AGG - VVR: A Decent CEF For An Uncertain Rate Environment But Finances Are Questionable

2023-08-14 19:17:18 ET

Summary

- The high inflation rate in the US is causing financial strain for Americans, leading to desperate measures such as dumpster diving and pawning possessions.

- Investors can combat the rising cost of living by investing in closed-end funds that specialize in generating income.

- The Invesco Senior Income Trust is one such fund that offers a current yield of 11.94% and has a stable performance track record.

- The fund failed to cover its distribution last year despite increasing it twice in the past twelve months. It is uncertain how sustainable it is likely to be going forward.

- The fund is currently trading at a discount to net asset value.

There can be little doubt that one of the biggest problems faced by the average American today is the incredibly high inflation rate that has been persistently dogging the economy. This phenomenon has rapidly driven up the price of everything that we use or consume, making it much more expensive than it used to be to live our lives from day to day. We can clearly see the full extent of this problem by looking at the consumer price index, which claims to track the price of a basket of goods that is regularly purchased by the average person. This chart shows the year-over-year rate of change of this index during each month of the past 25 years:

{kind=link}

As we can clearly see, the annual rate of change in this index spiked to levels that are far above average shortly after the outbreak of the COVID-19 pandemic and the widespread lockdowns that accompanied it. This was due to the fact that the Federal government and a compliant Federal Reserve increased the money supply by approximately 40% in the year following the outbreak of the pandemic. This was due to all of the income support and economic stimulus measures that were passed by Congress around that time. The problem with this is the actual productive output of the economy did not grow by anywhere close to this amount. Thus, there were more units of currency attempting to purchase each unit of economic production, resulting in prices being bid up. That is the root cause of all inflation.

Normally, this might not be a problem, but wages did not increase as rapidly as the prices of goods and services. As the majority of Americans live paycheck to paycheck, this strained budgets and made it increasingly difficult to get by from day to day. Out of desperation, we are now seeing Americans resort to measures such as dumpster diving and pawning possessions just to get by. In addition, there has been an increase in the number of people working second jobs to boost their incomes, which could be one reason why the job market has proven resilient despite numerous economic indicators stating that the nation is in or very near a recession.

As investors, we are certainly not immune to the rising cost of living. After all, we require food for sustenance and energy to heat our homes or businesses, just like anyone else. In addition, we probably want to enjoy occasional luxuries in our lives. All of these things are considerably more expensive than they were only a year or two ago. Fortunately, we do not need to resort to desperate measures to get the extra income that we need to maintain our lifestyles in today's inflationary environment. After all, we have the ability to put our money to work for us in this capacity.

One of the best ways to do this is to purchase shares of a closed-end fund, or CEF, that specializes in the generation of income. These funds are unfortunately not very well-followed in the financial media and many investment advisors are somewhat unfamiliar with them. As such, it can be difficult to obtain the information that we would really like to have in order to make an informed investment decision. This is a shame because these funds offer a number of advantages over ordinary open-ended and exchange-traded funds. In particular, a closed-end fund has the ability to employ certain strategies that have the effect of boosting their yields well beyond those of any of the underlying assets or indeed pretty much anything else in the market.

In this article, we will discuss the Invesco Senior Income Trust ( VVR ), which is one fund that investors can purchase in order to earn a very high income today. This is immediately apparent in the fund's 11.94% current yield. That is certainly enough to turn the eye of any investor that is seeking to earn some income from their portfolio today. I have discussed this fund before, but several months have passed since that time so naturally a great many things have changed. This article will therefore focus specifically on those changes, as well as provide an updated analysis of the fund's finances. Let us proceed and see if this fund could be a good addition to a portfolio today.

About The Fund

According to the fund's webpage , the Invesco Senior Income Trust has the objective of providing its investors with as high a level of current income as it can earn while still ensuring the preservation of capital. This is a fairly standard objective for a fixed-income fund, and this fund generally falls into that category. As we can see here, currently 90.16% of the fund is invested in bonds, although it has some exposure to other asset types such as common and preferred stock:

CEF Connect

It is not surprising that the fund's primary objective is the provision of current income considering that its portfolio primarily consists of debt securities. After all, this is the primary way through which these securities deliver their investment returns. An investor purchases a bond at face value, receives regular coupon payments from the bond issuer, and then receives face value back when the bond matures. Thus, the only net investment return that a debt security delivers over its lifetime is the coupon payment. Bonds do not deliver net capital gains over their lifetimes because they have no inherent link to the growth and prosperity of the issuing entity.

In the case of this fund, virtually all of the investment returns are going to be in the form of coupon payments received by the securities in the fund. This is because the fund is not primarily investing in senior floating-rate loans, which I mentioned in my last article on the fund. According to the fund's fact sheet ,

"Depending on current market conditions and the fund's outlook over time, the fund seeks to achieve its investment objectives by opportunistically investing primarily in floating or variable senior loans of issuers which operate in a variety of industries and geographic regions."

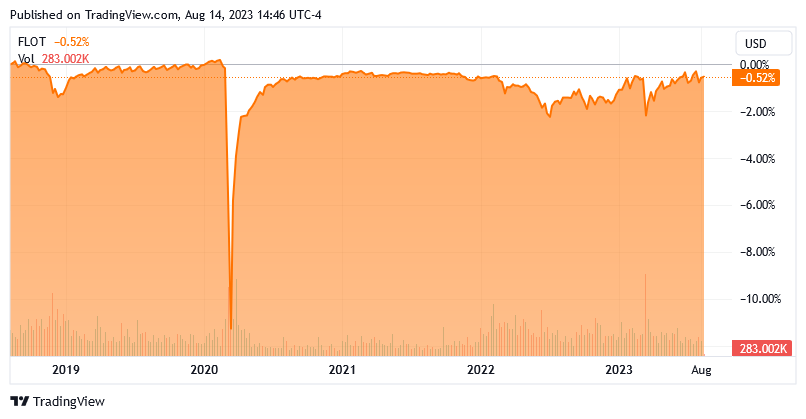

One of the defining characteristics of floating-rate debt instruments is that they tend to be remarkably stable regardless of changes in interest rates. We can see this quite clearly by looking at the Bloomberg US Floating Rate Note Index ( FLOT ), which has been almost perfectly flat over the past five years:

{kind=link}

This is very different from traditional fixed-rate bonds, whose price varies inversely with interest rates. It should be fairly obvious why this is the case. After all, the reason why bond prices decline when interest rates go up is that brand-new bonds will have a higher coupon rate than bonds that were issued when interest rates were lower. As such, nobody will buy an existing bond when they could get an otherwise identical brand-new one with a higher yield. As such, the price of the existing bond has to fall to the point at which it is delivering a competitive yield-on-cost as an otherwise identical brand-new bond. A floating-rate security, on the other hand, has a coupon that varies depending on the conditions in the market. As such, it will always deliver a competitive yield regardless of how old it is. Thus, the price tends to be very stable and all of the returns are delivered via direct payments to the investors.

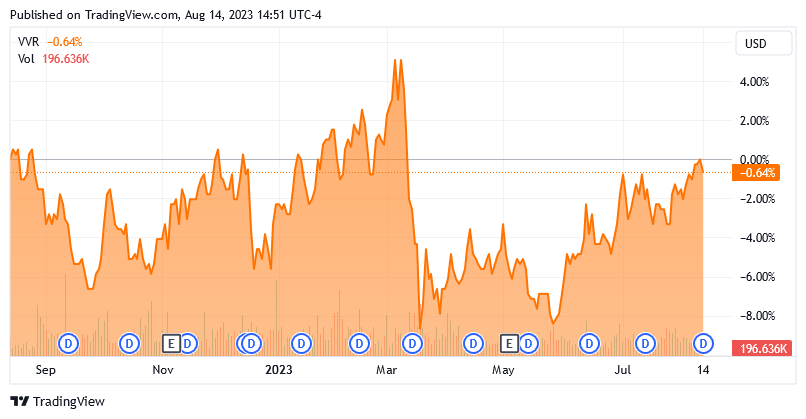

For its part, the Invesco Senior Income Trust has been relatively stable. Over the past year, the fund's share price is only down 0.64%:

{kind=link}

When we consider that this fund's yield is quite a lot above that 0.64% decline, it was more than sufficient to offset the share price decline. Overall, this fund has delivered a positive total return over the past twelve months. In fact, over the past year, the fund managed to beat both the floating-rate note index and the Bloomberg U.S. Aggregate Bond Index ( AGG ) on a total return basis:

{kind=link}

We see much the same over any longer trailing period as well. Over the three-year, five-year, and ten-year trailing periods, the Invesco Senior Income Trust delivered the highest total return, followed by the floating-rate note index. The Bloomberg U.S. Aggregate Bond Index was by far the worst performer of the three assets. This is not really surprising considering that floating-rate securities are going to be very stable performing assets over time price-wise, and usually have higher yields than traditional investment-grade bonds.

Unfortunately, most floating-rate securities, particularly the ones that this fund invests in, tend to be issued by non-investment-grade companies. For the most part, these are leveraged loans, which are loans that are issued by companies that already have a significant amount of debt. As such, their credit ratings tend to be worse than most investment-grade bonds. We can see that by looking at the credit ratings of the securities that comprise this fund's portfolio:

Invesco

An investment-grade security is anything rated Baa or above. As we can see, that is only 0.17% of the portfolio. This is something that may be concerning to risk-averse investors, as we have all heard about the high risk of default that typically accompanies junk bonds. However, the actual risk here may be somewhat exaggerated. As we can see above, 47.12% of the portfolio's assets are invested in securities that are rated either Ba or B. According to the official bond rating scale , companies whose securities have been assigned these ratings have sufficient financial strength to meet all of their current debt obligations through a short-term economic shock. Thus, the risk of default on these securities is not as high as many people might fear. The fund itself states that its default rate was only 4.80% over the last twelve months. When we consider that the interest rate on these securities is more than that, this is not too bad as the interest coming into the fund is more than enough to offset the default-related losses. This is ultimately the most important thing, as it indicates that the portfolio is profitable overall.

Leverage

In the introduction to this article, I stated that closed-end funds like the Invesco Senior Income Trust have the ability to employ certain strategies that allow them to boost their effective yields well beyond that of any of the underlying assets. One of these strategies is the use of leverage. In short, the fund borrows money and then uses that borrowed money to purchase floating-rate securities. As long as the interest rate that the fund pays on the borrowed money is less than the yield that it receives from the purchased assets, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will usually be the case. However, it is worth noting that this strategy is not as effective today with rates at 6% as it was eighteen months ago when it could borrow money for basically nothing. This is because the difference between the rate that the fund has to pay on the borrowings and the yield that it receives from the purchased assets is much narrower than it once was.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much debt because that would expose us to an excessive amount of risk. I generally do not like to see a fund's leverage exceed a third as a percentage of its assets for this reason. This fund certainly meets this criterion, as its leveraged assets comprise 32.19% of its portfolio. Thus, it appears that this fund is striking a fairly reasonable balance between risk and reward.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Invesco Senior Income Trust is to provide its investors with a high level of current income. In order to achieve this objective, the fund invests in speculative-grade floating-rate securities that tend to have fairly high yields and deliver nearly all of their investment return via direct payments to the investors. This fund then applies a layer of leverage to boost the effective portfolio return well beyond that of any of the underlying assets in the portfolio. The fund then pays out most to all of its investment returns to the shareholders. As such, we can probably assume that this fund would have a very high yield itself.

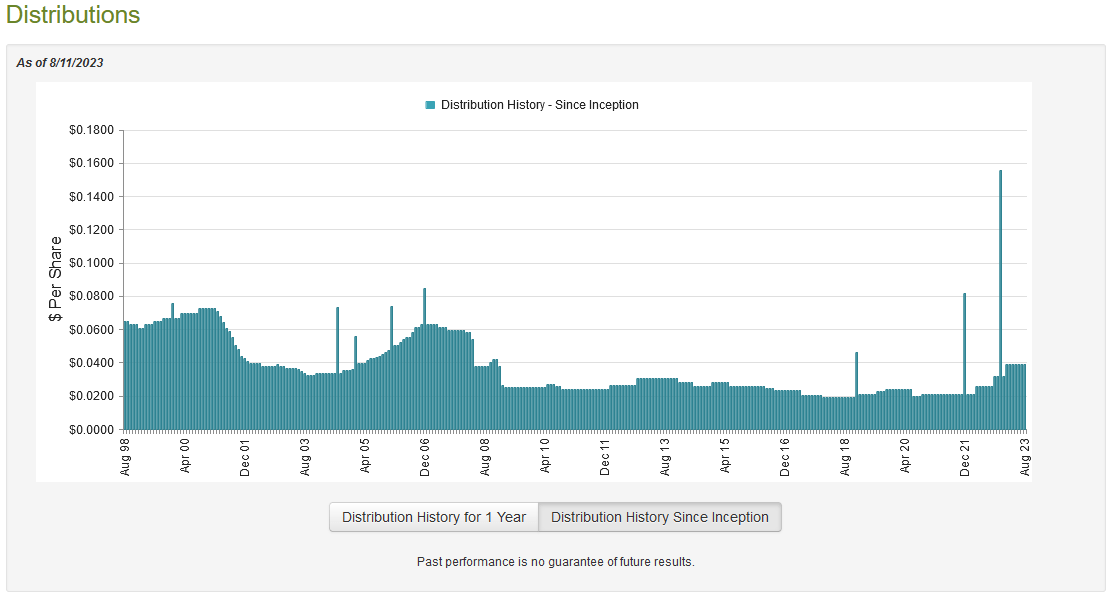

This is certainly the case, as it pays a monthly distribution of $0.0390 per share ($0.468 per share annually), which gives the fund an 11.94% yield at the current price. Unfortunately, this fund has not been particularly consistent with its distribution over time. In fact, it has changed it quite frequently:

{kind=link}

This is something that will probably serve as a turn-off for those investors that are seeking a safe and secure source of income to use to pay their bills or finance their lifestyles. However, it is not at all uncommon for a fixed-income fund to vary its distribution like this. After all, the investment performance of its portfolio is highly dependent on interest rates. This is especially true with floating-rate securities, as their price stability means that the fund's investment returns will be almost entirely the direct payments that it receives from the securities. Thus, the fund will have substantially higher income during periods in which interest rates are high compared to periods in which rates are low. The fund will adjust its distribution accordingly. That does make this a good way to hedge your portfolio though, as it will probably perform better in a rising environment than an ordinary bond fund.

As is always the case, we want to have a look at the fund's finances to ensure that it is not distributing more to the investors than it can afford. After all, the last thing that we want is for the fund to be depleting its assets. After all, the smaller the fund's assets, the higher the return that is needed to earn a specified level of income and if the portfolio gets too small then it may have to set a permanently lower payout no matter what interest rates do.

Fortunately, we do have a relatively recent document that we can consult for the purposes of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the full-year period that ended on February 28, 2023. As such, it will not include any information about the fund's performance over the past few months. However, it is still newer than the reports that are currently available for many other closed-end funds. It should also be able to give us a good idea of how well the fund handled the challenging conditions of 2022 as well as the market rebound that occurred early this year.

During the full-year period, the Invesco Senior Income Trust received $80,494,795 in interest and $1,891,246 in dividends from the investments in its portfolio. When we combine this with a small amount of income from other sources, the fund achieved a total investment income of $82,624,863 over the period in question. The fund paid its expenses out of this amount, which left it with $59,249,486 available for the shareholders. That was, unfortunately, nowhere close to enough to cover the $71,603,082 that the fund paid out in distributions over the period. This is concerning as we normally like a debt fund to be able to cover its distributions completely out of net investment income, but this one clearly is not able to accomplish that.

With that said, a fund like this does have other ways through which it can obtain the money that it needs to cover the distribution. For example, it might have been able to earn some capital gains that could be paid out to the investors. Unfortunately, this fund failed miserably at that task over the period. It reported net realized losses of $11,348,074 and had another $47,245,730 net unrealized losses. Overall, the fund's assets declined by a whopping $70,947,400 after accounting for all inflows and outflows during the period. This is concerning, as the fund clearly failed to cover its distributions through February. However, it has increased its distribution twice over the past year.

It remains to be seen whether or not this distribution is sustainable, as strong performance early this year may have been able to correct its problems, so we will want to take a very close look at the fund's semi-annual report in order to determine how sustainable the distribution is likely to be.

Valuation

It is always critical that we do not overpay for any assets in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the Invesco Senior Income Trust, the usual way to value it is by looking at the net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are obtaining a fund's assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of August 11, 2023 (the most recent date for which data is available as of the time of writing), the Invesco Senior Income Trust had a net asset value of $4.14 per share but the shares only traded for $3.92 each. This gives the shares a 5.31% discount on net asset value at the current price. That is in line with the 5.84% discount that the shares have had on average over the past month, so the price looks reasonable.

Conclusion

In conclusion, the Invesco Senior Income Trust is one reasonable way for an investor to generate a high level of income from their portfolio today. The fact that this fund invests in floating-rate securities should provide a degree of protection against changes in interest rates, which may be important today since the latest inflation report implies that the Federal Reserve's fight against inflation is far from over. The problem here is that the fund failed to cover its distribution last year, yet it still boosted its distribution. Thus, it is uncertain how sustainable its finances are right now.

For further details see:

VVR: A Decent CEF For An Uncertain Rate Environment, But Finances Are Questionable