WNC - Wabtec: Growth Is Good But Not Enough To Seal The Deal

2023-06-19 04:41:52 ET

Summary

- Westinghouse Air Brake Technologies (Wabtec) has underperformed the market, appreciating only 1% compared to the 11.4% seen by the S&P 500.

- Wabtec has seen positive financial growth, with revenue, net income, and EBITDA all increasing in the past year.

- Despite the company's strong financial performance and management initiatives, the stock is still considered a "hold" due to its current valuation compared to similar firms.

One of the problems with value investing is that the lofty margin of safety that you apply to your investment ideology can result in companies underperforming or outperforming expectations. For instance, when I rate a company a 'hold', I don't necessarily believe that shares won't move up or down from that point. Rather, I believe that they should generate returns that more or less match the market for the foreseeable future. But, relying on multiple factors, including the quality of the enterprise, I can sometimes rate a company perhaps a bit higher than I should have. A great example that I can point to where this has occurred recently is with Westinghouse Air Brake Technologies ( WAB ), colloquially known as Wabtec.

Recognizing that the company is a high-quality operator that should have a bright future ahead of it, I previously rated it a 'hold' to reflect my view that shares should generate returns that would more or less match the broader market. But since then, units have underperformed the market, appreciating only 1% compared to the 11.4% seen by the S&P 500. You would think that, with attractive revenue, profit, and cash flow growth, I would now switch my stance to a 'buy'. But in my opinion, shares of the company are not yet cheap enough for such an upgrade.

A look at recent fundamentals

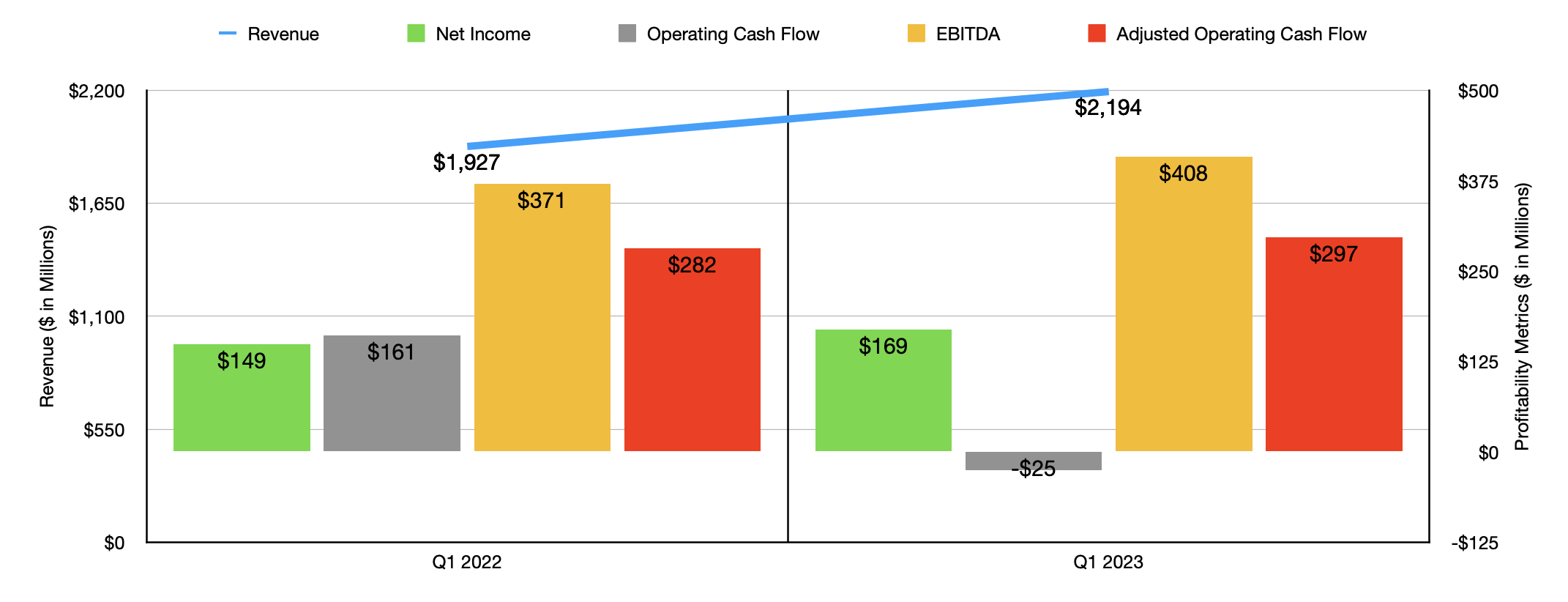

Fundamentally speaking, the picture for Wabtec and its shareholders has been quite positive recently. Revenue during the first quarter of the company's 2023 fiscal year, for instance, came in at $2.19 billion. That's 13.9% above the $1.93 billion the company reported only one year earlier. Acquisitions added $21 million to the company's top line during this time. But this was more than offset by a $56 million hit associated with foreign currency fluctuations. That leaves organic growth as the big driver of upside, with revenue expanding by $302 million because of it. On the equipment side of things, the company benefited from higher international locomotive sales. And on the services side, they benefited from a larger active locomotive fleet. All of this falls under the freight operations of the company. Under the transit side, organic sales growth was driven by higher demand for aftermarket products because of greater investments in infrastructure.

{kind=link}

On the bottom line, the company also saw some improvements. Net income grew from $149 million in the first quarter of 2022 to $169 million at the same time this year. It is true that operating cash flow went from $161 million to a negative $25 million. But if we adjust for changes in working capital, the metric would have risen from $282 million to $297 million. And over that same window of time, EBITDA for the company expanded from $371 million to $408 million.

{kind=link}

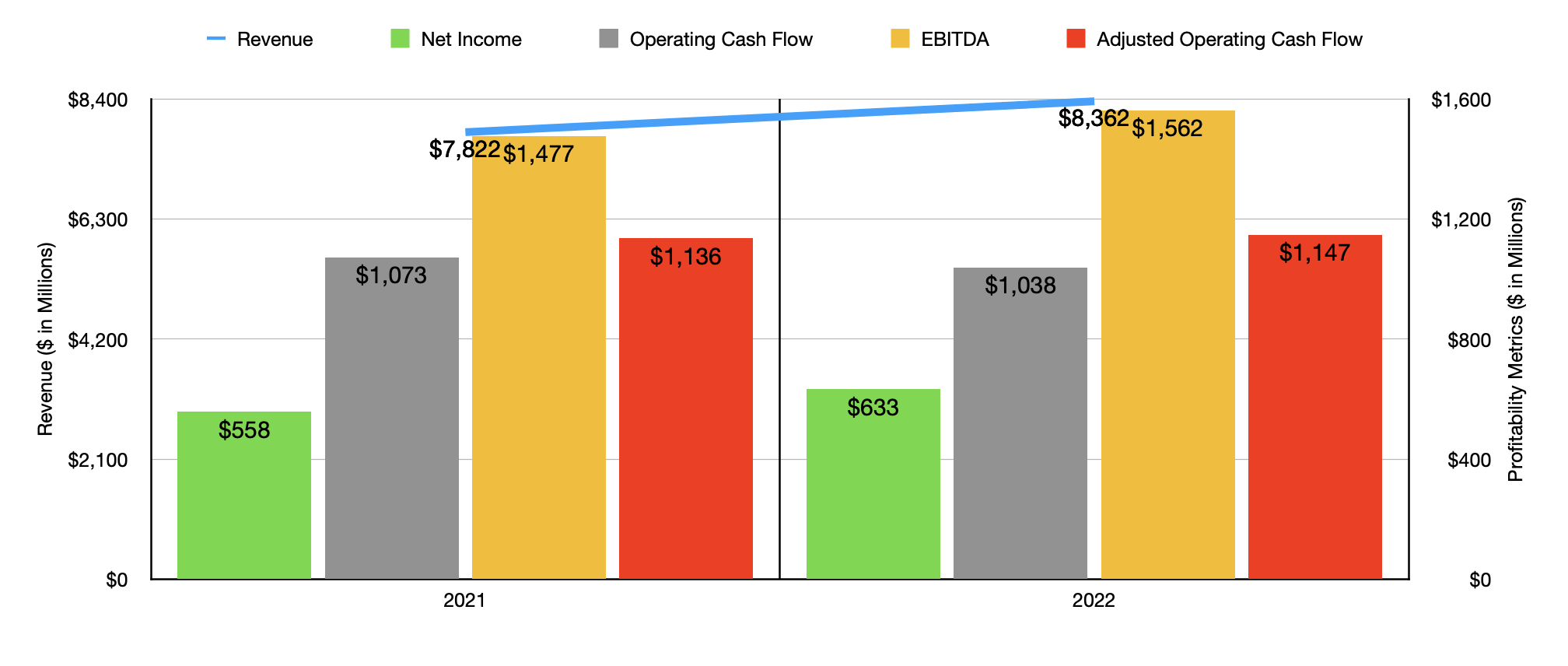

As the chart above illustrates, financial performance has continued to improve for an extended period of time. 2022 was a better year in almost every respect than the 2021 year was. With the exception of operating cash flow, every major metric that I look at increased during that time. Another positive about the company is that its backlog remains robust. Although backlog did decrease from $22.44 billion at the end of the 2022 fiscal year, to $22.33 billion in the first quarter, that's a fairly small decrease in the grand scheme of things.

Outside of the most recent financial data, investors should also be paying attention to some initiatives being pushed by management. Most notably, a little over a year ago, in the first quarter of 2022, management announced a three-year strategic initiative that they dubbed Integration 2.0. The ultimate goal of this initiative is to optimize operations in order to reduce costs. This includes A restructuring of its North American distribution channels and the expansion of operations in low-cost countries.

So far, this has not been all that costly and initiative. Management estimated that total expenses for restructuring would be between $135 million and $165 million. Of that, $78 million has already been incurred. This has resulted in the company's decision to close down fifteen of its facilities and lay off 1,100 employees. Specifics have not been provided as to what the total financial impact of these moves has been so far. But management did say that, in the five years following March 9th of 2022, it hopes to achieve between 250 and 300 basis points of margin expansion in addition to the mid-single digit core organic growth rate that the company is pushing for on an annualized basis. If we see the low end of that range realized from a margin perspective, it would imply about $209.1 million in additional profits on the company's bottom line for the 2022 fiscal year.

Shareholders should hope that this comes to fruition. But they should not bank on it. Rather, we should price the company using its most recent financial results. We should also use management's guidance for the current fiscal year. At present, the company anticipates revenue for 2023 of between $8.7 billion and $9 billion. Earnings per share should be between $5.15 and $5.55. At the midpoint, that would imply a net income of $718 million. Good estimates for adjusted operating cash flow and EBITDA would be $1.21 billion and $1.72 billion, respectively.

{kind=link}

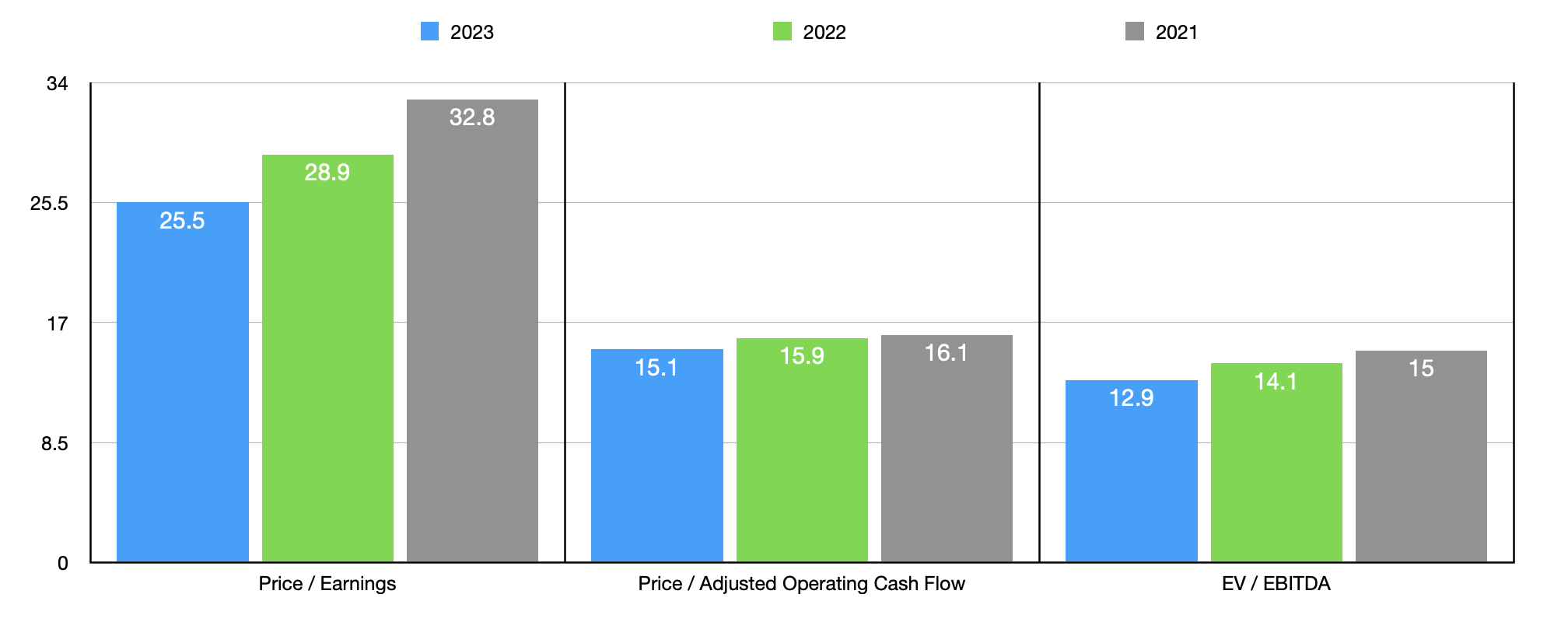

Based on these numbers, you can see how shares are priced on a forward basis in the chart above. You can also see pricing based on data from 2021 and 2022. On a price to earnings basis, shares of the company most certainly look pricey. But relative to the cash flow data, shares look perhaps fairly valued or very close to it. This does not mean that shares are cheap relative to similar firms. In fact, they are pricey on that basis for sure. In the table below, you can see how the stock is priced relative to five similar enterprises. On both the price to earnings basis and the price to operating cash flow basis, I calculated that four of the five companies ended up being cheaper than our prospect. And when it comes to the EV to EBITDA approach, Wabtec ended up being the most expensive of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Wabtec |

| 28.9 |

| 15.9 |

| 14.1 |

| Wabash National ( WNC ) |

| 8.7 |

| 5.9 |

| 6.2 |

| Caterpillar ( CAT ) |

| 18.3 |

| 14.4 |

| 12.9 |

| Terex ( TEX ) |

| 11.1 |

| 12.4 |

| 8.2 |

| Oshkosh ( OSK ) |

| 22.2 |

| 15.7 |

| 9.9 |

| Trinity Industries ( TRN ) |

| 30.6 |

| 30.2 |

| 12.4 |

Takeaway

When you put all of this data together, you can see that you have a high-quality company with a management team that is working to make the business even better. In the long run, I suspect that Wabtec will do just fine for itself and its shareholders. But this does not mean that the company makes for a great opportunity at this time. Given how shares are priced, I would still argue that the company makes for a solid 'hold' candidate at this time, even though it has underperformed the broader market since I last rated it that.

For further details see:

Wabtec: Growth Is Good, But Not Enough To Seal The Deal