WKCMF - Wacker Chemie: Finally Getting More Attractive

2024-01-05 15:01:19 ET

Summary

- Wacker Chemie has experienced a significant decline in its stock price and a negative return on investment.

- Despite the downturn, I remain confident in the company's long-term prospects and recommend considering it for investment.

- The company's sales have decreased, but it remains conservatively leveraged and has a strong balance sheet.

Dear readers/followers,

Wacker Chemie AG (WKCMF) is a company that I wrote about last time back in September 2023. We'll update on the company in this article, and you can find my last update on Wacker here.

Overall, the company has declined quite significantly. I managed to unfortunately time the height of the company's short-term cycle, which means that the small position I have in the company and have bought in accordance to my positive stance on the company is currently in a negative RoR.

However, this does not faze me. It's regrettable, but the company isn't a bad company for that, nor is its latest short-term downturn any sort of reason to not "BUY" more of the company in my view.

In this article, I mean to show you why that is, and why I still have a continued, high level of confidence in Wacker Chemie for the long term here.

While I realize that you may have had your fill of basic materials or chemical companies, especially low-yielding ones, I say that this one is still worth considering and potentially investing in.

Let's see what we have here.

Wacker Chemie - Looking at 3Q23, and what upside there is for the future

Chemical companies have not been the best investment for the past year and more. Most of these companies have seen a bit of a downturn, and I see no near-term trend reversal as likely here, based on the current geopolitical macro.

The latest set of results saw further confirmation of that downside, as well as confirmation of why there is a valuation downward trend as it currently stands.

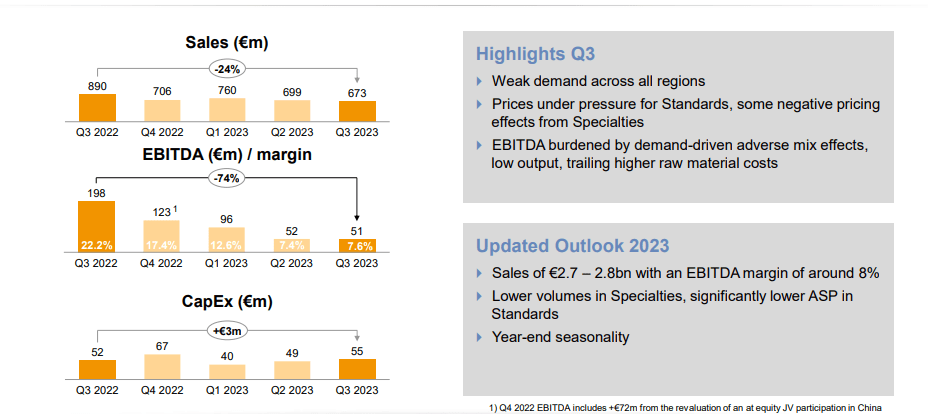

Top-line sales for the company were down 29%, but EBITDA was less than half YoY, with a margin of less than half and down to 10% on an EBITDA basis, with a company EPS that was less than an eighth of what it was to the YoY period. The company also, as a result, went up in terms of net debt.

What's going on here?

What's been going on for a few quarters here? The market is impacted by continued weak demand. There are exceptions to this, with polysilicon ASP for solar products being in continued high demand with a resilient underlying market.

However, the continued high energy prices, as well as pricing for input materials, continue together with these weak demands to hold the company back.

The company's updated sales guidance has been adjusted to the lower end of the previous guidance for the full year, with EBITDA lowered to below €1B, moving its guidance range down from a previous high of a billion. The company continues to push investments in silicones across the world, with new facilities across Asia coming online in 2025E.

With the current trends, much of the focus should be on the company's fundamentals and balance sheet. And the good news here is that Wacker remains one of the most conservatively-leveraged chemical players out there, with almost €5B in total equity of which €1.4B is in liquidity.

It's also clear as to what needs to happen to turn things around for this company.

{kind=link}

The demand needs to turn around for this company's results to improve. When it does, and when seasonality switches back to the positive, we'll see this company revert not only in earnings but in valuation as well - and that's just silicones. The picture for polymers is, as I said earlier, better. EBITDA is up despite lower sales due to good pricing.

{kind=link}

The company's biosolutions segment is one of the smaller ones, and it saw negative trends, being in the negative EBITDA for the third consecutive quarter here, with no continued relief in sight from the forecast for the year or short-term beyond that.

The company's main focus, at least legacy-wise, is the market for silicone rubbers, ethylene vinyl acetate polymer powder, silicon, and wafers. We have a good sales split, albeit a silicone-heavy one at 40%, with polysilicon currently seeing some weakness, and polymers at 20-25% each, which gives the company some diversification here.

Wacker Chemie is not large. In the context of the broader segment, this particular company is one of the smaller ones out there - and with a 70%+ EPS drop forecasted in 2023E, there aren't many analysts putting this one on their first investment spot or ideas list.

However, this is exactly the sort of situation where I have made, historically, market-beating returns. If you invest at a low price here, the valuation upside you have is nothing to underestimate. We'll look more at this in the valuation section.

The company is currently doing what it has been doing for most of the macro weakness. It's focusing on its financials, making sure its fundamentals stay up to par and that there is no fundamental danger to the company having to sell assets or stop investing in growth projects. It's not an easy thing in this environment, because every single segment that makes the company profitable is seeing headwinds.

What you need to remember about Wacker is that like most chemical businesses, this one is a mix of its input costs to output earnings, and with the inputs at a higher level and with sales issues, this company isn't going anywhere.

What Wacker as a business has going for it in a historical perspective is a clear underestimation of the upside. You've been able to, multiple times during its history, make a substantial market outperformance based on investing cheaply.

That is exactly what I am counting on here - because it's backed by data. Wacker, over 40% of the time, has a 10% MoE-adjusted likelihood of beating the analyst targets (Source: FactSet), and analysts aren't very good at forecasting where this company goes.

Is it the most qualitative, high-yielding business you could invest your hard-earned capital in?

No, it's certainly not.

Does it have an upside high enough for you to take that risk?

I believe it does, yes.

Let me show you the risks and upsides to this company.

Risks & Upside to Wacker Chemie

The risks to Wacker are similar to every company in this space. It's primarily a demand-driven environment prone to vicious down cycles and poor performance during those down cycles, only to revert when things go back to a high-demand period. The annual rates of return you can "clock" during those upcycles are almost 100% per year, if you look at example periods from 2020 to 2022 or the like. It's not as though volatility is rare for Wacker - it's more of a rule than an exception, with several fiscal years of 80-100% EPS decline or more in the last 15 years.

I still wouldn't characterize the company's operations or its fundamentals, or even its management as a risk, but as a boon. The company has proven, historically speaking, that it can survive down cycles and outperform during up cycles.

That's the risk/reward consideration you should have, or at least look at, if you mean to invest in Wacker Chemie.

Here's the valuation upside to the company as things currently stand.

Wacker Chemie - The valuation and upside

The company's 5-year average is between 15-18x P/E. My previous PT was €140, and I'm not shifting that at this time - though I would say that the company could go far, far higher in an upcycle.

Even at this time, I would say that at a low point of 15-16x, we now have a 30% annualized upside to a triple-digit 3-year upside if the company's reversal potential of over 15% per year materializes. That would also put the company at a PT of above €200/share.

Again, there's plenty of volatility here, and plenty of uncertainty.

This is not the investment idea most of you might be looking for. The yield is theoretically high, but this is only on a previous-year basis - what the forward yield turns out to be, we'll simply have to see when the company reports its full-year results early this year. That's when the company gives an AGM indication for the dividend.

I'm still not changing my price target for the company here - €140/share is good enough, and it's a great risk-adjusted target for what I believe is a solid company.

It, however, is not one of the first chemical companies that I would invest in here. That honor goes to a business like Evonik Industries AG (EVKIY), which has both a better size, a better fundamental sales mix, and a more future-proof business.

This is, I believe, an important lesson for any investor. Just because you find a good investment does not mean it's the best investment for you. A suitable investment for anyone combines a set of safety, upside, and usually income variables that specifically benefit that investor in that specific situation or timing. Sometimes what's right for me is not the right investment for you. You maybe should be investing in something safer with a lower upside, but a better income and safety, even if you might end up with a lower total RoR.

Wacker Chemie has an analyst average target of €140, coincidentally like my own. Analysts have a low €108 share price target, with a higher-end target range of €180/share. No one is currently expecting this company to make its way up to €200+ again - over the long term though, I don't think that is unlikely.

Out of 14 analysts, 11 are at a "BUY" or positive rating here, implying a high rate of conviction for these target levels.

I do not find any good arguments for why this company, in the longer term and upcycle, isn't a "BUY" here. The only reason why I would avoid the company completely here is if you believe the business won't recover from this in the long term.

Obviously, if it doesn't, this isn't a good investment.

Other than that, this is the thesis I would consider valid for Wacker Chemie.

Thesis

- Wacker Chemie is a leader in silicones and polysilicons. It's moving from commoditized chemicals to specialty chemicals, where much of the appealing, stable margins lie and I expect that the company will manage this move well over time. At the right valuation, I consider this company to be an attractive "BUY".

- The company currently trades at an average weighted P/E of 7-9x, depending on where you look and what you estimate. I believe this to be too cheap, despite believing in full in a 70% EPS drop from the 2023A highs during this year, and with a high upside for the next few years.

- That makes, in my mind, Wacker Chemie AG a "BUY" here. I give it a target of €140/share conservatively and am buying shares at this price. I reiterate this target as of the update for 2024 and for the next few years.

- I am buying more shares - though I am buying them slowly.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansions/reversions.

Wacker Chemie fulfills 5 out of 5 of my criteria here, making it a solid "BUY".

This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Wacker Chemie: Finally Getting More Attractive