provide some level of inflation protection to investors. Although the VTIP ETF outperformed long-duration TIPS funds like the iShares TIPS Bond ETF ( TIP ) in 2022, it still massively underperformed CPI inflation. In fact, when measured since the fund's inception, the VTIP ETF has significantly lagged CPI inflation, delivering total returns of 16.9% compared to 32.7% for CPI.

While current unitholders may enjoy VTIP's 5.1% trailing distribution yield, long-term investors are cautioned that the VTIP ETF does not truly protect one's capital against the ravages of inflation. I rate the VTIP ETF a hold .

For further details see:

VTIP: Losing To Inflation In The Long Run