ABC - Walgreens: Enough Is Enough?

Summary

- WBA stock got hammered yesterday following the release of Q1 FY ‘23 results, although it clawed back some of the loss during today’s market action.

- It is almost a cliche now, but Q1 FY ‘23 results really weren’t that bad, with WBA taking a charge of ($5.7B) to resolve the bulk of its opioid-epidemic litigation.

- Improving pharmacy operations and reduced headwinds from AllianceRx, among other factors, point to a stronger 2H performance.

- The recent sell-off presents a buying opportunity, especially as the US Healthcare segment is expected to turn positive in the back-half of the year.

Enough Is Enough?

After watching its shares sink heading into Q4 FY '22 earnings, Walgreens' ( WBA ) stock posted a good rebound in late 2022, driven in part by subsequent rating upgrades from Deutsche Bank and Cowen , with the firms setting price targets of $50 and $54 respectively.

Figure 1: WBA Stock Price Performance (Yves Sukhu)

Notes:

-

Data as of market close January 5, 2023.

Unfortunately, WBA shares gave back a bit of what they gained following the release of Q1 FY '23 results on January 5, falling ~(6%) to close at $35.19. Although, as I write this, shares are rebounding and up almost ~4%. I have been steadfastly bullish on WBA since I began tracking the company in late 2020. But, with the stock languishing in 2022 and, now, off to a bad start in 2023, is it time for long WBA investors like me to say "enough is enough"?

Post-Mortem: What Went Down in Q1 FY '23

I'll come back to my question in a moment; but first, let's talk about Q1. Putting aside today's decline in the share price, WBA actually beat sales and adjusted earnings estimates for the quarter.

Figure 2: WBA Q1 FY '23 Sales and Non-GAAP Earnings Vs. Estimates (Yves Sukhu/Seeking Alpha)

Notes:

-

WBA Q1 FY '23 sales and non-GAAP earnings estimates from Seeking Alpha .

So, what irked that market following earnings? Well, here are 4 points that certainly didn't help:

-

WBA incurred a non-operating charge of ($5.7B) related to the company's settlement of ongoing opioid-pandemic litigation. The charge drove a GAAP EPS loss of ($4.31).

-

Specialty pharmacy "boat anchor" AllianceRx continues to drag on US segment results, and introduced a (590 bps) US sales headwind during the quarter.

-

Comparable US pharmacy scripts growth, excluding immunizations, was a less-than-stellar 2.1%.

-

The anticipated full FY '23 fiscal year headwind from reduced COVID-19 testing and vaccinations was increased from a range of (15%) - (17%) to (16%) - (18%).

With the points above in mind, the following summarizes some key takeaways from the quarter:

-

Total sales of $33.4B grew 1.1% in constant currency versus Q1 FY '22. Sales growth was 3.2% on a constant currency basis "...excluding the negative impact from AllianceRx Walgreens of 485 basis points and the positive contributions from U.S. Healthcare M&A of 280 basis points." Total sales growth on a comparable basis stood at 3.8%. Readers should keep in mind that top-line growth in Q1 FY '23 came against a particularly tough comp, with WBA still enjoying pandemic-related tailwinds in Q1 FY '22.

-

US Retail/Pharmacy comparable sales grew 3.8% excluding the (590 bps) AllianceRx headwind versus the prior period. Total US Retail/Pharmacy sales of $27.2B declined (3.0%) versus Q1 FY '22.

-

US Retail comparable sales grew 2.1%, excluding tobacco, versus Q1 FY '22 accompanied by improved gross margin. Higher-margin beauty product sales grew 4.9% versus the prior period. Management noted that they saw good gross margin expansion in US Retail during the quarter "...reflecting effective margin management, including strategic pricing and promotional optimization and favorable shrink trends."

-

US Pharmacy comparable sales grew 4.8% versus the prior period, but scripts growth still trails the pre-COVID run-rate. Comparable scripts growth was flat; but, as mentioned above, grew 2.1% excluding immunizations. Despite the latter metric, WBA is still struggling to return to its pre-COVID scripts growth run-rate of ~5%.

-

US Healthcare pro forma sales growth of 38% with $989M in total sales during the quarter. VillageMD, Shields, and CareCentrix grew 49%, 44%, and 22% respectively. To date, VillageMD has nearly 400 operational clinics, with roughly half co-located with WBA stores; and is well on its way to WBA's original goal of 500 to 700 clinics by 2025.

-

International segment sales of $5.2B reflecting growth of 4.6% in constant currency versus the prior period, but significant operating margin headwinds. Boots UK continues to show strength coming out of the depths of the COVID-19 pandemic with comparable sales growing 8.7%. WBA's wholesale business in Germany also contributed to the good international segment performance growing 4.2% versus Q1 FY '22. However, management explained during today's earning call that "[strong] UK retail sales and good operational execution in the Germany wholesale business were offset by lower demand for COVID-19 pharmacy services in the UK, the adverse gross margin impact of NHS pharmacy funding and the expiration of temporary rental reductions received in the prior year. On a combined basis, these three items had an impact of around 27 percentage points [on operating margin performance]."

-

Operating cash flow and free cash flow of $493M and ($117M) respectively versus $1.1B and $645M in Q1 FY '22. WBA CFO James Kehoe noted that "[operating] cash flow was negatively impacted by increased inventories, including successful advance pays to secure product availability in the U.S. and UK holiday seasons" whereas "[the] year-over-year decline in free cash flow was due to lower earnings, some phasing of working capital and increased capital expenditures related to growth initiatives, including the VillageMD footprint expansion, the rollout of micro fulfillment centers and digital and omnichannel investments.

-

GAAP loss of ($3.7B) of ($4.31)/share. GAAP EPS in the prior period was $4.13/share. Note that WBA's Q1 FY '22 GAAP earnings results included a $2.5B after-tax gain on investments in VillageMD and Shields. Further, as mentioned at the outset of this section, Q1 FY '23 GAAP earnings include a ($5.7B) non-operating charge related to WBA's ongoing opioid litigation.

-

Adjusted earnings of $1.0B or $1.16/share. Adjusted EPS in the prior period was $1.68/share. As per management , "[the] year-over-year decline was mainly due to a 19% headwind from COVID-19, U.S. Healthcare growth investments of 5% and labor investments of 5%."

I know readers are probably tired of me saying it, but WBA's Q1 FY '23 results really weren't that bad. That being said, as implied earlier, Q1 FY '23 results did not necessarily point to a generally bullish outlook for the company in the fiscal year. Yet, as Mr. Kehoe explained , "[the] first quarter is traditionally quite weak as a start in the company" and total sales still came in ahead of management's forecast. Moreover, WBA is maintaining their adjusted EPS guide for FY '23 of $4.45/share - $4.65/share; and, they expect core business growth in the range of 8% - 10%. In other words, it would seem that yesterday's sell-off was a tad overdone.

Don't Throw in the Towel

Returning to my question in the introduction and building on the preceding paragraph, I don't think long WBA investors should throw in the towel just yet. Consider:

-

WBA's GAAP loss was driven by the company's ($5.7B) charge to settle opioid-related litigation. As CEO Roz Brewer noted during the earnings call "[WBA reached] an agreement in principle to pay approximately $5.7 billion over 15 years to resolve a substantial majority of [the company's] opioid-related litigation brought by states, political subdivisions, and tribes…[allowing] us to move forward." Hence, while WBA may yet incur additional charges related to the opioid-epidemic, the implication is that the company has taken the "hit" necessary to resolve the majority of pending litigation.

-

AllianceRx has been an ongoing thorn in the side of WBA and WBA investors. As I discussed in a prior article , management has been working to redesign and re-energize is specialty pharmacy business, albeit perhaps not at the rate that investors would like since Mr. Kehoe stated during the Q1 FY '22 earnings call that "[the market will] see us maybe in the next 6 months, come out with a more energized specialty strategy, which will be more integrated in how we surround potential partners with a series of integrated services." That, of course, didn't happen. However, he bluntly offered during yesterday's earnings call that "[this AllianceRx] headwind will stop after December." With WBA completing their acquisition of Shields on December 28, 2022, the expectation is that management should finally be able to present a fresh approach to the specialty market in FY '23.

-

Scripts growth, perhaps the most important metric describing the overall health of the business, has not been where it needs to be. Yet, as readers likely know, management is still working to return its pharmacies to pre-COVID staffing levels. And, management noted that, in those stores with normal pharmacy hours, "[they] are seeing mid-single-digit growth in stores with normal hours." Management explained further that they had a net gain of ~600 pharmacists during the quarter and are steadily improving pharmacy working conditions including enhanced pay, elimination of task-based metrics, and continued rollout of micro-fulfillment centers of which there were 9 operational at quarter-end. Hence, scripts growth in 2H may be far more robust as these activities gain steam.

-

The headwind resulting from reduced COVID-19 testing and vaccinations was forecast for quite some time; although management noted that the ongoing consumer trend that favors at-home testing over (more profitable) drive-thru testing was not fully anticipated and is contributing to the increased headwind forecast for FY '23. Still, investors should not overreact to management's decision to increase the range of the potential impact on EPS. For one thing, as I've argued in the past, WBA has had a tendency to "play it safe" when accounting for COVID-19 tailwinds and headwinds. In other words, they have not overestimated the potential positive impact from tailwinds; nor have they underestimated the potential negative impact from headwinds. Accordingly, investors might take refuge in the idea that management's updated range of (16%) - (18%) might reflect something of a "worst-case" scenario such that investors willing to stick things out through the end of FY '23 might be rewarded by a better-than-anticipated result. And let's not forget that there is another COVID-19 variant (XBB.1.5) that is circulating around now. As I've said so many times now so as to make it seem cliche, wherever we think the pandemic is over, we quickly find out that it is not.

The points above hint toward a much stronger 2H FY '23 versus 1H FY '23. And management, more or less, said that is exactly what investors should expect during yesterday's earnings call, explaining that Q2 FY '23 earnings will be impacted by COVID-19 headwinds, labor investments, and US Healthcare segment spending. However, with the bulk of those investments recorded in 1H, the EPS picture for the second-half of the year is much brighter.

Further, note that the US Healthcare segment is expected to exit FY '23 with a positive EBITDA result as management continues the aggressive pursuit of their healthcare strategy which has been bolstered by completion of the acquisition of Shields (mentioned above), VillageMD's acquisition of Summit Health, and the pending purchase of the remaining stake in CareCentrix expected to close in Q3 FY '23. The Summit deal is expected to be immediately accretive to EPS.

Accordingly, a decision to dump WBA based on Q1 FY '23 results seems a bit unreasonable based on all the signs pointing to a much stronger 2H and the fact that, to reiterate, Q1 FY '23 results really weren't that bad.

Staying the Course

Despite Deutsche Bank's and Cowen's recent bullish ratings, the broader analyst community remains mixed on WBA.

Figure 3: Selected WBA Analyst Ratings (Yves Sukhu/MarketBeat)

Although, sentiment among Seeking Alpha authors is firmly bullish.

Figure 4: Seeking Alpha Author Ratings for WBA (Seeking Alpha)

Along with other SA authors, I continue to recommend the stock as a "buy"; and believe that the recent sell-off provides a buying opportunity with the expectation of a stronger set of second-half results. Management continues to push judiciously toward its vision of rebuilding Walgreens into an integrated-care destination, funding their ambitions (in part) through simplification of the existing portfolio to unlock capital - as with the decision to sell ~$3B worth of AmerisourceBergen ( ABC ) shares in November and December of 2022 to help fund the acquisition of Summit.

Riding the volatility in WBA stock is not much fun as management doubles-down on healthcare.

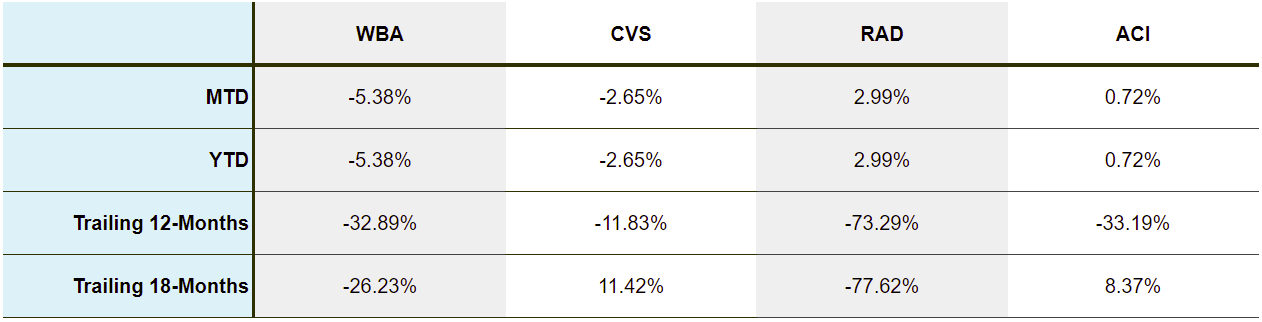

Figure 5: WBA and Selected Competitor Performance (Yves Sukhu)

{kind=link}

Notes:

-

Data as of market close January 5, 2023.

But, so far, they would appear to be doing a good job in terms of execution. And, as I've stated many times before, I admire that they took a very cautious approach with VillageMD in 2020, starting off with just a handful of clinics to prove the concept. That has now grown to several hundred locations around the country - to be complemented by several hundred more specialty-care and urgent care offices via the acquisition of Summit Health. I can't help but feel the stock is routinely punished without fair consideration of the firm's broader direction and strategy. With that in mind, the average analyst target price of $42.50 from Figure 3 suggests shares may hold ~16% upside from the close price of $36.61 as I write this. That in-and-of-itself may not seem too exciting. But, with all the talk of a looming recession in 2023, I think there are far worse places for investors to park their money in 2023 than in WBA, especially with Seeking Alpha currently offering a valuation grade of "A" and the dividend yield hovering around 5.5%. If indeed the market continues to "read" the stock wrong, then, of course, it is merely an opportunity for the rest of us.

For further details see:

Walgreens: Enough Is Enough?