GPOR - W&T Offshore: Even The Bonds Are Undervalued - Buy

Summary

- WTI improved tremendously its financial situation in 2022.

- The credit markets don't appreciate it, even though the 2023 bonds can be settled in cash.

- The poor credit perceptions weigh down on equity too.

- WTI remains one of the most discounted U.S. producers on cash flow, EBITDA, and NAV basis.

- When the refinancing announcement inevitably comes, the equity should re-rate much higher.

Investment thesis

W&T Offshore ( WTI ) is one of the most undervalued U.S. oil and gas producers. While in recent years the company struggled with its high leverage, a lot of progress was made in 2022. However, this progress doesn't seem to be fully reflected by the credit markets, and that in turn pressures the equity valuation. The impending announcement of the refinancing solution should be a massive re-rating event.

Background

I have written about W&T before, so this article can be seen as update of my prior coverage:

W&T Offshore: Value Play Vs. Debt Trap

W&T Offshore Looks Promising After De-Risking Event, Recent Correction

W&T Offshore: Better Fundamentals; Excellent Buying Opportunity

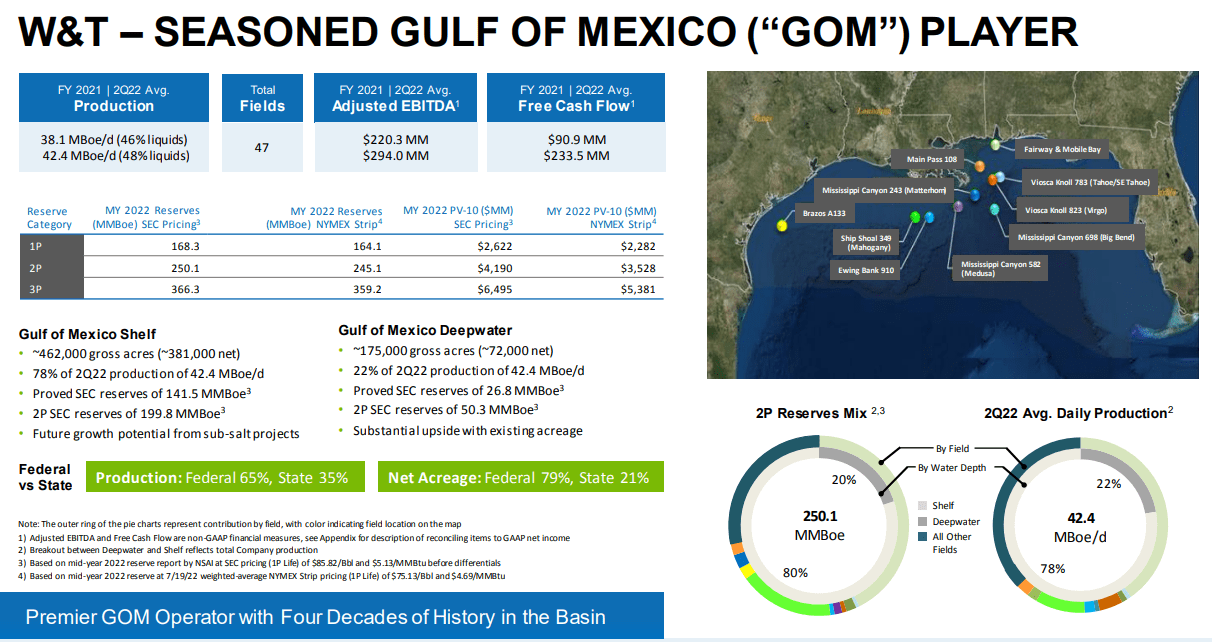

W&T has been a greatly discounted O&G producer, especially on net asset value basis. The company has offshore assets in the U.S. Gulf of Mexico, which, unlike onshore shale plays, are relatively long-lived. This means that W&T doesn't need as much capex to maintain production and is somewhat protected from oilfield services inflation:

{kind=link}

The valuation stands out

At $75 NYMEX strip, the company estimates 1P proved reserves PV-10 value of $2.2 billion; this is slightly more than twice the enterprise value, so you could say that W&T trades at 50% PV-10. For reference, IHS (behind paywall) cites a median price to NAV ratio of 99% for its midsize and small North American oil-focused E&P group, and that is based on $95 crude oil ( CL1:COM ) plus the NAV being augmented for unproved reserves.

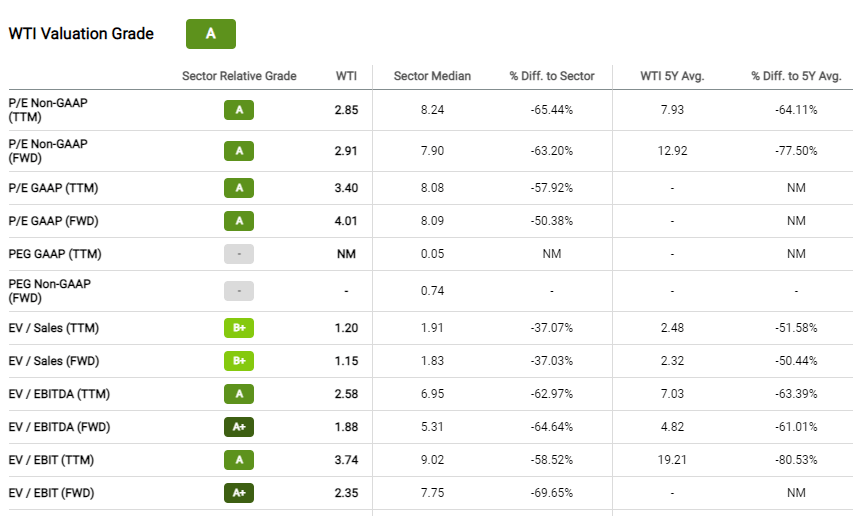

Seeking Alpha itself gives W&T an "A" on valuation:

{kind=link}

Note also the "A+" for enterprise value / forward EBITDA, which stands at 1.88x vs. over 5x for the sector.

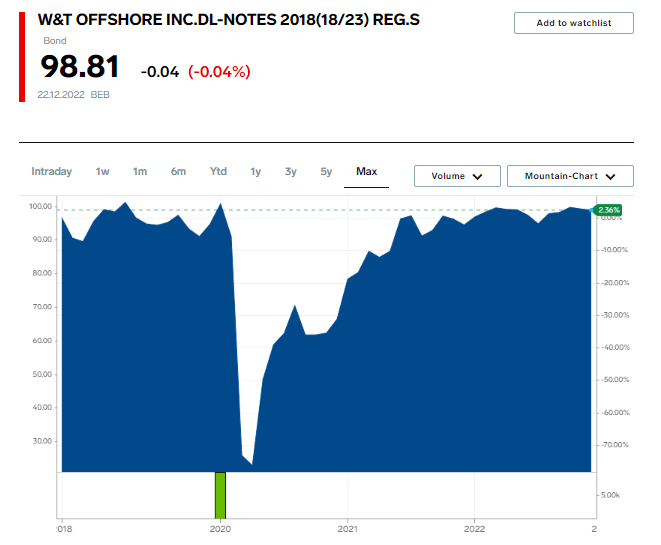

The 2023 Notes

Over the last few years W&T has struggled with its high leverage. The elephant in the room have been the 9.75% Second Lien Notes due on November 1, 2023:

{kind=link}

For quite a while, there was a question mark on W&T's ability to refinance. However, the company has made great progress towards this goal. In May 2021, the securitization of W&T's Mobile Bay assets effectively lengthened maturities and raised cash. In 2022, W&T continued increasing its cash balance and currently net debt is only 0.5x forward EBITDA.

On a flowing barrel basis, the de-leveraging is also obvious:

W&T Offshore Presentation

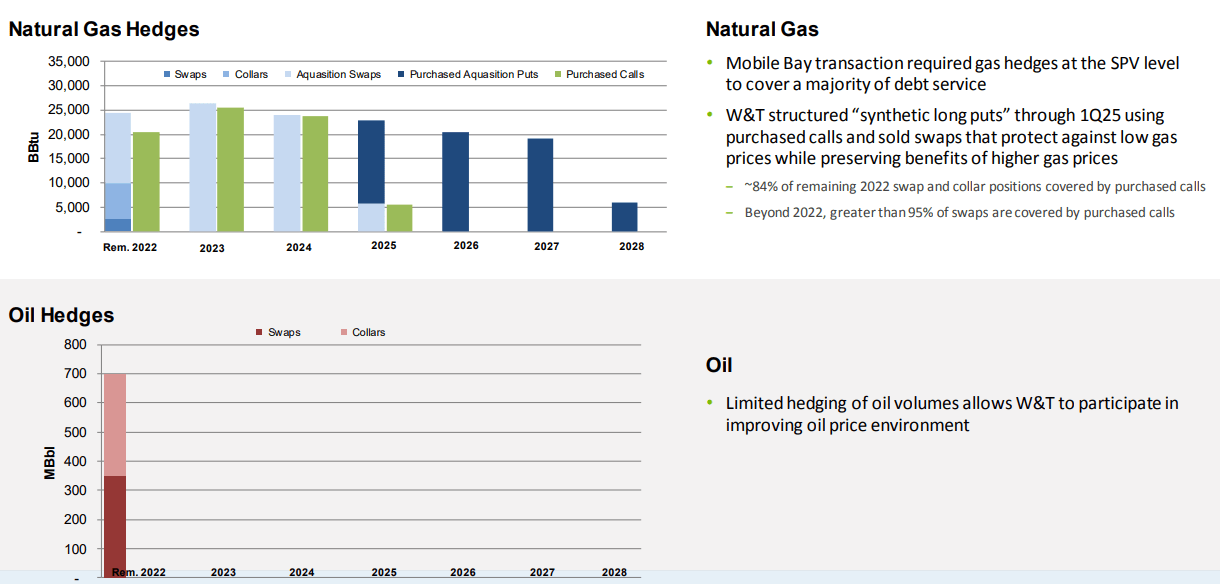

The hedging book looks a lot better

Besides the leverage, W&T was also dealing with unfavorable hedges. The good news is that from January 2023 the oil hedges are completely gone:

{kind=link}

The gas hedges remaining in place were a requirement for the Mobile Bay securitization transaction. These aren't favorable at about $2.50/mmbtu for 2023, but W&T has been able to offset some of the impact by purchasing call options. During 2022 Q3 W&T Offshore monetized a lot of these derivatives for $138 million in cash which significantly improved liquidity.

The credit markets are still unhappy

The 2023 Notes trade now at close to par, which is a big improvement from 2020-2021. However, these Notes were issued in not-so-good times at the end of 2018, during the "taper tantrum", and the 9.75% coupon is quite high for a healthy company.

Here is a comparison of W&T's credit spreads to those of a few other U.S. small-cap producers:

| Company |

| Net Debt / TTM EBITDA |

| Maturity |

| OAS (bps) |

| Rating |

| W&T Offshore ( WTI ) |

| 0.60x |

| Nov-23 |

| 652 |

| Caa2 |

| Earthstone Energy ( ESTE ) |

| 0.71x |

| Apr-27 |

| 507 |

| B3 |

| Laredo Petroleum ( LPI ) |

| 0.83x |

| Jan-25 |

| 525 |

| B3 |

| Gulfport Energy ( GPOR ) |

| 0.48x |

| May-26 |

| 415 |

| B3 |

| Kosmos Energy ( KOS ) |

| 1.29x |

| Apr-26 |

| 873 |

| Caa1 |

Source: Author's calculations

W&T's leverage is more like ESTE, LPI and GPOR and less like KOS. To me, W&T's bonds look undervalued by about 150 bps.

What more can W&T do?

The company has been overcommunicating that the 2023 bonds will be paid. CEO Tracy Krohn during the Q3 earnings call:

So in regard to our second - our senior second lien notes due November 2023, we continue to evaluate refinancing options. Should capital markets remain volatile, we're confident that we're able to repay these notes prior to maturity out of future expected free cash flows, our substantial cash on hand of $447 million and access to our unused $100 million aftermarket equity program. Additionally, we have $50 million in liquidity on our undrawn credit facility and natural gas calls that are currently worth $30 million to $40 million that can be monetized quickly...

With regard to the refi, we're in the enviable position of knowing that we can refi. It's not a matter of whether we can refi. We certainly can. Markets have been in flux here lately with increases in interest rates and bondholders being somewhat hesitant and the stock market being affected by the Fed speak, if you will. So we're being patient here and thinking that we know we can refi or worse - not a worst case, but one potential is that we just hang tight and we repay the debt over time.

So to pay $552 million, W&T has lined up $447 million in cash, $50 million available under an unused credit facility (which would be a loan from Tracy Krohn personally to the company), and may as last recourse issue $100 million in equity through its ATM program.

But the spreads suggest the credit market isn't fully convinced. This is unfortunate because it creates the perception of default risk and weighs down on the equity. It is possible that some of the W&T short interest is also driven by bondholders hedging their risk:

So ultimately we may need to wait for the official announcement. When that happens, I would expect significant re-rating.

The Holy Grail

From operational perspective, the refinancing situation is also a drag because W&T can't be as aggressive with its capex. Besides debt repayments, W&T also has to take care of its asset retirement obligations:

W&T's guidance range for capital expenditures in 2022 has been reduced to a range of $65 million to $75 million for the full year, which excludes acquisition opportunities. The reduction from the previously provided range of $70 million to $90 million reflects timing deferrals related to capital expected to now be deployed in early 2023 rather than late 2022 . Included in this range are planned expenditures related to one deepwater well and three shelf wells, as well as capital costs for facilities, leasehold, seismic and recompletions. The Company has significant flexibility to adjust its spending because it has no long-term rig commitments or near-term drilling obligations.

The guidance range for plugging and abandonment expenditures in 2022 is revised to between $65 million and $75 million. The Company spent $21.5 million on ARO settlements in the third quarter of 2022 and $61.3 million in the first nine months of 2022.

Namely, the potential spud date for block GB 783 A-4 "Holy Grail" will now be in 2023. As commenter @Phoenix_investor has pointed out under several Seeking Alpha threads, the Garden Banks block was part of the Entrada Field, which Callon Petroleum ( CPE ) was planning to develop back in 2008, but had to suspend its efforts due to the oil price crash. At that time, the probable reserves were estimated at 56 million boe, so this could be a significant add on to W&T, if it works out.

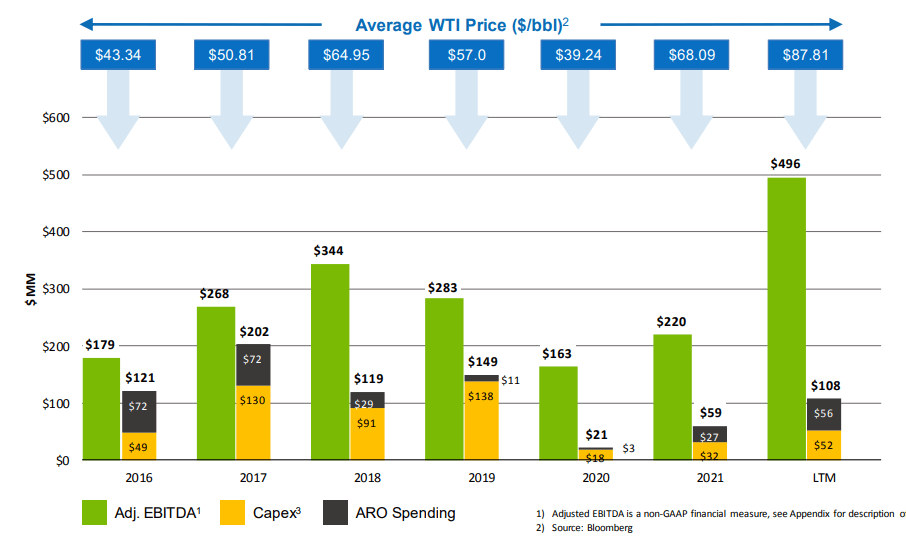

The Holy Grail capex will be around $80 million, which should be quite manageable with what W&T is making and spending so far:

{kind=link}

Conclusion

W&T Offshore is a significantly discounted U.S. offshore oil producer with big potential upside in 2023. The credit market is, unjustly in my view, pricing in some refinancing risk related to the company's 2023 debt maturities, and this in turn seems to be weighing down on the equity. Once the company announces its final plans for the 2023 Notes, a significant de-risking of both the debt and equity should occur, sending the stock price higher.

For further details see:

W&T Offshore: Even The Bonds Are Undervalued - Buy