STIP - VTIP: Real Yields Rise From The ZIRP Ashes

2023-12-05 06:04:57 ET

Summary

- Treasury Inflation Protection Securities pay a real interest rate and have semi-annual adjustments to the principal based on the Consumer Price Index.

- Vanguard Short-Term Inflation-Protected Securities ETF aims to track the performance of TIPS maturing in under 5 years.

- We analyze the setup and tell you why we think this deserves a position in your portfolio.

The run-of-the-mill treasury bonds issued by the U.S. government pay nominal interest. This means the yield on them is comprised of two parts, a real yield, plus the little somethin' somethin' that theoretically compensates the buyer for inflation. This extra bit is extrapolated at the time of the security issuance based on market expectations (it's complicated!). While the yield to maturity of the security varies based on its market price during its lifetime, the periodic coupon payments remain static. On the maturity date, the government returns the original principal back to the bondholder, along with the last coupon payment and both go their separate ways. In between, there is a fair bit of laughter and tears, including happy tears and nervous laughter, but that is not the topic of today's piece.

In this piece, we will talk about a sibling of the vanilla bonds, that goes by the name of Treasury Inflation Protection Security [TIPS]. While the treasury bond has a nominal interest rate set at its issuance, TIPS start off paying just the real interest rate. The inflation protection comes in the form of semi-annual adjustments to the principal based on the results of the Consumer Price Index [CPI]. So if the CPI comes in hotter, the coupon rate is applied to a higher principal amount and vice versa. The principal repaid at maturity is the higher of the original and the adjusted amount. So, the least an investor can recoup is the original face value of the security. The tax liability on these is explained well by the original seller of these securities.

Earnings from TIPS are exempt from state and local income taxes, as are other U.S. Treasury securities. TIPS owners pay federal income tax on interest payments the same year they receive those payments, and on growth in principal in the year it occurs.

Source: www.treasurydirect.gov

Investors tend to hold these securities in tax-exempt accounts, but we will leave the tax implication due diligence on that, to you. What we will do instead, is move on to the protagonist du jour, an exchange-traded fund that caters to investors interested in TIPS.

The Fund

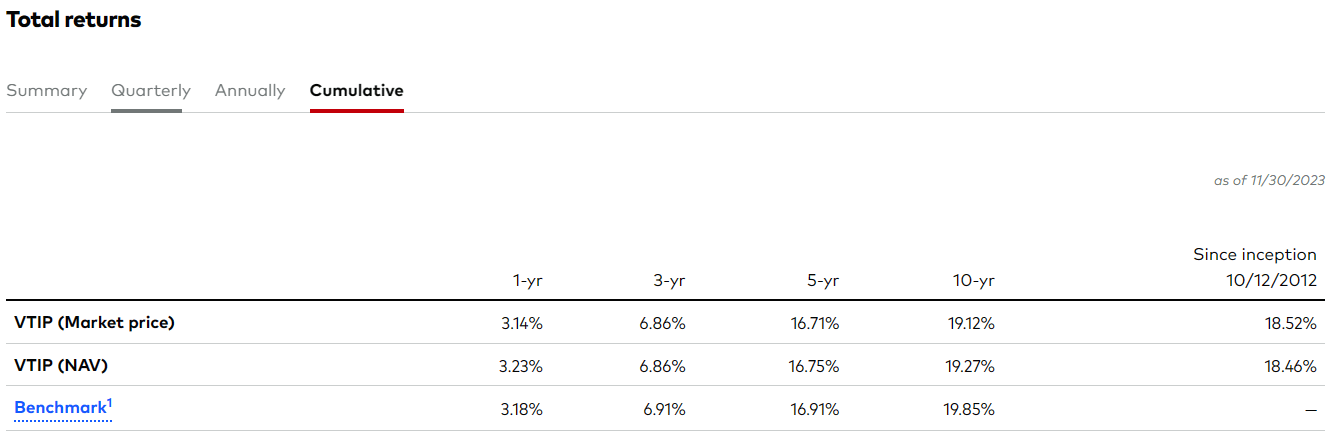

Vanguard Short-Term Inflation-Protected Securities ETF ( VTIP ) aims to pursue the performance of the Bloomberg U.S. 0-5 Year Treasury Inflation-Protected Securities. As its name suggests, the index comprises TIPS maturing in under 5 years. VTIP has an annual expense ratio of 0.04% and that is pretty much the difference between its performance and that of its benchmark index (the index does not have any expenses). Note that the returns shown below are cumulative, not annualized.

{kind=link}

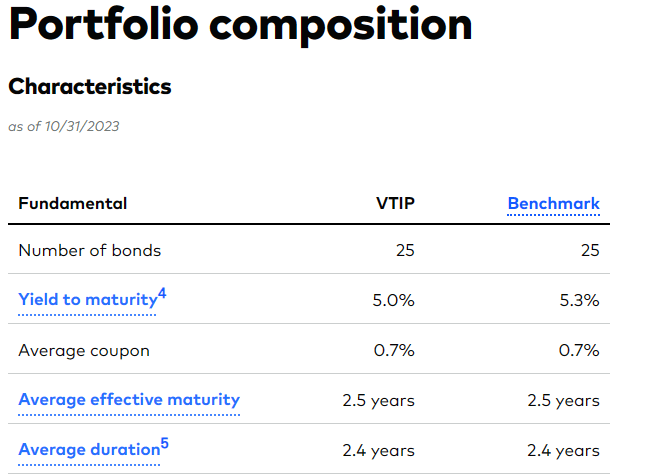

The ETF's investment methodology consists of investing all or majority of its assets in the components of the index, and in around the same proportion too. We can see this replication in action in the most current data published on the fund website.

{kind=link}

TIPS face duration risk just like other fixed-income securities and the rate hikes over the last couple of years, made the duration risk a reality.

The fund had around a 10% decline in price during this time frame in response to approximately a 400 basis points increase in the real rates. This is in line with the 2.4 years of average duration of the VTIP portfolio. For the uninitiated, what duration risk signifies is that with every 100 basis points increase in rates, the value of the VTIP portfolio will drop by 2.4%, and vice versa. At this stage of the cycle, we consider VTIP's duration risk very modest. This is despite believing that the Federal Reserve is not done with the rate hikes as yet. Another noteworthy item under the portfolio composition shown above is the 5.0% yield to maturity of the portfolio. This is indicative of the real rate plus current inflation expectations of the market.

Distributions

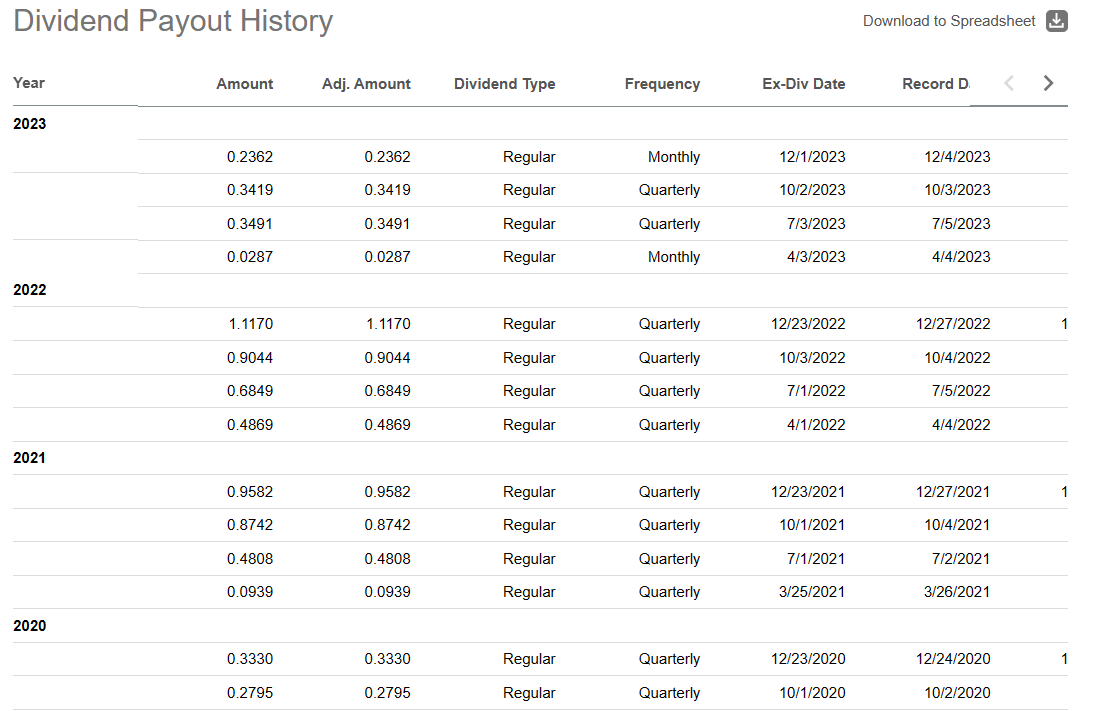

When an investor directly purchases TIPS, they receive interest on a semi-annual basis. VTIP and similar ETF on the other hand, pay distributions based on income earned plus/minus the CPI-linked principal adjustments. So there is no fixed number of distribution dates during the year. Investors have been paid quarterly over the last three years, and as we can see in 2020, only two payments were made.

{kind=link}

From 2012 to 2017, only one distribution payment was made per year. To extrapolate the number of payments or the forward yield of funds holding these securities would be akin to figuring out how many angels fit on a pin, so we will avoid the exercise. VTIP explains the reason for the income fluctuations in its summary prospectus .

The Fund's quarterly income distributions are likely to fluctuate considerably more than the income distributions of a typical bond fund. In fact, under certain conditions, the Fund may not have any income to distribute. Income fluctuations associated with changes in interest rates are expected to be low; however, income fluctuations associated with changes in inflation are expected to be high. Overall, investors can expect income fluctuations to be high for the Fund.

Outlook & Verdict

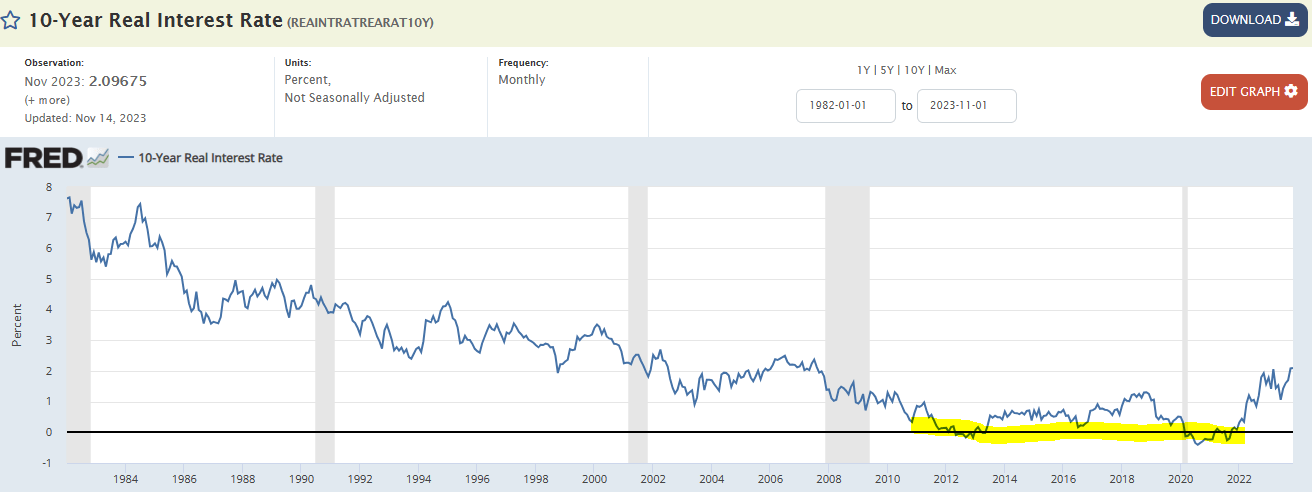

After a period of horrendous pricing, real interest rates have risen from the ashes. We have shown the 10-year real rates below but you can see this jump across the entire curve.

{kind=link}

It is very hard here not to at least allocate some capital towards TIPS. While a 2.0%-2.5% real yield may not mean that much to investors used to chasing bubbles sky-high, it means a lot to us from a capital preservation standpoint. This real yield also stands on guard if inflation turns out to be stickier than what the Treasury bulls have been calling for. The time to buy these securities is when they are forgotten and everyone believes that the inflation problem has been solved. That appears to be now. VTIP is also very friendly for the investor who is looking to get into this space, without the beta of longer duration TIPS funds like iShares TIPS ETF ( TIP ).

While real yields could rise, we would celebrate that by adding more of such funds rather than worrying we were early. We rate VTIP a buy here. It gives us ample protection against inflation and we think it likely does ok eventually, even in a deflationary shock. We currently have a small position in TIP but will likely add VTIP down the line.

For further details see:

VTIP: Real Yields Rise From The ZIRP Ashes