CVS - Walgreens Is Spending Too Much On Primary Care

Summary

- Walgreens' core business is struggling as public and private healthcare payors push for lower healthcare spending.

- Since its troubles began to surface four years ago, WBA has gradually lost its long-term backers, mirrored in the 52% decline in share price.

- The company is spending aggressively on primary care at the expense of the health of its balance sheet.

Investment Thesis

The opioid settlement was a severe setback for Walgreens ( WBA ) and its shareholders in FQ1, costing the company $5.9 billion and leading to an operating loss of $6.2 billion. The blow was hard but anticipated, which, I suppose, makes it a bit easier to swallow.

I am a bit disappointed with management's decision to spread out the ~$5 billion settlement payment over the course of fifteen years. I would have preferred a lump sum that puts the matter to rest once and for all, as Walmart ( WMT ) did for most of its penalty, instead of being reminded of this dark page of WBA's history for the next fifteen years. Nonetheless, I am not surprised by management's choice to seek to optimize the financial impact to the last cent, in line with its pragmatic approach underpinning its every decision.

It is common for retailers to seek efficiency, but management seems to have pushed it a little too far, as mirrored in the state of many of its stores. WBA's position on Brand Finance ranking declined from #8 in 2018 to #13 in 2021.

This streamlined approach to service also touches on its labor shortage headwinds, which I believe have hit Walgreens more than others. How many pharmacy graduates do you know who list WBA as their first career choice? Very few. Most of its stores are operating below their stated minimum staffing levels, which is a great indicator of how broken the chain truly is. Out of its 9,000 stores, a third work reduced hours due to labor shortage.

Equally important is the influence that WBA's standing on Main Street has on its position on Wall Street. WBA's pragmatic approach is met by a pragmatic shareholder base. Since its troubles began to surface four years ago, WBA has gradually lost its long-term backers, mirrored in the 52% decline in share price.

Every time WBA makes headlines, it's for all the wrong reasons: cashier seating backlash, employees murdered on store premises, Medicare fraud , merchandise theft , and tobacco sale to minors , to name just a few. Not a great first impression for a company that wants to be known as "your neighborhood pharmacy."

This means that, as an investor, you might be rubbing shoulders with an opportunistic shareholder base looking to capitalize on a beaten-down stock instead of a loyal base of patrons sharing the company's vision and mission. Once this opportunity expires and shares rise, even if incrementally, everyone will likely jump ship, lowering the share price. For this reason, at least this year, I don't see a significant recovery in WBA's price multiples.

Market Position

In the retail sector, scale is everything. Retailers gain significant competitive advantage through the economics of scale, higher purchasing power with suppliers, and the opportunity to assume the role of price leader. As the second-largest drug chain in the US by revenue, WBA gains a significant advantage through its size, which is why management and investors are panicking over WBA's market share decline in recent years. The table below shows 30-day equivalent drug sales growth in the past three years.

| Prescription Drug Sales |

| Ticker |

| 2022 |

| 2021 |

| 2020 |

| 2019 |

| Walgreens |

| ( WBA ) |

| $ 1,216.4 |

| $ 1,210.6 |

| $ 1,165.3 |

| $ 1,150.1 |

| % Change |

| 0.5% |

| 3.9% |

| 1.3% |

| CVS Health |

| ( CVS ) |

| $ 1,623.8 |

| $ 1,587.60 |

| $ 1,465.2 |

| $ 1,417.2 |

| % Change |

| 2.3% |

| 8.4% |

| 3.4% |

The restructuring plans, which saw the closure of unprofitable branches, might have marginally increased profitability, but their favorable impact on competitors was even more. Customers of a closed store will invariably switch to another outlet nearby. One can't ignore price pressure resulting from regulatory dynamics impacting Medicare and Medicaid reimbursement rates, as well as regulatory interventions in the pricing of drugs. Thus, while WBA is a defensive stock with revenue characterized by inelastic demand, margin stability is not a given. The impact of these trends is amplified, given the industry's maturity.

In the recent quarter, management emphasized its strategy to increase engagement and bring some fresh air to its stores, and have recently rolled out the My Walgreens royalty program and other initiatives to deliver "Store Optimization" and "Transformational Cost Management Program." I remain skeptical about these initiatives, and these buzzwords only mirror the panic at WBA's headquarters to stabilize its core business.

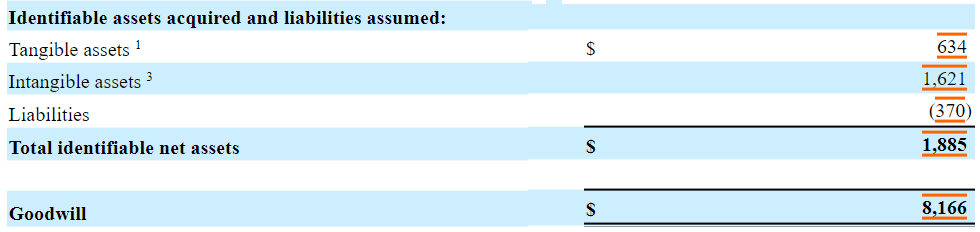

WBA is also under pressure to deliver growth and has found an opportunity in the primary care market, which is fine, given the continued regulatory support and industry leaders' consensus over the importance of primary and preventive care as a tool to lower national healthcare spending. However, I find it difficult to understand the aggressive pursuit of multi-billion dollar acquisition deals, such as Village MD (and WP CityMD), Care Centrix, and Shields. Healthcare clinics are not a capital-intensive business. The most expensive asset is the physician, which begs the question, why are all these billions spent and recorded as "intangible assets" on a company's balance sheets? Why doesn't WBA build its primary care network, starting slow and gradually building its reputation? If it has what it takes to run a primary care business, it will eventually build a customer base with a fraction of the price it is currently paying. Below is a chart showing Goodwill and Intangible asset progression over the years.

Last year, WBA increased its share in Village MD to 63%, up from 30%, for 5.2 billion, valuing MD at $15 billion. Since then, WBA has boarded new investors, diluting its share to 53%. Nonetheless, looking closer at the asset composition of Village MD, we see that Identifiable Assets, whether Tangible or Intangible, is a mere $1.9 million, with the remaining flushed into the Goodwill account.

{kind=link}

Village MD Assets ((WBA))

Rating agencies are unhappy about WBA's spending spree on primary care, funded mainly by new debt issuance but also through the sale of terrific pieces of business, including Alliance Healthcare's sale to AmerisourceBergen ( ABC ). While the sale generated a nice sum, from a portfolio point of view, it replaced a cash cow with ten birds on a tree.

Summary

WBA is far from a thriving business, but it is good enough as a defensive buy for investors looking for a haven from the market turmoil. The company has a low valuation at only an 8x P/E ratio, with a defensive business model underpinned by inelastic demand for healthcare products. However, there is no reason it should outperform the market over the long run. The company faces significant headwinds from increased drug price regulation and declining profit margins. At this point, I believe its shareholder base consists of opportunistic investors aggressively pushing management to expand in new growth initiatives to bank on price volatility. This is not a company with a long-term moat, and it will take a lot of work to overcome the challenges in front of it.

For further details see:

Walgreens Is Spending Too Much On Primary Care