CMP - Vulcan Materials Offers Long-Term Upside Despite Being Pricey

2023-07-28 12:33:54 ET

Summary

- Vulcan Materials Company is a "boring" but interesting company that provides aggregates and construction materials.

- The company has achieved attractive growth in recent years and operates in a highly fragmented industry with the potential for continued growth through acquisitions.

- Despite concerns about lower tons shipped in the first quarter of 2023, management is optimistic about the future and forecasts solid profits and cash flows for the year.

- Shares are pricey, but the catalysts propelling it should justify this lofty price.

Perhaps I'm an oddball, but I have always found some of the most "boring" types of companies out there to be the most interesting to analyze and, when possible from a valuation perspective, purchase. Unlike the "exciting" businesses that permeate the headlines, the "boring" companies tend to fly under the radar and, as a result, are sometimes overlooked.

One high quality company that fits the "boring" designation that investors should at least be aware of, in large part because of the catalyst that it has, is Vulcan Materials Company ( VMC ), a provider of aggregates and other construction materials. In recent years, management has achieved attractive growth for the business, and that growth looks set to continue in the near term. Shares of the business are most certainly not cheap. But when you consider the catalyst propelling it forward, I would argue that a soft "buy" rating is appropriate at this time.

Great results in recent years

According to the management team at Vulcan Materials, the firm operates as the largest supplier of construction aggregates in the U.S. For those who don't know, construction aggregates are basically crushed stone, sand, and gravel. Even though these may not seem like materials that have the potential to generate attractive returns because they are seemingly everywhere, they are actually very important when it comes to various construction activities. For instance, they can be used as a base material beneath highways, walkways, airport runways, parking lots, and even railroads. They can be used to assist in water filtration, purification, and erosion control. They can also be used in the construction of various structures like homes and apartments, schools, power plants, sewer systems, and more.

{kind=link}

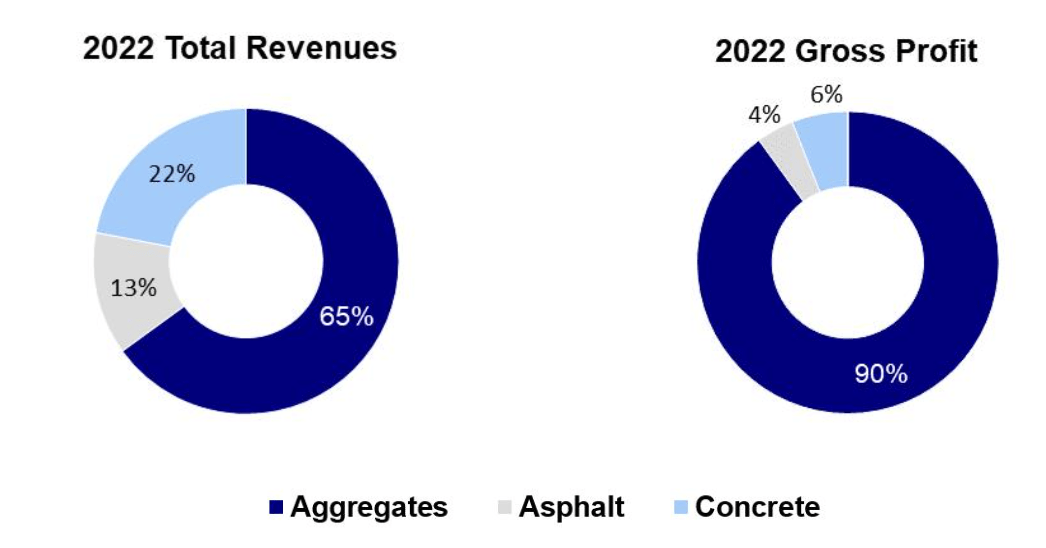

The industry in which the company operates is highly fragmented, with around 5,000 companies managing roughly 10,000 different operations last year alone. This leaves open the opportunity for continued growth by means of acquisition. Of course, the company does offer up other offerings as well. While 65% of its revenue came from aggregates in 2022, 22% of sales came from concrete. The remaining 13% of revenue was attributable to asphalt. Now, when it comes to profitability, the picture is radically different. About 90% of its profits can be chalked up to aggregates. That compares to 6% for concrete and 4% for asphalt.

{kind=link}

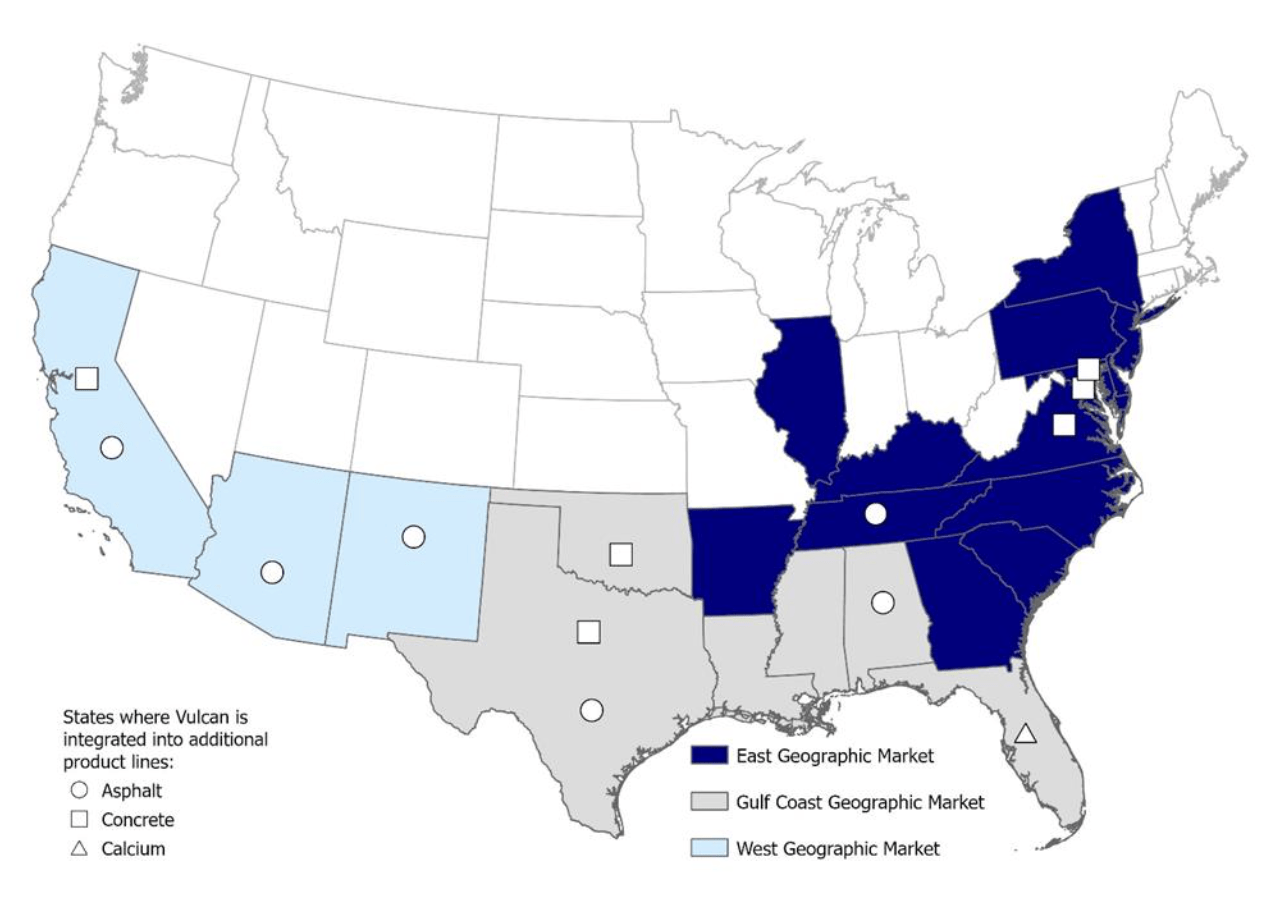

This makes the company a specialist in the aggregate space. Only one other publicly traded enterprise in the U.S. market generates over 50% of its revenue from aggregates. That happens to be Martin Marietta Materials ( MLM ). Most of the other players in the space generate significant sources of revenue from cement or other similar construction products. Of course, in order to become as large as it is, Vulcan Materials must have a massive physical footprint. As of the end of last year, the company had 404 active aggregates facilities, largely centered around the southern and central portions of the nation. These facilities had a combined 15.6 billion tons of proven and probable reserves. In terms of overall land, the firm's footprint is massive as well. Its overall land portfolio has over 240,000 acres in it. This allows the company to sell some of its properties from year to year. In 2022, for instance, the firm generated $23.6 million in revenue from the sale of some real estate in Southern California. But the year prior to that, proceeds from land sales was a far more impressive $182.3 million.

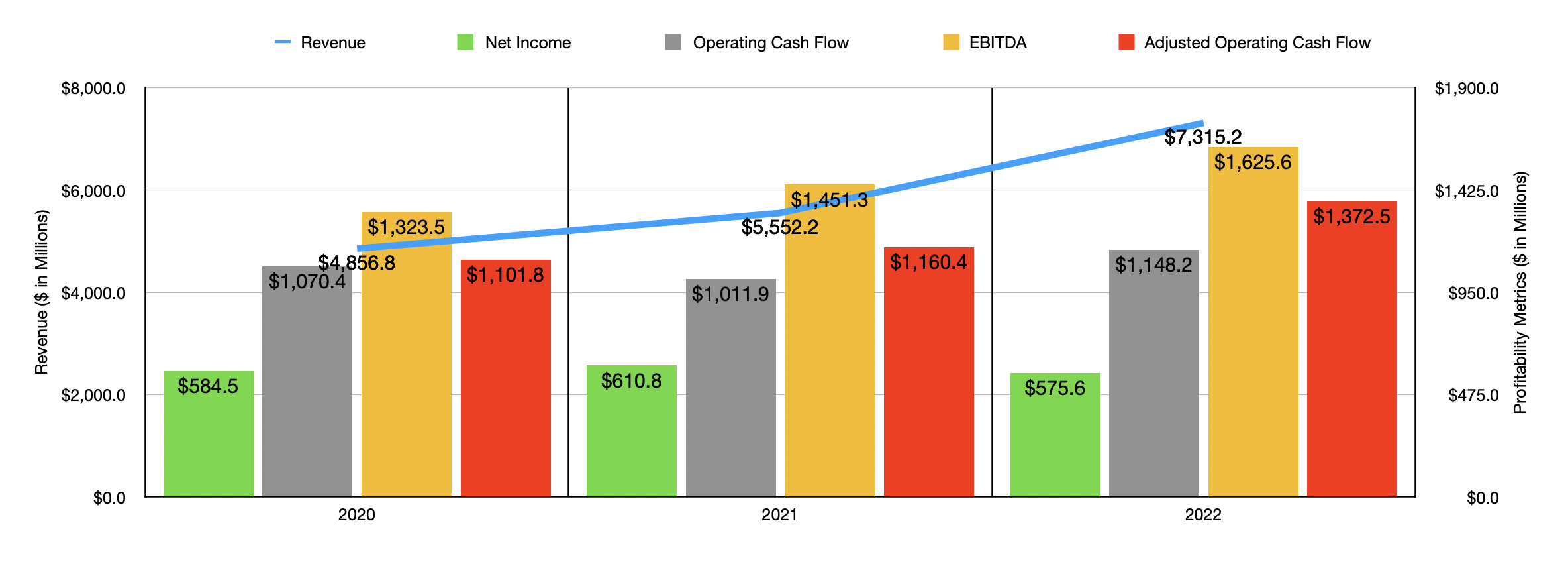

Over the past few years, management has done a fantastic job growing the enterprise. Revenue expanded from $4.86 billion in 2020 to $7.32 billion in 2022. A good portion of this growth came from the company's aggregates production. Overall tons of product shipped jumped from 208.3 million to 236.3 million. Freight adjusted prices per ton also aided the enterprise, with the metric growing from $14.44 to $16.40. A rise in asphalt shipments from 11.8 million tons to 12.2 million tons over that same window of time also occurred. And the business benefited from an increase in the average sales price per ton rising to $71.29 compared to the $57.97 reported two years earlier.

Even more impressive from a shipment perspective was the increase any units of concrete sold. These jumped from 3 million tons to 10.5 million tons. And during this time, the average sales price per ton grew from $128.93 to $150.82. The company does also sell some calcium, but this was not all that material during this window of time.

{kind=link}

With the increase in sales came growing cash flows but mixed profits. As you can see in the chart above, net income for the company has remained in a fairly narrow range over the three years that my analysis covers. However, operating cash flow managed to grow from $1.07 billion to $1.15 billion. If we adjust for changes in working capital, the metric grew consistently from year to year, rising from $1.10 billion to $1.37 billion. And finally, EBITDA for the enterprise managed to climb from $1.32 billion to $1.63 billion.

{kind=link}

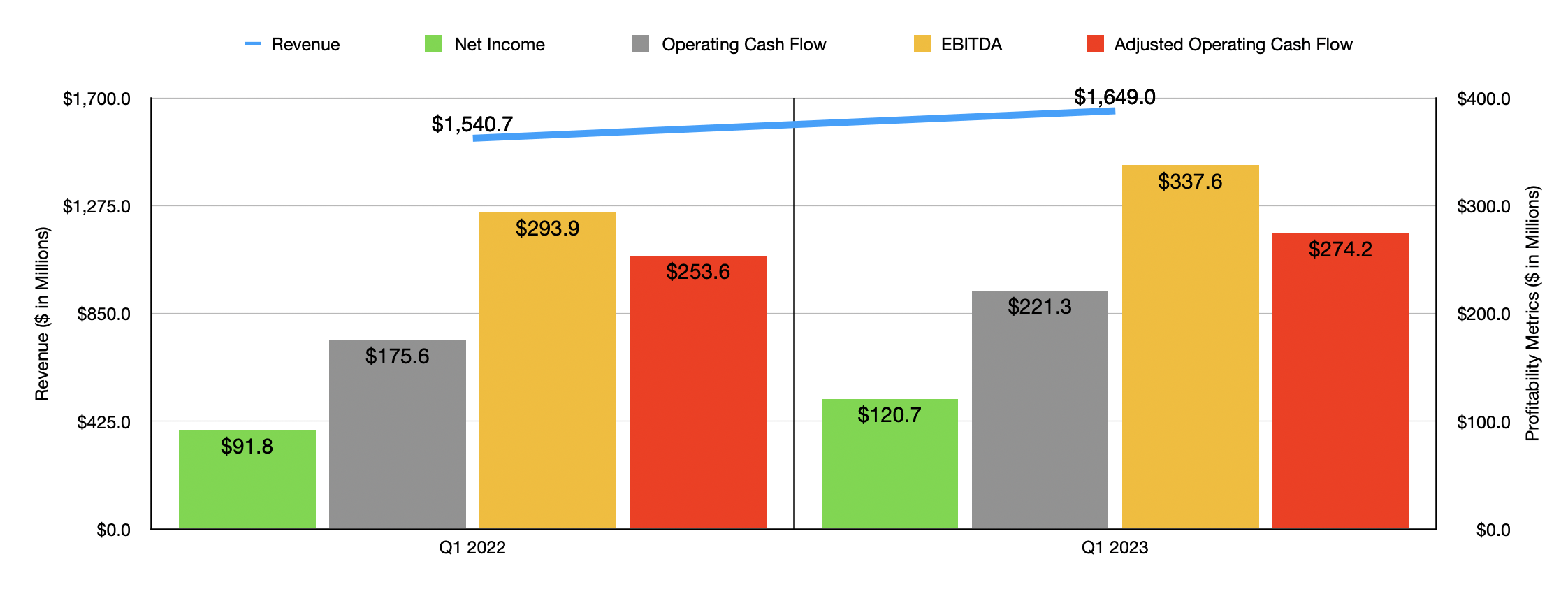

In the chart above, you can see that strong financial performance for the business continued into the 2023 fiscal year. Revenue, profits, and cash flows all rose year-over-year. Interestingly, however, when you dig deeper into the data, you find something you wouldn't necessarily expect. As you can see in the image below, actual tons shipped by the company were lower almost across the board during the first quarter of 2023 compared to the first quarter last year. The only reason why revenue was higher was because of an increase in average sales prices per ton. At first glance, this concerned me.

{kind=link}

My worry was that continued price increases caused by inflationary pressures and the desire to milk as much profit as possible while times are good, may have caused a weakening of demand for the firm’s offerings. Considering the high interest rate environment that we are in right now, and the impact that should have on things like construction, I felt like this fear was justified. However, management stated that the reason for the pain largely centered around inclement weather, with high rainfall in places like California, Texas, and Arizona, negatively impacting demand. This does seem to check out. Unfortunately, I could not find comprehensive rainfall data for each state. But I did find enough data to convince me that management is correct. For the first quarter of 2023, for instance, rainfall in the Dallas/Fort Worth area of Texas was 91.7% higher than it was the same time last year. And in an article published in the middle of March of this year, it was calculated that San Diego experienced more rainfall from the start of January until March 15th than it experienced in all of 2022 combined.

{kind=link}

In spite of these troubles, the management team at Vulcan Materials believes that this year will be a rather solid one. They are forecasting, using midpoint guidance, net profits of $855 million. They believe that EBITDA for the year will come in at around $1.90 billion. This would imply adjusted operating cash flow of roughly $1.60 billion. In the chart above, you can see how this affects the pricing of shares on a forward basis.

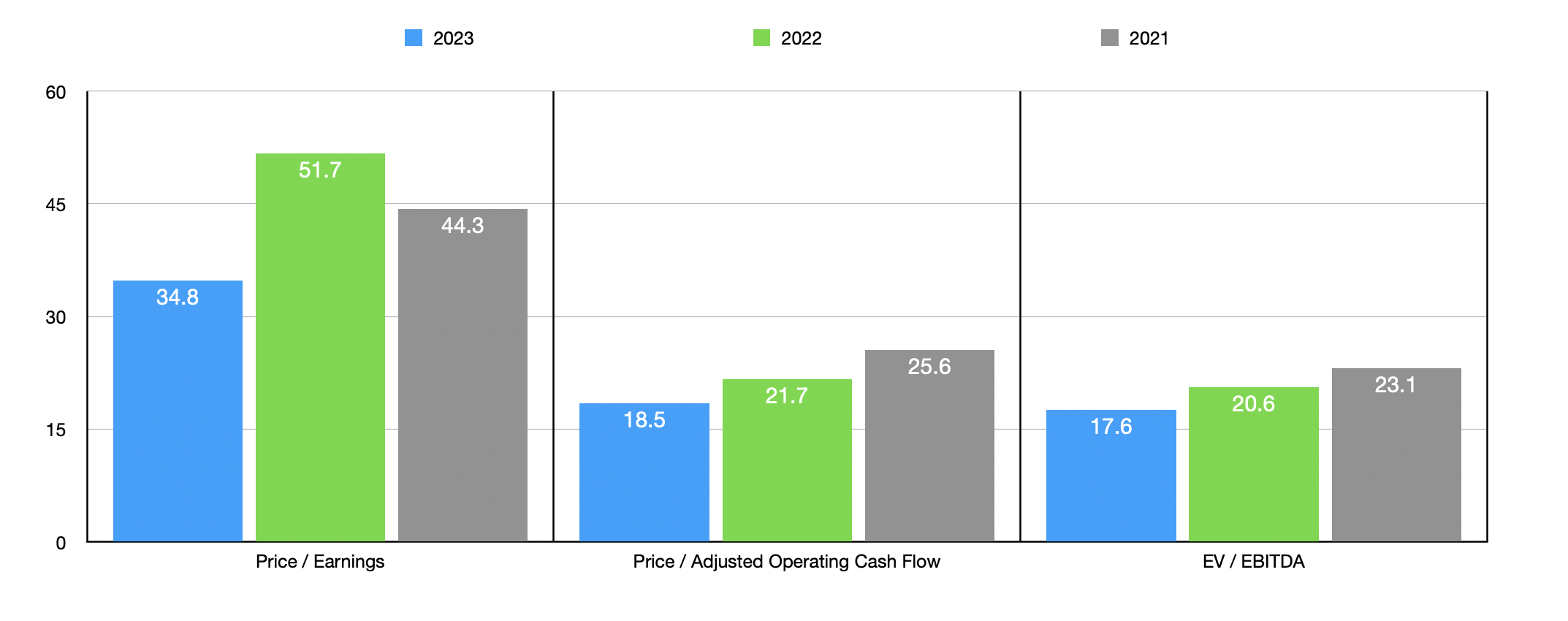

In the table below, meanwhile, you can see how shares are priced compared to similar firms. Even using the forward estimates, the company is more expensive than any of the peers that I listed on both a price to earnings approach and using the EV to EBITDA approach. When it comes to the price to operating cash flow approach, three of the five companies ended up being cheaper than our prospect.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Vulcan Materials Company |

| 34.8 |

| 18.5 |

| 17.6 |

| Martin Marietta Materials |

| 28.7 |

| 28.3 |

| 17.5 |

| Summit Materials ( SUM ) |

| 15.8 |

| 14.4 |

| 8.3 |

| James Hardie Industries ( JHX ) |

| 25.0 |

| 21.1 |

| 14.6 |

| Compass Minerals International ( CMP ) |

| 34.7 |

| 11.8 |

| 10.7 |

| Eagle Materials ( EXP ) |

| 14.7 |

| 12.5 |

| 10.3 |

A look to the future

{kind=link}

Given how shares are priced on both an absolute basis and relative to similar firms, you might think it peculiar that I, a value investor, have rated the company in a bullish light. The reason behind my rating has a lot to do with what the data suggests about the firm's future. The first thing I would like to point to in this regard is the image above. In it, you can see the billions of tons of aggregates consumption that the US has experienced over the past few decades. Consumption peaked somewhere around 2006, which would make a great deal of sense when you consider the housing boom that the country went through at the time. But even though the economy has recovered and surpassed the levels seen since then, we have not staged a full recovery, either when it comes to private construction tons used or public. The overall trend, however, is positive.

{kind=link}

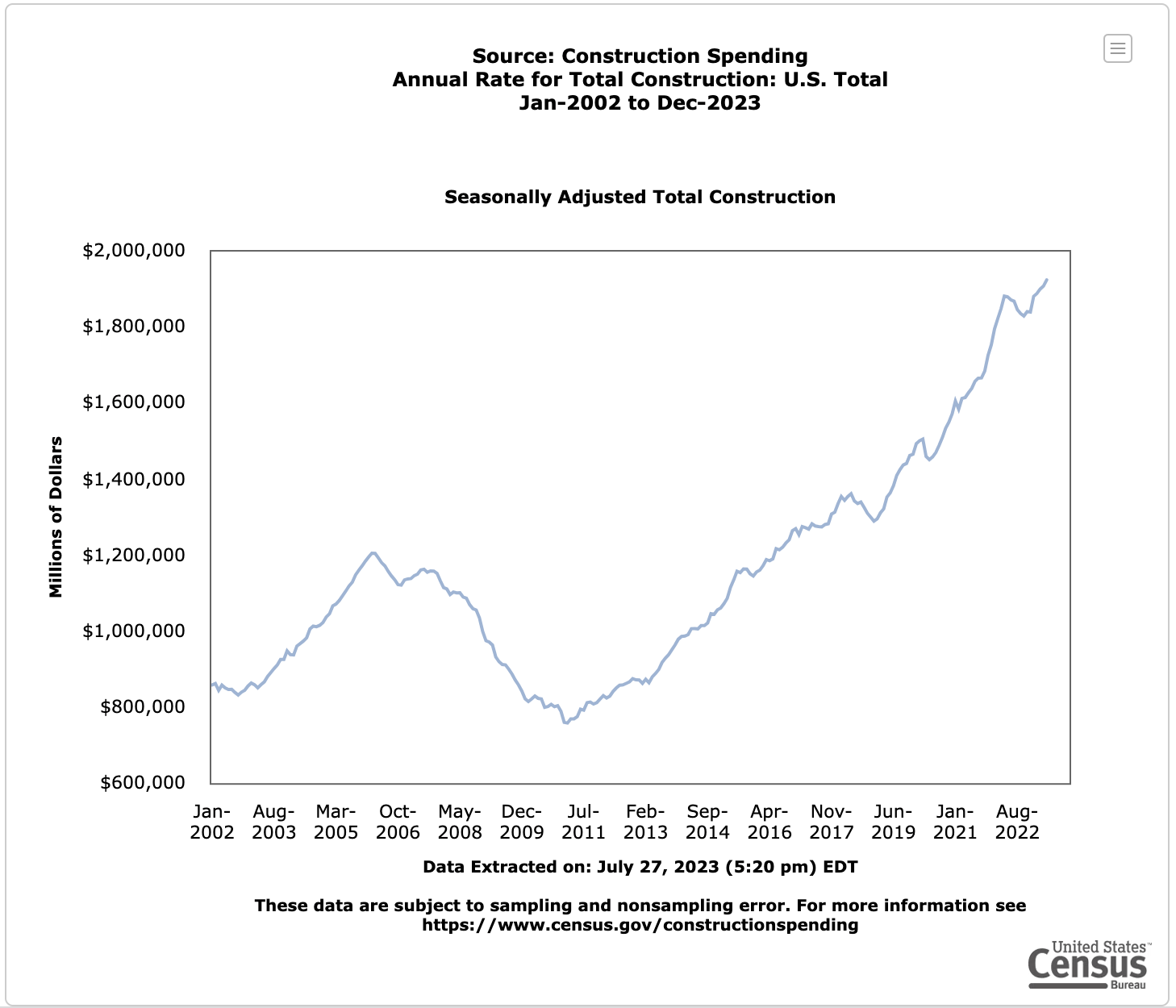

Those who are less bullish than I am might justifiably point out that high inflation and rising interest rates are not exactly conducive to continued construction spending. Normally, I would agree with that assessment wholeheartedly. However, data provided by the US Census Bureau shows that total construction spending, which includes both public and private combined, has not only hit an all-time high, but also continues to show no signs of stopping. Obviously, spending and aggregates consumption don't necessarily align as the two images show. But in general, if spending grows enough, aggregates consumption should climb as well. After all, you can only build so much without it.

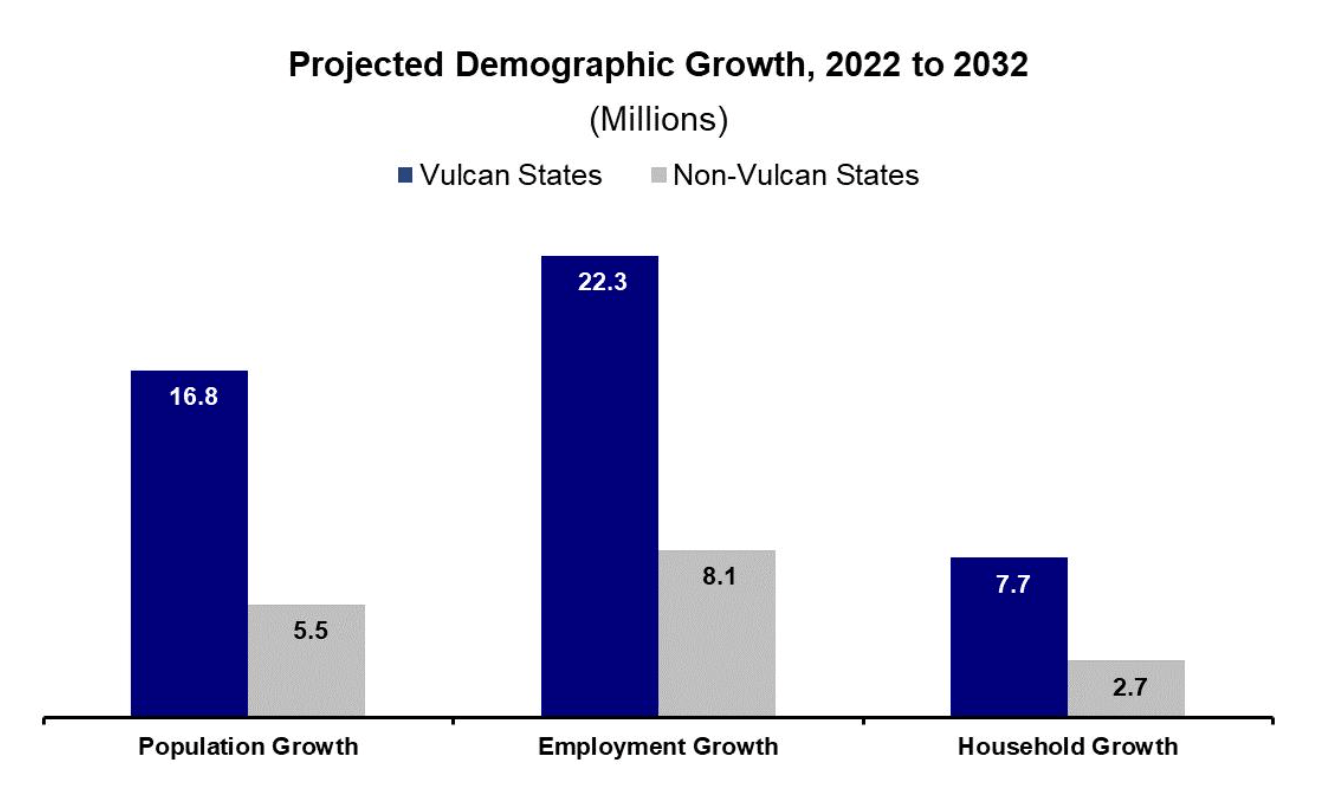

It’s also worth noting that not all parts of the country are the same. Areas with greater population growth will inevitably see more infrastructure spending. And as you can see in the image below, the next decade should bode well for the states in which Vulcan Materials operates in.

{kind=link}

This is not to say that things can't change in a negative way. They most certainly can. And that is why investors should pay special attention to when management announces financial results before the market opens on August 3rd. The current expectation is for management to report revenue of $2.05 billion. This would represent an increase of only 5.1% over the $1.95 billion reported one year earlier. On the other hand, earnings per share are forecasted to come in strong at $1.89. That compares favorably against the $1.50 reported for the second quarter of 2022. This would take net profits from continuing operations up from $200.5 million to $252.7 million. Although analysts have not provided estimates for other profitability metrics, those should also increase. And in the table below, you can see what these looked like in the second quarter of 2022.

{kind=link}

Takeaway

Based on all the data provided, I must say that Vulcan Materials Company is interesting. From a valuation perspective only, the company very much looked like a "hold" candidate to me. However, when you look at the continue to aggregates consumption and growing construction spending, you get a rather attractive catalyst. Management is also optimistic about 2023 and, absent a significant economic downturn, a downturn that, I might add, is becoming less likely by the day, the overall picture for the business moving forward should be attractive. Given all of these factors, I feel as though the company warrants a soft "buy" rating at this time.

For further details see:

Vulcan Materials Offers Long-Term Upside Despite Being Pricey