VVR - VVR: Fully Funded 13% Yield But Shrinking NAV

2023-03-22 01:26:56 ET

Summary

- The VVR fund is a senior loan-focused closed-end fund.

- It pays a 13.1% fully-funded forward yield but only earns 3-5% average annual total returns.

- This discrepancy suggests the fund may be 'reaching for yield' and incurring permanent losses of principal in order to achieve high NIIs.

The Invesco Senior Income Trust ( VVR ) generates high current yield from a portfolio of senior secured loans. The fund pays a forward yield of 13.1% that appears fully funded from net investment income.

However, investors are cautioned that VVR's distribution rate is far beyond what is plausible for the asset class (senior floating rate loans) over a cycle. In fact, the fund's long-term average annual total returns are only 3-5%, suggesting the fund may be 'reaching for yield' in order to generate high NII but suffering losses of principal as a result.

Fund Overview

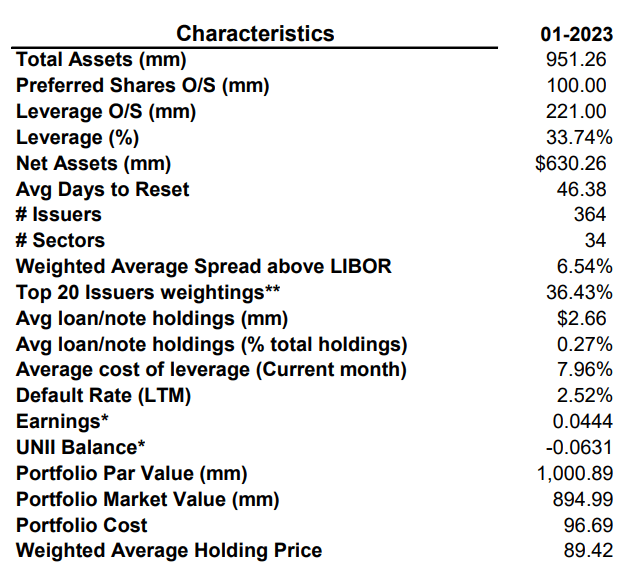

The Invesco Senior Income Trust ("VVR") is a closed-end fund ("CEF") that provides high current income from a portfolio of senior secured floating rate loans ("bank loans") and other fixed income securities. The VVR fund may use leverage to enhance returns. As of January 31, 2023, the VVR's effective leverage was 34% (Figure 1).

Figure 1 - VVR fund characteristic (VVR January 2023 factsheet)

{kind=link}

The VVR fund has $730 million in assets as of February 28, 2023, and charged an annualized 2.80% total expense ratio for the 6 months to August 31, 2022.

Portfolio Holdings

As seen from figure 1 above, VVR's portfolio contain loans from 364 issuers with the top 20 issuers accounting for 36% of the portfolio as of January 31, 2023. The gross portfolio value was over $1 billion although the carrying value was only $895 million.

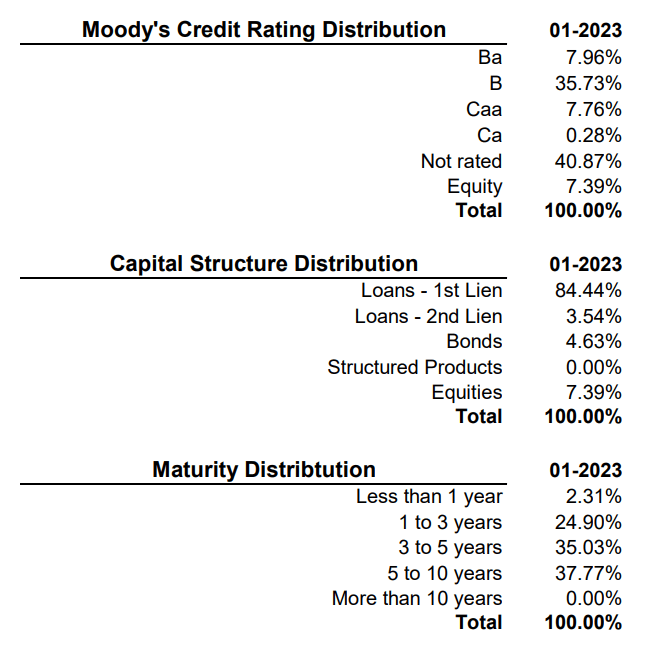

Figure 2 shows the asset allocation, credit quality allocation, and maturity distribution of VVR's portfolio. Senior 1st lien loans make up 84.4% of the portfolio while 2nd lien loans and bonds make up 3.5% and 4.6%, respectively.

Figure 2 - VVR portfolio characteristics (VVR January 2023 factsheet)

{kind=link}

Using Moody's credit ratings, VVR's portfolio is entirely non-investment grade ("junk") with 8.0% rated Ba, 35.7% B-rated, 7.8% rated Caa, and 40.9% not rated.

27.2% of VVR's portfolio has a maturity less than 3 years, 35.0% is 3-5 years, and 37.8% is 5-10 years.

Returns

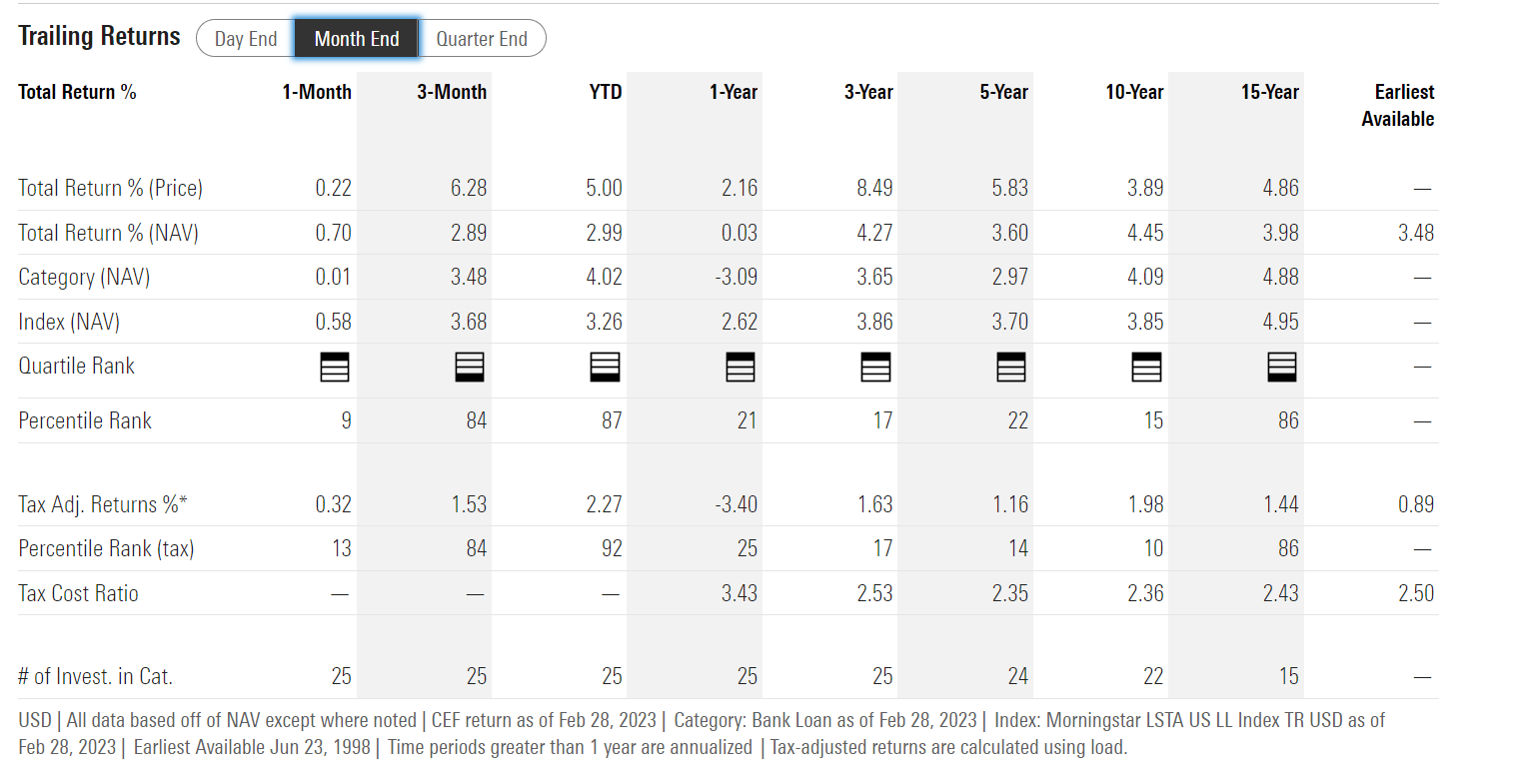

The VVR fund has delivered modest historical returns, with 3/5/10/15Yr average annual returns of 4.3%/3.6%/4.5%/4.0% respectively to February 28, 2023 (Figure 3). VVR has outperformed its peer group, consistently ranking in the top quartile within the Bank Loan category on Morningstar.

{kind=link}

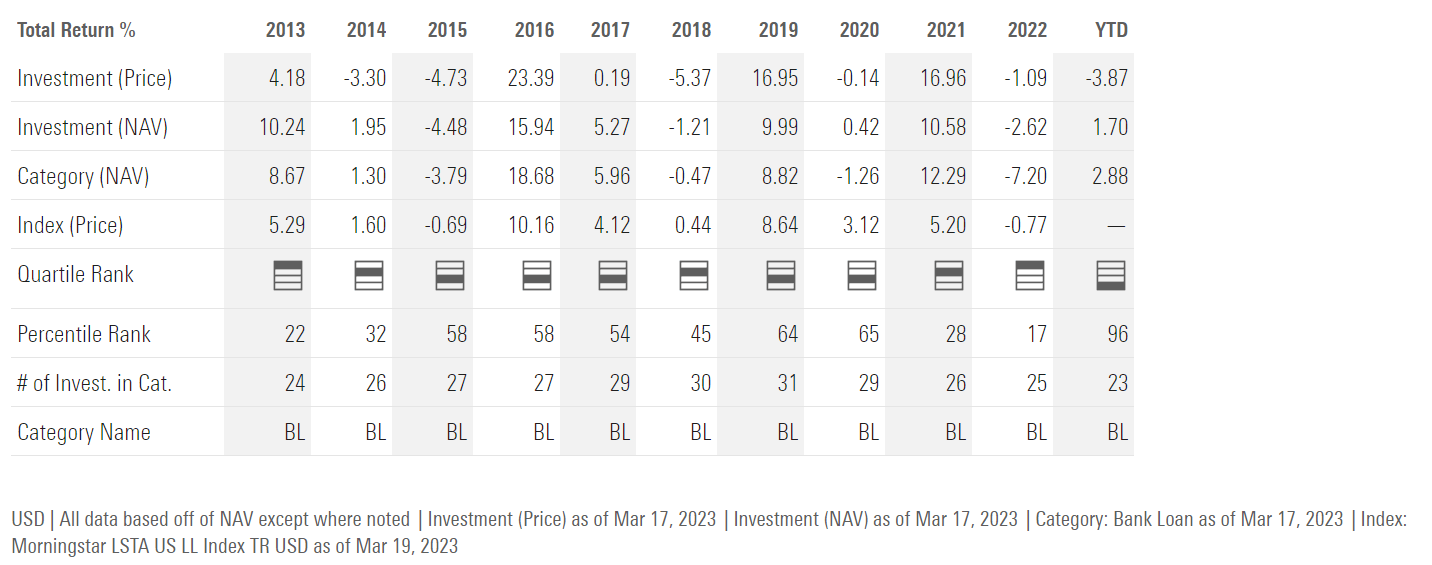

2022 was a weak year for VVR, with the fund returning -2.6% (Figure 4). Note that due to the floating rate nature of VVR's holdings, returns are driven by high yield credit spreads and should average mid- to high-single-digits over a cycle.

{kind=link}

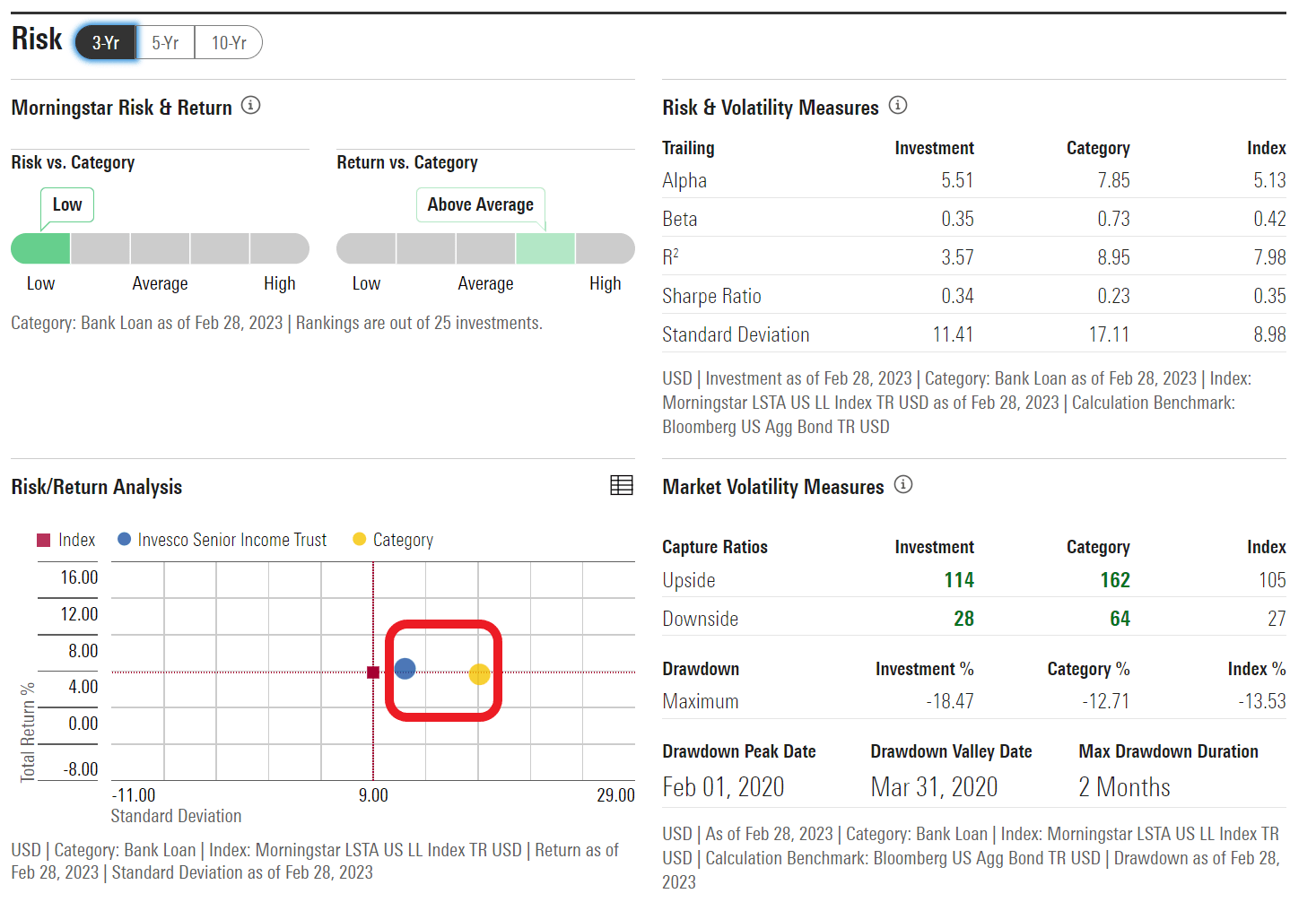

In terms of risk, VVR has consistently delivered above average returns and below average volatility against its peer group on 3, 5, and 10 Yr time horizons (Figure 5).

Figure 5 - VVR has delivered above average returns and below average risk (morningstar.com)

{kind=link}

Distribution & Yield

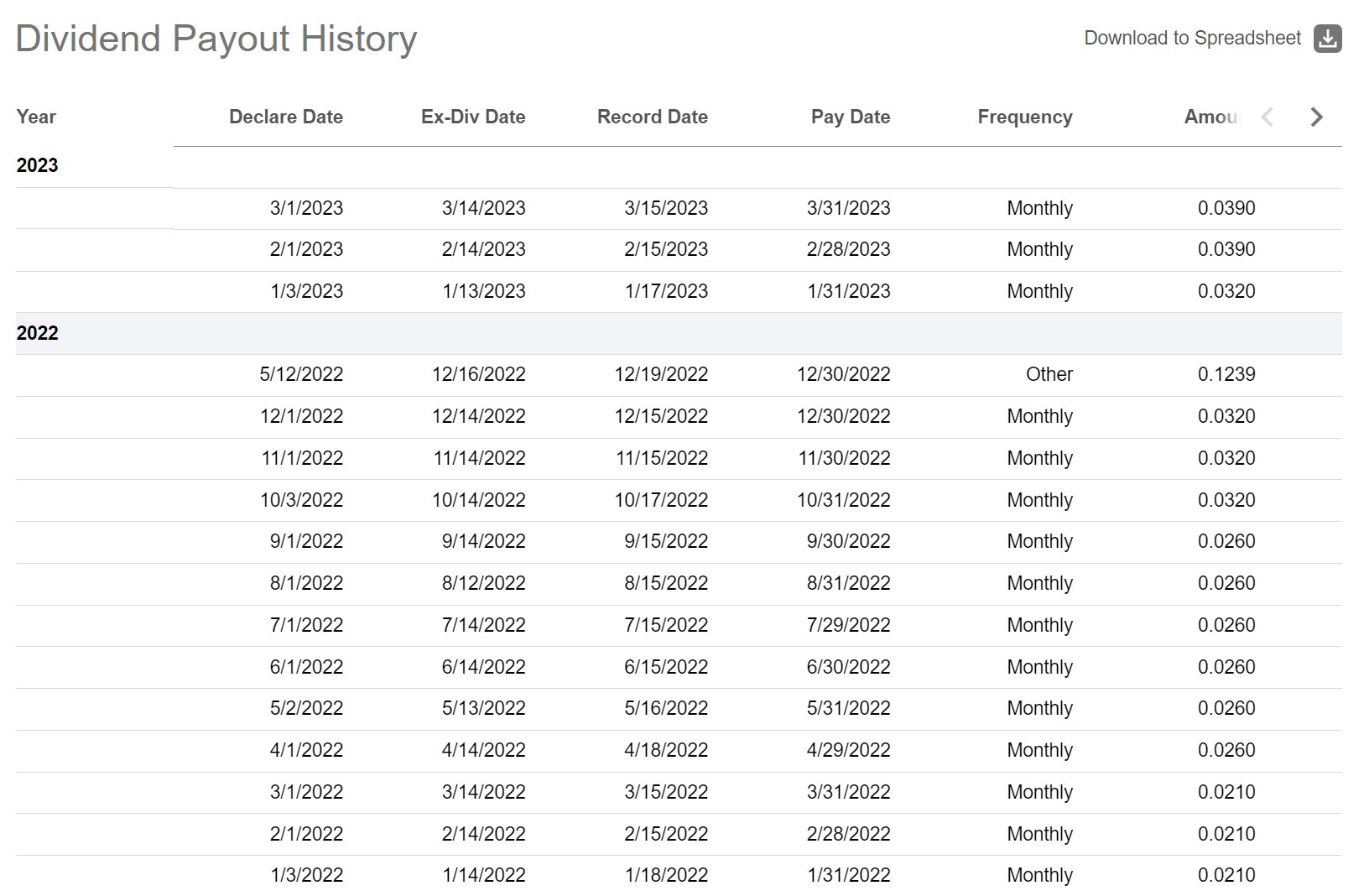

The VVR fund pays a high monthly distribution, currently set at $0.039 / share or a forward yield of 13.1%. On NAV, the fund is yielding 11.6%. Due to the floating rate nature of VVR's senior loan holdings and the rise in short-term interest rates, VVR's monthly distribution has been on an uptrend in the past few quarters, from $0.021 in early 2021 to the current $0.039 rate (Figure 6).

Figure 6 - VVR's distribution has been rising (Seeking Alpha)

{kind=link}

Generous Distribution Funded From NII

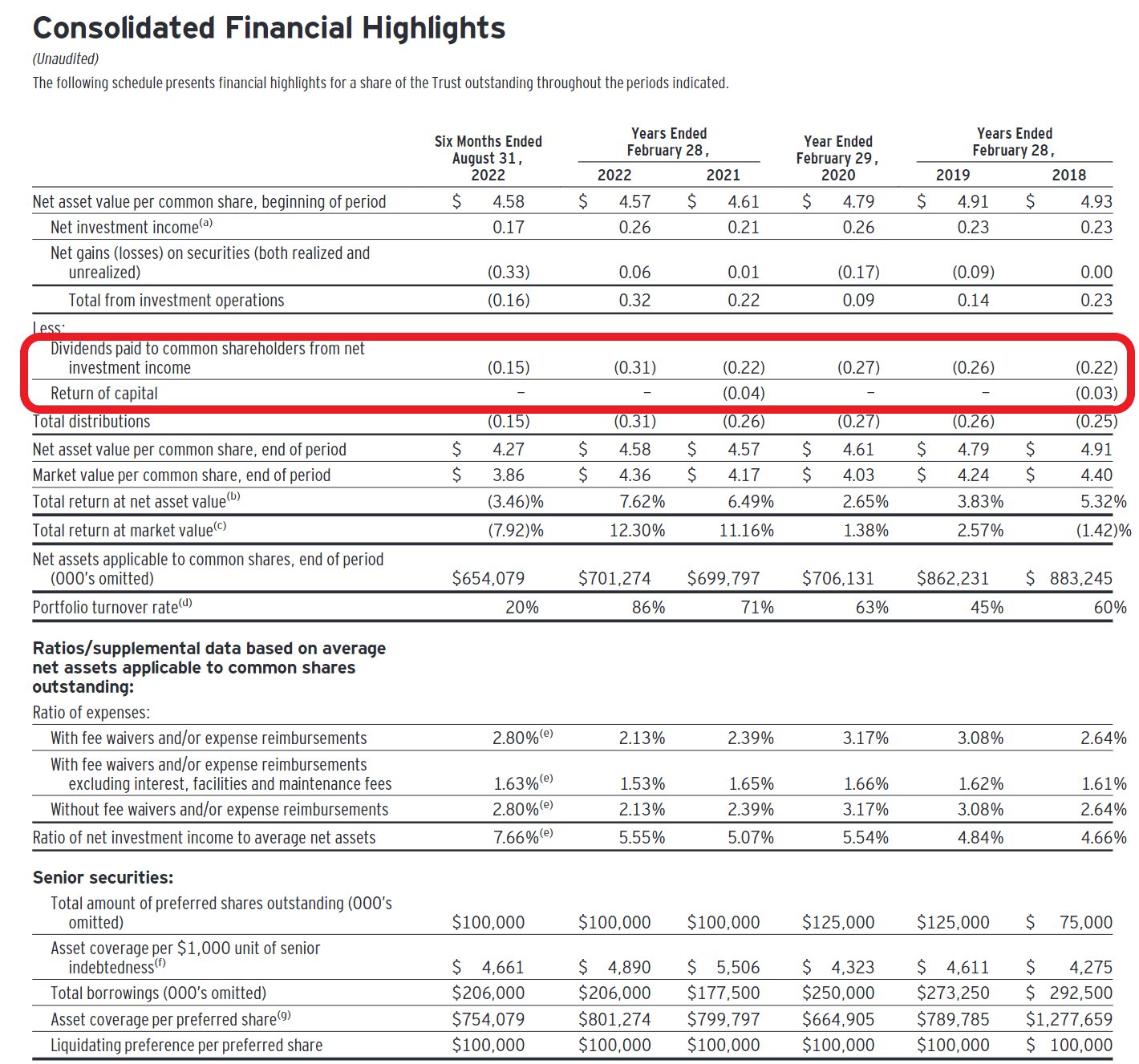

Historically, VVR's distribution has been funded out of net investment income ("NII") (Figure 7).

Figure 7 - VVR has historically funded its distribution from NII (VVR 2022 semi-annual report)

{kind=link}

But It Has An Amortizing NAV Problem

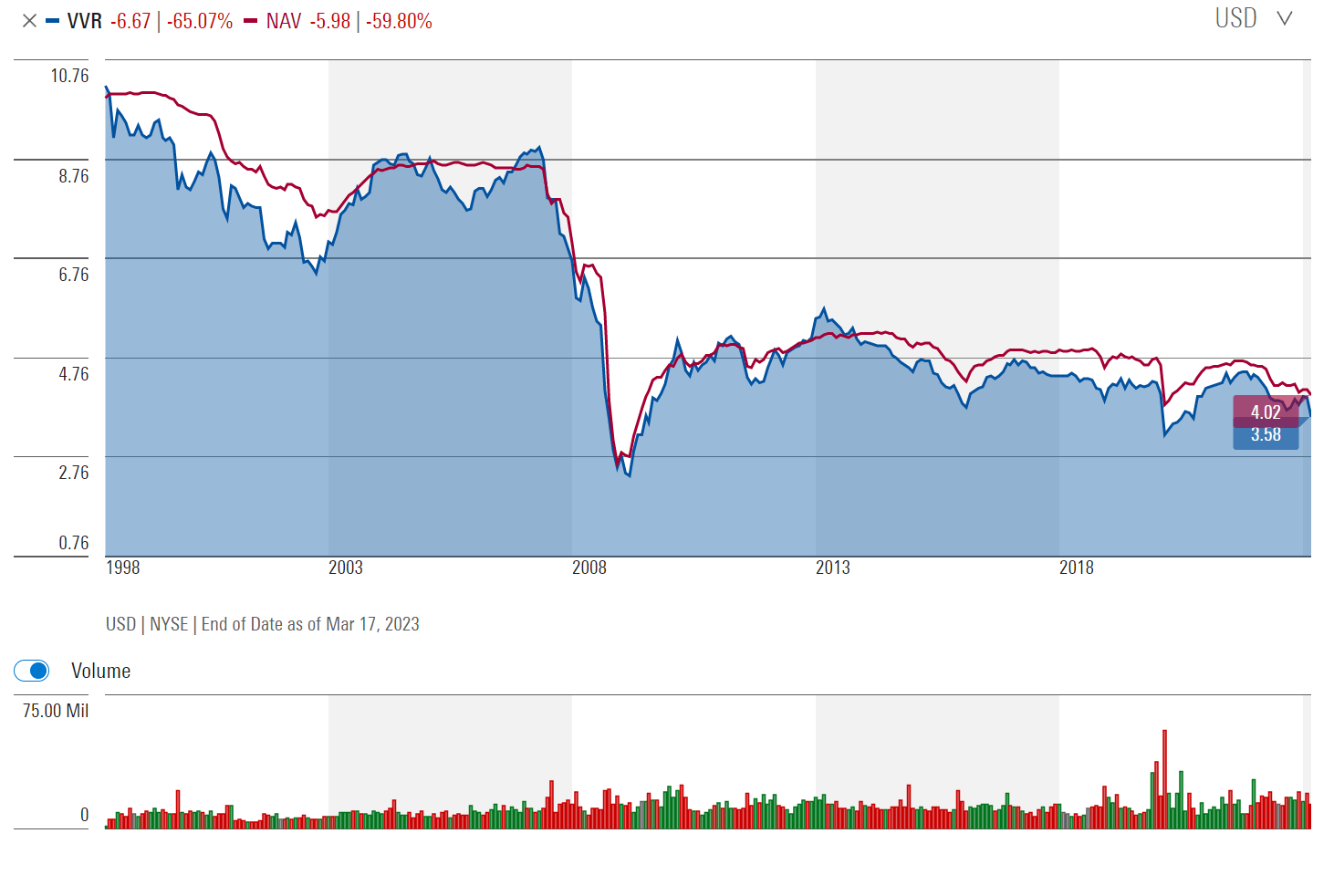

However, investors should note that the VVR fund has a long-term amortizing NAV, which is a characteristic of 'return of principal' funds that do not 'earn' their distributions (Figure 8). Mathematically, we can see that the VVR fund's distribution rate (11.6% of NAV) is far above the fund's historical average annual total returns (3Yr average annual total returns of 4.3%), despite the distributions being 'fully covered'. What could be going on?

{kind=link}

Theoretically, a portfolio of prudently selected senior loans should mature at par (less any defaults), so VVR's amortizing NAV is perplexing. VVR's trend of fully funded distribution but shrinking NAV is very similar to a number of senior-loans focused funds like the Apollo Senior Floating Rate Fund ( AFT ), the Apollo Tactical Income Fund ( AIF ), and the Blackstone Strategic Credit Fund ( BGB ) that I have reviewed in recent months.

Could The Fund Be Stretching For Yield?

Referring to figure 7 above, we can see that although the VVR fund has generated $1.36 / share in cumulative NII between 2018 to August 2022, the fund also suffered a cumulative $0.52 / share in realized and unrealized gains and losses in that time period.

The poor gains/losses performance suggests the VVR fund may be 'reaching for yield' and selecting poor investments that end up permanently impairing principal. So although the fund generates sufficient NII to fund its distribution, it also suffers from principal losses from credit events that detract from total returns.

Credit events do not have to be full on bankruptcies. A credit event could be a simple credit downgrade from the ratings agencies that cause an issuer's credit spread to widen and loans to fall in price. With the fund turning over 40-80% of its portfolio on an annual basis (from figure 7 above), the VVR fund could also be 'churning' loans in order to earn the highest NII to 'fully fund' its distribution yield, but crystallizing losses in the process.

Conclusion

The Invesco Senior Income Trust generates high current yield from a portfolio of senior secured loans. The fund is currently paying a 13.1% forward yield that appears fully funded from net investment income. However, investors are cautioned that the VVR fund has a troubling trend of long-term declining NAV caused by realized and unrealized losses on investments. This behaviour is not consistent with the mean reverting nature of credit investments and suggests the fund may be 'reaching for yield' and realizing losses in the process.

At the end of the day, senior loans are a direct play on high yield credit spreads. The asset class should generate mid- to high-single digit returns through a cycle, as confirmed by VVR's long-term average annual returns. The fact that VVR is paying a double-digit distribution yield well above what is plausible for the asset class should be a warning sign for investors.

For further details see:

VVR: Fully Funded 13% Yield, But Shrinking NAV