ASTE - Wabash National Corporation: A Ride That's Still Not Over

Summary

- Wabash National Corporation has had a great run over the past several months, with strong sales and growing backlog pushing the stock higher.

- Profits and cash flows continue to climb, and the 2023 fiscal year is likely to be even better.

- Add in how cheap shares are, and the firm does seem to offer even more upside potential moving forward.

One of the disadvantages of running a very concentrated portfolio is that you will often come across companies that you believe have excellent potential but that you ultimately pass on, only to see significant share price appreciation. One really great example that I can point to here involves a firm called Wabash National Corporation ( WNC ). Even at a time when the broader market has declined, shares of this particular business have roared higher, more than doubling in price. This has come on the back of strong fundamental performance and rosy guidance about what the future holds. Naturally, some investors may be inclined to take these profits and run. But if management can at least keep operations as profitable as they have been, then some additional upside could very well be warranted from here. As such, I've decided to keep the 'buy' rating I had on the stock previously.

A change of fortune

Back in late September of 2021, I wrote an article discussing the investment worthiness of Wabash National. At that time, I felt as though, from a fundamental perspective, the company was not particularly great. Even so, I concluded that it wasn't bad either. The firm was showing signs of a turnaround after what had been a fairly difficult year and the overall trajectory of the business was positive. On top of this, shares were trading at attractive levels, making it a prospect that could deliver some good returns. All combined, this made me rate the business a 'buy', reflecting my belief that shares should outperform the broader market for the foreseeable future. Fast forward to today, and the S&P 500 is down 5.5%. By comparison, shares of Wabash National have generated a return for investors of 100.7%.

{kind=link}

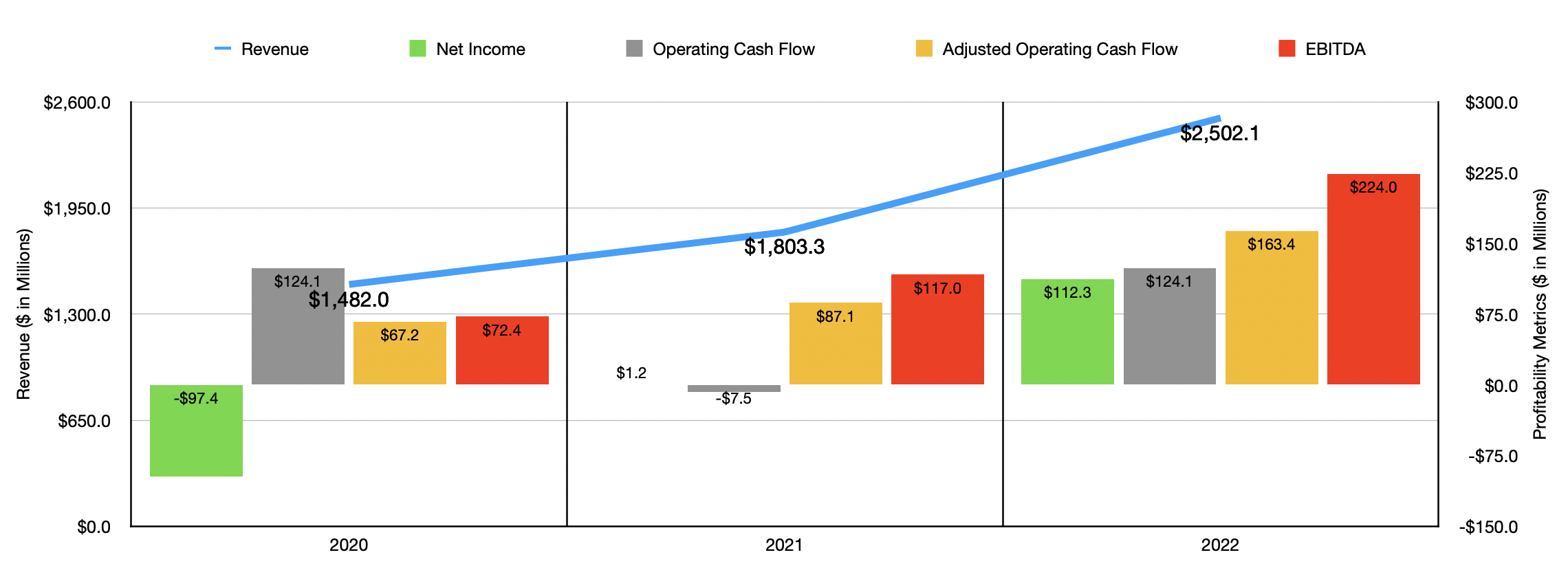

Although I was bullish about the company back then, I never would have imagined that the return disparity would end up quite that large. But after all this time, I believe that the business deserved it. Consider financial performance covering the entirety of its 2021 fiscal year . Revenue of $1.80 billion came in far higher than the $1.48 billion reported only one year earlier. But that was only the start of the increase. In 2022 , sales climbed further still, spiking to $2.50 billion. As those who follow the company closely know, the enterprise specializes on the production and sale of trailers and truck bodies. In 2022, the company shipped 52,035 new trailers. That was up from the 45,365 that it shipped in 2021. this was offset to some degree by a decline in the number of new truck bodies shipped, with that number declining from 16,560 to 14,800.

New trailers revenue of $2.01 billion accounted for the bulk of the company's sales, with that number dwarfing the $1.35 billion reported only one year earlier. It's also worth mentioning that the company benefited from strong results elsewhere as well. Components, parts, and service revenue of $139.8 million beat out the $131.9 million reported one year earlier. And equipment and other revenue jumped from $314.5 million to $346.6 million. Used trailer revenue also increased, rising from $2.5 million to $2.9 million, with the number of used trailers shipped remaining flat at 95.

Bottom line results for the company also increased during this time. The company went from a net loss of $97.4 million in 2020 to a net profit of $1.2 million in 2021. But this paled in comparison to the $112.3 million in profit generated in 2022. For context, the net income achieved in the 2022 fiscal year was the highest that the company has reported since 2016. Other profitability metrics followed a similar trajectory. Operating cash flow, however, was an exception to the rule. This number actually went from $124.1 million in 2020 to negative $7.5 million one year later. But then, in 2022, it surged back to $124.1 million. If we adjust for changes in working capital, however, the picture changes. In this case, the metric would have risen from $67.2 million in 2020 to $87.1 million in 2021 before almost doubling to $163.4 million in 2022. A similar path can be seen when looking at EBITDA. According to management, that metric rose from $72.4 million in 2020 to $117 million in 2021. For the 2022 fiscal year, it came in at $224 million.

By the end of the 2022 fiscal year, the company boasted $3.4 billion in backlog. This was up an astounding 46% compared to the amount reported for September of 2022, and it was 34% higher than it had been one year earlier. This backlog, according to management, will help to fuel revenue of between $2.8 billion and $3 billion for the 2023 fiscal year. Earnings per share, meanwhile, should come in at between $2.70 and $3, with a midpoint translating to net income of $141.2 million. The company didn't provide guidance for any other profitability metric. But if we assume that they were to increase at the same rate that net income should, then we should anticipate adjusted operating cash flow of $205.5 million and EBITDA of $281.6 million.

{kind=link}

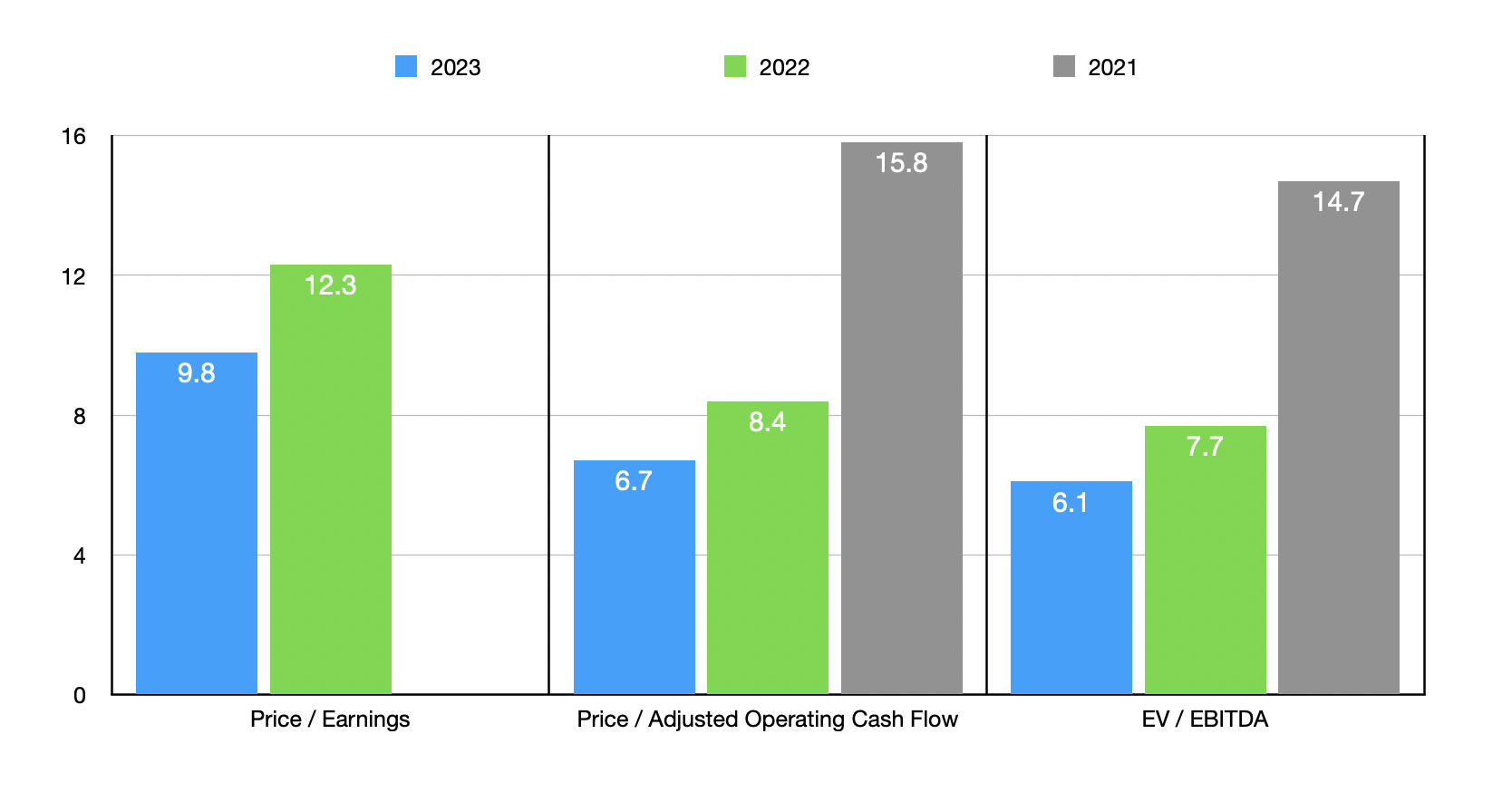

Using these figures, we can calculate that the company is trading at a forward price-to-earnings multiple of 9.8. The forward price to adjusted operating cash flow multiple would be 6.7, while the forward EV to EBITDA multiple would be 6.1. Using the data from 2022, these multiples would be a bit higher, coming in at 12.3, 8.4, and 7.7, respectively. But even if we assume that financial performance were to eventually revert back to what it was in 2021, I wouldn't say that shares are overvalued relative to cash flows. Those multiples can be seen, along with those for the 2022 and 2023 fiscal years, in the chart above. As part of my analysis, I also compared the enterprise to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 13.7 to a high of 76.1. Using the price to operating cash flow approach, the range was from 21.9 to 169.1. And when it comes to the EV to EBITDA approach, the range would be from 7.8 to 43.9. In all three cases, Wabash National was the cheapest of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Wabash National |

| 12.3 |

| 8.4 |

| 7.7 |

| Douglas Dynamics ( PLOW ) |

| 27.2 |

| 169.1 |

| 16.1 |

| The Shyft Group ( SHYF ) |

| 29.7 |

| 21.9 |

| 21.9 |

| Astec Industries ( ASTE ) |

| 76.1 |

| 132.6 |

| 43.9 |

| Terex Corp ( TEX ) |

| 13.7 |

| 49.8 |

| 9.7 |

| Manitowoc ( MTW ) |

| 29.2 |

| 65.3 |

| 7.8 |

Takeaway

Given current economic conditions, I can understand why some investors may be cautious when it comes to Wabash National at this time. Having said that, the fundamental condition for the enterprise is stronger than it has been in a very long time. On top of this, the robust backlog for the business should keep sales, profits, and cash flows, all up for at least the 2023 fiscal year. Even a return to the levels of profitability seen in 2021 would indicate a company that's perhaps fairly valued. But using data from 2022, on both an absolute basis and relative to similar firms, Wabash National appears cheap enough to still warrant the 'buy' rating I assigned it well over one year ago.

For further details see:

Wabash National Corporation: A Ride That's Still Not Over