WTI - W&T Offshore: Very Good News Might Only Be Weeks Away (Rating Upgrade)

Summary

- W&T Offshore, Inc. prudently seized upon the booming oil prices of 2022 to clean up their balance sheet.

- Despite oil prices sliding lower, this has continued since conducting my previous analysis with their net debt plunging.

- W&T Offshore could hit zero net debt later in 2023 and, excitingly, they are repaying and refinancing their problematic debt maturity.

- I suspect this will unbind the hands of management, thereby allowing them to either reinstate shareholder returns or grow their company bigger via acquisitions.

- Either way, this builds upon my previous thesis, and with the W&T Offshore, Inc. share price modestly lower, I believe that upgrading to a strong buy rating is now appropriate.

Introduction

The once-struggling oil company, W&T Offshore, Inc. ( WTI ) benefitted immensely from the booming oil prices of 2022, and thanks to prudent capital allocation, left their shares alike to a coiled spring ready to jump higher, as my previous article highlighted. In the following months, they have continued making prudent moves regarding their debt, and as they approach their upcoming results for the fourth quarter of 2022, I suspect very good news might only be weeks away.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and, importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

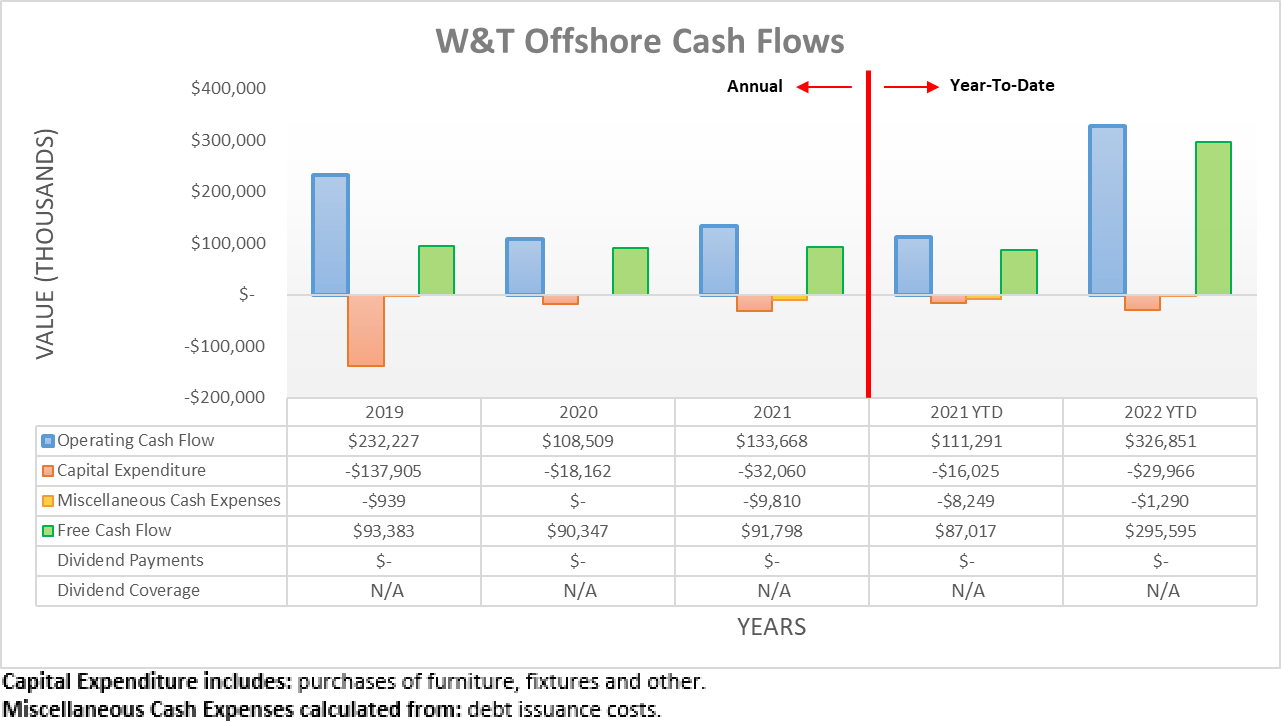

After seeing their operating cash flow surge during the second quarter of 2022 thanks to the booming triple-digit oil prices, unsurprisingly, it subsequently moderated as oil prices began sliding lower. As a result, their operating cash flow across the first nine months climbed to $326.9m, and whilst this is almost three times higher year-on-year versus their previous result of $111.3m during the first nine months of 2021, it nevertheless marked a slowdown versus the second quarter of 2022.

{kind=link}

This dynamic is more easily visible when viewing their operating cash flow on a quarterly basis with the third quarter of 2022 seeing a reported result of $89.1m and thus moderated versus the $210.2m observed during the second quarter. That said, their result for the third quarter was still solid historically speaking, and apart from the second quarter, it was actually their highest result since at least the beginning of 2021. To make this even better, the third quarter was not materially skewed by working capital movements and still produced $84.6m of free cash flow, thanks in part to their continued minimal capital expenditure.

Whilst the third quarter of 2022 was largely unaffected by working capital movements, this nevertheless means they have still not reversed their working capital builds of $52.8m and $24.9m during the first and second quarters, respectively. Since their working capital builds and draws during 2021 largely netted out, this effectively sees more than $70m of latent capacity for a cash infusion that in theory should land during subsequent quarters, thereby further helping clean up their balance sheet and, as I suspect, help make way for very good news in the coming weeks.

{kind=link}

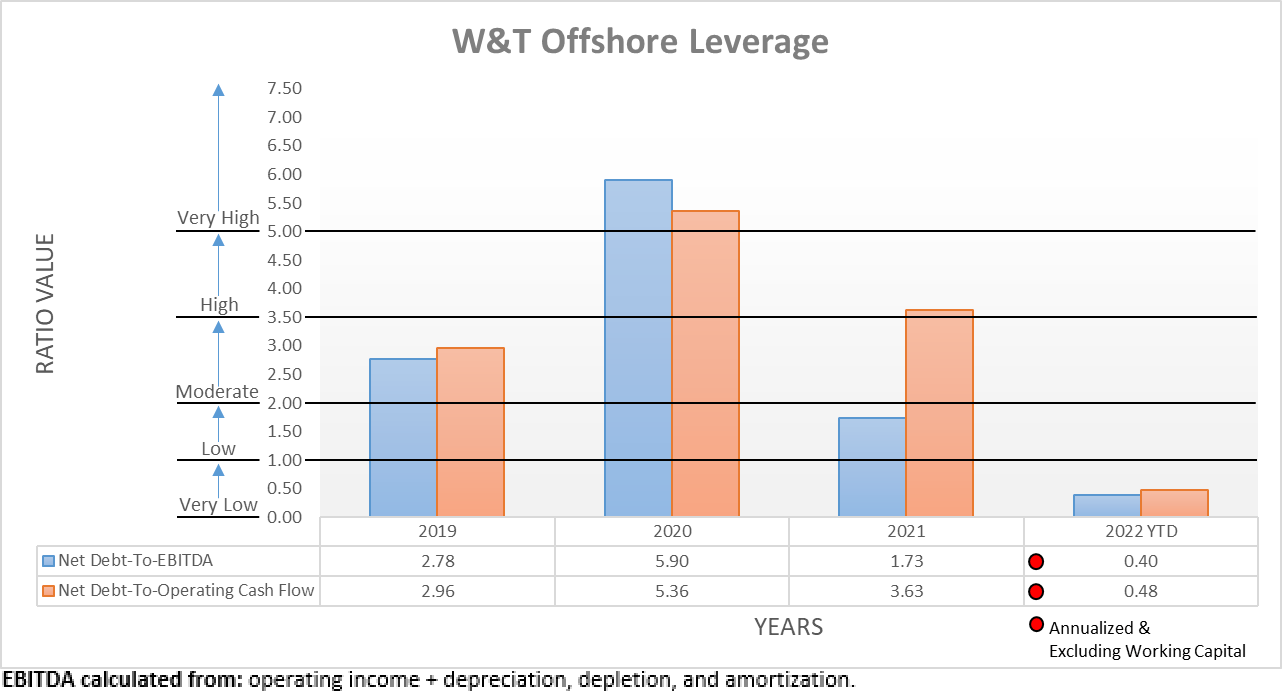

When looking at their capital structure, it saw further improvements during the third quarter of 2022 despite their cash flow performance moderating with net debt landing at $254.3m, which is down a very impressive circa 23% versus its previous level of $331.4m following the second quarter. When looking ahead, their upcoming results for the fourth quarter should see their net debt plunge even lower, likely to sub-$200m, especially if they release the latent cash from their aforementioned working capital build.

Since they can shave away $50m+ of net debt per quarter even with oil prices moderating, herein lies one of the two reasons why I expect that very good news might only be weeks away. Namely, unless they ramp up their shareholder returns during 2023, they will likely end the year with zero debt and possibly even reach this point not far past the middle of the year, depending upon future oil prices and working capital movements. When a company carries zero net debt, they have no choice other than shareholder returns or alternatively, pursue acquisitions that materially grow their company and thus, in theory, push their share price higher if executed prudently. In light of this outlook, it would be redundant to reassess their leverage or debt serviceability in detail, especially with only one quarter having elapsed since conducting the previous analysis.

The two relevant graphs are still included below to provide context for any new readers, which to no surprise shows their leverage continues heading lower with their net debt-to-EBITDA now at 0.40 and their net debt-to-operating cash flow not far behind at 0.48, thereby both sitting beneath the threshold of 1.00 for the very low territory. Concurrently, their healthy debt serviceability persisted with interest coverage of 7.25 and 5.95 when compared against their respective EBIT and operating cash flow. If interested in further details regarding these topics, please refer to my previously linked article.

{kind=link}

{kind=link}

{kind=link}

When looking at W&T Offshore, Inc.'s liquidity, it continued powering ahead during the third quarter of 2022 as their cash balance climbed higher to $447.1m versus its previous level of $377.7m following the second quarter. As a result, their respective current and cash ratios climbed in tandem to 1.60 and 1.17 versus their previous respective results of 1.43 and 0.98 across these same two points in time.

Even more excitingly, this additional cash is being utilized to proceed with a mixture of repaying and refinancing their once problematic debt maturity that is slated to come due in November 2023, which represents the second reason why I expect very good news might only be weeks away. When conducting the previous analysis, I flagged the repayment or refinancing of this debt as a catalyst for the commencement of shareholder returns or if not, acquisitions that grow the company and thus as a result, their free cash flow. Since this debt maturity, being their senior second lien notes, represents almost the entirety of their debt structure, it significantly unbinds the hands of management once removed from their debt structure.

W&T Offshore Q3 2022 10-Q

Once repaid and refinanced, its previous $552.5m balance drops to only $275m and does not come due until 2026, thereby being much more manageable, along with their $157m term loan that does not mature until May 2028. Whilst they have not mentioned shareholder returns, at least it seems acquisitions are on their radar as their debt plunges, as per the commentary from management included below.

"I like the way the company looks right now with our balance sheet and it feels good to be in a position where you can pay off all the debt as well or carry it further into the future with a modest amount of debt and leverage by making accretive acquisitions."

-W&T Offshore Q3 2022 Conference Call.

Whilst they have not mentioned dividends nor share buybacks anytime recently, I have a hard time imagining that upon seeing zero or near zero net debt, they will only pursue acquisitions. Partly because management cannot count on simply finding suitable assets or companies to acquire at any given moment, as this depends upon what is available for sale and competing bids. Plus, their commentary makes it seem they are open to operating with some degree of leverage and since acquisitions increase their financial performance, they can carry more debt without necessarily pushing their leverage higher. In turn, they do not need to hold back every dollar of free cash flow waiting for the right acquisition, thereby facilitating shareholder returns, especially in this era when oil and gas companies are more focused on returning cash to shareholders, generally speaking.

Conclusion

Either way, W&T Offshore, Inc.'s net debt is plunging towards zero, and they are in the process of repaying and refinancing their most problematic debt maturity. I once again expect this to act as a catalyst to see very good news in the coming weeks when announcing their upcoming results for the fourth quarter of 2022. Even if my expectations are wrong and W&T Offshore, Inc. only pursues acquisitions instead of shareholder returns, these should help propel their free cash flow even higher and given their rapidly diminishing net debt, they should not require dilutive equity issuances. In light of this outlook building upon the thesis laid out in my previous analysis, I believe that upgrading my previous buy rating of W&T Offshore, Inc. to a strong buy rating is now appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from W&T Offshore's SEC Filings , all calculated figures were performed by the author.

For further details see:

W&T Offshore: Very Good News Might Only Be Weeks Away (Rating Upgrade)