WMMVF - Wal-Mart de Mexico: Well Equipped To Weather The Cycles

Summary

- Walmex’s latest quarterly result was as good as it gets, given the weakening consumer backdrop.

- Sales growth and margins have been resilient, even with the investment cycle ramping up.

- The stock trades very reasonably relative to its underlying fundamentals.

Q3 2022 was yet another quarter of best-in-class execution from Wal-Mart de Mexico ( OTCQX:WMMVY ) (Walmex), as the company grew through a challenging macro and consumer backdrop. Overall growth this quarter came in well ahead of peers in core Mexico at +40bps above ANTAD (i.e., the industry average compiled by the National Retailers Association of Mexico), helped by solid traffic numbers, price investments, and the penetration of its e-commerce ecosystem. At a ~24x fwd P/E valuation, Walmex offers investors a compelling vehicle to invest in Mexico ahead of a potential downturn, combining a proven management team focused on driving market share gains across brick-and-mortar and e-commerce with robust pricing power through the cycles.

Overall Sales Growth Remains Intact

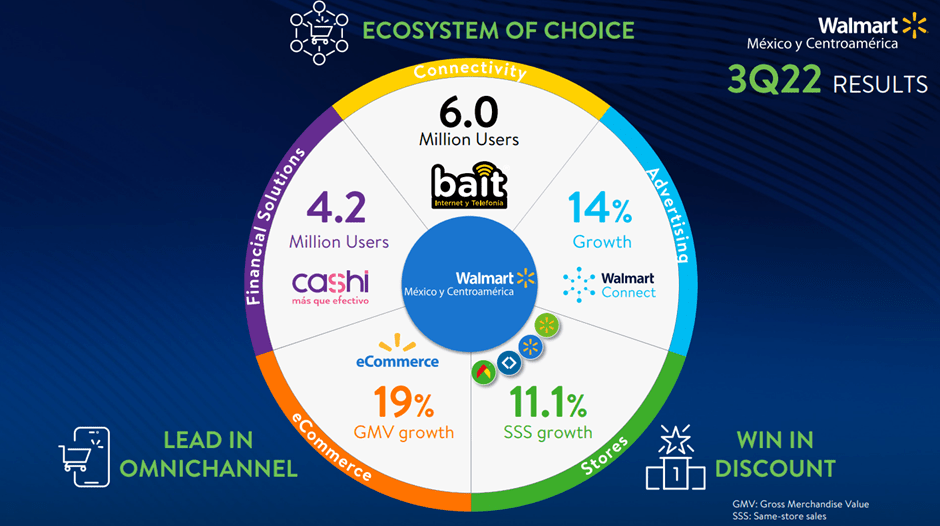

On a consolidated basis, Walmex's revenue growth was impressive at +12% YoY, led by its Mexican operations, which delivered a solid same-store sales growth print of +11% for the quarter (~40bps above the supermarket industry per ANTAD). Underlying the headline sales number was improved traffic, helped by Walmex's strategic investment in widening the pricing gap to peers overall. The +100bps gap also helped Bodega (Walmex's discount format) and Sam's Club outperform. Also boosting growth was Sam's Club's private label offering, Member's Mark, which saw sales penetration rise by an impressive ~290bps YoY to ~20%.

{kind=link}

That said, the weaker consumer backdrop is concerning - per management, customers are trading down, meaning smaller package sizes and more purchase splitting, reflecting the ongoing inflationary pressures. While purchase frequency (i.e., trips) has also increased, the pressure on purchasing power, particularly for low-income customers, is a concern. Yet, management has deployed strategic investments well to offset the impact, capitalizing on seasonal merchandise to drive a strong revenue performance this time around. Back to School sales, for instance, were up ~60% YoY (and ~12% above pre-COVID levels), emphasizing the importance of execution in the current environment.

E-Commerce Growth Pacing Well but Lagging Behind Ambitious Mid-Term Targets

Walmex's e-commerce growth has also been progressing well - this quarter saw a robust ~19% YoY gross merchandise value (GMV) growth, driving a +17% YoY increase in net sales from e-commerce. As a result, Walmex's online penetration currently stands at ~5% of total sales in Mexico for the quarter, contributing ~80bps of overall growth. Key operating metrics have also been trending well, with marketplace sellers up ~20% and SKUs up ~6% on a sequential basis, while ~30% of marketplace orders are now handled by Walmart Fulfillment Services (i.e., Walmex's in-house logistics network). The only hiccup this quarter was a disruption in the transition to a new app technology - while this weighed on online sales this time around, any impact will be transitory and should reverse in the coming quarters.

{kind=link}

On-demand also continues to be a strong point, with the Bodega format emerging as a key growth driver amid the challenging consumer backdrop. The pending roll-out to catchment areas such as the rural Mi Bodega stores is, thus, timely and should also boost overall e-commerce penetration down the line. That said, Walmex's 10% online penetration target by FY24 (as well as to become a co-leader of the Mexican e-commerce market) is some way off, and the company will need to accelerate the pace of growth significantly to get there. Thus, expect a cycle of greater investment spending in the next year, which will weigh on margins alongside the increased contribution from lower-margin e-commerce activity. Incremental income from advertising and ancillary services (e.g., connectivity and financial services), as well as logistics, should help in the meantime.

Margins Pressured Amid Strategic Investment Ramp Up

Walmex still saw ~15bps of expansion at the gross margin level despite a +100bps YoY wider pricing gap to competitors. In particular, supply chain efficiencies and increased contributions from higher-margin income streams such as Walmart Connect (i.e., the merchant media model) more than offset the pressure from its pricing investments. That said, the company also incurred a higher SG&A ratio at +60bps on a ramp-up in strategic investments to support long-term share gains. This led to an ~70bps YoY EBITDA margin contraction on a reported basis (~40bps ex one-offs) despite baseline expenses growing in line with revenue, as the benefits from Walmex's productivity measures (e.g., around employee scheduling) kicked in.

{kind=link}

Besides the investment cycle, which will stretch on through FY24, the government's decision to raise the minimum wage by >20% in early 2022 before implementing further increases in 2023/2024 is a structural margin headwind. On the flip side, the policy will also support the purchasing power of low-income consumers, which Walmex is well-positioned to tap into via Bodega. With the conversion of the Superama format to Walmart Express also on track, the extended store growth runway for Bodega should help as well.

Well-Equipped to Weather the Cycles

In my view, heading into a challenging economic backdrop for Mexican retail, Walmex remains a worthy defensive addition to any portfolio. As highlighted in the Q3 report, the company maintains the pricing power and the scale and efficiency advantages to protect margins and outperform peers (e.g., Soriana and Liverpool) through the cycles. Beyond the near term, investing in omnichannel will be key to unlocking long-term growth, but so will balancing growth investments with profitability and return expectations. Thus far, management has scored well on both fronts, delivering through-cycle EPS growth in the double digits % alongside industry-leading ROICs. The valuation isn't too pricey either at ~24x fwd earnings (relative to >20% through-cycle EPS growth), and I wouldn't be surprised to see a wider relative premium as we enter a more uncertain consumer environment ahead.

For further details see:

Wal-Mart de Mexico: Well Equipped To Weather The Cycles