WMMVF - Wal-Mart De MeXico: Long-Term Hold With Current Headwinds

2024-01-02 09:57:00 ET

Summary

- Wal-Mart de México’s Q3 performance was reasonably strong, with operational efficiencies offsetting the lack of operating leverage that we typically see in the retail industry.

- Despite a promising entry into Q4, economic headwinds persist, while other trends discussed here could strengthen those headwinds.

- If you've been a long-term holder of Walmex, consider taking some profits now before the headwinds really kick in.

- Those who are underwater or near breakeven should sell the stock, but long-term investors might want to hold on to this retailer, whose growth story is still unfolding.

Thesis

Wal-Mart de México, S.A.B. de C.V. (WMMVY) (from here on, 'Walmex') has had a rough and tumble ride through the 2023 fiscal year, yet ranging in a $10 band between $32 and $42 over that period, give or take. With Q3 results having been announced in late October, let's look at this as a potential investment vehicle for long-term portfolios. Based on the analysis to follow, I would recommend holding on to your Walmex stocks for now because there are some near-term headwinds that need to be navigated over the crucial holiday quarter and heading into 2024.

Let's first become a little more acquainted with the brand, after which we'll look at Q3 performance as well as prospects for the future.

About Wal-Mart de México

The origins of Wal-Mart de México, a subsidiary of Walmart U.S. (WMT), date back to more than 30 years ago, when the first Sam's Club opened in Mexico in 1991. Initially launched as a joint venture between Walmart and Cifra, the former acquired a majority stake in the latter in 1997. Since then, Walmart has expanded in Mexico as well as other Central American countries using the same method of first forming a partnership and then increasing its stake to majority ownership. Today, the entity is known officially as Walmart de Mexico y Centroamérica, but the business is more commonly known simply as Walmex.

Revenue Growth and EBITDA Profitability

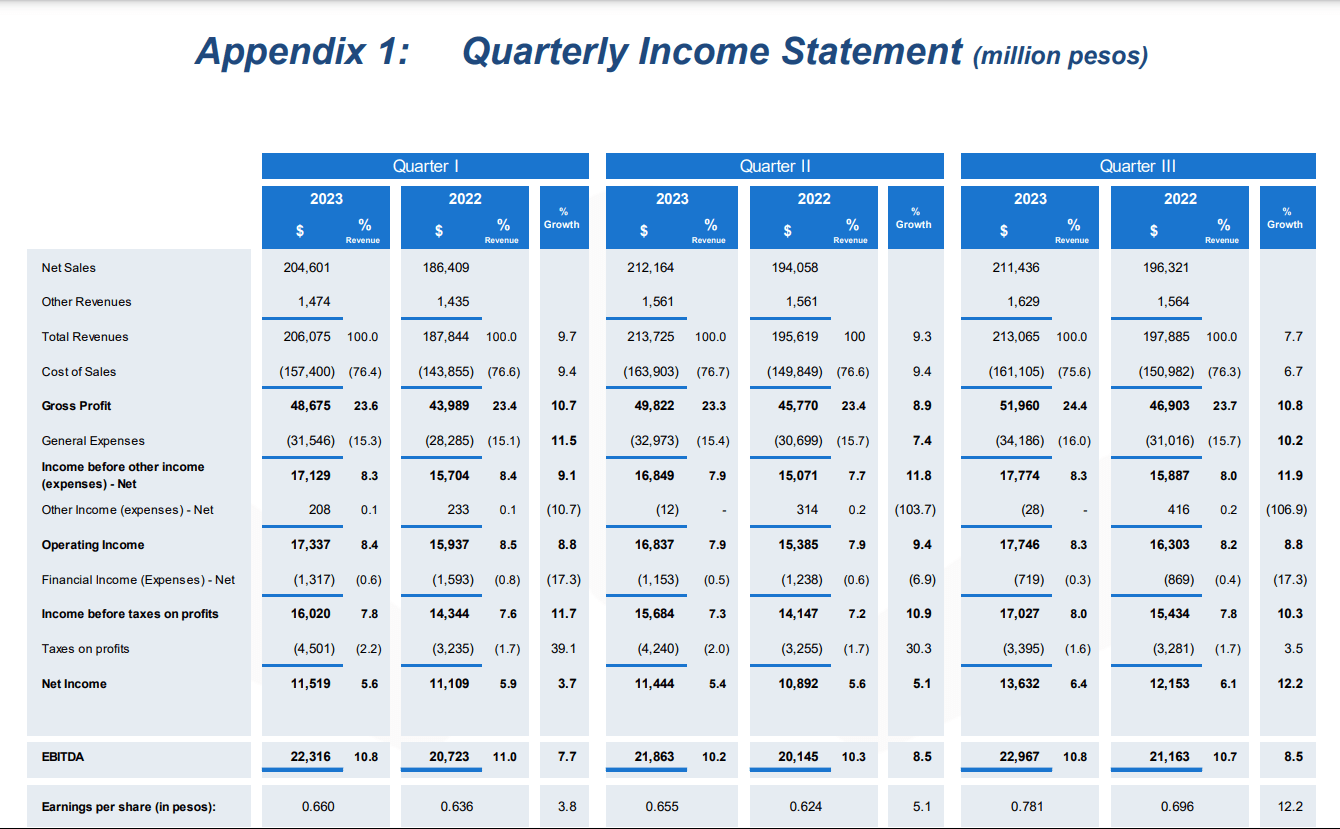

To kick off the investment narrative, let's look at how Walmex performed on the P&L side of things in Q3 2023. Earnings were reported on October 25, 2023.

{kind=link}

At the top , WMMVY exhibits healthy growth trends in the near term. Over the past three quarters, revenue has been growing at a near-steady clip of over 7.5%, peaking at 9.7% in the first quarter of fiscal 2023. The downtrend is unignorable, of course (9.7% in Q1, 9.3% in Q2 and 7.7% in Q3, all on a YoY basis), but it was also accompanied by a Q3 EBITDA of 23 billion pesos that grew 8.5% year over year. While the leverage came from the quarter's cost of sales (down 70 basis points, YoY) rather than operating expenses (up 30 bps YoY), this lack of operating leverage is not unusual in the retail sector because of the lower fixed costs associated with the sector itself. That's why I believe that the CFO's claim of "Operating income and EBITDA outpacing sales growth" (on the Q3 call ) should be taken with a grain of salt. An admirable achievement in YoY EBITDA growth, no doubt, but it should be seen in that broader context because gross margin expansion was, according to management:

helped by the solid contribution of the new verticals, improved commercial margins and lower import costs driven by an FX benefit.

Unfortunately, this leverage was partially diluted or offset by general expenses increasing 10.2% over the prior period, with the result that the EBITDA margin only increased by 10 basis points, validating the lack of operational leverage we just discussed.

Why is this important? Investors need to read into the numbers to avoid coming to the erroneous conclusion that revenue increases will automatically afford leverage down the P&L or, at the very least, not be completely negated by increased Opex. We'll get back to this later on in the discussion.

Now that we have more perspective on how the topline impacts (or fails to impact) profitability, it's equally apparent that growth at the top is far from running out of steam. Further supporting Walmex's growth story is the 2.8% increase in ticket and an even stronger 5.2% increase in traffic in Q3 2023 over the prior year, so we're looking at upticks in basket size as well as footfalls, resulting in very strong 8% comps.

To digress slightly, that's significantly healthier than the U.S. Census Bureau's advance estimate figure of a 3.1% YoY increase in retail and food sales across America in the third quarter of 2023. More specifically, retail trade sales were up only 3%, while nonstore retail (read e-commerce) sales growth was a more robust 8.4%.

It tells me that sales growth for Walmex - in its core markets of Mexico and Central America - is very close to e-commerce growth rates in the U.S. That's an important consideration, especially for investors in traditional U.S. retail, because it offers a diversification opportunity not too far away from home and still within the subsector of traditional retail. Well, hybrid retail, considering Walmex's focus on omnichannel but, nevertheless, a significant stimulus to diversify outside U.S. retail.

Revenue growth for Walmex is still healthy at high single-digit levels, so WMMVY looks like it's in a good position to post a reasonably strong fourth quarter, which brings us to the question of 'what will drive growth moving forward?'

Growth Drivers

I believe the holiday season will be the most significant growth driver for Q4, along with aggressive expansion and a greater focus on private-label brands. Together, these drivers should contribute to strong revenue growth in the short term. Let's break them down and analyze these three main growth drivers.

Holiday Season

WMMVY still has a healthy growth runway from the important shopping holidays in Latin America, kicking off with Singles' Day or Double Eleven all the way through to Christmas, during which Deloitte says consumers typically spend an average of up to $155 on presents, or roughly 2750 pesos.

There's also a flipside to this. Per the IMF , Latin America's economic growth is expected to show slow growth of about 2.3% this year, down from 4.1% in 2022, likely because inflation is expected to remain relatively high at around 5%. The IMF also projects a more optimistic inflation rate of 3.6% in 2024, so trends are clearly improving, but we can still expect a relatively muted holiday quarter this year due to the still-high inflation levels in the region.

Store Growth

Walmex is also continually expanding its footprint in both core markets, with 24 openings in Mexico and 3 in Central America over Q3, increasing total sales area from 7.41 million square meters in Q3 2022 to the current (as of the end of Q3 2023) 7.51 million square meters. Although the growth rate is relatively small at 1.3% on a year-over-year basis, let's also keep in mind the strong comps growth of 8%, as well as the fact that this 1.3% increase led to a 1.6% contribution to overall growth, which also tells me that these expansions are adding strategic value at the top.

Private Brands

Company Presentation

Another strong growth driver is this familiar big-box strategy , which is working well for Walmex and should be a key driver of future growth, not only in the short term but also over the long haul. In Q3, private label brands' comps grew 11% against an 8% store-wide growth rate, year-over-year, and per CEO Guilherme Loureiro, penetration is now at 15%. Adding 700 new products this year didn't hurt, either, and the total number of private-label products now stands at over 7,000.

There's clearly some notable momentum on this front, and I believe Q4 should see a further bump in growth rates as well as penetration from private brands. Referring back to our study of Walmex's EBITDA profitability, in the absence of any real operating leverage, this initiative will play an important support role in EBITDA growth in Q4 and beyond.

Net Profitability, Cash Flows, and Balance Sheet Health

Revenue growth - and, indeed, EBITDA profitability - is often meaningless unless it's translating into bottom-line profits, and this is particularly important for retailers because of the relatively low margins they tend to have. To offer some perspective, here's a look at historical profit margins in the retail segment so we have something to compare Walmex's performance with.

US Census Bureau, Forrester Analysis

So, we're looking at an industry with sub-4% net margins for the past couple of decades. Let's see how Walmex has performed on that front. It's important to look at liquidity and cash flows as well; with margins this slim, cash flows offer better visibility into how management allocates capital.

EBITDA margin for the first nine months of FY 2023 showed an 8.2% increase on the back of 8.9% revenue growth, both over the prior period. Although there's little to no operating leverage, I think management's been doing a great job filtering more pesos through to the bottom line, which is reflected in net income growing 7.1% over the same period. Net income margins came in at 6.4% for Q3, with the TTM figure at around 5.9%. This is not a one-off performance because that's the level management has been reporting for the past several quarters.

But, once again, I point to a lack of operating leverage. 30 bps of net income margin expansion is what trickled down from a 70 bps increase in gross margins.

Looking at cash flows, cash from operating activities grew nearly 9.5% YoY for the period under discussion. Although the key drivers of that appear to be higher earned interest and higher D&A levels compared to the prior period, it's encouraging to see Walmex's Operating Cash Flow to Net Income Ratio hold relatively steady, dropping slightly from 1.42 to 1.4 over that same period.

There's clearly some pressure on operating efficiency but management has been able to avoid losing any significant ground on that front. Impressive? No. Encouraging? Definitely, considering the retail sector still faces inflationary headwinds in the short term.

This is a positive in my view because the balance sheet is already under pressure from long-term debt and lease liabilities. The current ratio stands at 0.98 in Q3 2023, down from 1.04 in Q3 2022, so Walmex's balance sheet is not as liquid as it was in the year-ago period, and I suspect that it's primarily due to the dividend payout of nearly 13 billion pesos this past quarter. This also impacted their cash position, as mentioned by CFO Paulo Garcia :

"Cash decreased 5.4% compared to 3Q22, mainly due to the first installment of the dividend paid in April."

Overall, the signs are encouraging that management can return value to shareholders despite the tough retail environment. In addition, Walmex's board has given the green light on a relaunch of its 5 billion peso share repurchase program, but it's probably not the best time to be buying back shares when they're trading near 52-week highs. Regardless, I'm cautiously pleased with the company's performance this quarter and I expect some additional gains to be made through Q4 2023.

Now that we know the company is profitable and prudently managing cash despite returning value to shareholders, let's look at it from a valuation perspective based on forward expectations. This is where the story takes a bit of a turn.

Outlook and Valuation

Seeking Alpha

As I said, my outlook for Walmex is somewhat positive, but my optimism is tempered by headwind expectations, not only from high current inflation rates in the holiday quarter but also an appreciating Mexican peso (MXN:USD graph above), which has already caused a hit to revenues in Q3, as stated by management on the earnings call. The outlook is not great either, and if the U.S. Fed starts cutting interest rates in 2024, as predicted by market money makers, it could put further pressure on the top line.

The gist of it is that the Fed plans to issue a "smaller-than-expected" amount of long-term debt, which boosts long-term bond prices because when demand remains the same and supply is tightened, prices tend to move up, thereby lowering the yield, which has an inverse relation to bond price. This Axios article explains it in simple terms.

That also means Walmex is possibly in for a rough ride with respect to currency headwinds, which ties into my not-overly-positive outlook for Q4 2023 and beyond. WMMVY's price-to-forward sales multiple is already high at 1.3 based on full-year 2023 revenue expectations, which is roughly 25% over the sector median of 1.04. Combine that with ongoing headwinds not expected to abate any time soon, and this is not a name I'd risk my money on.

{kind=link}

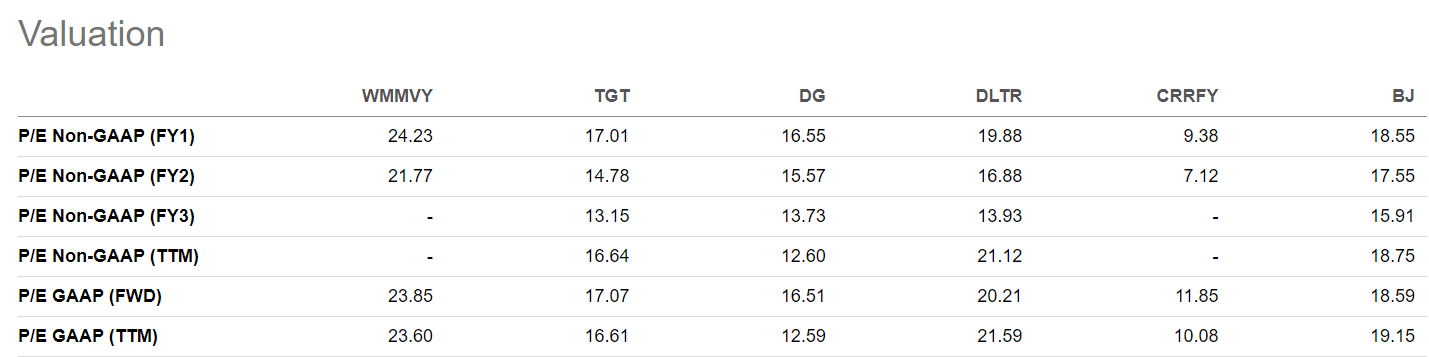

Since Walmex is showing strong earnings growth, projected at over 10% for FY23, it's fair to look at valuation from that perspective as well. Unfortunately, at a price-to-forward earnings estimate of 25x for FY23, it's clear that the stock is on the expensive side from a peer comp perspective.

Another perspective is historical valuations, and the 5-year figure of around 25x tells me this premium is holding up well. The problem is that such valuations are extremely sensitive to reported earnings, and any slowdown on that front could hit the stock price badly; which is not to say that Walmex won't post a stellar Q4 print, but it does oblige the investor to be watchful of any declines in profitability as we navigate a potentially tough FY24.

My Analysis

The twist here is that I'm recommending a Sell for investors who are either at breakeven on their investment or have made handsome returns. The main thesis, however, is a Hold, and that ties into the risk factors I've outlined as well as the unique price action that this stock is subject to after earnings. I'll elaborate on that below.

{kind=link}

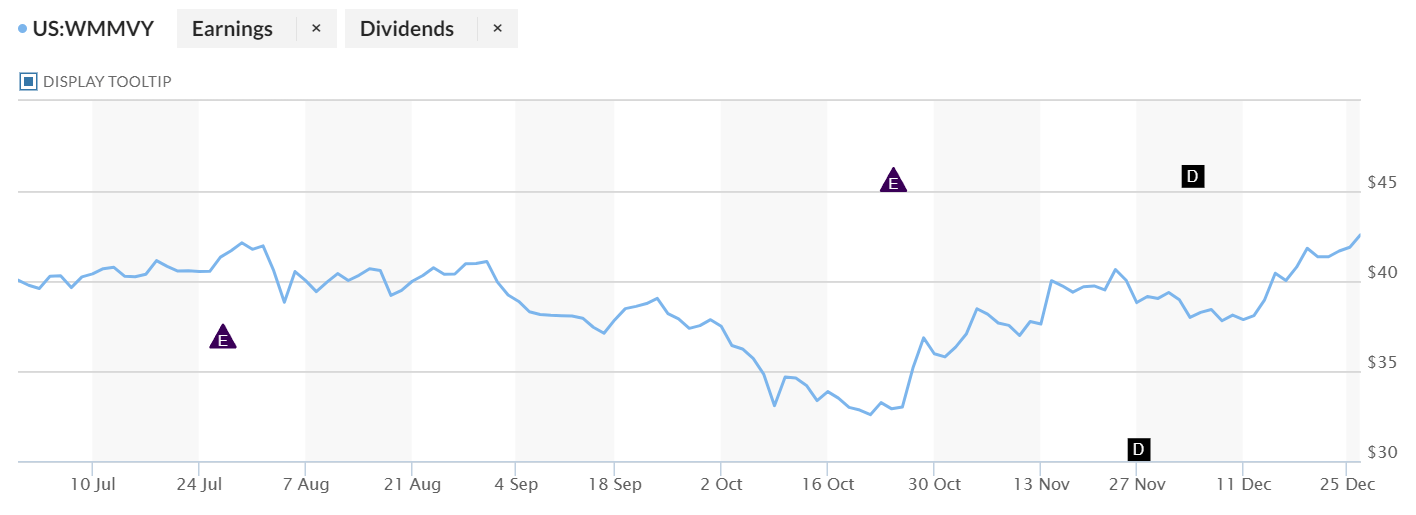

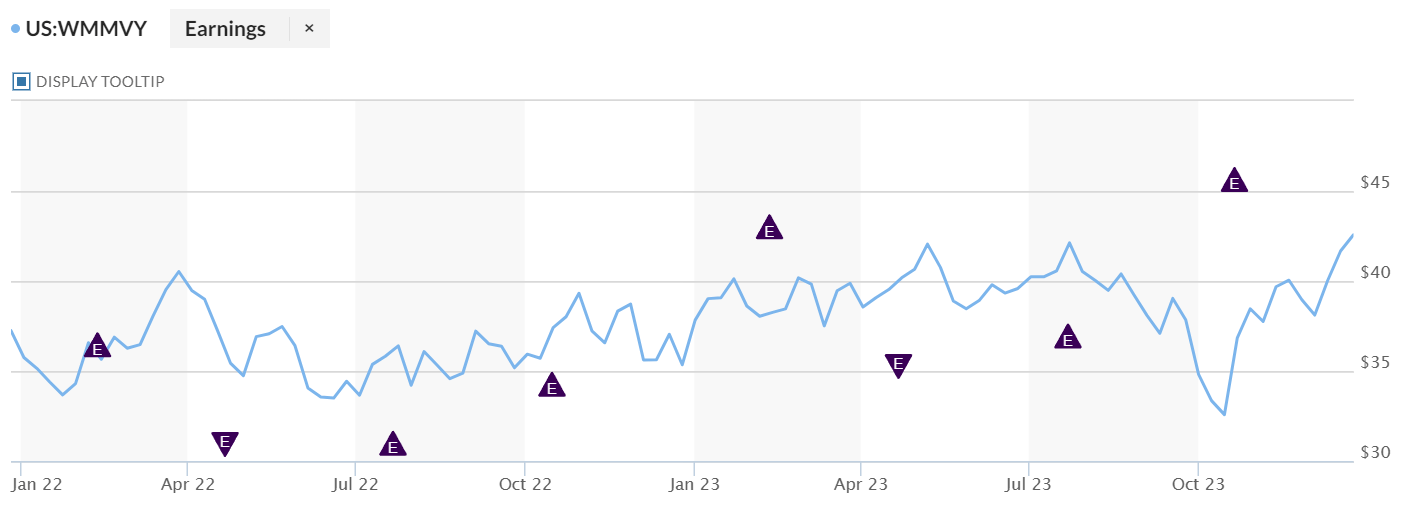

Of note is the fact that market sentiment improved after earnings were announced, and the stock has now clawed back the losses made between July 2023 and now. So, if you're in that breakeven position on a cost basis and the only gains you've made are the dividends, it's probably best to get rid of your position while the stock is on a post-earnings high similar to the one that was seen after the release of Q2 earnings. I'll tell you why.

{kind=link}

My biggest short-term concern around this stock is that post-earnings gains aren't long-lasting. And whenever stocks lose positive momentum soon after an earnings rally, caution is warranted. Let me break it down.

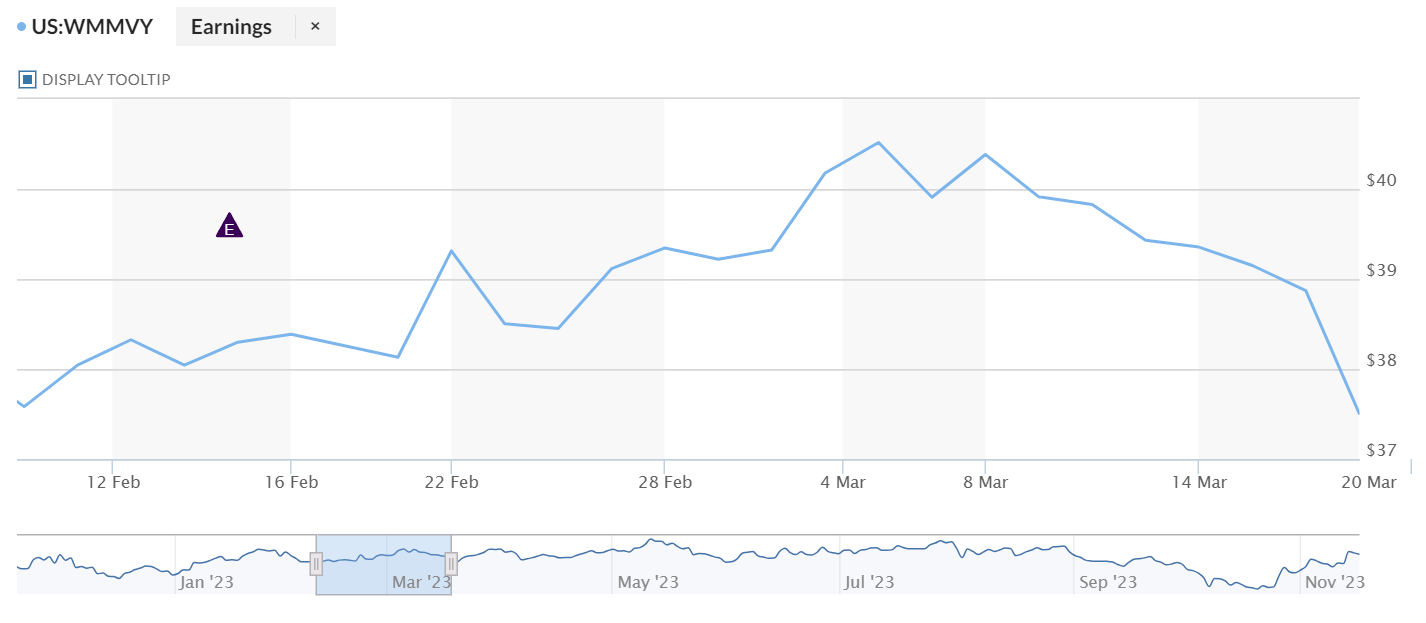

After Q4-22 earnings last year (calendar 2023), the stock rallied for a little under a month before giving back its gains - and then some.

{kind=link}

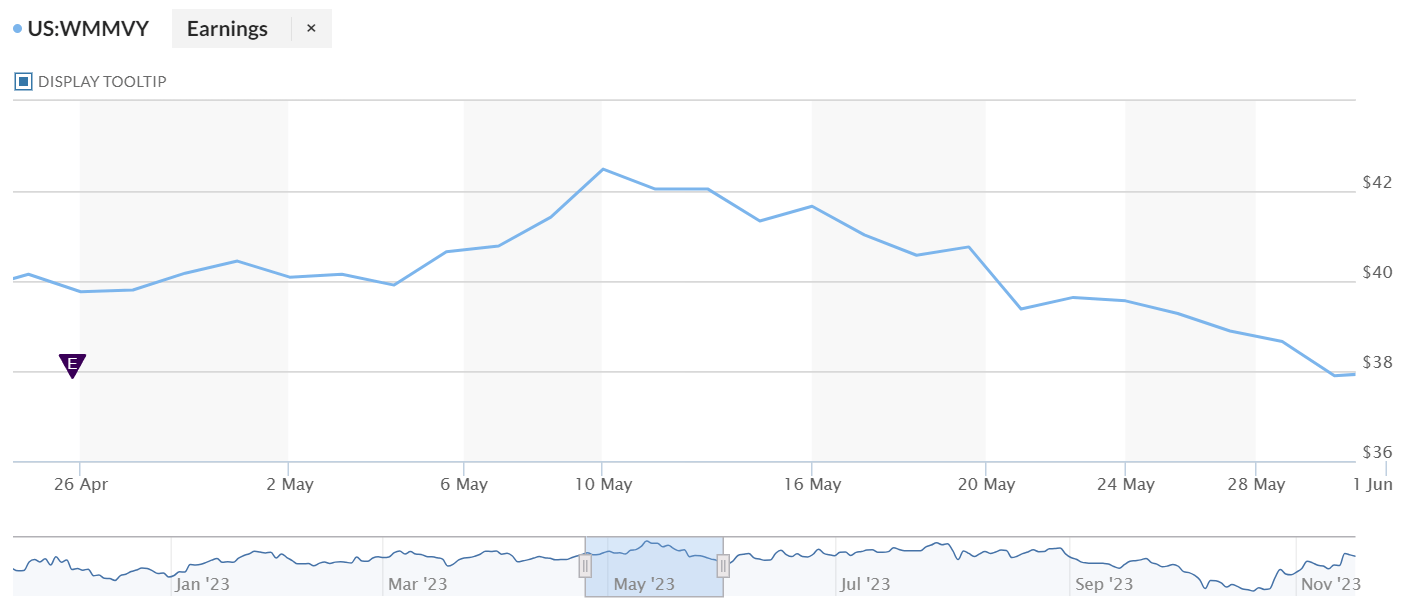

After Q1-23, we see an even shorter rally and a wiping out of those gains - and then some.

{kind=link}

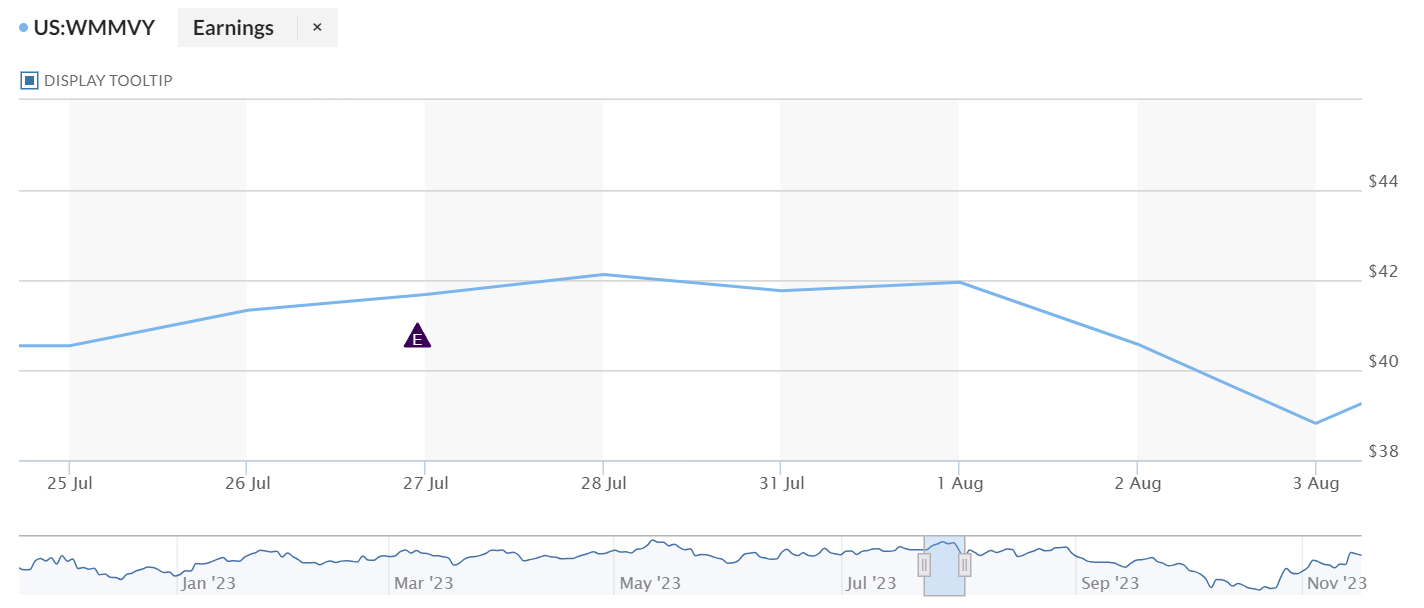

Post Q2-23, there wasn't even a rally, and the stock was down below pre-earnings levels in a matter of a week or so.

{kind=link}

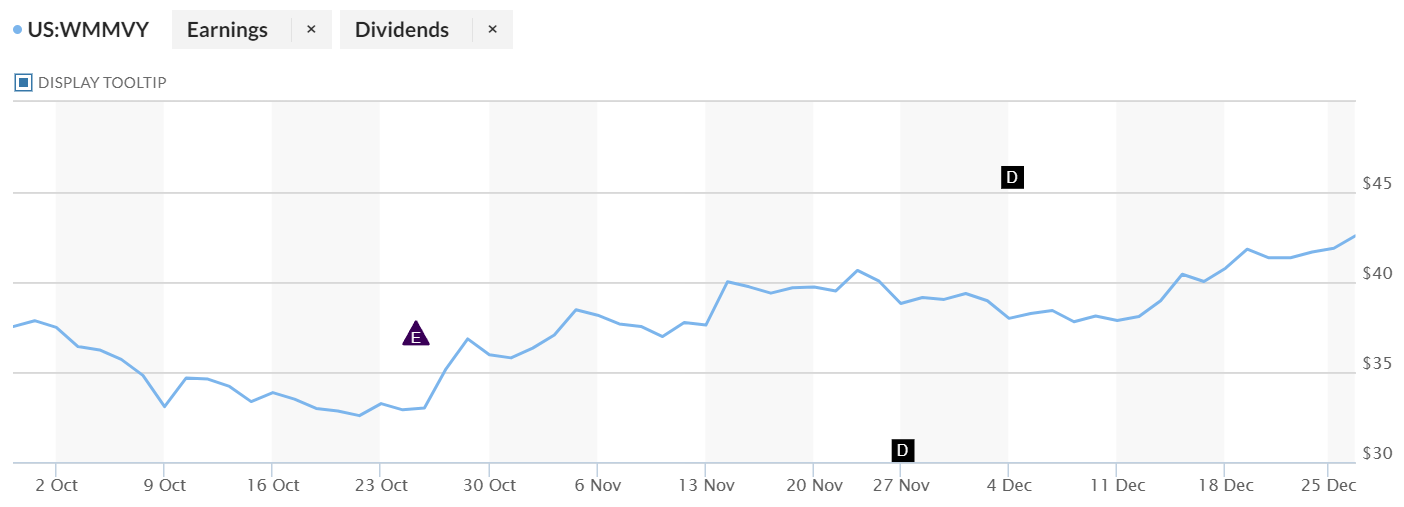

The rallies sometimes last for up to 3 weeks post earnings but there are subsequent sell-offs to offset those gains - and then some. And that's my main concern here as we stand at the end of the fourth and most crucial quarter of the year - the holiday season. The stock seems to have hit a wall right above $42, which could be an indication that this rally is over.

{kind=link}

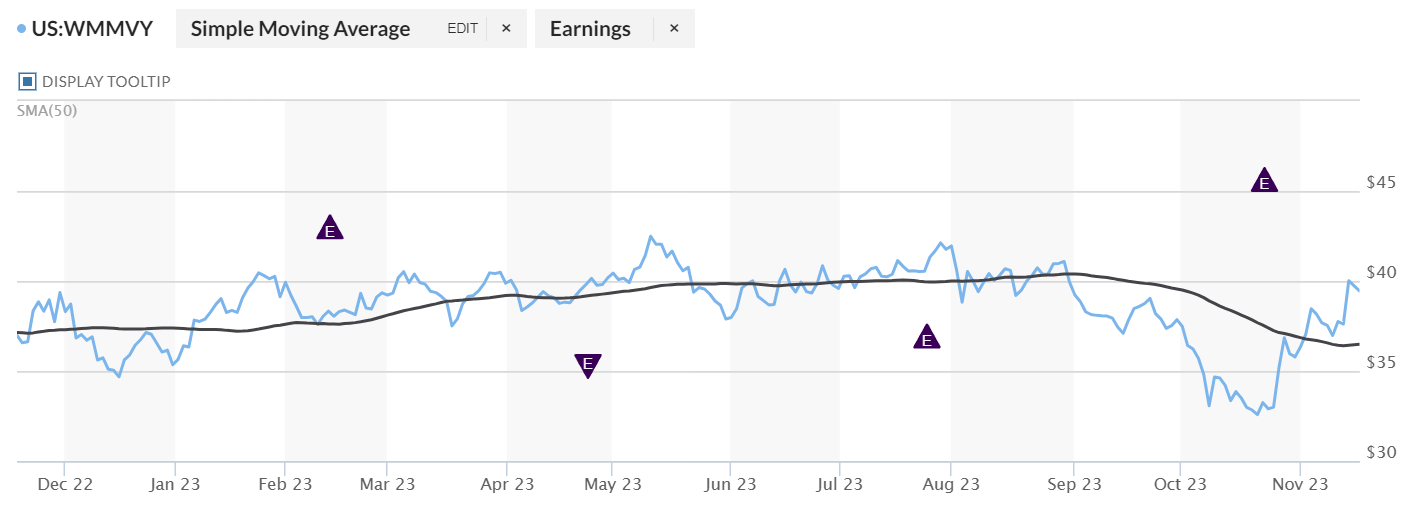

Admittedly, the rally after Q3 has lasted much longer than those of preceding quarters, but that still represents a material risk to any new investments in WMMVY.

If you own Walmex stock, it's probably a good idea to take whatever dividend returns you've made so far and walk away, hopefully with as little capital loss as possible. The stock is a little risky at the moment, and it's probably better to rotate your funds into a more stable and predictable investment vehicle that gives you a higher yield than Walmex's dividends.

Walmex had a great quarter, no doubt. You can see the market lapping it up over the past few weeks since earnings were released. That said, I'm not seeing a very rosy picture in the short to medium term.

{kind=link}

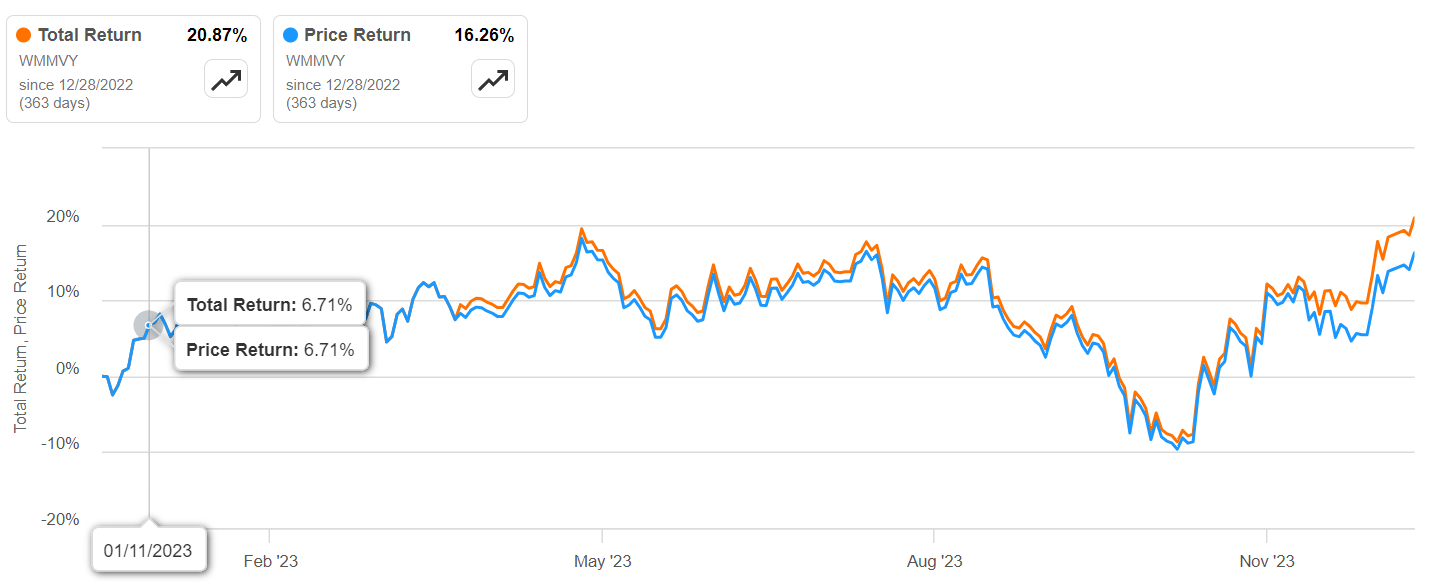

Over the past two years, the stock has had a reasonably good price return of around 16%, with the rest coming from dividends.

{kind=link}

As a relatively new investor sitting at near breakeven with this stock, I'd recommend offloading your holding and calling it quits for now.

I'd also recommend taking some profits off the table if you're an early investor and have enjoyed the kind of capital appreciation that the stock has seen over a longer period. If you bought in at 2005 prices or thereabouts, you've already seen a gain of +400% on your holding for a CAGR of 9.5% for nearly two decades straight.

There's your alpha right there, so liquidating a portion of your holding might be a good idea because it gives you the dry powder you need for more lucrative and less risky investments.

MarketWatch

On the other hand, if you're only a little above water, it's probably best to hold on to the stock. You might go through a price correction based on the high current valuation, but this is not a bad investment, per se; it's just a bad investment at this point in time because of the ongoing and expected headwinds I've outlined here. The upside risk here is that Walmex posts strong Q4 earnings and triggers a rally you might miss out on.

On the other hand, holding the stock long-term at least gives you the chance of future price appreciation, and I'm certain that will happen in the long run because headwinds are never permanent, especially economic ones. The tide has to turn at some point, but you have to be patient, like those investors who now enjoy a +400% return over two decades, or 5 times your initial investment. That's not your real yield, mind you, just the nominal gains. Still, it's market-beating and most certainly a feather in your cap.

In closing, unless you're about breakeven, the best option I can see is to hold for the long haul. Revenue is going up, gross margin gains are countering the lack of operating leverage, and once the headwinds abate, as they must, WMMVY could become a long-term winner in your portfolio. Long-term shareholders have seen this value first-hand, and my analysis tells me this isn't the end of Walmex's growth story regardless of the current macro environment. I'll be back after the Q4 results are announced - if only to see if my thesis bore out.

For further details see:

Wal-Mart De MeXico: Long-Term Hold With Current Headwinds