TEX - Wabtec: A Solid Firm But Not A Great Purchase

Summary

- Wabtec Corporation has done quite well for itself and its investors over the past few quarters, with sales and profits up nicely.

- Backlog is higher year-over-year but is showing some signs of weakness.

- If shares were cheaper, the company would make a good prospect, but that's not the case today.

One of the largest industrial transportation companies out there is a firm called Westinghouse Air Brake Technologies Corporation ( WAB ), typically referred to as Wabtec Corporation. Largely as a result of acquisitions that the company has engaged in over the years, it has grown into a behemoth with a market capitalization of $18.50 billion. Recent growth achieved by the firm has been rather impressive and backlog is near all-time highs. At first glance, this may lead investors to think that the company is a no-brainer. But when you dig a bit deeper, you see some recent weakness in backlog and see that shares of the company, while not expensive, are definitely not cheap. Given these factors, I feel as though a solid 'hold' rating, indicative of return potential that should more or less match the broader market moving forward, is appropriate at this time.

A specialty industrial transportation firm

As I mentioned already, Wabtec operates as an industrial transportation firm. But what this means can be rather vague without further details. At its core, the company serves as one of the largest providers on the planet of locomotives. It also offers customers value-added, technology-based equipment, systems and services for global freight rail and passenger transit industries, and more. To best understand the company, however, it would be helpful to break up the firm's operations into its two operating segments.

The first of these is Freight segment. Through this, the company produces and sells aftermarket parts and services for new locomotives. It also provides components for both new and existing locomotives and freight cars. It produces new commuter locomotives, supplies rail control and infrastructure products, and offers its customers software-enabled solutions designed to improve the efficiency of its customers, as well as productivity. On top of all of this, the company also overhauls locomotives, provides heat exchangers and cooling systems for the rail and other industrial markets, and more. Over the years, the company's efforts have yielded significant fruit, with a global installed base of roughly 23,000 locomotives currently in use. This is also the largest segment of the company, accounting for 67% of its sales in 2021, with 68% of the segment's sales focused on aftermarket products and services.

The second set of operations for the company is its Transit segment. It is through this that the company produces and services components for both new and existing passenger transit vehicles. Examples of this include regional trains, high-speed trains, subway cars, light rail vehicles, and buses, etc. Specific components produced by the company include but are not limited to event recorders, monitoring equipment, positive train control equipment, electronically controlled pneumatic braking products and more. It is worth mentioning that some of these offerings can be utilized outside of the locomotive space, with marine and mining products also in its wheelhouse. This is the smaller of the two segments the company has, with only 33% of its revenue coming from it.

In terms of the overall industry in which the company operates, the global market for railway products and services was estimated in 2020 at being in excess of $120 billion. Although a large slice of the market, it's only expected to grow at an annual average rate of roughly 2.3% through the year 2025. What this means to me is that while the total revenue opportunity for the company is most certainly significant, the amount of growth that investors can or should expect isn't all that material, especially considering that this is a heavily competitive market.

{kind=link}

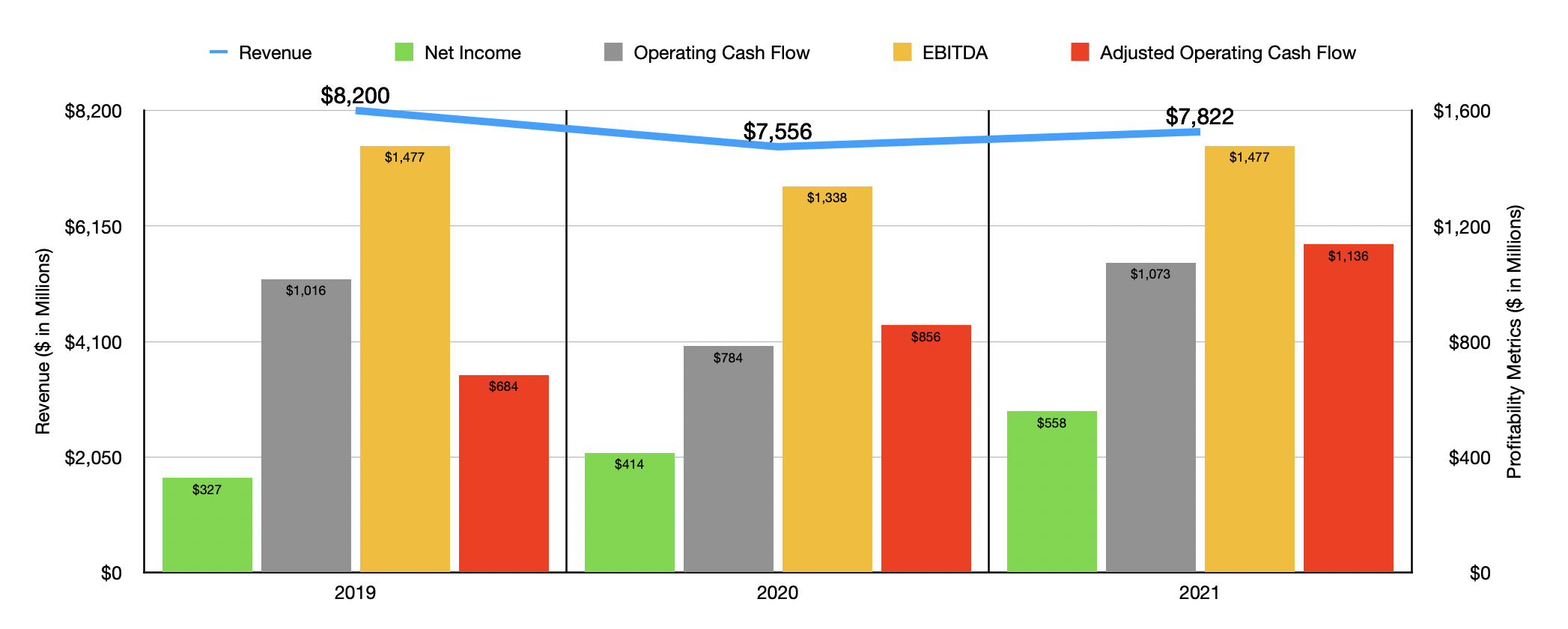

When it comes to valuing the company, the picture becomes complicated when you consider the number of major transactions the firm has completed in recent years. The most notable of these was its merger with GE Transportation that was divested from industrial conglomerate General Electric ( GE ) in 2019. Because of the impact that deal had, I've decided to focus on financial performance data from 2019 through the current day. During that time, we would have seen a bit of a bumpy ride from a revenue perspective. Sales dropped from $8.20 billion in 2019 to $7.56 billion in 2020. Even though that was the case, sales increased some in 2021, ultimately hitting $7.82 billion. Even though the 2020 to 2021 time period does not involve any major financial transactions, the company still benefited during that time to the tune of $138 million from smaller acquisitions the company had made. Foreign currency volatility added another $134 million to the company's top line, with organic sales actually declining by $6 million.

Although sales have not been on the rise to the extent that I would have liked to have seen, profitability for the company has done quite well. Net income grew from $327 million in 2019 to $558 million in 2021. From 2020 to 2021, the increase in profits from $414 million to the aforementioned $558 million came not only as a result of increased revenue but also because of a 2% improvement in the company's gross profit margin. At first glance, this may not seem like much. But when applied to the amount of revenue the company generated, it translates to an extra $156.4 million in profits for the firm. That's the beauty of fairly low-margin, asset-intensive businesses. Even a small improvement in margin can have an outsized impact on overall bottom line results. Other profitability metrics have been more similar to revenue in terms of volatility. Operating cash flow, for instance, dropped from $1.02 billion in 2019 to $784 million in 2020. In 2021, it came in at $1.07 billion. If we adjust our changes in working capital, however, it would have risen consistently from $684.3 million to $1.14 billion over the same three-year window. And finally, EBITDA dropped from $1.48 billion in 2019 to $1.34 billion in 2020 before ultimately popping back up to $1.48 billion in 2021.

{kind=link}

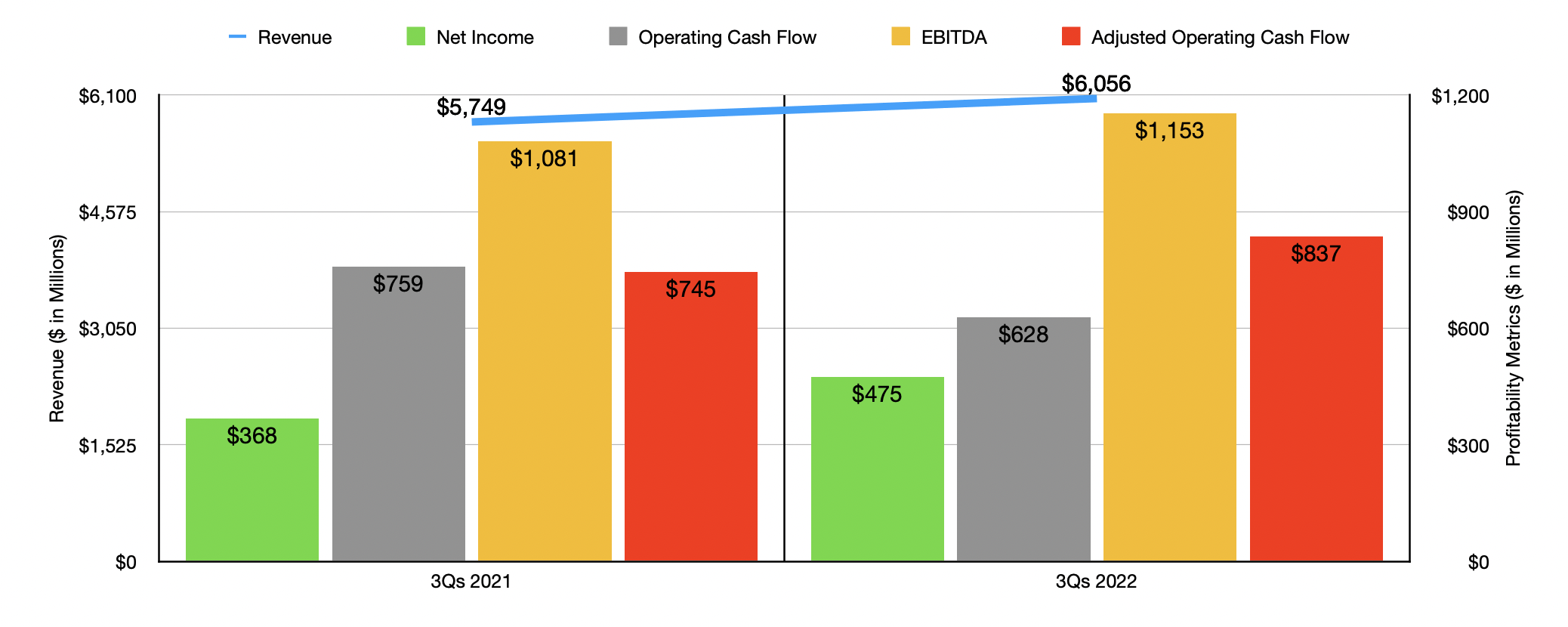

For the 2022 fiscal year, the data that we have for the company so far has been promising. Despite being hit to the tune of $212 million from foreign currency fluctuations, the company saw revenue jump from $5.75 billion in the first nine months of 2021 to $6.06 billion the same time of its 2022 fiscal year. Organic growth led the way, adding $454 million to the company's top line thanks to a $508 million increase associated with its Freight segment as higher locomotive modernizations and a larger active locomotive fleet, as well as greater equipment sales thanks to higher international locomotive deliveries and higher mining equipment sales, greater components sales from higher rail car build, increased railcars and operation, and growth in industrial end markets, all added to the firm's top line. Acquisitions, it should be said, added only $65 million to the company's sales year over year. The rise in revenue brought with it improved profits. Net income jumped from $368 million to $475 million. Although operating cash flow drops from $759 million to $628 million, the adjusted figure for this expanded from $745 million to $837 million. Over that same window of time, EBITDA for the company expanded from $1.08 billion to $1.15 billion.

By all accounts, this favorable picture should make investors feel bullish about the company. Another positive here is that backlog for the business ended in the latest quarter at $22.61 billion. That's up from the $21.84 billion reported the same time one year earlier. 12-month backlog also increased year over year, rising from $5.71 billion to $6.27 billion. But when you look a little deeper, you would see that backlog in the second quarter of 2022 was actually higher at $23.23 billion, while the 12-month backlog totaled $6.57 billion. This contraction and backlog could be evidence that some weakening caused by broader economic issues is in the works.

Even though the backlog figures for the company seem to be contracting to some degree, I could look over that if shares of the company were cheap enough. I really want to rate the company highly because I like its business model and the industry in which it operates. But if we assume that midpoint guidance for earnings provided by management is accurate, shares don't look cheap enough to capture my interest further. Current guidance calls for revenue in 2022 of between $8.15 billion and $8.35 billion. This is down from the prior expected range of between $8.30 billion and $8.60 billion. Although that downward revision has to do with foreign currency fluctuations as opposed to weakening demand. Earnings per share, meanwhile, should be between $4.75 and $4.95. That would translate to net income of $882.2 million. Based on my own calculations, adjusted operating cash flow should be around $1.28 billion and EBITDA should total $1.58 billion.

{kind=link}

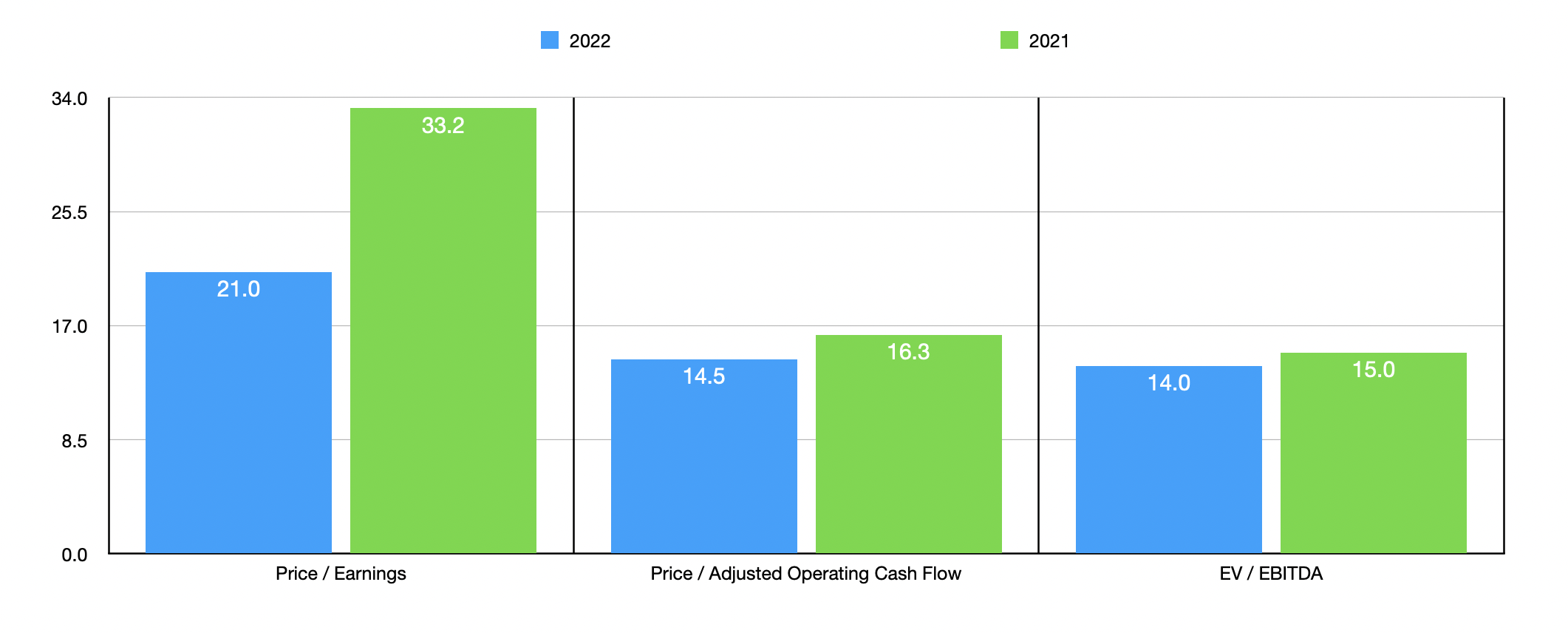

Based on these figures, the company is trading at a price-to-earnings multiple of 21. The price to adjusted operating cash flow multiple should be 14.5, while the EV to EBITDA multiple should come in at 14. You can see how these numbers are lower than what we would get using data from the 2021 fiscal year if you look at the chart above. As part of my analysis, I also compared Wabtec to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 12.2 to a high of 69.4. And using the EV to EBITDA approach, the range was from 8.9 to 20.2. In both of these cases, three of the five companies were cheaper than our prospect. And finally, using the price to operating cash flow approach, the range was from 8.2 to 44.5. In this scenario, two of the five companies were cheaper than our target.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Wabtec Corporation |

| 21.0 |

| 14.5 |

| 14.0 |

| Wabash National ( WNC ) |

| 28.0 |

| 9.3 |

| 12.2 |

| Caterpillar ( CAT ) |

| 18.5 |

| 21.2 |

| 13.5 |

| Terex ( TEX ) |

| 12.2 |

| 44.5 |

| 8.9 |

| Oshkosh ( OSK ) |

| 69.6 |

| 8.2 |

| 20.2 |

| Trinity Industries ( TRN ) |

| 16.4 |

| 21.1 |

| 14.1 |

Takeaway

Based on the data provided, I believe that Wabtec is a solid company that will probably do quite well for itself in the long run. Even though 2022 data has been largely encouraging, I do see some weakness potentially on the horizon. This picture could worsen depending on economic concerns moving forward. But I see all of these as transitory issues that will eventually come to pass. The bigger question to me is not about the company's future operations but about how much investors are paying for the firm. While the pricing of the company does not indicate that it's overvalued, the stock is expensive enough to make me less bullish on it than I would otherwise like to be. Because of this, I believe that a 'hold' rating is appropriate at this time.

For further details see:

Wabtec: A Solid Firm But Not A Great Purchase