WAFD - WaFd Continues To Perform Remarkably Well

2023-11-08 08:10:28 ET

Summary

- WaFd has an interesting and generally positive track record, including during this difficult year.

- In particular, the firm's deposits are now growing again and its overall risk level appears to be on the low side.

- The bank has shown positive growth in net interest income, net profits, deposits, and loans, making it an appealing investment option.

- Add on top of this the attractive price that shares are going for and investors have a lot to be happy about.

While analyzing the banking sector for much of this year, I have found some very interesting prospects. I have also found some companies that I would have no interest in owning and others that are in between the two. One company that certainly strikes me as appealing given recent financial performance and how shares are priced is Washington Federal ( WAFD ), now known as WaFd . 2023 is shaping up to be a really solid year for the bank even in spite of difficulties for the sector more broadly. But even if we ignore the improvements seen this year, shares of the company look attractively priced and the business has a decent track record for growth. Given these factors, I have decided to rate the bank a very solid ‘buy’ at this time. And if shares happen to fall further, I could even see myself upgrading it to something more bullish.

Banking on WaFd

According to the management team at WaFd, the company is a traditional commercial bank that is based out of the state of Washington. It was originally founded back in 1917. As of August of this year, the company operated 199 branches spread across 8 western states. From these branches, the institution provides a wide array of services for its clients. Like any bank, it accepts deposits. It then lends those deposits out for various purposes.

Primarily, the bank specializes in issuing commercial loans, with construction loans representing the largest category under that umbrella. But when looking at specific categories of loans and ignoring whether they are commercial or consumer, the greatest exposure for the bank is to single family residential properties. As of the end of its 2022 fiscal year, these accounted for 29.8% of its gross loan values. The company also gives out loans for other purposes. For instance, it issues land consumer lot loans, HELOCs, commercial real estate loans, multifamily loans, and more.

There are other operations that the business engages in as well. For instance, it has its own insurance subsidiary that offers individual and business insurance policies to customers of the bank, as well as to members of the general public. The firm operates a mortgage services company that holds and markets real estate that's owned. One of its subsidiaries acts as a trustee under deeds of trust to which the bank is a beneficiary. And lastly, the company has a small subsidiary called Pike Street Labs that provides data and technology services to the institution.

{kind=link}

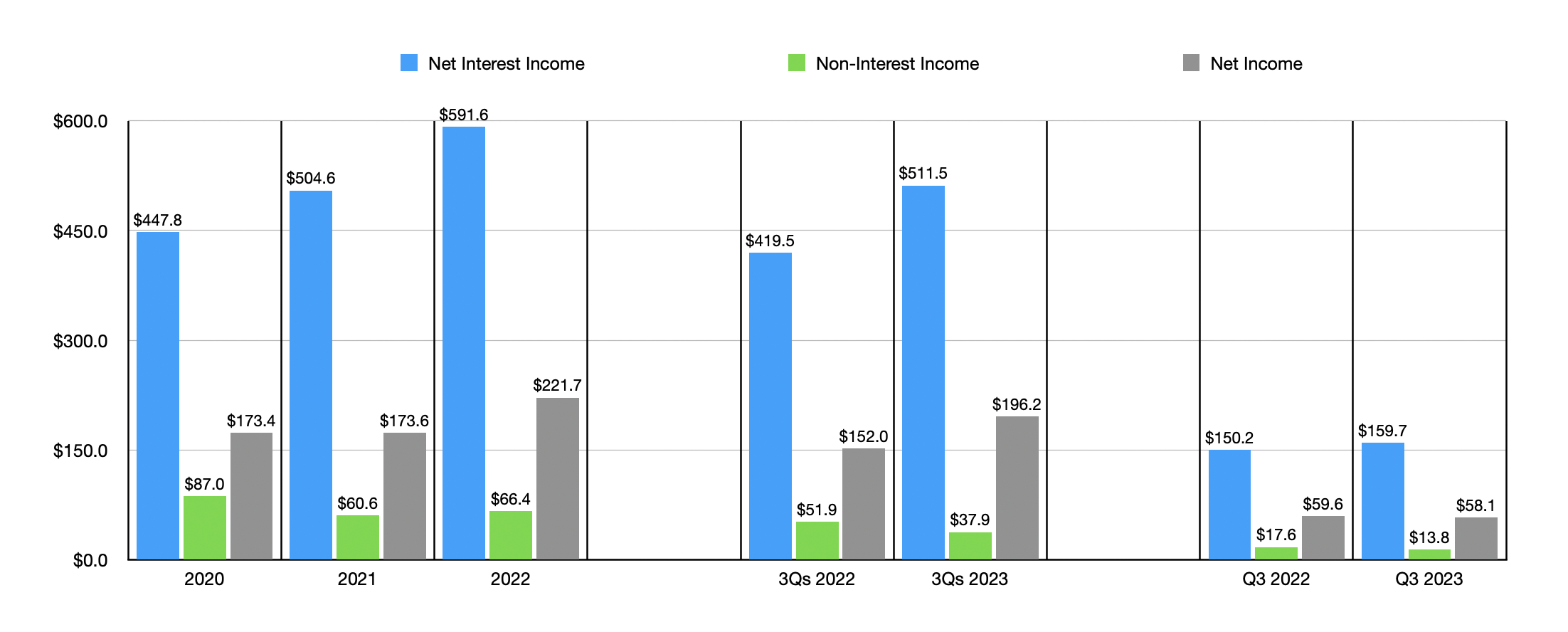

In recent years, the general trend for the bank has been positive. Net interest income grew from $447.8 million in 2020 to $591.6 million in 2022. Over that same window of time, non-interest income declined from $87 million to $66.4 million. But that didn't stop net profits from climbing from $173.4 million to $221.7 million. As you can see in the chart above, growth for the bank has continued into the current fiscal year. For the first nine months of the 2023 fiscal year, the bank reported net interest income of $511.5 million. That's up nicely from the $419.5 million reported one year earlier. A growth in the value of loans, combined with higher interest rates, certainly helped in this regard. But unfortunately, non-interest income managed to fall yet again. The good news is that this didn't stop net profits from shooting up from $152 million last year to $196.2 million this year.

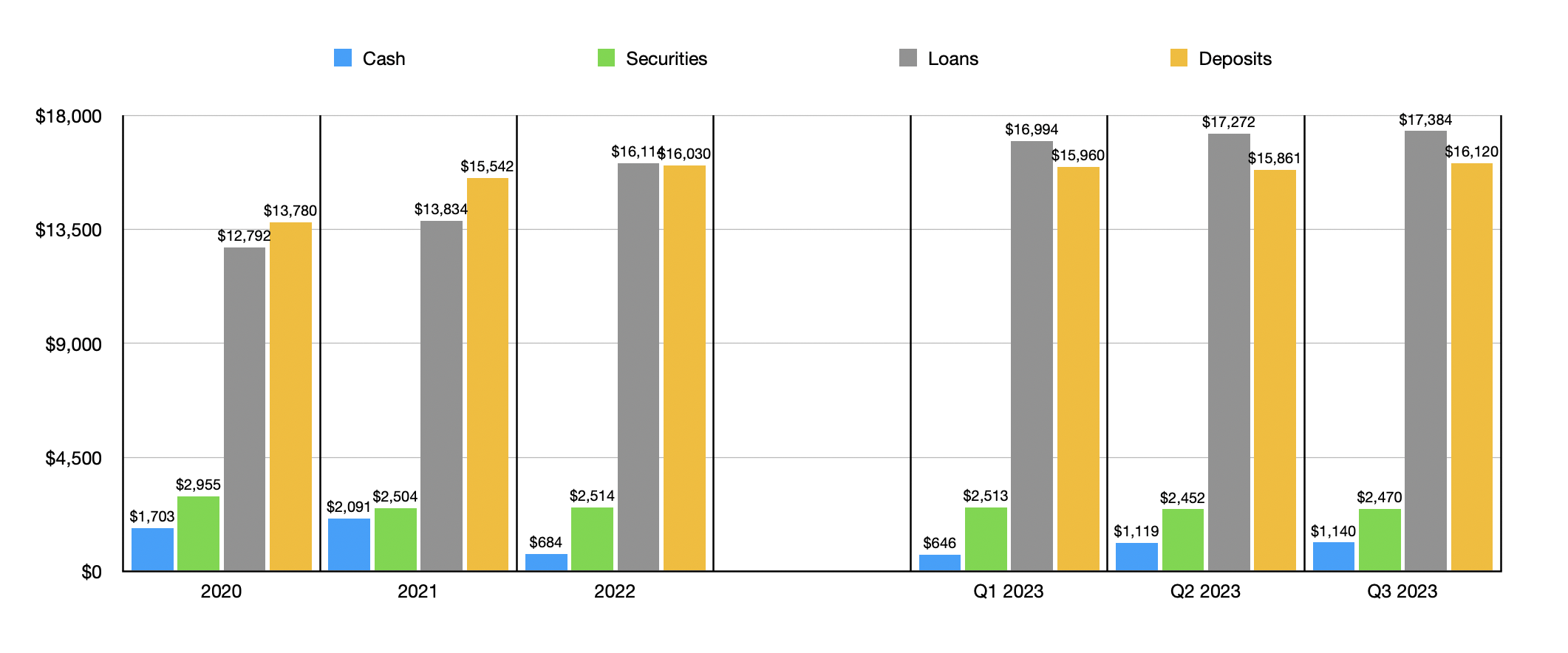

The overall growth of revenue and profits for the bank was only possible thanks to continued growth in its assets. And growth in its assets was only made possible by continued growth in deposits. Deposits jumped from $13.78 billion in 2020 to $16.03 billion in 2022. We did see declines in the first and second quarters of this year. But by the third quarter of 2023, the value of deposits had reached an all-time high of $16.12 billion. Is also worth noting that the company achieved all of this while decreasing its uninsured deposit exposure from 30.6% of all amounts at the end of last year to 25.7% as of the end of the third quarter. Personally, I like to see this number no higher than 30%. So it ticks that box for sure.

{kind=link}

As deposits have grown, the value of loans have increased also. They grew from $12.79 billion in 2020 to $16.11 billion in 2022. They continue to grow throughout this year, eventually hitting $17.38 billion by the third quarter. At the same time this occurred, the value of cash on the company's books managed to increase, growing from $684 million at the end of 2022 to $1.14 billion by the end of the third quarter. All the while, the value of securities barely budged, inching down slightly from $2.51 billion at the end of last year to $2.47 billion the same time this year. When it comes to loans, I know that some investors are worried about exposure to office properties. And honestly, this makes a lot of sense. The good news is that only around 5% of the company's overall loans involve office assets. That's not the lowest I have seen, but it is quite low.

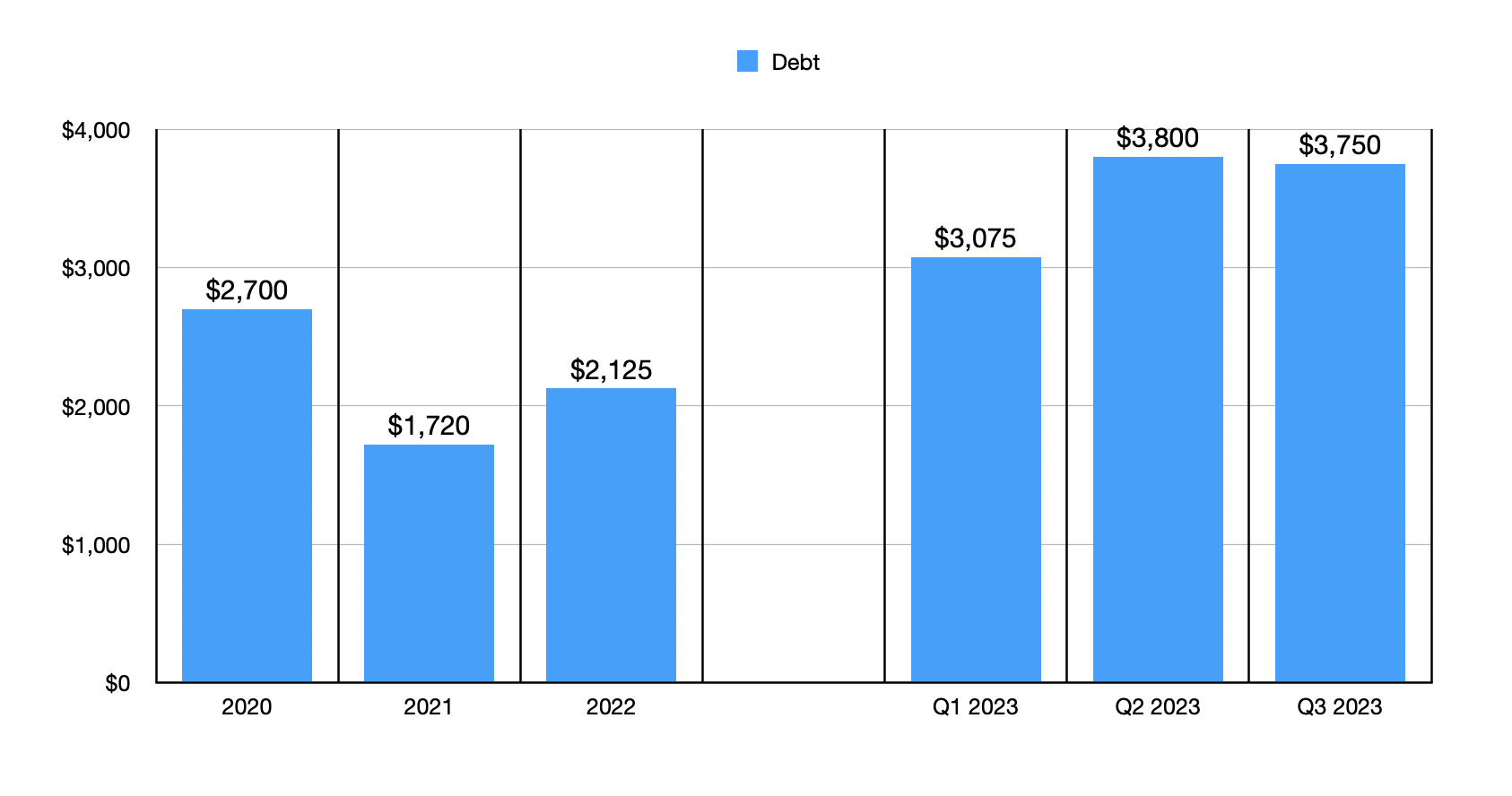

We also should be paying attention to debt. You see, in order to grow both cash balances and loans at a time when deposit growth first turned negative and then only barely recovered management resorted to taking on additional debt. At the end of 2022, the bank had $2.13 billion in debt on its books. This number increased over the next couple of quarters, eventually hitting $3.75 billion as of the end of the most recent quarter. That's not high enough to be terribly concerning. But investors should keep a close eye on borrowed amounts.

{kind=link}

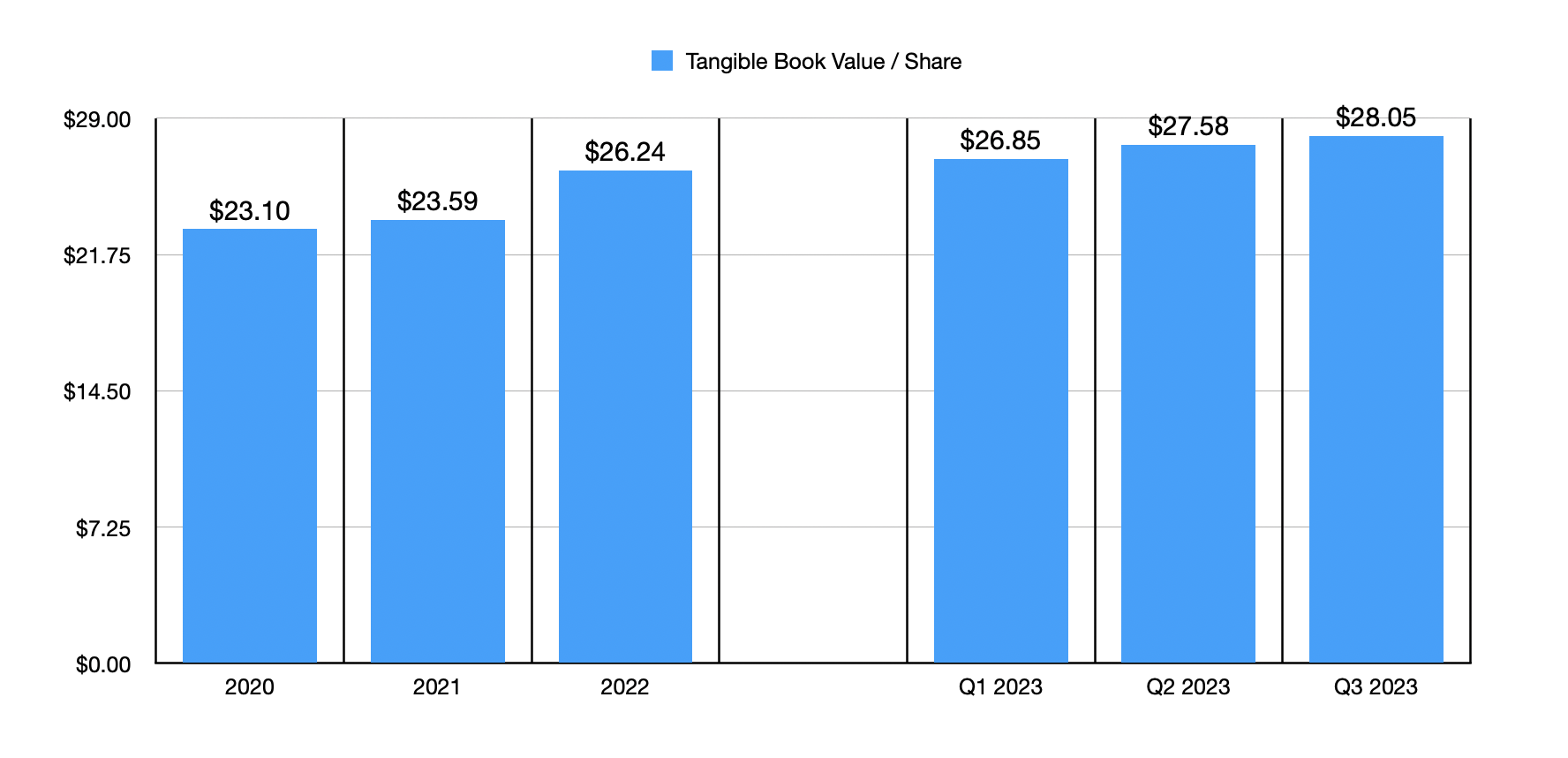

When it comes to valuing the company, there are a couple of methods that we can use. The first is to compare the share price of the company to its book value per share. At the end of the most recent quarter, the tangible book value per share of the bank stood at $28.05. Shares are trading at $26.67 as of this writing, meaning that they are trading at a roughly 95 end of book value. The other way is through the lens of the price to earnings multiple. Using last year's results, the bank is trading at a multiple of 7.8. If we annualize results seen so far for 2023, we would get a decline to 6.1. Either way, these are attractive levels that shareholders should be drawn to, especially with shares also trading at a discount to tangible book value.

{kind=link}

Takeaway

Based on the data provided, WaFd seems to be a bank that investors might want to consider banking on. It's not quite attractive enough to rate a ‘strong buy’ in my book. That's a very difficult rating to earn from me. But it is quite close to that point. If we could see debt fall further, the bank might just warrant such a step up in optimism. But for now, I do think a solid ‘buy’ rating makes sense.

For further details see:

WaFd Continues To Perform Remarkably Well