TALO - W&T Offshore Is Near Long-Term Support And Offers An Option On Both Oil And Natural Gas

2023-07-03 09:35:19 ET

Summary

- W&T is fairly valued at strip pricing/2023 earnings, but the long-term reserve value is less appreciated.

- The stock has dropped to long-term support levels, but, unlike 2021, debt is currently not an issue.

- W&T offers upside optionality on both oil and natural gas prices; the Holy Grail drilling prospect remains a potential catalyst.

Investment thesis

W&T Offshore ( WTI ) hasn't done well since I last covered it in December; it has reverted to its 2021 levels when oil prices were similar:

The difference is that in 2021 there was much uncertainty whether W&T could refinance its 2023 Notes. Thanks to the cash flow lifeline from 2022, debt is no longer an issue. The notes were partially repaid, partially extended to 2026 and W&T Offshore reduced its annual interest expense from $70 million to about $44 million.

Despite some operational hiccups in Q1' 23 and the ongoing weakness in oil and gas prices, I project WTI to realize a 9.5% FCF yield on market cap in 2023 at strip pricing while EV is about 3.7x forward EBITDA. These are decent valuation metrics with much upside if either oil ( CL1:COM ) or natural gas ( NG1:COM ) edges up.

WTI appears even more discounted in reference to reserve measures; while the company is now lying low and being strategic about drilling its prospects or using its cash to acquire assets, it has the flexibility to ramp up capex and production as soon as the commodity outlook brightens.

At its current sub-$4 price, W&T offers optionality to the upside with limited downside; each visit to these levels in the past couple years has been followed by a bounce back. Even if oil remains weak, natural gas can also push up WTI despite the fact that the company's gas production is close to 60% hedged. The Holy Grail drilling prospect is also a dormant catalyst that can add a lot to production.

Why did W&T Offshore's stock drop?

For more background on the company, I would refer you to my prior coverage here . One reason for the weak performance were the operational issues in Q1 that impacted production:

The last call, we discussed that in the first quarter of 2023, we would have planned period out of facility and pipeline maintenance projects underway at the Mobile Bay field that required us to temporarily shut in the field. These activities shut in production at the Mobile Bay fuel for 35 days compared to 25 days that we estimated in the guidance range provided for the first quarter of 2023. We also experienced unplanned downtime at some non-operated fields that also temporarily reduced our production volumes in the first quarter. These 2 events contributed to the lower Q1 2023 production levels, but most of the non-operated fields that were shut in are now back online and the maintenance project at Mobile Bay was completed. Despite the lower overall production, our Q1 2023 oil production of 1.35 million barrels for the quarter was above our guidance range. Total company production has mostly recovered and we're currently having approximately 38,100 barrels of oil equivalent per day.

As oil veteran CEO Tracy Krohn explained further on the earnings call, these technical mishaps happen to everyone. The good news is the issues have been taken care of, and the company has affirmed its original 2023 production guidance.

Another reason for the stock's poor performance was likely the weakness in natural gas, which now represents 51% of the company's production volumes:

Ironically, the company's gas hedges, which were put in place as part of the Mobile Bay securitization deal and much berated during the 2021-2022 gas bonanza, helped W&T's bottom line with a $39 million unrealized derivatives gain.

The weakness in oil prices and the recessionary fears clearly haven't been helpful either, although I think the operational issues and gas pricing do explain why W&T did worse than other E&Ps:

Is W&T Offshore fairly valued now?

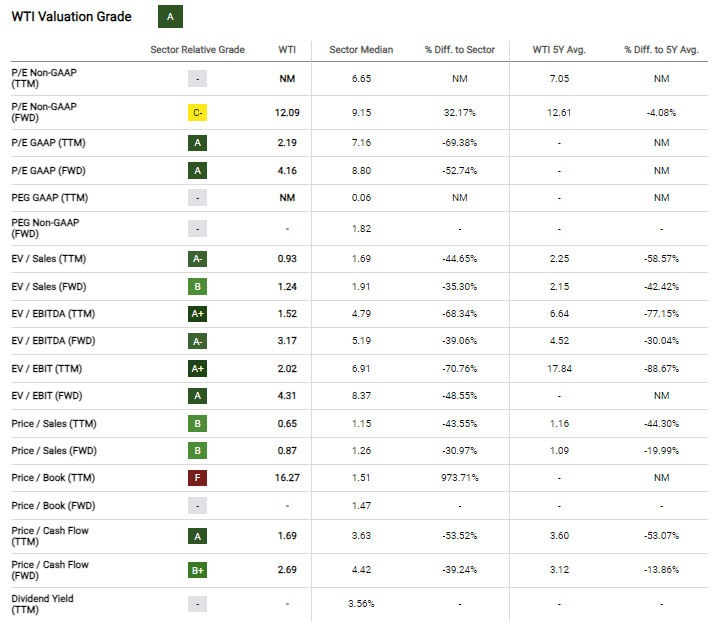

Seeking Alpha gives W&T an "A" valuation score:

{kind=link}

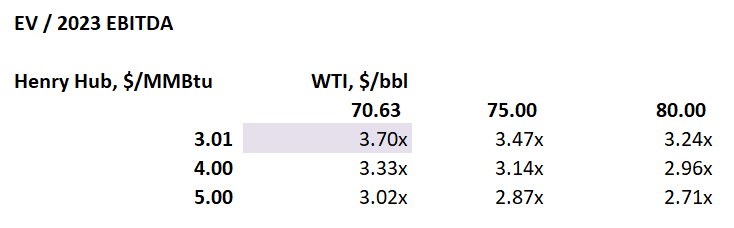

The problem with these valuation multiples is that we went from average $94 oil/$6.50 gas in 2022 to what so far looks like $70 oil/$2.50 gas for 2023. Based on the latest strip pricing for Q3 and Q4, to stay macro neutral, I arrive at a more conservative '23 EV/EBITDA of 3.70x (still cheap though compared to the sector average):

{kind=link}

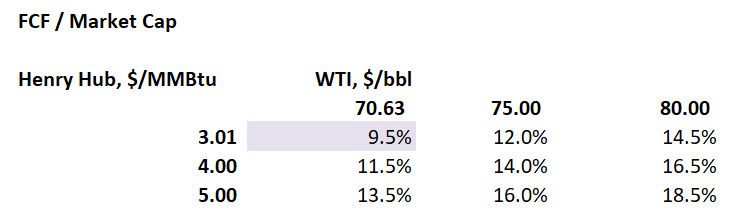

Here is how Q3/Q4 pricing may impact the '23 FCF yield:

{kind=link}

At strip pricing, the valuation looks fair, but a modest move up in either gas or oil could make it a lot more attractive.

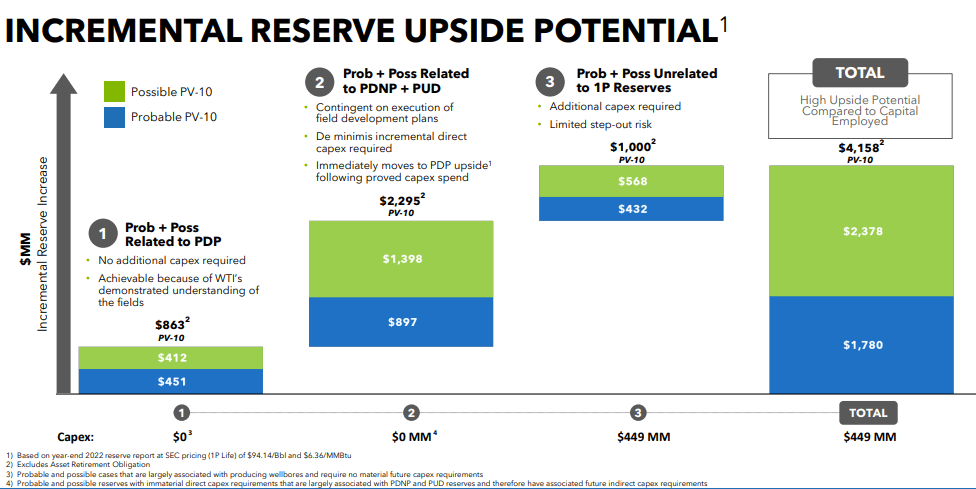

W&T's reserves will add long-term value

Focusing on 2023 makes sense as management provides guidance, but ultimately it is just one year. The long-term potential of an E&P company is perhaps better captured by its reserves and this is where W&T appears fairly discounted :

{kind=link}

Further, W&T can add some of its second party probable reserves into the first party basket with relatively little capex:

{kind=link}

This isn't necessarily true of its peers, especially the onshore ones that focus on shale plays.

I compared WTI to a couple other small caps that also have offshore focus, including Talos Energy ( TALO ), Kosmos ( KOS ) and VAALCO ( EGY ):

{kind=link}

*PV-10 here is instead the SEC Standardized Measure.

This is a tough comparison because the entire group is arguably undervalued when compared to onshore/shale. Nonetheless, W&T has the lower ratios. One reason is that it is much more gas-focused than the others and gas prices fell relatively more from 2022 to 2023, implying a larger discount to the YE '22 PV-10 values.

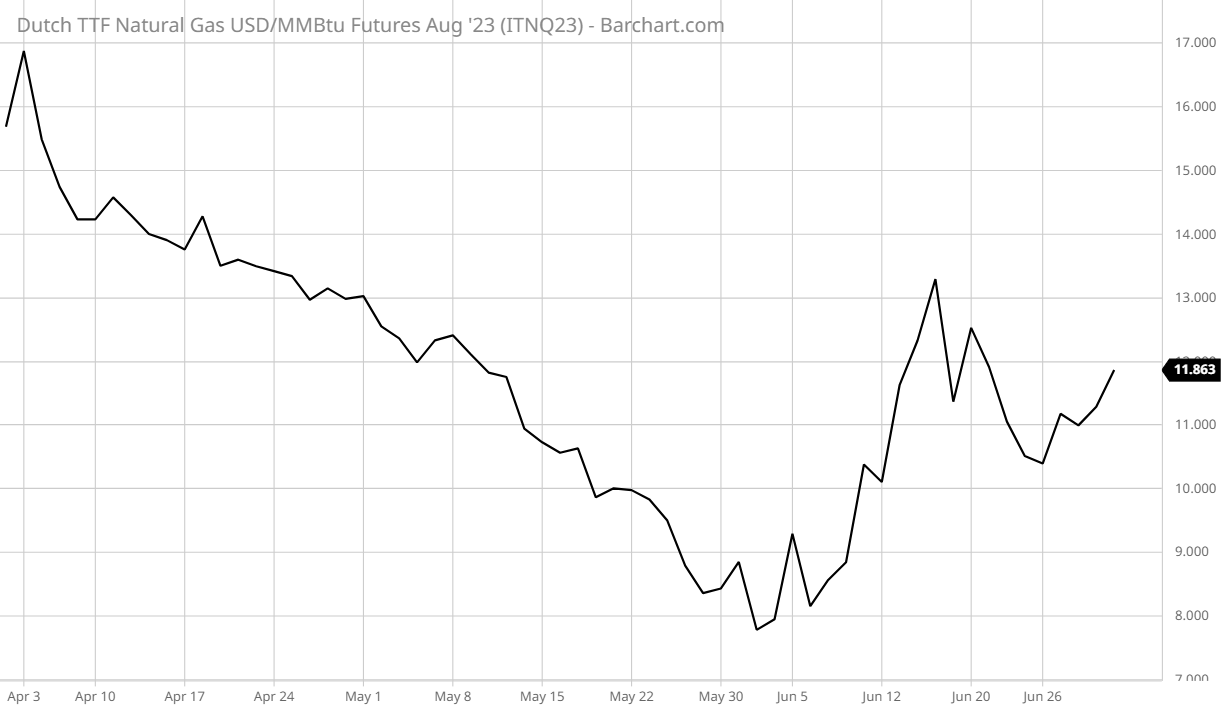

However, the gas focus may carry advantages too. Unlike oil, gas has already shown signs of a bottom:

European TTF futures are also up which will provide some support through U.S. LNG exports:

{kind=link}

If a nasty recession indeed materializes, oil may fall further despite Saudi Arabia's efforts . Gas demand will be more robust as much of it is power generation and heating related.

The Holy Grail may be a catalyst

W&T's drilling plans include block Garden Banks 783 A-4, aka the "Holy Grail", which was part of the Entrada Field that Callon Petroleum ( CPE ) was planning to develop back in 2008, but had to suspend its efforts due to the oil price crash. At that time, the probable reserves were estimated at 56 million boe, so this could be a significant add to W&T, if it works out.

The Q1 press release included a short update:

Front-end Engineering and Design and permitting processes are underway on the Holy Grail well at Garden Banks 783 in the Magnolia Field.

However, Tracy Krohn hinted that he may delay the decision whether to drill or use the cash to scoop up assets on the cheap through an opportunistic acquisition:

We continue to have the flexibility and dry powder to make additional acquisitions, drill our current prospects and continue to build cash, all while further paying down debt. Because we have no long-term rig commitments or near-term drilling obligations, we have flexibility to ramp up or defer capital opportunities.

This follows up on his Q4 comments on spudding the Holy Grail in 2023:

The reality is we're evaluating that. We're thinking maybe -- what maybe we defer on that for a while. I like the cash position we have. I think that maybe we have a better shot at buying reserves and we do a drilling form right now. And Holy Grail isn't going to go anywhere because it's proved reserves that we're drilling for. So apparently, those reserves have been there for a few million years. They can wait another year or so.

In a way, it's hard to disagree with Mr. Krohn. Deferring the drilling decision only adds optionality, and with 35% ownership of W&T (probably the highest management ownership ratio in the industry) he is clearly focused on long-term value creation. However, sooner or later the Holy Grail will come and that could be an awakening moment for the market.

Bottom line

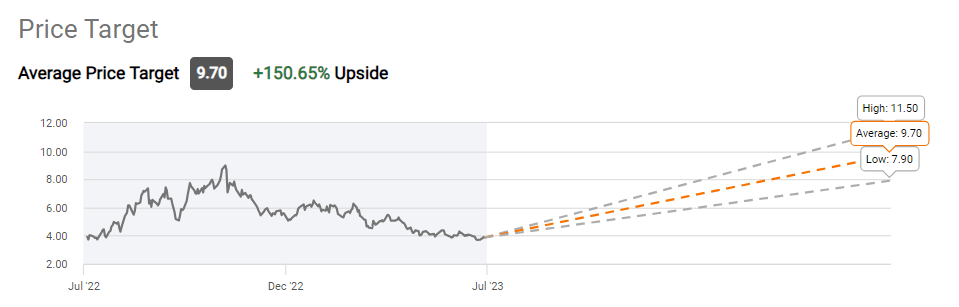

Wall Street gives W&T Offshore an almost $10 price target:

{kind=link}

It is rare that street analysts see a 3-bagger in an out-of-favor small-cap oil stock. I believe the low estimate is from an analyst at Stifel and the latest update was to $7.90 from May 30 .

I personally can't justify the street target without a return to 2022 oil pricing or the Holy Grail happening sooner than what the earnings calls suggest, but I still see this as a "buy" going to $5 or $6. We just need some stabilization in oil and natural gas to move into the $3 to $4 range.

Short interest has also been trending down and in the past this has signaled reversals:

In conclusion, W&T has hit a level where the downside is getting limited while there is plenty of optionality on the upside plus a dormant catalyst. However, like much of 2021, this may also trend sideways between $3-$4 for quite a while until something interesting happens.

For further details see:

W&T Offshore Is Near Long-Term Support And Offers An Option On Both Oil And Natural Gas