VVR - VVR: A Fixed-Income Fund For Rising Rates

Summary

- The Federal Reserve's interest rate tightening scheme has had a negative effect on most fixed-income securities.

- Invesco Senior Income Trust invests in floating-rate loans, which should prove more resilient to rising rates than traditional bonds.

- The fund maintains a very well-diversified portfolio to ensure that default risk is fairly minimal.

- The fund is paying its distribution solely out of net investment income, which should be comforting for risk-averse investors.

- The fund is trading at a reasonably attractive valuation right now.

Without a doubt, the biggest problem faced by Americans over the past year or so has been the incredibly high inflation that has been permeating the economy. This inflation has resulted in nineteen months of negative real income growth and, as it has been focused on necessities such as food and energy, has forced many people to take on second jobs or enter the gig economy simply to obtain the extra money that they need to support themselves.

Fortunately, as investors, we have other options that can be utilized in order to increase our incomes and achieve the same task without having to go through the aggravation of doing extra work. One of the best of these options is to purchase shares of a closed-end fund that specializes in the generation of income. These funds are nice because they provide us with easy access to a diversified portfolio of assets that can use various strategies that result in higher yields than those of the underlying assets.

In this article, we will discuss the Invesco Senior Income Trust ( VVR ), which is one fund that can be used for the generation of income. The fact that the fund is yielding an impressive 10.05% at the current price provides further evidence of its capacity for income generation. The fund has a reasonable valuation in addition to a high yield, which further increases its attractiveness to those investors that are seeking income. Therefore, let us investigate and see if this high-yielding fund could prove a worthy addition to your portfolio!

About The Fund

According to the fund’s webpage , the Invesco Senior Income Trust has the stated objective of providing its investors with as high a level of current income as is consistent with the preservation of capital. Annoyingly, the fund’s webpage is rather spartan and contains very little information about the fund that would be useful to investors. It does not even state what assets the fund is investing in, and I must admit that I expected much better from a major fund house like Invesco.

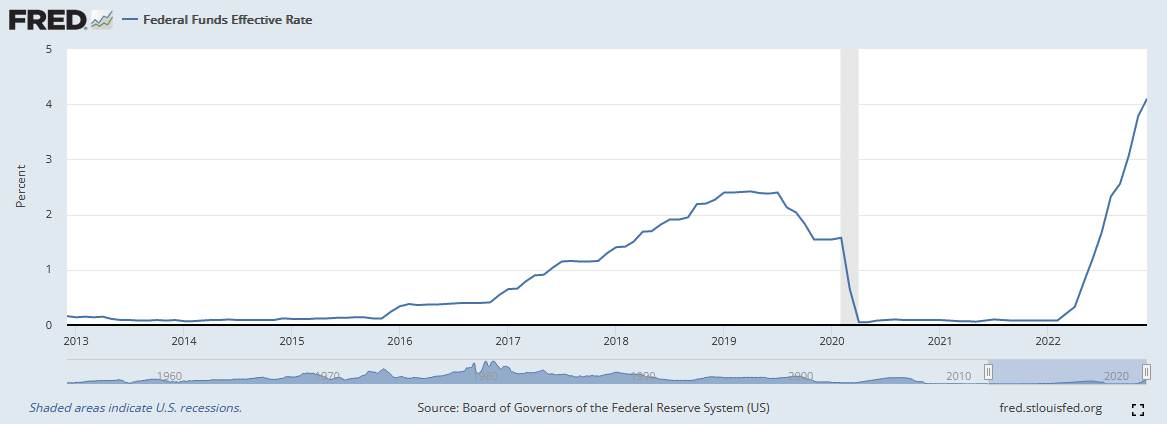

Fortunately, the fund’s fact sheet is much better, although it is not a very pretty document to look at. As the name of the fund would imply, the Invesco Senior Income Trust primarily invests in senior secured loans, which are also known as leveraged loans. These are fixed-income securities that are somewhat different from traditional bonds. The biggest difference is that these loans have a floating rate, which means that the interest rate paid by the borrower actually increases when interest rates go up and declines when rates go down. This helps address one of the biggest problems faced by other fixed-income securities in today’s environment. As everyone reading this is no doubt well aware, the Federal Reserve has shifted away from its long-standing policy of loose money in order to combat the high inflation that has been plaguing the economy. Back in February 2022, the federal funds rate sat at 0.08% but it averaged 4.10% in December 2022, which is the highest rate that we have seen in a decade:

{kind=link}

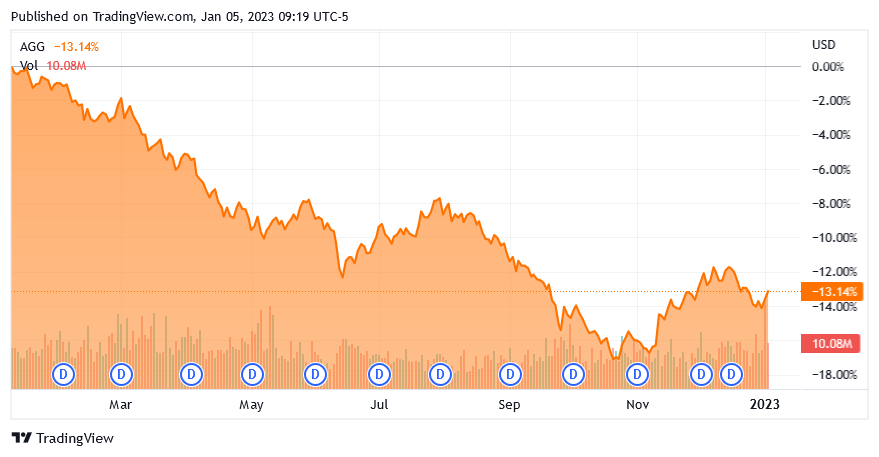

This has had a devastating effect on fixed-income assets due to the fact that their prices vary inversely with interest rates. Basically, when interest rates go up, bond prices go down, and vice versa. As the Federal Reserve has been raising interest rates over the past year, the prices of bonds throughout the American economy have been falling. This is evident in the fact that the Bloomberg U.S. Aggregate Bond Index ( AGG ) is down 13.14% over the past twelve months:

{kind=link}

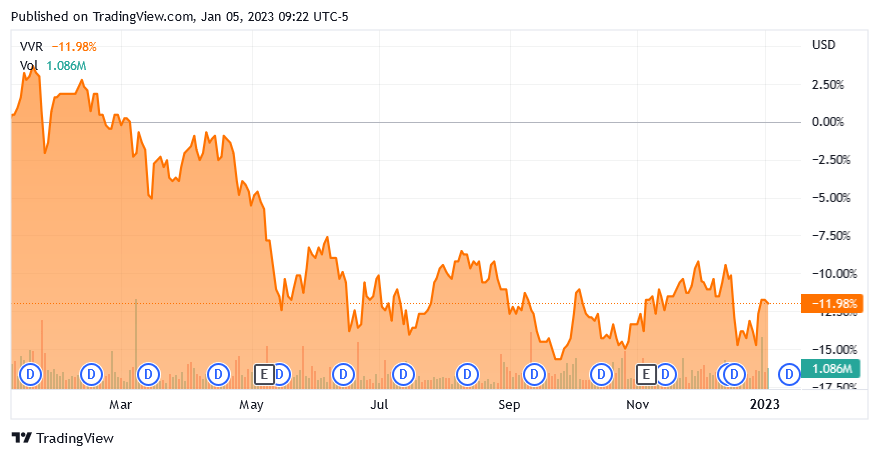

The reason for the decline in bond prices is that newly-issued bonds will have a yield that correlates to the higher interest rate in the economy. Thus, nobody will buy an existing bond with a lower yield unless its price declines to the point where the bond is giving the same effective yield-to-maturity as a newly issued bond with the same characteristics. The fact that the securities that the Invesco Senior Income Trust purchases have an interest rate that increases along with the federal funds rate should mean that these securities will hold their value much better than traditional bonds in a rising interest rate environment. This certainly plays out somewhat when we look at the fund’s share price as it is only down 11.98% over the same twelve-month period:

{kind=link}

The fact that the Invesco Senior Income Trust has a much higher yield than the Aggregate Bond Index makes the performance difference even starker. Overall, this is the kind of fixed-income fund that we really want to be held in a rising interest rate environment. The Federal Reserve has projected that it will continue to raise rates in 2023 to a peak of between 5% and 6%. Thus, the price of traditional bonds will almost certainly continue to decline over the coming months, which makes the Invesco Senior Income Trust an even more worthy fund for consideration today as it will likely continue to outperform for a while.

One potential downside here is that the assets that comprise the Invesco Senior Income Trust are leveraged loans. This means that they are extended to companies that already have a considerable amount of debt and are therefore riskier than most traditional investment-grade bonds. We can see this pretty easily by looking at the credit ratings that have been assigned to the various securities in the fund’s portfolio. Here is a high-level summary:

Invesco

An investment-grade fixed-income security is anything rated Baa or higher so we can quickly see that everything in the fund is lower than that. This is something that may concern more conservative investors that are concerned with principal preservation, which is a category that includes many retirees. However, 47.15% of the assets in the portfolio have either a Ba or B rating. These are the two highest ratings for speculative-grade securities and, according to the official bond rating scale , a company whose securities have these ratings will have the financial capacity to meet its debt obligations even in the event of a short-term economic shock. They may be vulnerable to a long-term economic downturn but we have not had one of those since the Great Depression. Thus, just under half of the securities in the fund should be just fine even in a recession, which is now widely projected to occur in 2023.

Another way that the fund can reduce its risk of losses due to defaults is by having a large number of securities in the fund. This is because such a setup would imply that the fund only has a very small amount of exposure to any individual issuer and thus a loss on one company would have a negligible impact on the portfolio in aggregate. The fund is certainly accomplishing this through its 599 current holdings. However, it is still possible that one holding could account for a fairly significant portion of the overall portfolio, and the fund, unfortunately, does not provide us with a list of its largest positions so that we can determine that. Overall, though, the sheer number of positions should ensure that the fund is protected against all but widespread defaults. If a situation occurs that sees a massive number of defaults sweeping the country, the economy has far bigger problems than a few fixed-income investors suffering losses. In fact, in such a situation, there would likely not be anything that we could turn to for protection so it is not really worth worrying about default risk here.

The fact that the fund’s investments are nearly all in speculative-grade debt (there is a small allocation to stocks in the portfolio) is still likely to be off-putting to some investors. However, leveraged loans have one characteristic that greatly reduces the risk of losses due to a default. This characteristic is that the borrowing company must pledge an asset as collateral for the loan. This is usually some piece of real property, such as a factory or other valuable real estate. The lenders are then able to seize and sell that property to recoup their losses in the event of a default. As the pledged piece of property is usually valuable enough to secure the loan, the risk is greatly minimized. As we can see here, 83.92% of the loans in the fund are secured with first liens on the collateral:

Invesco

This should provide us with a great deal of reassurance that we are unlikely to lose much money if a default occurs. When we combine the value of the pledged collateral with the overall diversity of the portfolio, we can see that we really should not worry at all that the companies whose securities are held by the fund are at higher risk of default than a normal investment-grade bond. Our overall risk here is actually quite low.

Leverage

As stated in the introduction, closed-end funds like the Invesco Senior Income Trust have the ability to utilize a variety of strategies that have the effect of increasing their yield beyond that of any of the underlying assets. One of these strategies is the use of leverage. Basically, the fund is borrowing money and then using that borrowed money to purchase senior-secured loans. As long as the interest rate that the fund has to pay on the borrowed money is less than the yield of the purchased assets, the strategy works pretty well to boost the overall yield of the portfolio. The fund is able to borrow at institutional rates, which are considerably lower than retail rates, so this will usually be the case.

Unfortunately, the use of leverage is a double-edged sword because debt boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage since that would expose us to too much risk. I do not usually like to see a fund’s leverage exceed a third of its assets for this reason. Fortunately, the Invesco Senior Income Trust fulfills this requirement as its levered assets only comprise 32.92% of the total portfolio. The fund’s leverage is therefore quite close to the maximum limit that I typically like to see but it is overall acceptable. The fund is striking a pretty reasonable balance between risk and reward here.

Distribution Analysis

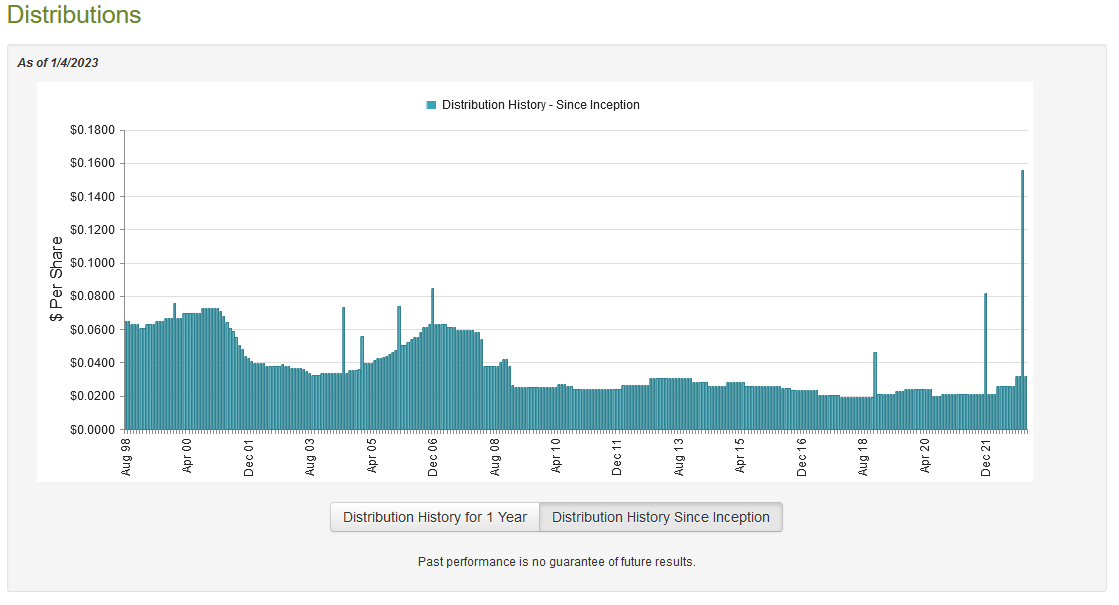

As mentioned earlier in the article, the primary goal of the Invesco Senior Income Trust is to provide its investors with a high level of current income. This is a pretty similar objective to any other fixed-income closed-end fund. In order to accomplish its objective, the fund invests in high-yielding senior secured loans and then employs leverage to boost the effective yield of the portfolio. As such, we might assume that the fund itself has a fairly high yield. This is certainly the case as the Invesco Senior Income Trust pays out a monthly distribution of $0.0320 per share ($0.3840 per share annually), which gives the fund a 10.05% yield at the current price. The distribution has varied a great deal over the years, but it has been increasing for a while and the fund increased the distribution in both April and October 2022:

{kind=link}

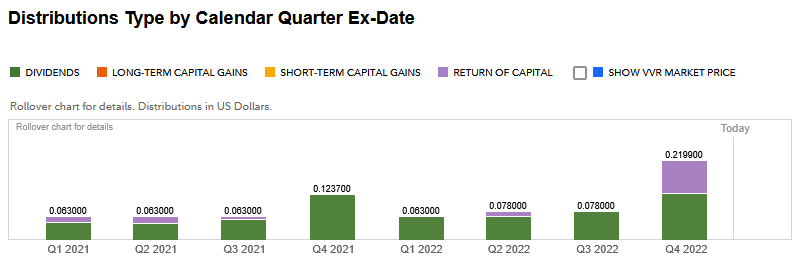

The fact that the fund’s distribution has varied so considerably over the years might prove to be a bit of a turn-off for those investors that are looking for a safe and secure source of income with which to use to pay their bills. However, the fact that the fund increased the distribution twice in the past twelve months proves the point that has been made throughout this article that the assets in the fund should perform reasonably well in a rising-rate environment. Another thing that is rather nice to see is that the fund’s distributions are almost entirely classified as dividend income, although the return of capital in the most recent quarter is concerning:

{kind=link}

The reason that the return of capital distribution is concerning is that a return of capital distribution can be a sign that the fund is returning the investors’ own money back to them. This is obviously not sustainable over any sort of extended period. However, there are other things that can cause a distribution to be classified as a return of capital, such as the distribution of unrealized capital gains. The fact that most of these distributions are dividend income is comforting though because this is the most sustainable form of distribution for a fixed-income fund. After all, these distributions are paid directly from the money that is paid by the securities in the fund’s portfolio and is not dependent on its ability to actually earn capital gains. As I pointed out in the past though, it is possible for the fund’s distributions to be misclassified. As such, we do want to analyze its finances in order to determine just how sustainable the distributions are likely to be.

Fortunately, we have a very recent document that we can consult for this task. The fund’s most recent financial report corresponds to the six-month period ending August 31, 2022. It will, therefore, not include information from the past few months but this is a much more recent document than most other funds currently have available to their investors and it will definitely give us some good insight into how the fund is navigating the current rising interest rate environment. During the six-month period, the Invesco Senior Income Trust received a total of $845,876 in dividends and $34,344,476 million in interest from the assets in its portfolio. When we combine this with a small amount of income from other sources, we see that the fund had a total income of $35,374,638 over the period. The fund paid its expenses out of this amount, leaving it with $25,915,991 available for investors. This was sufficient to cover the $23,107,642 that the fund actually paid out in distributions during the same period. It thus does overall appear that the fund is not overdistributing as it is simply paying out the overwhelming majority of its income. The distribution will likely vary a bit with the fund’s income and thus may start declining if the Federal Reserve pivots and begins reducing rates but that does not appear to be a problem for the near term.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the Invesco Senior Income Trust, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund’s assets for less than they are actually worth. This is, fortunately, the case with the Invesco Senior Income Trust today. As of January 4, 2023 (the most recent date for which data is currently available), the fund has a net asset value of $4.07 per share but it actually trades for $3.83 per share. This gives the fund’s shares a 5.90% discount at the current price. This is not as attractive as the 6.64% discount that the shares have possessed on average over the past month so it might make sense to wait a few days and see if the price does ultimately become more attractive. However, the current price is certainly not unreasonable if you are impatient and want to buy today.

Conclusion

In conclusion, the Invesco Senior Income Trust looks like a pretty good fixed-income fund to buy today in response to the Federal Reserve’s monetary tightening regime. The fact that the loans in which the fund is invested are floating-rate securities helps maintain the asset value in such an environment. The securities are certainly riskier than traditional investment-grade bonds, but the fund appears to be mitigating that quite well and overall, we should not have to worry much about defaults. The fund also has a very sustainable 10.05% distribution yield and an attractive valuation. There is a lot to like here.

For further details see:

VVR: A Fixed-Income Fund For Rising Rates