PDO - VVR: Benefiting From Rising Rates And Boasting A Remarkable 13.6% Yield

2023-10-27 11:30:02 ET

Summary

- Invesco Senior Income Trust offers a high level of income, with a whopping 13.65% yield, higher than most other funds in the market.

- The fund invests primarily in floating-rate debt securities, which remain stable in rising interest rate environments.

- The fund's leverage is reasonable and its distribution appears to be sustainable based on its net investment income.

- The fund's net assets did decline during the most recent financial period, but that was only due to unrealized losses.

- The fund is trading at an attractive discount on net asset value right now.

The Invesco Senior Income Trust ( VVR ) is a closed-end fund, or CEF, that can be employed by those investors who are seeking to earn a very high level of income from the assets in their portfolios. This is quite evident in the fact that the fund currently boasts a whopping 13.65% yield, which is considerably higher than just about anything else in the market. In fact, this yield is so high that it is a clear sign that the market expects that the fund may have to cut its distribution before too long. This is concerning, particularly in today's inflationary world, as we generally need as much income as we can get in order to sustain the lifestyles to which we are accustomed.

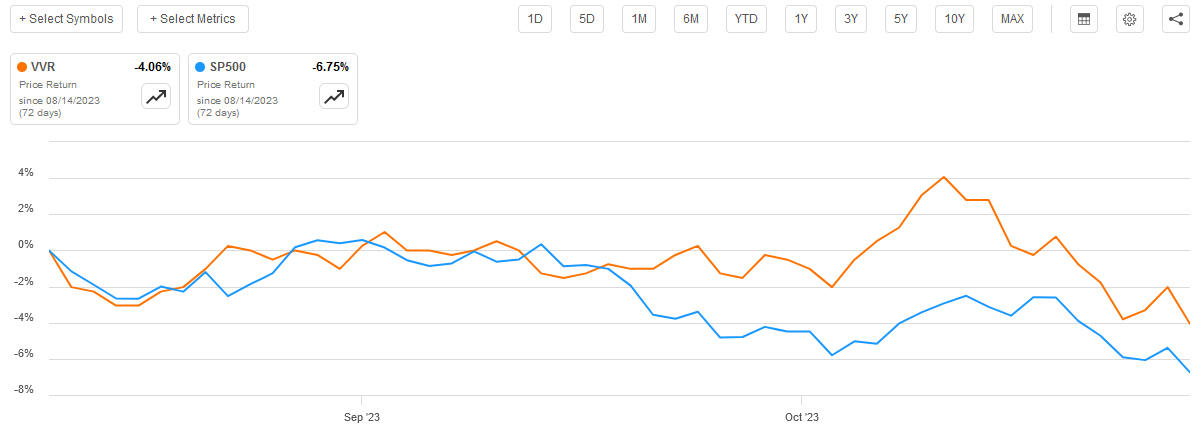

As regular readers may recall, we last discussed the Invesco Senior Income Trust in mid-August of this year. The fund has admittedly not performed as well as may be hoped since that time, although it has proven to be a better holding than the S&P 500 Index ( SP500 ):

{kind=link}

This is a good sign, but it is not especially surprising. Over the past few months, the market has been plagued with rising interest rates. After all, at the time that the last article on this fund was published, the ten-year U.S. Treasury (US10Y) was only at 4.18%. It is around 4.925% today, an increase of 74 basis points in just over two months:

{kind=link}

This naturally pushed down the earnings yield of both the S&P 500 Index and everything else. After all, why would investors want to take a risk when they can earn nearly 5% by betting on a sure thing?

Fortunately, as I pointed out in previous articles on this fund, the Invesco Senior Income Trust should hold its value reasonably well even during a rising interest rate environment. This gives it a marked advantage over many other things in the current environment. Let us investigate to see if this is still the case.

About The Fund

According to the fund's webpage , the Invesco Senior Income Trust has the primary objective of providing its investors with a high level of current income while still ensuring the preservation of capital. This is not particularly surprising, as it is a common objective for fixed-income funds such as this one. As we can see here, 90.16% of the fund's assets are invested in bonds, although it has a surprisingly large allocation to common stock as well:

CEF Connect

These are not the ordinary fixed-rate coupon bonds that one would expect to find in any other bond fund, however. The website itself is not particularly clear on the contents of this fund, but the fact sheet states:

Depending on current market conditions and the Fund's outlook over time, the Fund seeks to achieve its investment objectives by opportunistically investing primarily in floating or variable senior loans of issuers which operate in a variety of industries and geographic regions.

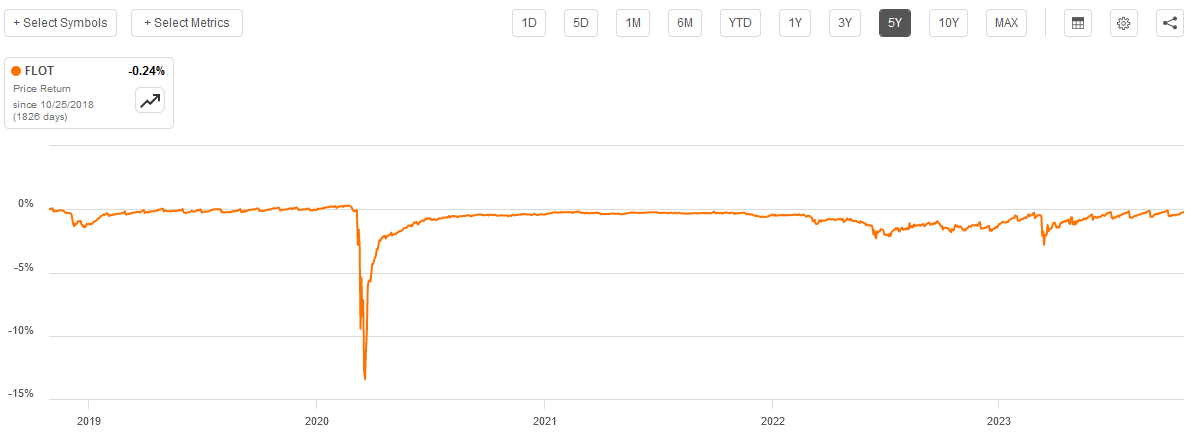

This description clearly describes a floating-rate bond fund, which means that the interest rate of the securities that are held by this fund varies based on the prevailing market interest rate. It is usually expressed as Base Rate + XXXX%, where XXXX% is a spread over the base rate in the economy (such as LIBOR). This allows these securities to remain remarkably stable in many market conditions. We can see this by looking at the Bloomberg US Floating Rate Note < 5 Yrs. Index ( FLOT ):

{kind=link}

As we can see, the only event that had any real effect on this index over the past half-decade was the market crash in 2020. That event was driven simply by investors' panic selling in reaction to the outbreak of the COVID-19 pandemic. It had nothing really to do with a change in interest rates. We can also see that the rising interest rates over the past two years have had almost no effect on the index. This is, therefore, exactly the kind of asset that we want to be holding if we expect rates to rise.

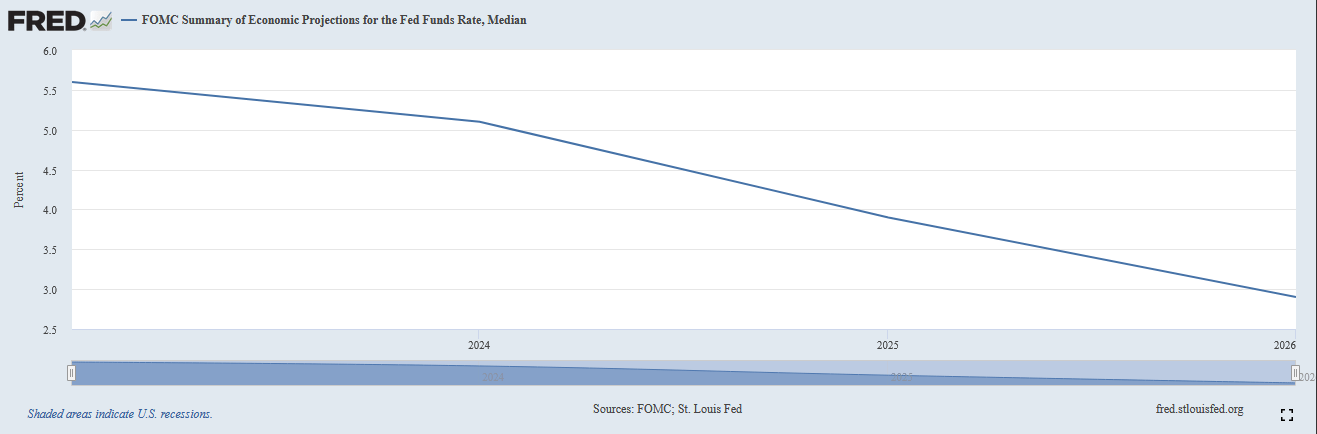

The question now, of course, is whether or not interest rates will actually increase further. There may be some reason to expect that this will be the case. The members of the Federal Market Open Committee do not believe that this will be the case, as the median prediction right now is that the federal funds rate will be at 5.1% at the end of 2024, 3.9% at the end of 2025, and 2.9% at the end of 2026:

Federal Reserve Bank of St. Louis

{kind=link}

However, the federal funds rate does not necessarily mean that market interest rates, which are more dependent on the ten-year Treasury yield, will actually cooperate with officials trying to lower interest rates. In particular, the U.S. Federal Government's insatiable demand for money could make it difficult for the Federal Reserve to control interest rates. I discussed this in a previous article . In short, the Federal Government's demand for money is essentially starving the private sector for funds. As the M2 money supply is not increasing, money must go to either the Federal Government or the private sector, and the fact that demand is growing but supply is not is pressuring interest rates upward. Thus, the Federal Reserve may be forced to choose between low interest rates or low inflation, as it will not be possible to have both. It is uncertain how this situation could be resolved, as mandatory spending alone is higher than total tax revenue, and raising tax revenue will require more money going to the private sector in order to stimulate income growth. While I am uncertain of a solution to this problem, it does show that interest rates may increasingly be out of the control of the Federal Reserve. Fortunately, the fact that the Invesco Senior Income Trust invests mostly in floating-rate securities should allow the value of its assets to remain relatively stable regardless of the direction that interest rates actually take.

In fact, rising interest rates should benefit the Invesco Senior Income Trust. This is due to the fact that the average security held by the fund carries an adjustable coupon of 5.07% over the base rate. Thus, when the base rate increases, the amount of money paid by the bond should increase. This is the reason why floating-rate debt securities do not decline when interest rates increase. It also means that the fund's income should increase along with interest rates, even if the fund does not actively replace the securities in its portfolio. In the case of traditional fixed-rate bonds, a fund would actually have to buy a new bond to realize the benefits of rising interest rates. Thus, this gives the Invesco Senior Income Trust another advantage over ordinary bond funds, particularly if interest rates keep rising.

As is frequently the case with closed-end debt funds, the Invesco Senior Income Trust does not engage in a significant amount of bond trading. During the most recent full-year period for which the fund has reported results, it only had an annual turnover of 38.00%. This is not especially high, but admittedly many debt funds tend to have fairly low turnover. It is still, however, nice to see that this fund is not imposing an excessive level of costs on its investors due to its trading activity. This fund also does not really need to do much in the way of trading anyway, due to the fact that many of its holdings pay out larger amounts as interest rates go up.

One of the big downsides here, though, is that many of the fund's securities are issued by companies that may not have the strongest balance sheets. As I explained in my previous article on this fund:

Unfortunately, most floating-rate securities, particularly the ones that this fund invests in, tend to be issued by non-investment-grade companies. For the most part, these are leveraged loans, which are loans that are issued by companies that already have a significant amount of debt. As such, their credit ratings tend to be worse than most investment-grade bonds.

Here is how the securities that comprise the portfolio of the Invesco Senior Income Trust are rated by the major credit-rating agencies:

Fund Fact Sheet

An investment-grade security is anything rated Baa or higher, so we can see that this only accounts for 0.16% of the fund's holdings. In addition, the fund's portfolio includes 7.51% common equity, so that is naturally not going to be rated at all. Thus, we can conclude that approximately 7.67% of the fund's portfolio consists of something other than junk-rated debt.

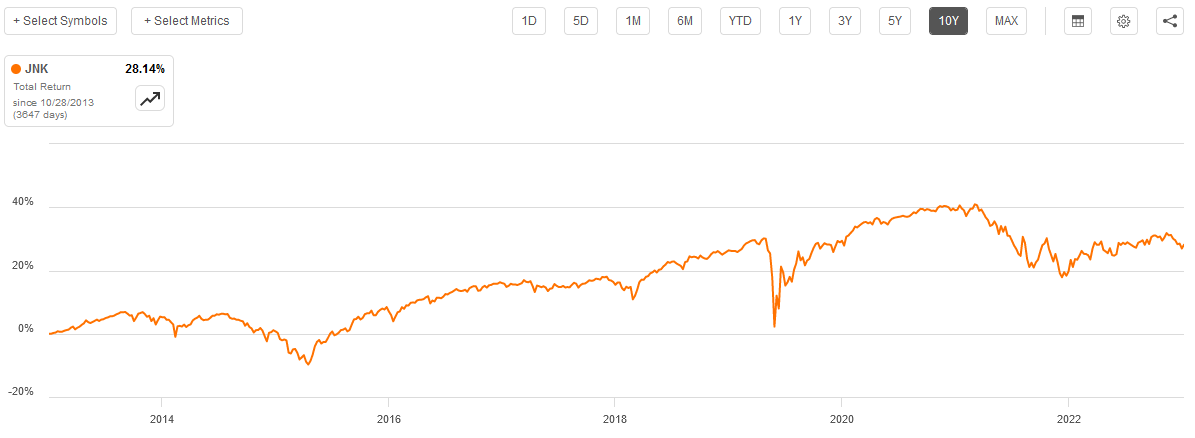

That is something that may concern some investors, particularly those of a more conservative nature, such as retirees. This is due to the fact that junk debt has a considerably higher default rate than traditional investment-grade debt. In fact, the fund's fact sheet states that it has had a default rate of 5.05% over the past twelve months, which is significantly higher than would be found in an investment-grade credit fund. That is not necessarily a problem though as the fund has taken some precautions. For example, it has 359 current issuers whose securities are represented in the portfolio, so each individual position should only account for a very small percentage of the portfolio. Thus, an individual default should not have a noticeable impact on the portfolio as a whole. When we also consider that the spread above the base rate is higher than the current default rate, we can also see that investors should be able to make money overall even with securities defaulting. This is why things such as the SPDR Bloomberg High Yield Bond ETF ( JNK ) are still able to make money even though it is also losing money through defaults:

{kind=link}

As we can see, the junk bond ETF has generally always had a positive total return over the past ten years, despite the fact that economic conditions during a few of these periods resulted in a significant increase in default-related losses. The same should be true of the Invesco Senior Income Trust, which should prove at least somewhat comforting to investors who are highly concerned with the preservation of capital.

Leverage

As is the case with most debt funds, the Invesco Senior Income Trust employs leverage as a method of boosting the effective yield of its assets. I explained how this works in my previous article on this fund:

In short, the fund borrows money and then uses that borrowed money to purchase floating-rate securities. As long as the interest rate that the fund pays on the borrowed money is less than the yield that it receives from the purchased assets, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably cheaper than retail rates, that will usually be the case. However, it is worth noting that this strategy is not as effective today with rates at 6% as it was eighteen months ago when it could borrow money for basically nothing. This is because the difference between the rate that the fund has to pay on the borrowings and the yield that it receives from the purchased assets is much narrower than it once was.

Unfortunately, the use of leverage in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much debt because that would expose us to an excessive amount of risk. I generally do not like to see a fund's leverage exceed a third as a percentage of its assets for this reason.

As of the time of writing, the Invesco Senior Income Trust has leveraged assets comprising 32.45% of its portfolio. This is relatively in line with the 32.19% leverage that the fund had the last time that we discussed it, which is a sign that the fund has not really changed its leverage too much since the last time that we discussed it. It is also below the one-third maximum which represents a reasonable balance between the risk and reward. As such, the fund's current leverage should be okay, but admittedly it might be preferable to see a lower level of leverage considering that the benefits are no longer as great as they used to be.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Invesco Senior Income Trust is to provide its investors with a high level of current income. In order to accomplish this objective, the fund invests in a portfolio consisting primarily of high-yielding floating-rate debt securities. As already mentioned, the average security in this fund carries a coupon that adjusts so that the bond will always deliver a yield that is 5.07% above the base rate in the economy. That puts all of the fund's assets with pretty close to a 10% yield at a minimum right now, and when we consider that the fund is using leverage to boost the effective yield, we can conclude that this fund should be able to pay out an enormous yield to its investors.

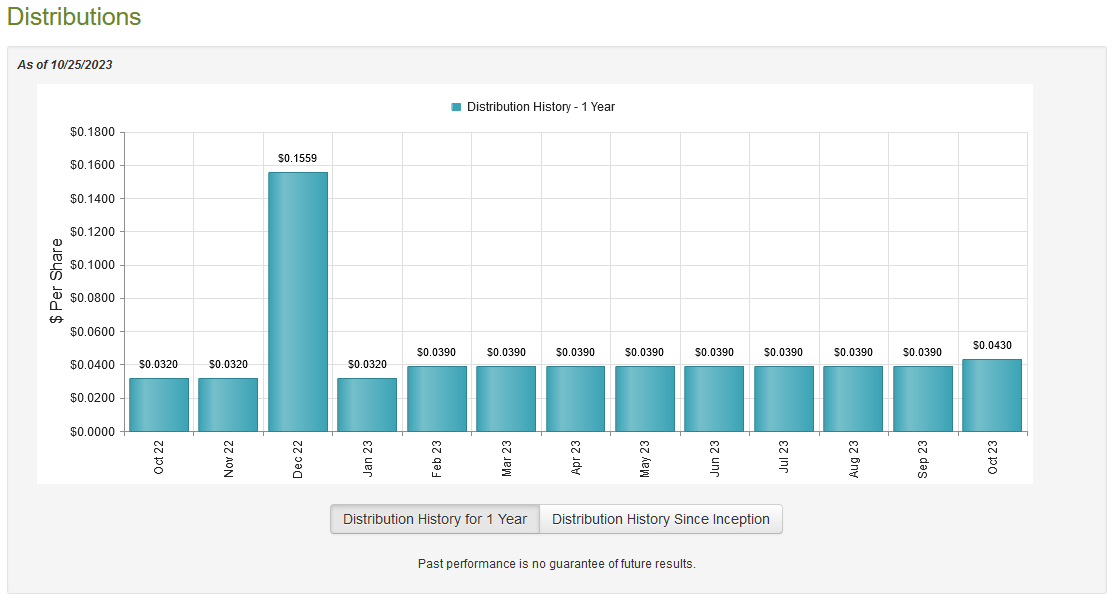

That is indeed the case, as the Invesco Senior Income Trust currently pays a monthly distribution of $0.0430 per share ($0.516 per share annually), which gives it a 13.65% yield at the current price. This is without a doubt a whopping yield that would have easily turned heads a few years ago. However, nowadays there are several other debt funds that can boast comparable yields:

| Fund Name |

| Current Yield |

| Invesco Senior Income Trust |

| 13.65% |

| Apollo Senior Floating Rate Fund ( AFT ) |

| 12.84% |

| PIMCO Dynamic Income Opportunities Fund ( PDO ) |

| 14.30% |

| Ares Dynamic Credit Allocation Fund ( ARDC ) |

| 11.82% |

| Eaton Vance Floating Rate Income Fund ( EFT ) |

| 11.82% |

Thus, it may no longer be true that a double-digit yield is a sign that a fund may be forced to lower its distribution in the near future. After all, we are currently in an environment in which many junk bonds are yielding fairly close to that level. However, we still want to analyze the fund's finances as it has not been particularly consistent with respect to its distribution over the years:

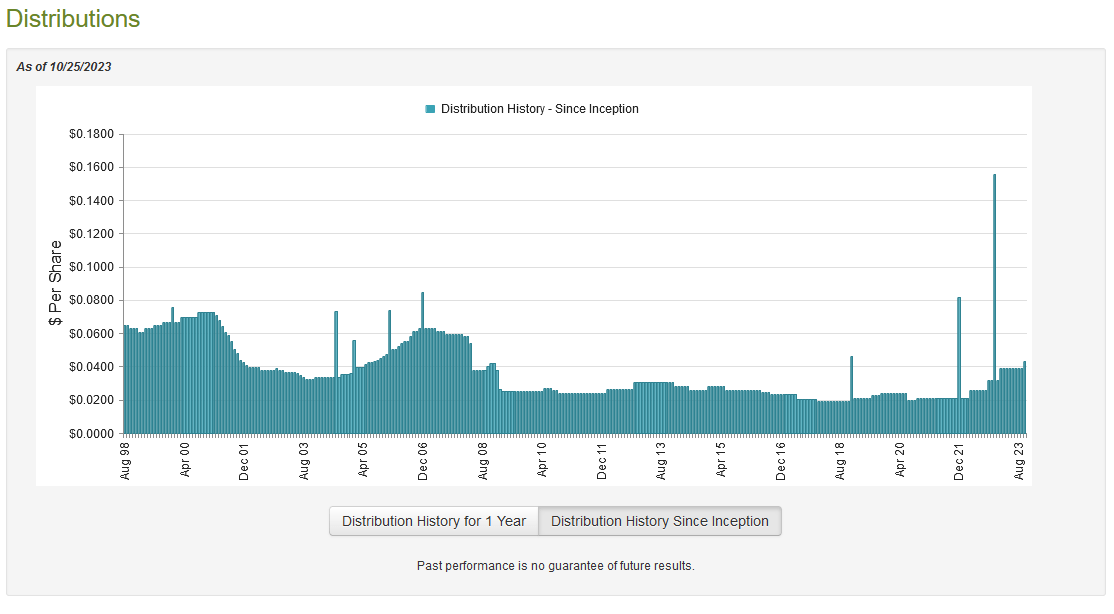

{kind=link}

This is something that may not inspire much confidence into those investors who are seeking to earn a safe and sustainable level of income from the assets in their portfolios. That goal could be necessary for retirees and others who are dependent on their portfolios to generate the income that they need to pay their bills or finance their overall lifestyles. However, we can see that the fund has been fairly rapidly increasing its distribution over the past two years or so. In fact, it has increased its payout twice over the past twelve months:

{kind=link}

This is similar to what we have been seeing among other debt funds that invest heavily in floating-rate debt. This is due to the fact that the income of these funds increases as interest rates go up. We discussed this earlier in this article. We do still want to ensure that the fund is not paying more than it can afford though, as depleting its assets to pay a distribution is not sustainable over the long term.

Fortunately, we have a very recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on August 31, 2023. This is one of the newest reports that we have available from any closed-end fund, and it is also more recent than the one that we had available the last time that we discussed this particular fund. That is nice because of the fact that interest rates really started to rise quickly in mid-July and this report will give us some insight into how well the fund managed to handle that particular situation.

During the six-month period, the Invesco Senior Income Trust received $34,344,476 in interest along with $845,876 in dividends from the assets in its portfolio. When we combine this with a small amount of income from other sources, we see that the fund had a total investment income of $35,374,638 over the six-month period. It paid its bills out of this amount, which left it with $25,915,991 available for shareholders. That was sufficient to cover the $23,107,642 that the fund distributed to its shareholders during the same period. Thus, the distribution should prove to be reasonably sustainable right now as the fund is simply paying out its net investment income. That is exactly what we like to see with any fund that invests in the fixed-income market.

With that said, the fund's net assets did decline during the period due to a significant amount of unrealized losses. The fund reported net unrealized losses of $53,956,069 over the course of six months, which were only partially offset by $3,952,742 net realized gains. The fund's net assets declined by $47,194,978 after accounting for all inflows and outflows during the period.

That is certainly very disappointing, but it is important to keep in mind that this was all due to unrealized losses. As such, they are not necessarily permanent and could be easily erased if the market becomes a bit more favorable. Overall, we should not worry here as the fund is bringing in more than enough money simply due to the coupon payments on its bond holdings to cover its distributions.

Valuation

As of October 25, 2023 (the most recent date for which data is currently available), the Invesco Senior Income Trust has a net asset value of $4.09 per share but its shares currently trade for $3.80 each. This gives the fund's shares a 7.09% discount on net asset value at the current price. That is a very reasonable discount that is quite a bit better than the 5.31% discount that the fund's shares have had on average over the past month. Thus, the current price is a very reasonable entry point for anyone interested in adding this fund to their portfolio today.

Conclusion

In conclusion, there could certainly be some very real reasons to recommend the Invesco Senior Income Trust to investors today. In particular, this is one of the few debt funds on the market that benefits from rising interest rates. Despite what some analysts say, it is very difficult to envision any scenario in which interest rates decline without inflation becoming a much bigger problem than it currently is. As such, it could be a good idea for investors to be holding something that benefits from rising interest rates and this fund certainly fits the bill. The fact that it manages to do this and still pay a very high and apparently sustainable yield makes it a rather attractive position right now.

For further details see:

VVR: Benefiting From Rising Rates And Boasting A Remarkable 13.6% Yield