WNC - Wabtec: Great Performance Is Encouraging But It Doesn't Warrant An Upgrade Just Yet

2023-10-05 05:36:18 ET

Summary

- Wabtec's financial performance is strong, with increased revenue, profits, and cash flows in the second quarter of 2023.

- The company's stock has outperformed the broader market, rising by 2.7% compared to a 2.4% drop in the S&P 500.

- WAB's long-term outlook is positive, with guidance for increased revenue and earnings per share, but the stock is priced higher than similar companies.

One of the downsides of being a value investor is that companies that look fairly valued or sometimes even overvalued can still appreciate relative to the broader market. This is true both in the short term and the long term. And it is especially true when the firms in question achieve robust financial performance. A great example that I could point to in this regard is Westinghouse Air Brake Technologies Corporation ( WAB ), more commonly known as Wabtec. Even though the company has seen a slight decrease in backlog on a year over year basis, revenue, profits, and cash flows are all up nicely. In the long run, I have no doubt about the company's ability to thrive. But the value investor in me still can't get over how shares are priced, both on an absolute basis and relative to companies that have similarities to it. So even though recently my call on the company has been proven slightly off, I do still maintain a 'hold' rating at this time.

Great performance continues

Back in June of this year, I found myself asking what kind of upside potential, if any, Wabtec might offer investors. Financial performance in the first quarter of 2023 proved to be positive compared to the same time one year earlier. The company also had a track record of achieving revenue, profit, and cash flow growth, even though some of those metrics improved only modestly from one year to the next. But because of how shares of the company were priced, I could not help but rate the enterprise a 'hold' to reflect my view at the time that the stock looked more or less fairly valued. This kind of call signals my belief that shares should see upside that should more or less match the broader market for the foreseeable future. But that's not what happened. Since the publication of the article , shares have risen by 2.7%. That compares to the 2.4% drop seen by the S&P 500 over the same window of time.

{kind=link}

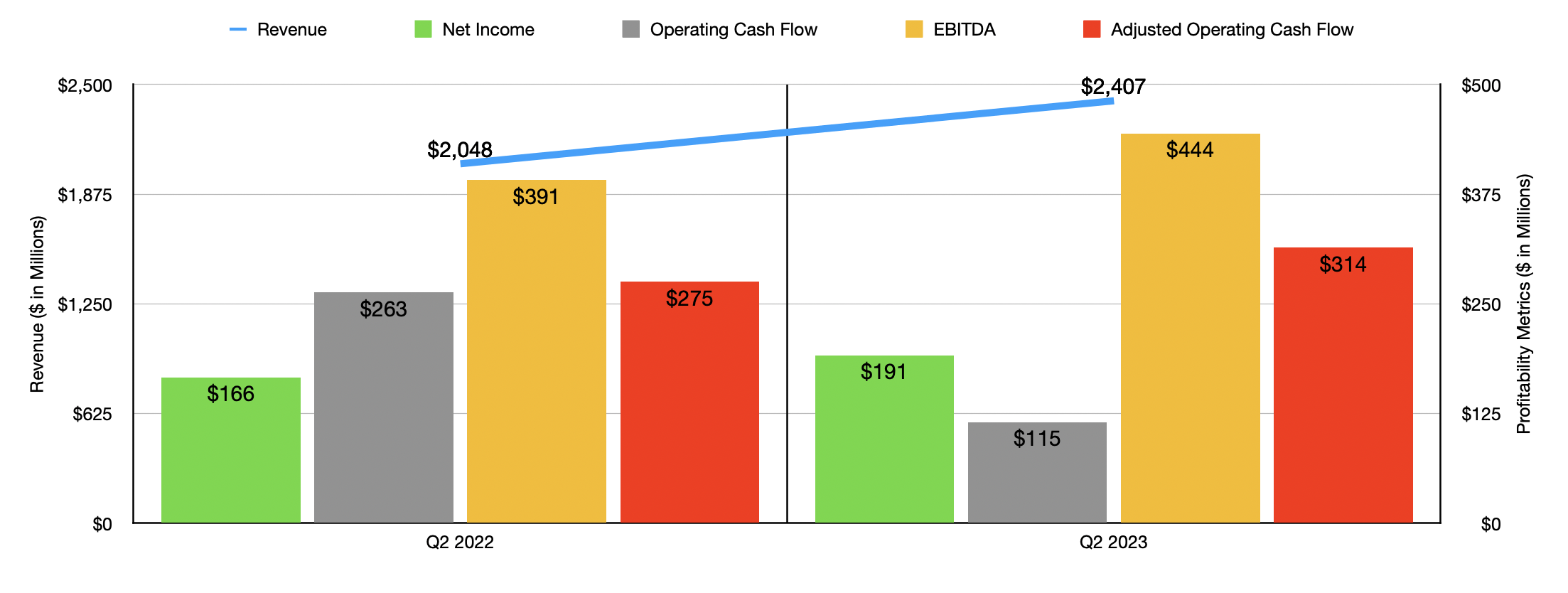

This outperformance can almost certainly be chalked up to strong fundamental performance achieved during the most recent quarter for which data is available. This would be the second quarter of the 2023 fiscal year. Revenue for that time came in at $2.41 billion. That's 17.5% higher than the $2.05 billion reported one year earlier. While the company did see a 9.5% increase in sales associated with services, the vast majority of the upside came from the sale of goods.

Revenue spiked from $1.58 billion to $1.90 billion. That increase, according to management, was driven mostly by organic growth. $216 million of the $355 million organic growth came from the company's Freight segment, with strength coming from components sales, equipment, and the company's Digital Intelligence offerings. Components sales jumped $55 million because of higher original equipment railcar construction activities and an increase in market share that the company claims to have captured. Equipment sales grew by $40 million because of higher locomotive sales. And Digital Intelligence revenue expanded because of higher demand for onboard locomotive solutions and international Positive Train Control (or PTC) products. Transit segment revenue, meanwhile, also increased nicely, with $82 million of growth on the product side coming from original equipment manufacturing sales and $57 million coming from aftermarket sales. Management attributed this demand to an increase in equipment door, HVAC, and brake systems offerings, as well as to increases in infrastructure investment.

{kind=link}

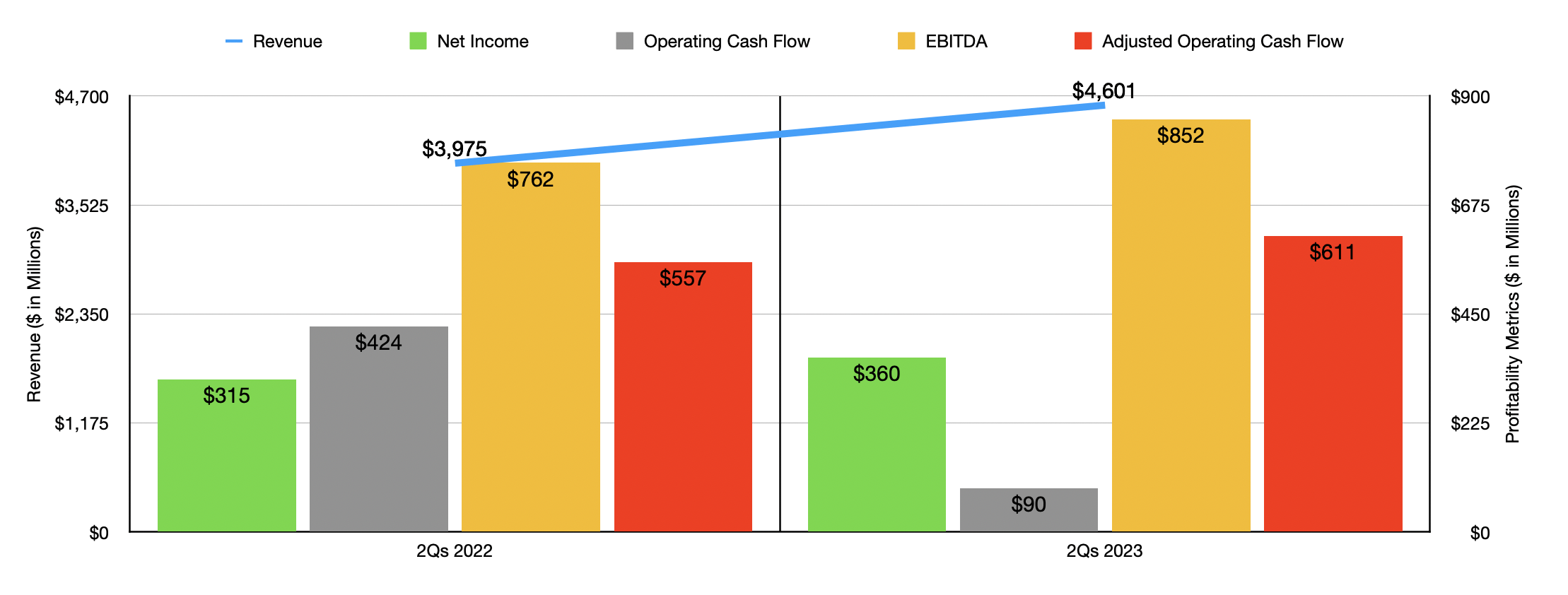

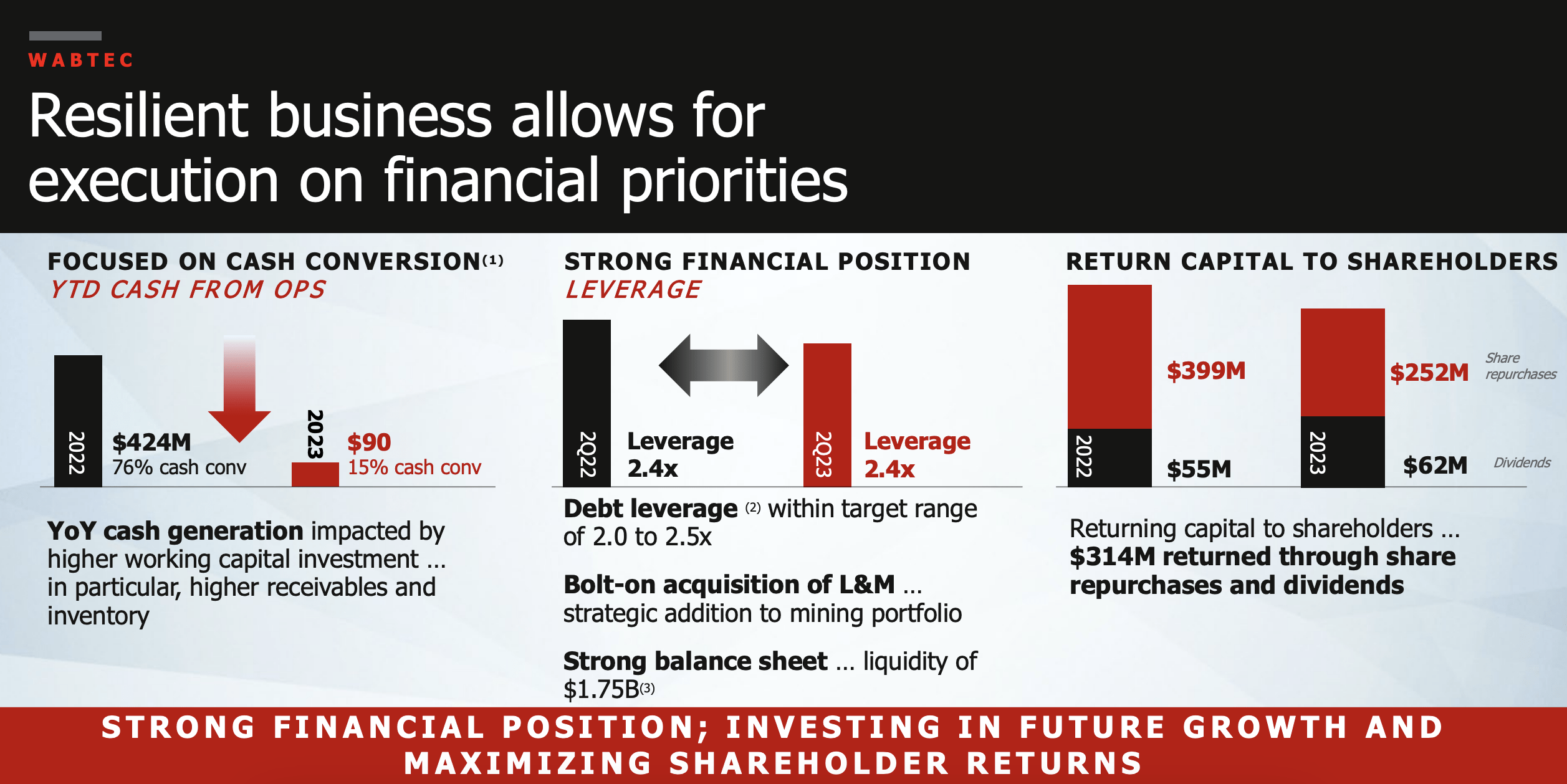

The rise in revenue for the company brought with it higher profits as well. Net income jumped 15.1% from $166 million to $191 million. While revenue for the company drove profits nicely higher, the improvements the company saw from this were offset to some extent by an increase in the cost of goods sold by the company from 72.4% of sales to 73.7%. So even though net profits grew, margin contraction was a slight negative for the enterprise. Other profitability metrics were largely positive. The one exception was operating cash flow. It was slashed from $263 million last year to $115 million this year. But if we adjust for changes in working capital, we get an increase from $275 million to $314 million. Meanwhile, EBITDA for the company jumped from $391 million to $444 million. As you can see in the chart above, the second quarter of the year was not the only time of strength for the company. Results for the first half of the year as a whole ended up being soundly higher than what they were at the same time last year.

{kind=link}

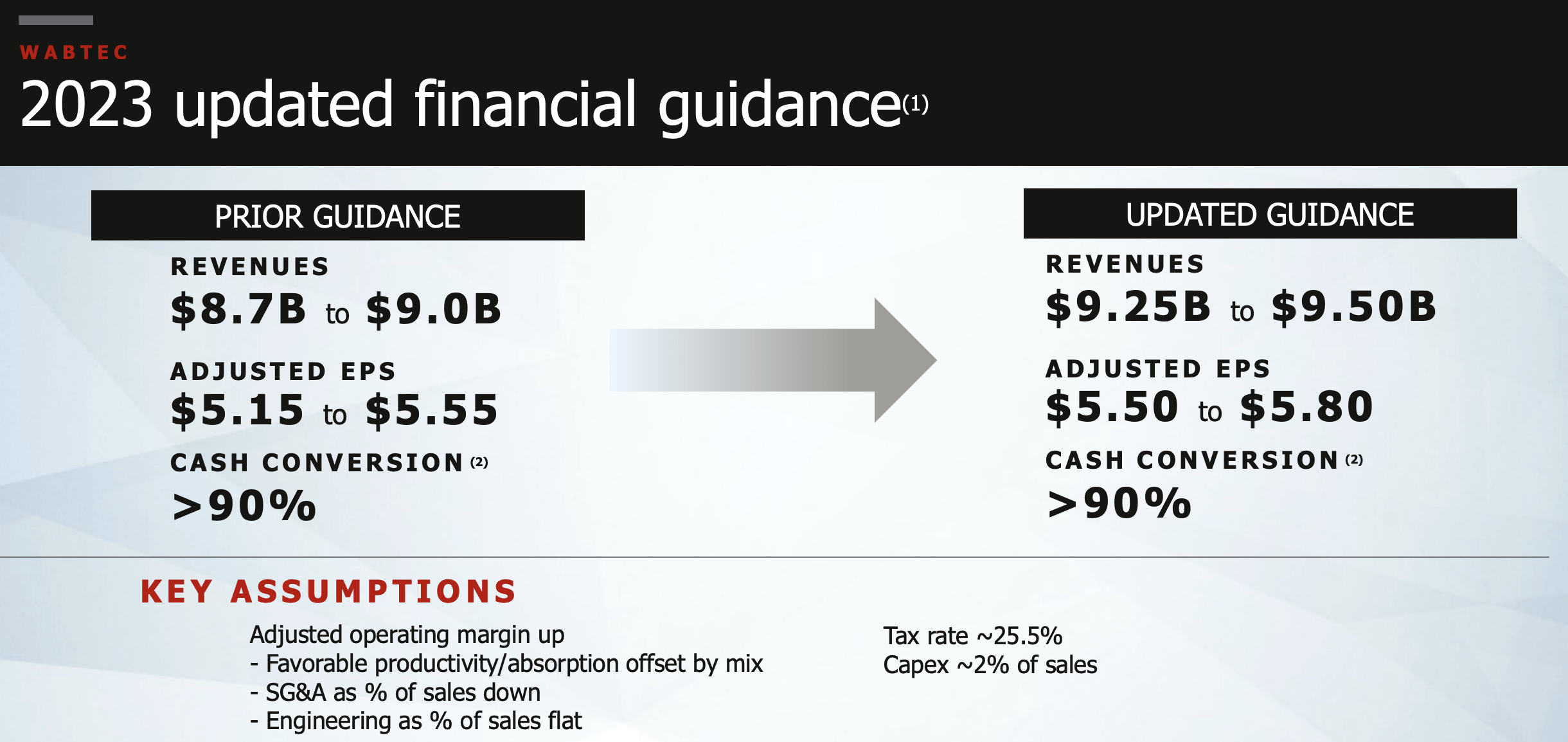

For this year in its entirety, management is forecasting revenue of between $9.25 billion and $9.50 billion. To me, this sales increase over the $8.36 billion in revenue reported for 2022, is not shocking. I say this because, although the company did see its backlog drop from $23.23 billion in the second quarter of 2022 to $22.43 billion at the same time this year, 12 month backlog actually expanded from $6.57 billion to $7.22 billion. Earnings per share, meanwhile, are forecasted to be between $5.50 and $5.80, with a midpoint of guidance translating to net income of $1.01 billion. Using these figures, I was able to get a good idea of what other profitability metrics might look like for the year. Adjusted operating cash flow, as an example, should come in at around $1.26 billion. Meanwhile, EBITDA should total $1.75 billion.

{kind=link}

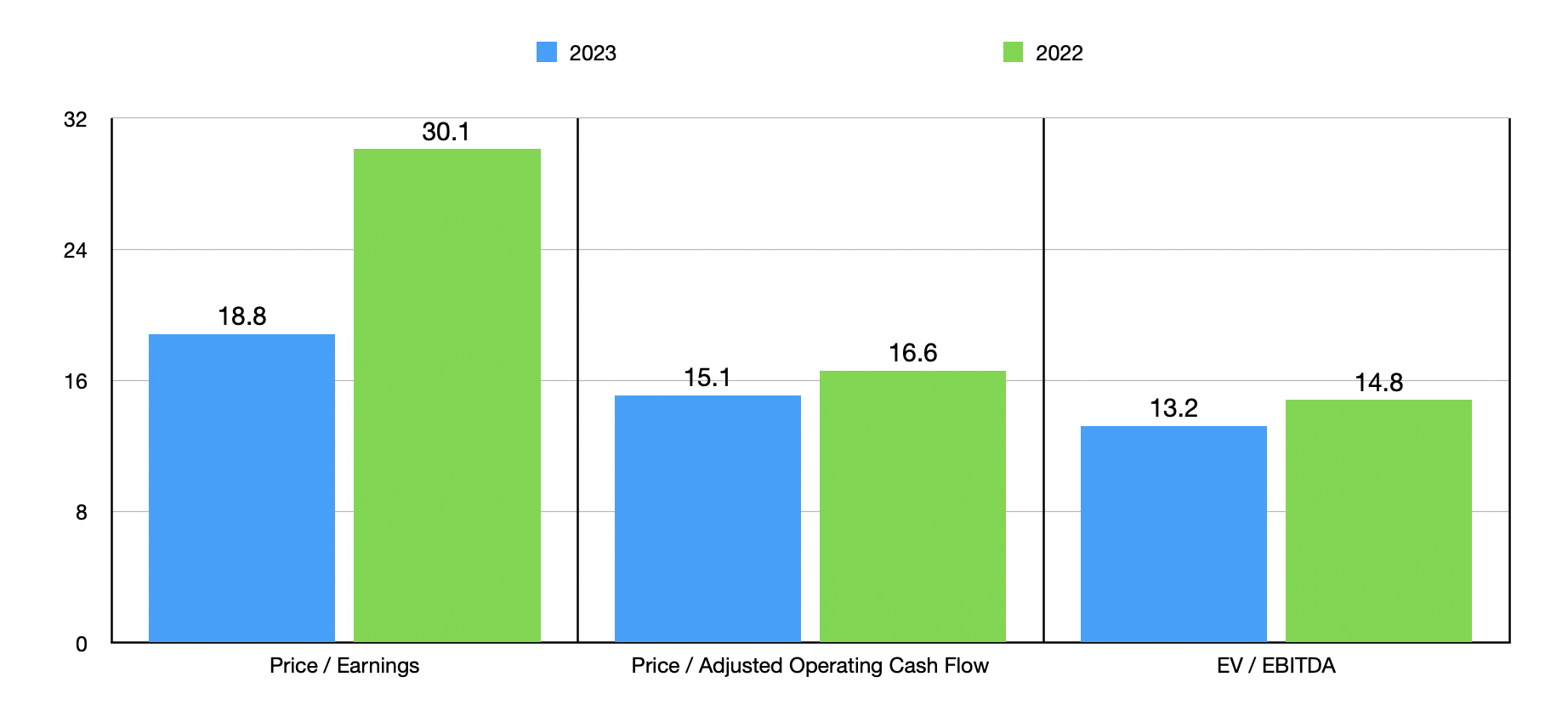

Using these figures, I was able to value the company as shown in the chart above. That chart shows pricing for the company on a forward basis, as well as using data from 2022. In all three cases, the stock does look cheaper on a forward basis. But that only makes sense when you consider the rise in profits seen so far this year. In the table below, I compared the enterprise to five similar firms. On a price to earnings basis, four of the five companies were cheaper than our target. But using the price to operating cash flow approach and the EV to EBITDA approach, our target ended up being the most expensive of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Wabtec |

| 18.8 |

| 15.1 |

| 13.2 |

| Wabash National ( WNC ) |

| 5.1 |

| 5.6 |

| 3.9 |

| Caterpillar ( CAT ) |

| 17.0 |

| 14.2 |

| 12.5 |

| Terex ( TEX ) |

| 8.8 |

| 10.6 |

| 6.7 |

| Oshkosh ( OSK ) |

| 15.8 |

| 10.9 |

| 8.7 |

| Trinity Industries ( TRN ) |

| 25.9 |

| 10.4 |

| 12.1 |

It will be interesting to see what the longer-term picture has in store for Wabtec. Already, the current guidance does represent an increase over what guidance was when the company reported results during the first quarter of the year. This makes me wonder if the company will end up increasing guidance for its five-year outlook as well. In the second quarter, management said that the five-year outlook called for mid-single digit core organic revenue growth on a year over year basis. The company is also targeting margin expansion of between 2.5% and 3%. Even based on the midpoint of guidance for this year an improvement at the low end of this spectrum would translate to an extra $234.4 million in profitability for the company in any given year.

{kind=link}

It's unlikely that the company will materially reduce leverage. I say this because the net leverage ratio right now is 2.4 and management's long term target range is between 2 and 2.5. So we are more or less where management wants the company to be. If that has not paid off, there could be the potential for future acquisitions. The company does have liquidity right now of $1.75 billion. Then again, rewarding shareholders by returning capital to them directly might be the way to go. Last year, for instance, Wabtec spent $399 million on share repurchases and paid out $55 million in the form of dividends. Dividends this year have increased to $62 million, while share repurchases have dropped to $252 million. But the more profitable the company becomes, the more likely it is to engage in these types of activities.

Takeaway

From all that I can see, Wabtec is doing a really good job at this moment. The company has a significant amount of backlog and financial performance on both the top and bottom lines continues to improve nicely. However, the stock does look rather pricey relative to similar firms, while being perhaps more or less fairly valued on an absolute basis. For now, and even at the risk of potentially missing out on upside, I will prioritize the valuation of the firm. And because of that, I've decided to keep it ready a 'hold' at the moment.

For further details see:

Wabtec: Great Performance Is Encouraging, But It Doesn't Warrant An Upgrade Just Yet