WTI - W&T Offshore: The Current Weakness Creates A Buying Opportunity

2023-03-18 07:57:49 ET

Summary

- Following the record 2022, the shares of W&T Offshore are sliding on falling oil and gas prices.

- The company will postpone the much anticipated spudding of the Holy Grail well.

- There’s still no indication of initiating a shareholder return program, despite the improving financial position.

- I estimate that in the current price environment, WTI should be able to generate around US$150M of cash flow – more than enough to fund its 2023 CAPEX.

- Reserves continue to grow, positioning the company in an excellent position to benefit from potential future oil and gas price increases.

Recently, W&T Offshore (WTI) released its annual results and 2023 guidance. The figures revealed a record-breaking performance in 2022 and significant balance sheet improvement. However, following a strong start of 2023, in the last month the share price is sliding on deteriorating oil and gas prices. The latest conference call revealed that a much anticipated expansion project will be postponed and there was no mention of initiating a shareholder return program. On the other hand, WTI expanded its reserves yet again and I estimate that even in today's price environment it will have no problem self-funding its 2023 CAPEX. With one of the highest insider ownership percentages amongst energy firms, WTI is clearly more focused on the long-term, which could lead to considerable reward for patient investors. On the other hand, WTI may not be the optimal choice for income oriented investors or those looking for a short-term upside triggers.

Record-breaking 2022

2022 highlights (WTI)

{kind=link}

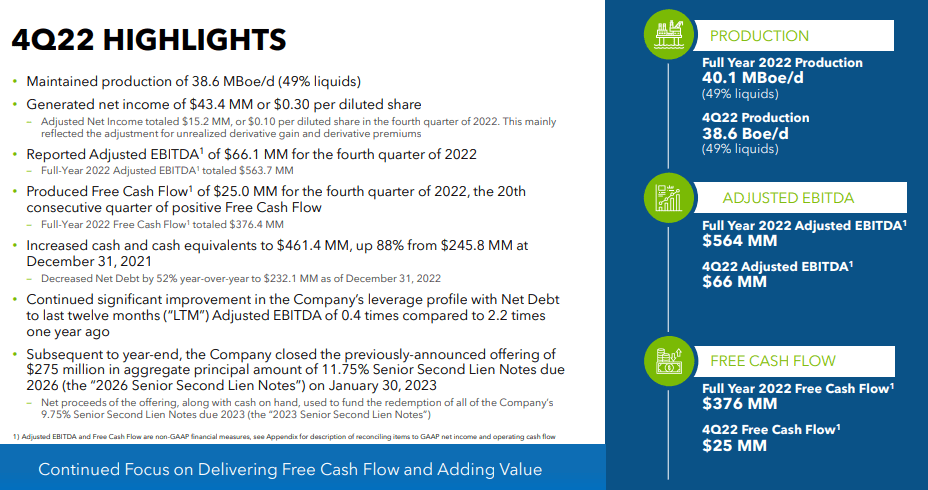

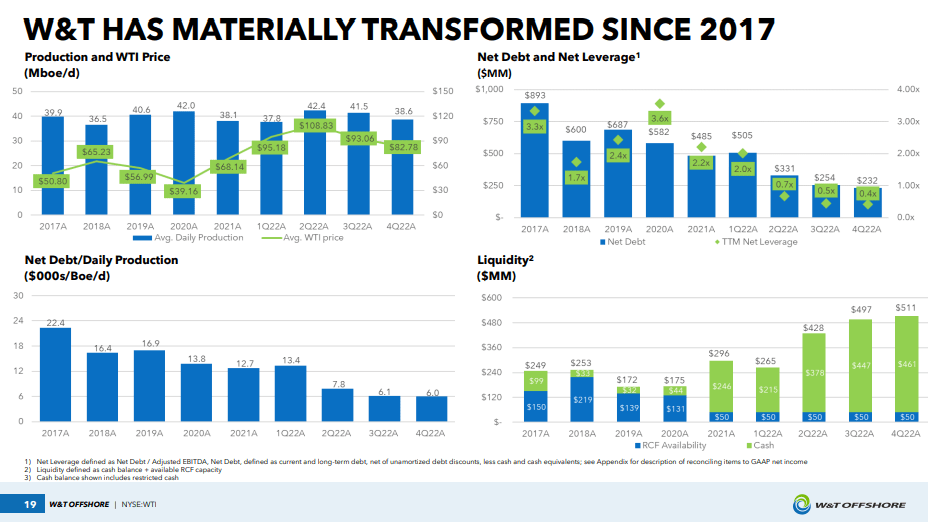

2022 has been an amazing year for WTI. The company benefited from elevated oil and gas prices as well as the opportunistic monetization of natural gas calls of US$146.1M. As a result, annual EBITDA skyrocketed 156% YoY to US$563.7M. Free cash flow amounted to US$376.4M more than quadrupling YoY. This allowed the company to significantly improve its balance sheet with net debt melting from US$485.1M in the beginning of 2022 to US$232.1M as of year-end.

Production and financial strength (WTI)

{kind=link}

In terms of production, the company achieved full year production rate of 40.1kBOE/day (49% liquids), but the Q4'22 number was slightly lower at 38.6kBOE. These numbers are in line with what WTI has been producing in the last 5 years.

Some bad news for shareholders

Alongside the great full year and Q4'22 revenue and earnings beat came in the earnings call , which was a sobering experience for shareholders. It turns out, that the much anticipated spudding of the Holy Grail well, which was expected to deliver considerable increase in production, will be postponed, according to the CEO of WTI - Tracy Krohn:

We're thinking maybe -- what maybe we defer on that for a while. I like the cash position we have. I think that maybe we have a better shot at buying reserves and we do a drilling form right now. And Holy Grail isn't going to go anywhere because it's proved reserves that we're drilling for. So apparently, those reserves have been there for a few million years. They can wait another year or so...

So apparently, WTI will likely spend its cash pile on acquisitions instead of developing the Holy Grail this year. Also, nothing about initiating a shareholder return program was even mentioned. This is a bit discouraging, as the successful spudding of the Holy Grail well and returning value to shareholders would've been a potential significant upside triggers. As most energy companies are distributing dividends and/or repurchasing their stock, income oriented investors will naturally be turned away from WTI.

2023 guidance

2023 guidance (WTI)

{kind=link}

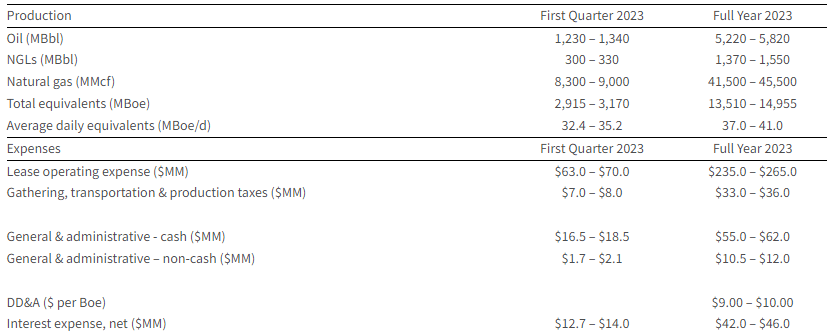

The 2023 guidance suggests some deterioration in production, as the guidance midpoint of 39kBOE/day is lower than the 40.1kBOE/day achieved in 2022. In terms of revenue, I expect much larger deterioration as the one-off derivatives monetization gain and the considerably lower prices of oil and gas will weigh in negatively. Assuming the midpoint of guidance and using the current pricing environment of WTI price of around US$70/barrel and natural gas price of around US$2.5/mmbtu I estimate that the company could generate around US$150M of pre-CAPEX free cash flow (US$1.04/share), which will be more than enough to cover the projected CAPEX of US$90M-US$110M.

Cash flow/share sensitivity to oil and natural gas prices (author's own estimates)

In order to test the sensitivity of the cash flow/share to oil and natural gas prices, I performed a sensitivity analysis.

Valuation

I expect energy prices to rise again soon, given the chronic underinvestment in oil and gas exploration and development and the industry being the favourite target of activists and politicians in the West. US natural gas prices for example could receive a boost by expanding the export capacity through building more LNG infrastructure. This makes companies like WTI, where natural gas is a significant part of the production mix, positioned very well to benefit.

2022 reserves (WTI)

{kind=link}

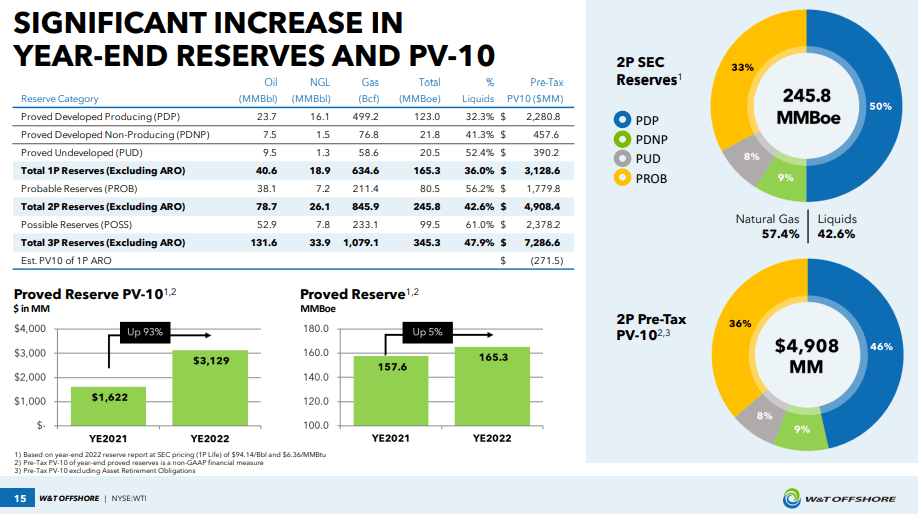

Still, even in the current price environment, with a market cap of US$700M, WTI should have cash flow yield of around 20%, which leaves room for share price appreciation. The company has been very successful at not only replenishing, but even expanding its resource base.

Proved reserves economics (WTI)

The company has reported significant increase in the estimated after-tax NPV of its proven reserves to US$2.3B (+95.7% YoY). For reference, the current EV of the company is around US$930M. Note, that the price assumptions for the calculation were considerably increased, compared to the 2021 figures. The 2022 calculations used oil price of US$94.14/barrel and natural gas price of US$6.36/mmbtu, compared to US$66.55/barrel and US$3.60/mmbtu. While the latest inputs seem quite ambitious, considering the current price environment, if the energy crisis resumes again, they could easily be reached.

Takeaway

WTI has been hit by falling oil and gas prices. However, the company could generate significant cash flows even in the current price environment, covering its 2023 CAPEX with ease. While the postponement of the Holy Grail well spudding and the lack of dividends/buyback are discouraging to some investors, WTI's management appears to be oriented towards long-term value generation as the emphasis is put on expanding reserve base. This may turn out to be rewarding for long-term investors and the current weakness in share price could be viewed as an accumulation opportunity.

For further details see:

W&T Offshore: The Current Weakness Creates A Buying Opportunity